recep-bg/E+ via Getty Images

Antero Resources (NYSE:AR), a natural gas [NG] producer with pristine resources, made an about face during the last conference call. On the surface, this change of face might seem uneventful, but closer inspections yield otherwise. Companies generating inordinate levels of cash do run out of drab scenery and places to spend money. That time might be or most likely is coming sooner than investors think. When that happens, the next about face is more likely yields, lucrative yields; something worth watching through the glass windows of travel.

Spending for High Cash Flow Generators & Resources

Companies generating high levels of cash often find three or four ways to use it: repair bloated balance sheets by buying back debt, lower stock counts, pay distributions, or purchase new assets either through internal capital or direct purchase. At Resources’ last conference, management announced the balance sheet, repaired, while adding a billion dollars to the already billion dollar stock repurchase authorization. This about face clearly focuses on lowering shares of stock placing the company’s spending focused at the second type. Now, the most important question becomes, for how long? A second, which phase is next? We hope to provide logical answers as we watch the scenery pass. But, first, let’s figure out the cash for the next few years.

The 3rd Quarter and YTD Results

When management reported 3rd quarter results, they spent most of the call discussing its use of cash. In particular, they stated and shown in the next slide:

- A purchase of 22 million shares.

- Total share counts equals 300 million as of Oct. 21, 2022.

- A purchase of over $400 in debt.

- Total debt now equals slightly more than a billion.

Antero Resources

The next slide shows management’s then belief in cash flow going forward.

Antero Resources

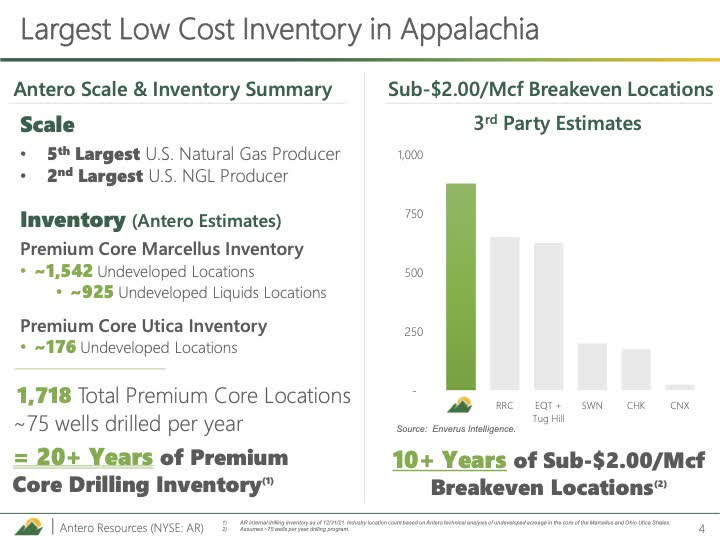

The balance of the presentation and call focused on key advantages held by Resources. Summarized in slides following, the advantages include location, types of wells and other resources plus markets. The first illustrates the cost for its inventory in the Appalachia.

Antero Resources

Adding depth, management noted that:

by the amount of Marcellus inventory that they have with breakeven cost below $2 per Mcf. As you can see, Antero has the greatest amount of low-cost inventory in the basin, more than 800 future locations which will continue to drive our consistent performance well into the future.”

The next slide shows the transportation cost advantage.

Antero Resources

Adding even more depth, the company’s cost advantage with respect to Henry Hub equals $0.50.

Also announced was an increase to its share repurchase bringing the total to $2 billion. The goal continues at reducing debt where possible, but now it’s mostly about repurchasing shares.

On the issue of capital or other purchase, management’s approach adds properties in smaller parcels. It is their belief that this approach yields much lower total costs.

The Conflict

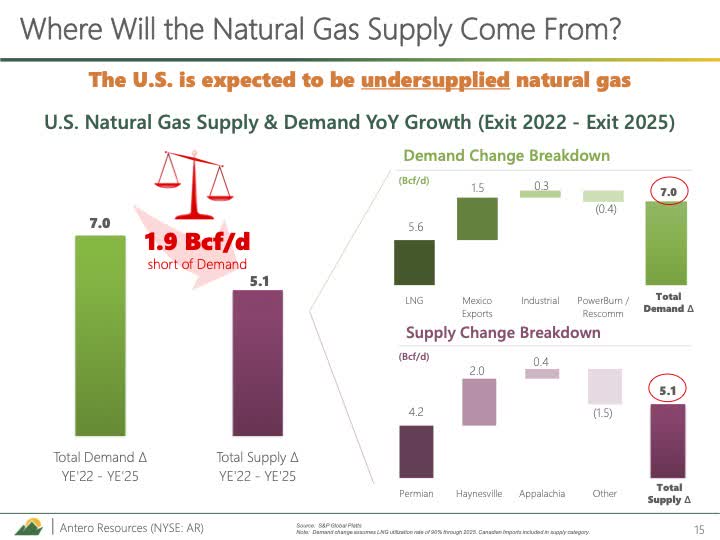

Resources believes that NG production is headed into a short supply with details shown in the next slide.

Antero Resources

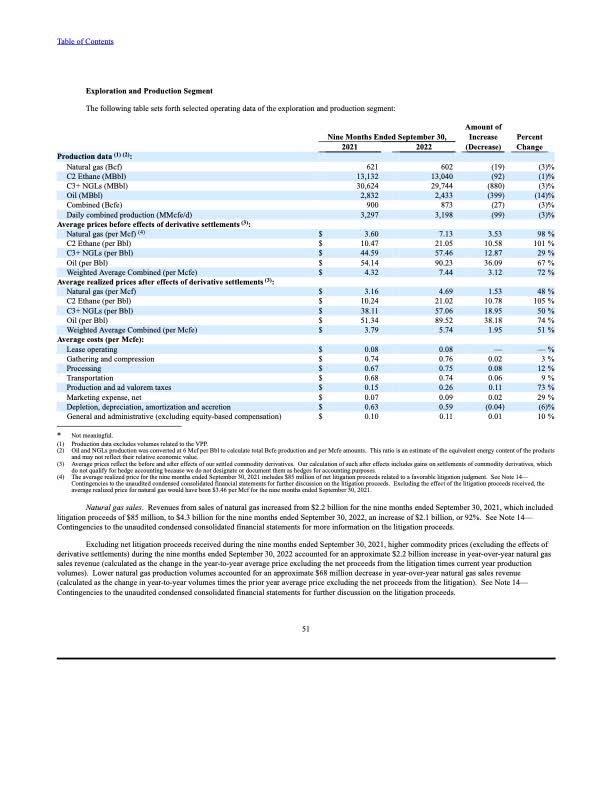

As stated above, the company believes that cash flow for 23 will be similar to 22. Driving that belief is the fact the most egregious derivative, its overriding royalty interest agreement, signed in 2020, rolls completely off through the early part of 2023. The effects of this agreement plus the lessor 2nd derivative can be seen in the quarterly report table.

Antero Resources

The average price for the nine months before the derivatives, $7.13, is steeply discounted vs. the $4.69 after. A second derivative, VVP, amounts to approximately 3%-4% (75 MMcf/d) the total production. The VVP completely rolls off in 2027. The idea of $5 average NG pricing for 2023 seems a necessity for reaching goals in the presentation. A statement similar to this, “Next year on $5 gas,. . .” showed up several times. Thus we assume that the $2 billion in free cash flow is based on this belief.

Now the contrary story. The EIA wrote, “Continued increases in U.S. dry natural gas production are expected to outpace domestic demand and exports this year and in 2024 according to the EIA.” But also added, “The return of Freeport LNG after a fire in June 2022 will also drive higher natural gas demand in the first quarter, . .” Warm weather particularly in the east is driving gas usage down leaving inventories slightly above the five-year average. Analysts at Tudor, Pickering, Holt & Co. commented:

January degree day totals were set to come in 16% below the five-year average even after increasing week/week, while early February forecasts were pointing to degree days coming in 4% shy of the five-year, according to the firm’s estimates as of early Friday.

The national average for the week of January 20th averaged $4.82 down significantly over the week before. NG benchmark shown at Oilprice now equals less than $3.0. Henry Hub prices, a key for determining Antero’s numbers, are higher than benchmark with a recent prices at $3.35. Again, remember that Resources’ transportation advantage adds $0.50. The issue for weak NG resides with robust production coupled with very unseasonal winter weather in North America and Europe. One analysts states his expectation for this issue to continue into 2024 or longer. Antero’s management obviously disagreed. It remains to be seen who’s correct.

Competition from Other Regions for 2023

Continuing, management noted:

we expect regional basis differentials in Appalachia, the Permian Basin and the Haynesville to remain wide with deeper discounts due to the pipeline capacity constraints. In the Permian, we do not expect basis improvement or meaningful supply growth reaching markets until the third quarter of 2023 . . . The Haynesville is in a similar constrained position over the next nine to 12 months as it awaits incremental pipeline capacity.”

Running Out of Ways to Spend Cash

For companies generating huge cash flows, places to spend disappear. With the company basing its 2023 cash flow estimate at $5.0 NG average and with prices significantly under that price, cash flow estimates might be significantly lower. In the above figure generated from the last 10-Q, the company noted an average of $3.1 for nine-months in 2021. The free cash flow equaled $1400 million for the year. The result came by adding all the free cash flow numbers from the individual quarterly press release found at Seeking Alpha. The next table helps place timing on when that might happen using the base of $1400 million and estimating higher returns should NG return to higher prices.

| CF Use | Cash Flow Case 1 | Cash Flow Case 2 | Cash Flow Case 3 |

| NG Price | $3.1 | $4.0 | $5.0 |

| Cash Flow Estimate (yearly result) | $1400 | $1700 | $2000 |

| Stock Price | $35 * | $37.5 | $40 |

| Shares Purchased (Millions) | 40 | 45 | 50 |

* Assumed a higher stock price with higher NG pricing.

With 300 million shares and further without debt reduction, Resources will have 250 million shares at the end of 2023 and significantly less than 200 million shares by the end of 2024. The question becomes how much stock is too much and how much is too little? It appears to us that somewhere between the middle of 2024 and into 2025, scenery changes forcing the company to make another about face. But before we continue, Michael Kennedy, Resources CFO, stated, “No. We try not to stockpile cash.” Cash generated will be spent some way. At 200 million minus shares, $2 billion in free cash flow generates $10 a share with a significant amount likely being spun off as distributions. For example at $8/share, the stock price might reach a $100 with an 8-9% yield. The number of years, for this possible about face, isn’t that far into the future, maybe as few as eight quarters. We must ask what else can they do with it? Burn it? Smoke it?

Risk

Now for risks and there are some major risks, one being the collapsing price of NG, the primarily reason for the stock price in the high $20’s.

NG pricing has collapsed into the high 2’s or low 3’s. (A good place for charting NG is YCharts.) The current price issue is primarily about weather being unseasonal bearish. But, weather models, both U. S. and European are predicting significantly colder weather in coming weeks. ““National demand will increase to strong levels as cold air over the central U.S. spreads into the East,” NatGasWeather said.”

And coupled with colder weather, Freeport’s LNG plant began its startup during the week of January 23rd. This unit consumes about 2% of total U. S. production. A news outlet summed the effect, “This would enable it to ramp up 2 Bcf/d of capacity within weeks, drawing gas from domestic supplies and compensating for the mild weather start to 2023.” Still, weather issues have been abnormal across the globe driving NG pricing into the basement. Yet, weather does change.

Before we close this worthwhile bit of advice is likely important for investors, “For gas longs frustrated by the tenacity of the bears, I would suggest the wisdom of John Maynard Keynes, who famously said: “Markets can stay irrational longer than you can stay solvent.” Even so, we rate riding Antero Resources a buy at opportune prices. We use a 3 bar close above the 18 bar moving average in the half hour bar for one of our opportune buy signals. We are buying, slowly. Riding with Antero seems like the sweet joy of riding in a sleeping car.

Be the first to comment