damircudic

A wise man gets more use from his enemies than a fool from his friends.”― Baltasar Gracian

Today, we put a small Israeli-based tech concern called Riskified Ltd. (NYSE:RSKD) in the spotlight for the first time. The company came public at the tail end of the IPO/SPAC craze that ran from the second half of 2020 throughout the summer of 2021. Powered in a large part by very accommodative policies from the Federal Reserve and a consequent 40% increase in the money supply over two years, most equities that debuted on the market from this ‘vintage‘ have destroyed a huge amount of shareholder value. The shares of Riskified are no exception. Has the equity finally fallen enough to be considered in the ‘bargain bin‘? An analysis follows below.

Seeking Alpha

Company Overview:

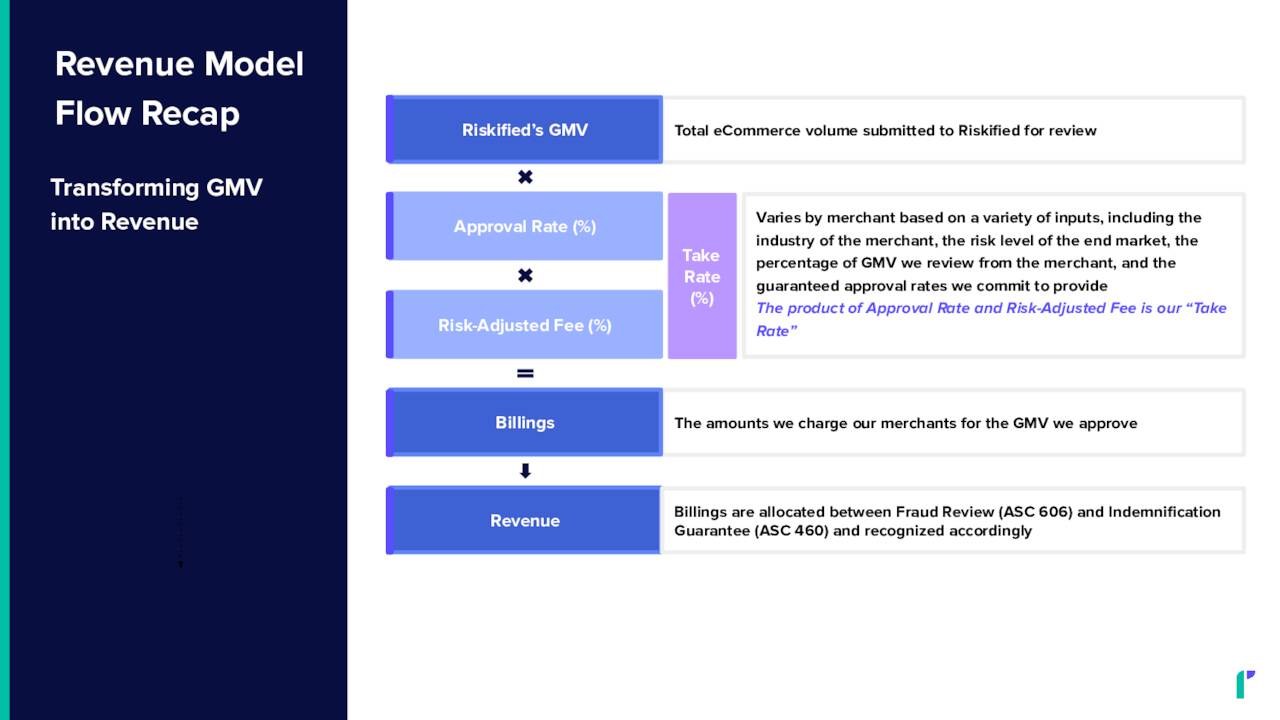

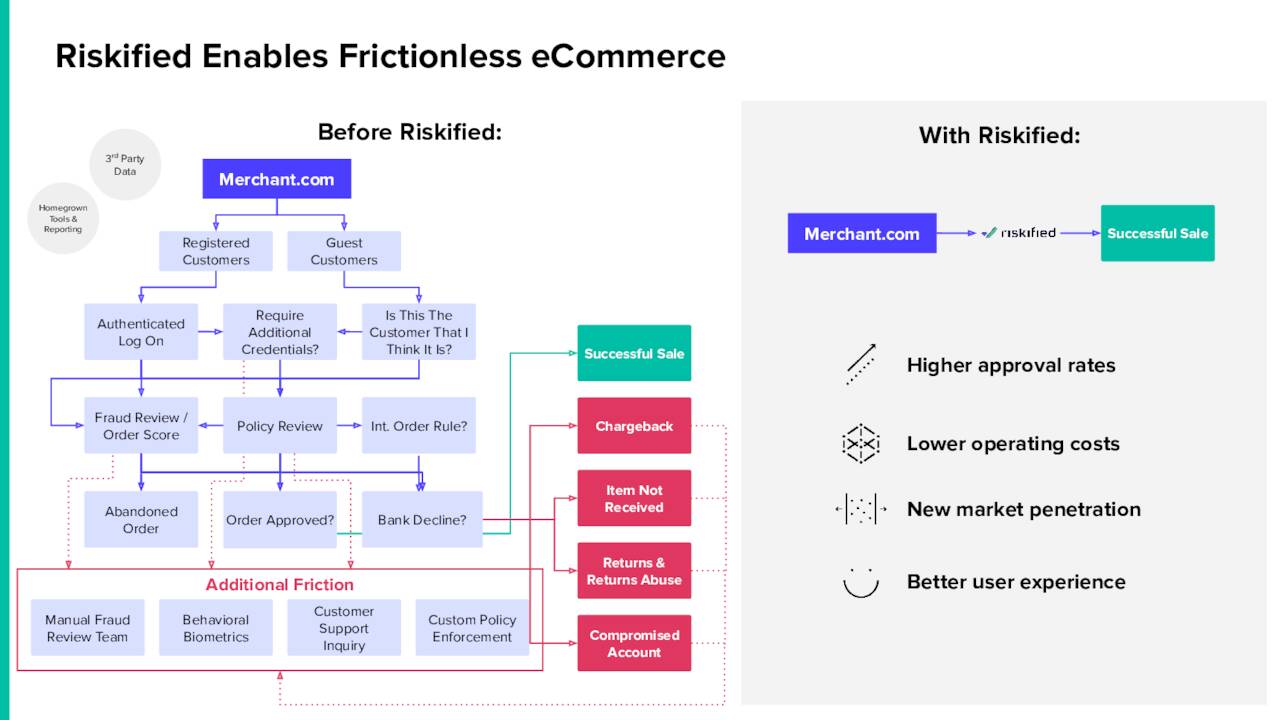

Riskified Ltd. is based in Tel Aviv, Israel. The company has developed and provides a risk management platform that delivers frictionless eCommerce capabilities to online merchants.

November Company Presentation

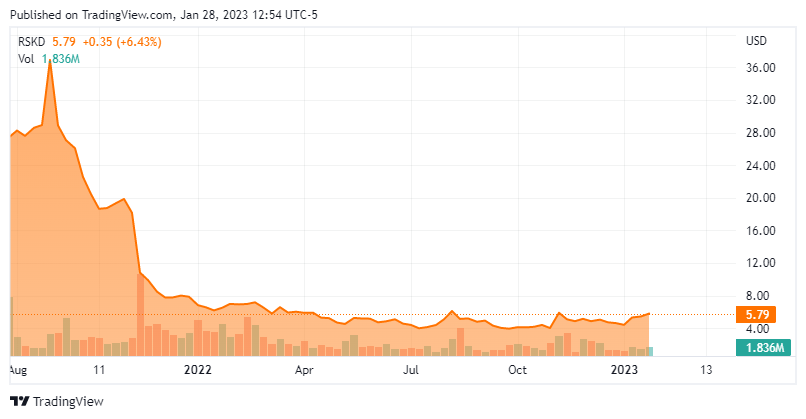

The company has a strong footprint in the tickets and travel ecommerce space. Approximately, 30% of Riskified’s business comes from tickets, travel and events. The stock trades just under six bucks a share and sports an approximate market capitalization just south of $1 billion.

November Company Presentation

Third Quarter Results:

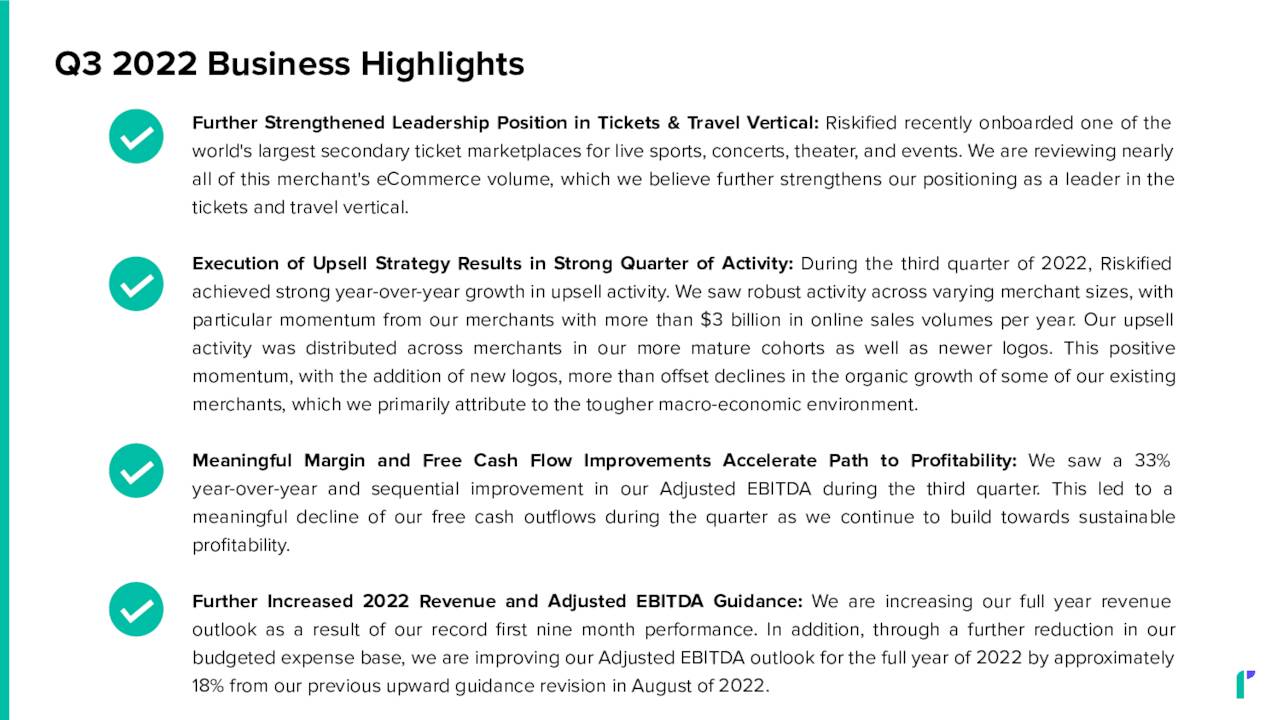

On November 9th, Riskified posted its third quarter numbers. The company had a non-GAAP loss of a nickel a share, 11 cents above expectations. Revenues rose just over 20% on a year-over-year basis to just over $63 million, approximately $4 million over the consensus. Revenues were negatively impacted by four percent by a strong dollar during the quarter.

November Company Presentation

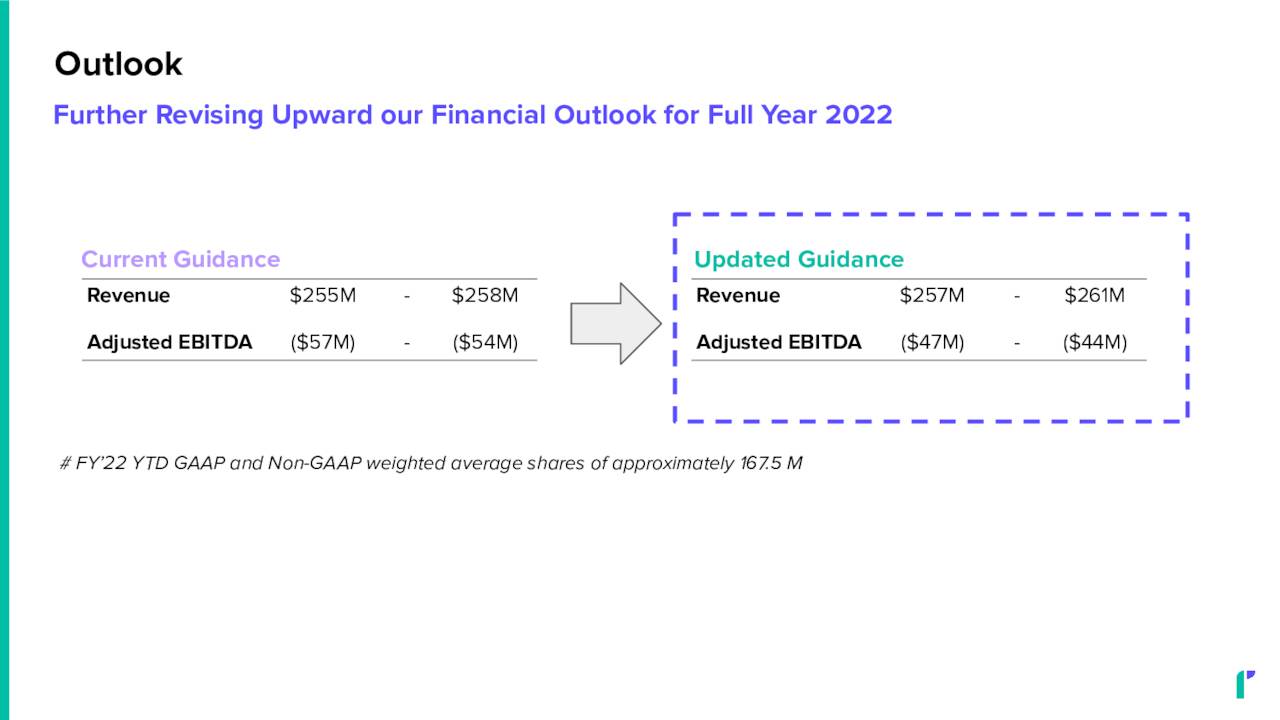

Leadership bumped up FY2022 revenue guidance slightly to a range of $257 million and $261 million. Management also reduced its forecast for adjusted EBITDA loss for the fiscal year to $44 million to $47 million from previously forecast calling for an adjusted EBITDA loss in FY2022 of $54 million to $57 million. The positive $10 million adjustment was primarily the result of a decrease in budgeted expense base. Riskified’s adjustment EBITDA loss also improve 33% in the third quarter compared with 3Q2021 it should be noted. Non-GAAP gross profit margin also rose to 52% from 47% in the same period a year ago. Finally, free cash flow was a negative $4 million in the quarter, a 75% improvement on a year-over-year basis.

November Company Presentation

Analyst Commentary & Balance Sheet:

Opinion in the analyst community has been mixed since third quarter results came out despite the company beating quarterly expectations and raising guidance. Both Credit Suisse (CS) ($9 price target) and Barclays (BCS) ($7 price target) maintain Buys on the stock. KeyBanc downgraded RSKD to a Hold while JPMorgan (JPM) reissued its Neutral rating and lowered its price target a buck a share to $6. Finally, Goldman Sachs (GS) upgraded the equity to a Neutral from a Sell noting:

The company has likely gone through its “trough” growth period and that revenue growth is likely to accelerate in the coming year and they expect Riskified’s EBITDA margins to inflect higher this year, driven by the company’s “strong” cost control measures and the lapping of what was a heavy investment year in 2022.”

That said, Goldman currently has a tepid $5 current price target on RSKD. Just over two percent of the outstanding float in the stock is currently held short. The company ended the third quarter with just over $480 million in cash and marketable securities against no long-term debt.

Verdict:

The current analyst firm consensus is that Riskified will lose just over a quarter a share in FY2022 even as revenues rise to in the low teens to nearly $260 million. The consensus has the same earnings outcome penciled in for FY2023 even as sales grow in the high teens. It should be noted there is a wide variance of profit estimates for the next fiscal year, ranging from a 7 to 66 cent a share loss.

It is hard to find stellar reasons right now to buy the dip in Riskified other than its fortress balance sheet. Sales growth is also solid and the third quarter did bring improvements in some key metrics. The company has little in the way of positive analyst coverage despite solid third quarter results and it is likely the company remains unprofitable over the near and medium term horizon.

Most analyst firms also project a significant slowdown in ecommerce spending in 2023, which would likely be a headwind to Riskified. Finally, I have also not done well with Israeli small caps over the years, RedHill Biopharma (RDHL) being one prima facie example. Therefore, until Riskified gains additional traction getting into the black on the earnings front, I have no investment recommendation around the stock.

When you surround an army, leave an outlet free. Do not press a desperate foe too hard.”― Sun Tzu, The Art of War

Be the first to comment