Thuchaphol Chaiyakal/iStock via Getty Images

Cohen & Steers REIT and Preferred and Income Fund (NYSE:RNP) last paid out $0.136 as a monthly distribution for a 7.4% yield that should help form a backstop for any income portfolio. There are a number of reasons to be bullish here, albeit only partially countered by some risks that still do not sway the overall investment thesis. RNP, as the name infers, invests in a basket of REITs and preferred shares. The CEF has essentially formed its holdings from the largest and most stable REITs which all come from a range of sectors.

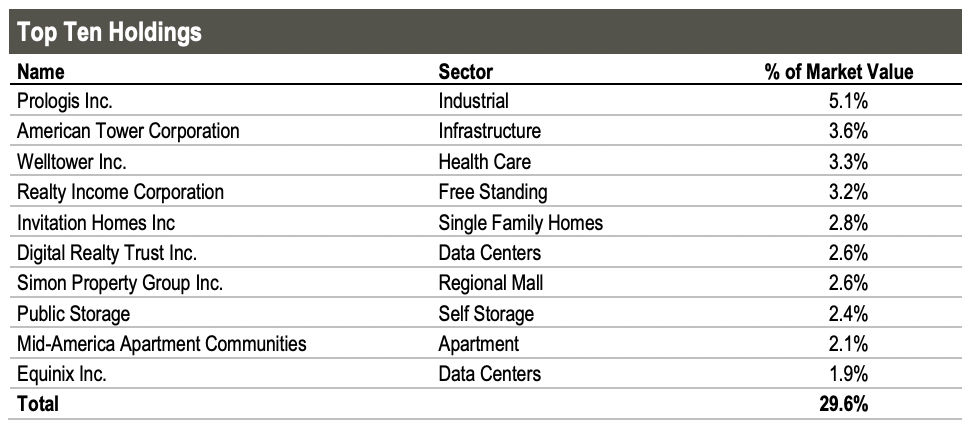

Cohen & Steers REIT and Preferred and Income Fund

This ranges from American Tower (AMT), an owner and operator of wireless and broadcast communications infrastructure to Equinix (EQIX), the largest data centre and colocation provider for enterprise network and cloud computing in the world. RNP manages around $1.41 billion in assets and currently holds around 289 positions as of its most recent quarter ending December 31, 2022.

Critically, the payout and its safety are what matters for any RNP income investor. This factor is especially acute against inflation running at multi-decade highs and the creeping specter of a recession. RNP represents an intensely defensive positioning with half of its portfolio formed from preferred shares and the other half from high-quality REITs. These are set to shield the CEF from broader economic volatility expected this year.

Cohen & Steers REIT and Preferred and Income Fund

RNP’s top four sectors; Industrial, Infrastructure, Apartment, and Health Care, can be thought of as broadly recession resistant. These REITs own assets whose tenants are not strongly as reactionary to periods of negative economic growth as the more sensitive consumer discretionary sector. Most of the coming economic risk would likely centre on Regional Mall which just forms 5% of the REIT portfolio.

Cohen & Steers REIT and Preferred and Income Fund

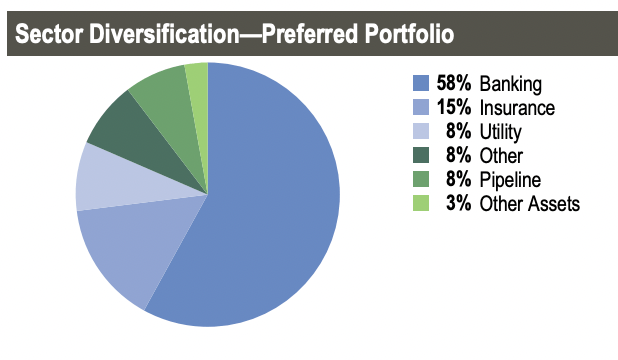

Preferred shares are an asset class that investors seldom have exposure to. They rank higher on the dividend totem pole than common shares and offer a bond-like security with regular distributions and maturity events which is when the issuer is obliged to buy them back. The bulk of RNP’s preferreds, around 58%, are from banking companies with another 18% from insurance companies. Banks have been recording record earnings on the back of fast-expanding net interest income amidst the rising interest rate environment.

Discount To NAV, No Return of Capital, And Stability

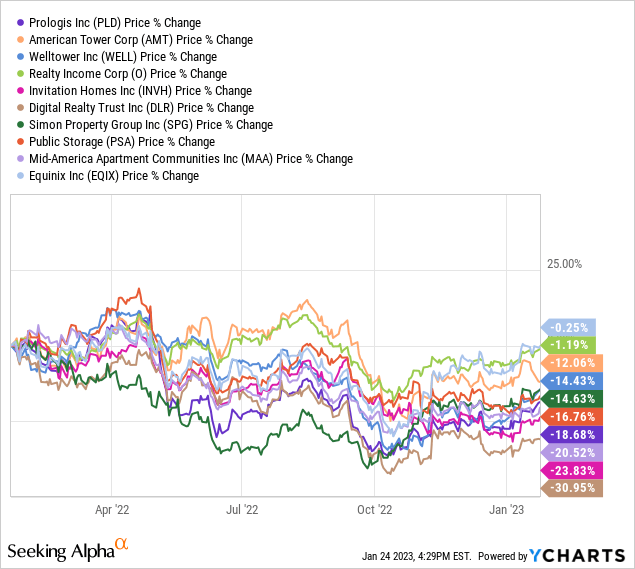

REITs have trended down over the last 12 months in response to interest rates that moved to their highest level since 2007. The Fed fund rate currently sits at 4.25% to 4.5% following a 50 basis point hike last month. This is important for RNP as the CEF’s distributions are formed from four sources; dividend income, short-term capital gains, long-term capital gains, and return of capital.

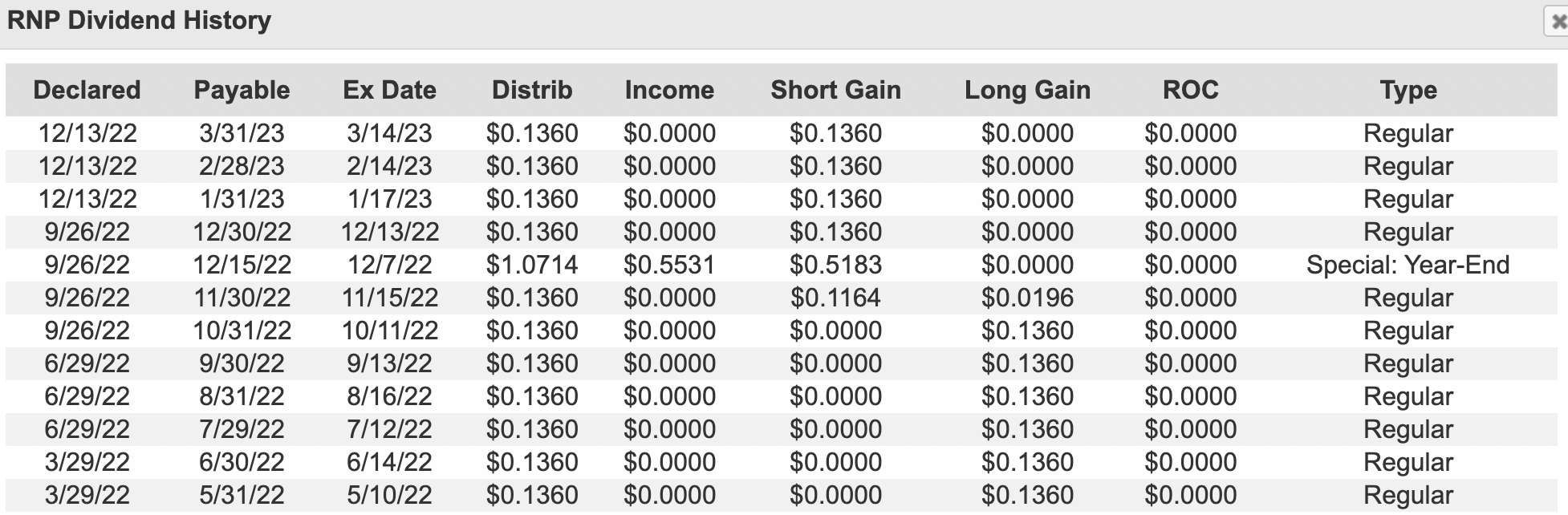

CEFConnect

Most of the distributions for the last 12 months have been paid out from capital gains, with the CEF having to lean on short-term gains, positions held for less than a year, for its most recent distributions. This forms a risk to the distribution rate as capital gains are more volatile against a market that’s retrenching. The US economy is widely expected to fall into a recession later this year and interest rates continue to rise with inflation only set to fall to the 2% Fed target towards the second half of 2023. REITs will likely experience more volatility this year which would increase the uncertainty of using short-term capital gains for distributions.

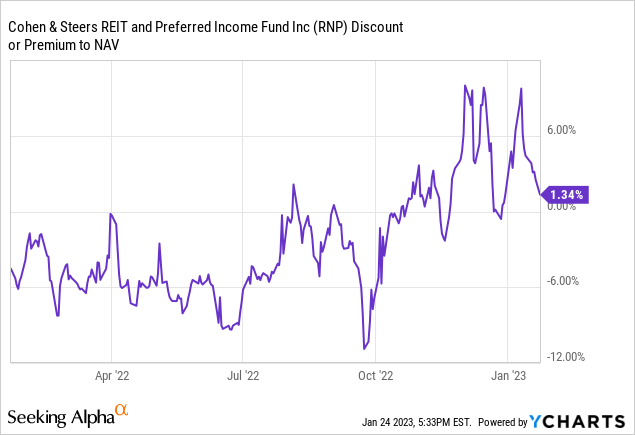

RNP currently trades on a 1.34% premium to its net asset value, which whilst low, is at a divergence to its average 3-year discount of 4.54%. The CEF’s premium has fallen in recent weeks as REITs staged a strong rally to start off the new year. Whilst the risk here is of course a return to mean, a stable income is what matters for RNP’s investors.

Scope For Return Of Capital To Come Into Play

RNP is managed with 30% leverage and had a relatively low portfolio turnover of 21% as of its most recent semi-annual report ending June 30, 2022. The CEF reported a total investment income of $30.09 million, this was mainly formed of $15.86 million in interest income and $13.9 million in dividend income.

Cohen & Steers REIT and Preferred and Income Fund

With a net investment income of $19.32 million for the period against $38.66 million in distributions paid, the CEF suffered a shortfall that was only plugged by capital gains. This potentially sets the tone for return of capital to be used if capital gains are insufficient to meet future distributions. Whilst RNP’s portfolio looks robust from an investability perspective especially going into a recession, the health of its distributions is uncertain as the CEF stares down more economic volatility this year. Return of capital is not inherently bad, especially from an equity perspective, but the current shortfall creates uncertainty. Hence, I’m neutral on RNP.

Be the first to comment