Kameleon007/iStock via Getty Images

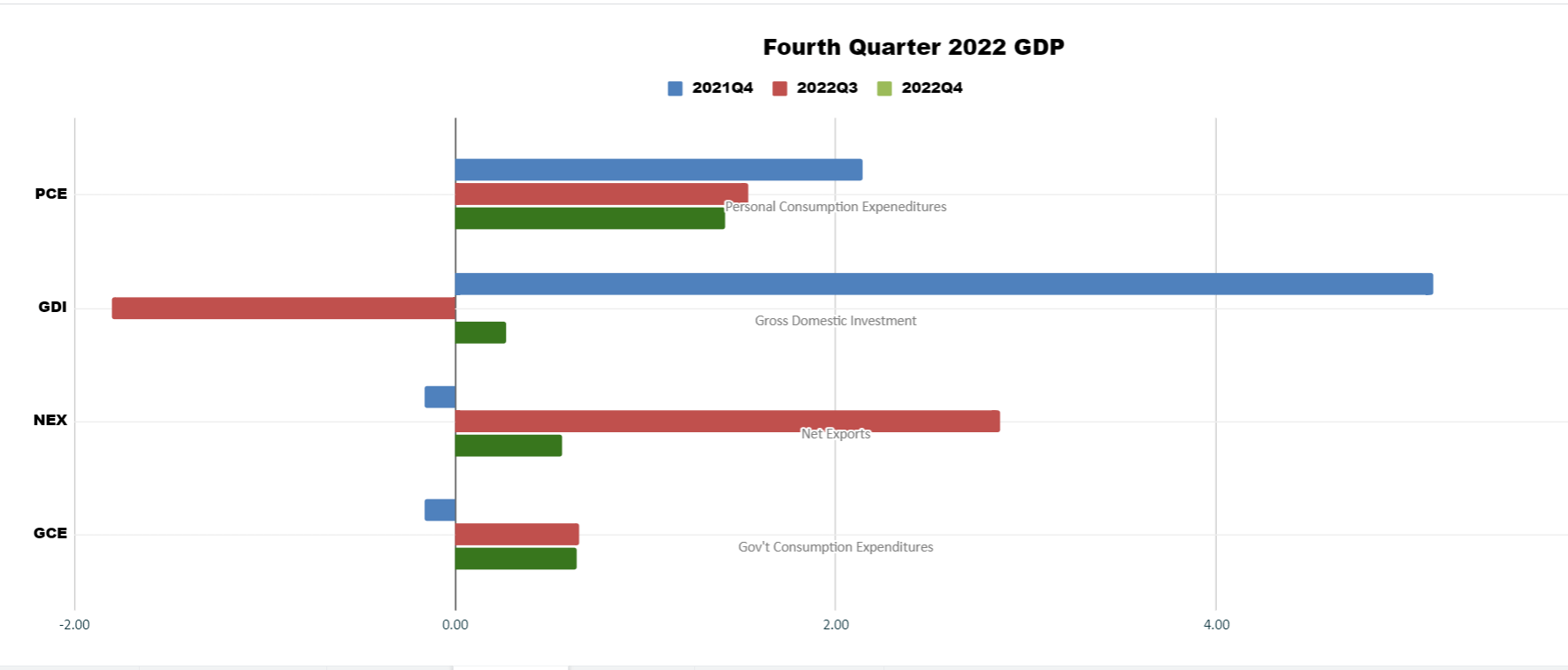

NEW YORK (January 26) – GDP printed at 2.9% this morning, above expectations of 2.6%. The separate components were as follows:

2022Q4 GDP Components (Comparables) (The Stuyvesant Square Consultancy Chart from BEA Release)

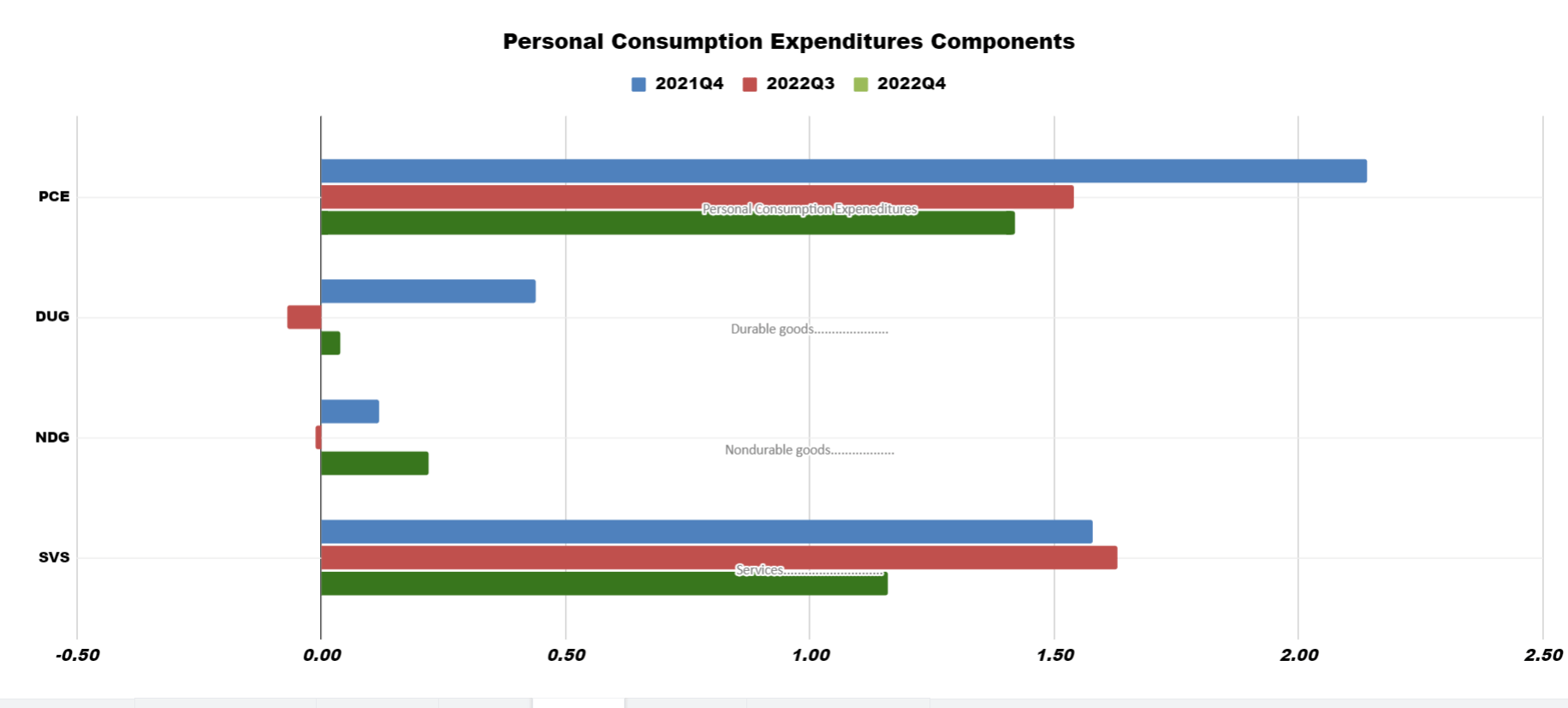

The leading component of the GDP was Personal Consumption Expenditures, or PCE. Those gains, in turn, were propelled by the consumption of services, or SVS, as illustrated below.

Components of PCE (The Stuyvesant Square Consultancy from BEA Data)

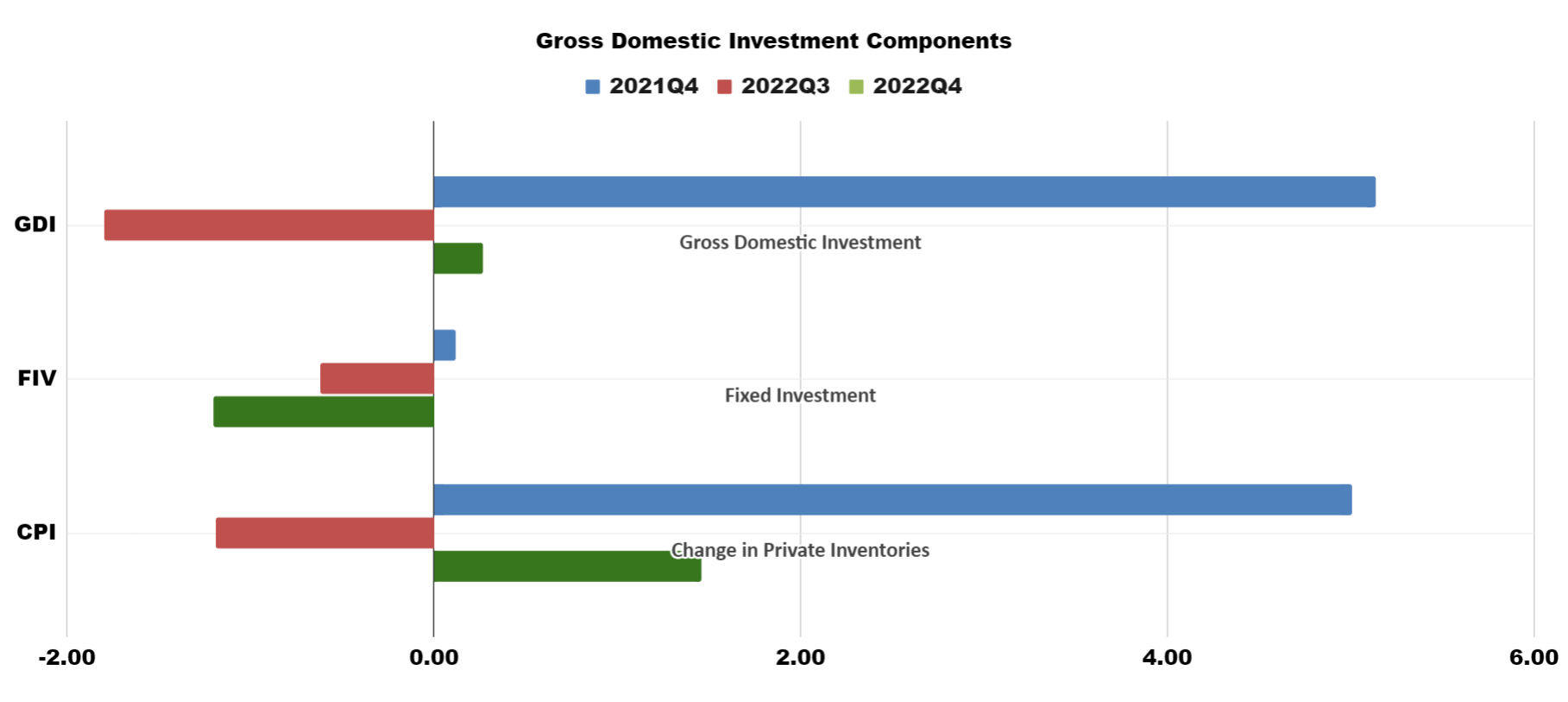

Less obvious is the falloff in Gross Domestic Investment, principally because Fixed Investment was offset by an increase in private inventories, as shown here:

Gross Domestic Investment and Components (The Stuyvesant Square Consultancy from BEA Release Data)

Fixed investment fell because residential investment fell 129 bps from last quarter.

ANALYSIS

We think that the data today and recently indicates an above-average risk of recession in 2023, which we put, as of today, at 70%.

As Japan and China return from the pandemic, their own anemic domestic consumption will cause them to try to export their way to growth, causing inventories of manufactured goods to grow. That will, in turn, cause discounting and margin pressure on many suppliers and retailers, particularly in consumer durables sold at places like Lowe’s (LOW), Home Depot (HD), and the like as well as at auto dealers. (We’re anxious to see durable goods orders for January because the December number was optimistic, but digging further, it turns out much of the dollar value of new orders was in non-defense aircraft (to 28,879 in December from 13,404 in November MOM.) Boeing (BA) touted it’s strong December orders performance in its earnings call yesterday.)

We’re also troubled that so many tech companies announced layoffs ahead of their earnings reports. Yesterday’s negative forward guidance from Microsoft (MSFT) drove down the indexes in all markets, and we expect the other tech giants to report similarly.

We anticipate that any recession will be led by the tech and manufacturing sectors, and that layoffs in those mostly higher-wage sectors will work their way through to the service sector in reduced consumer spending, adding to the aforementioned margin pressure.

_________________________

Author’s Note: Our commentaries most often tend to be event-driven. They are largely written from a public policy, economic, or political/geopolitical perspective. Some are written from a management consulting perspective for companies that we believe to be under-performing and include strategies that we would recommend were the companies our clients. Others discuss new management strategies we believe will fail. This approach lends special value to contrarian investors to uncover potential opportunities in companies that are otherwise in downturn. (Opinions with respect to such companies here, however, assume the company will not change). If you like our perspective, please consider following us by clicking the “Follow” link above.

Be the first to comment