RichVintage

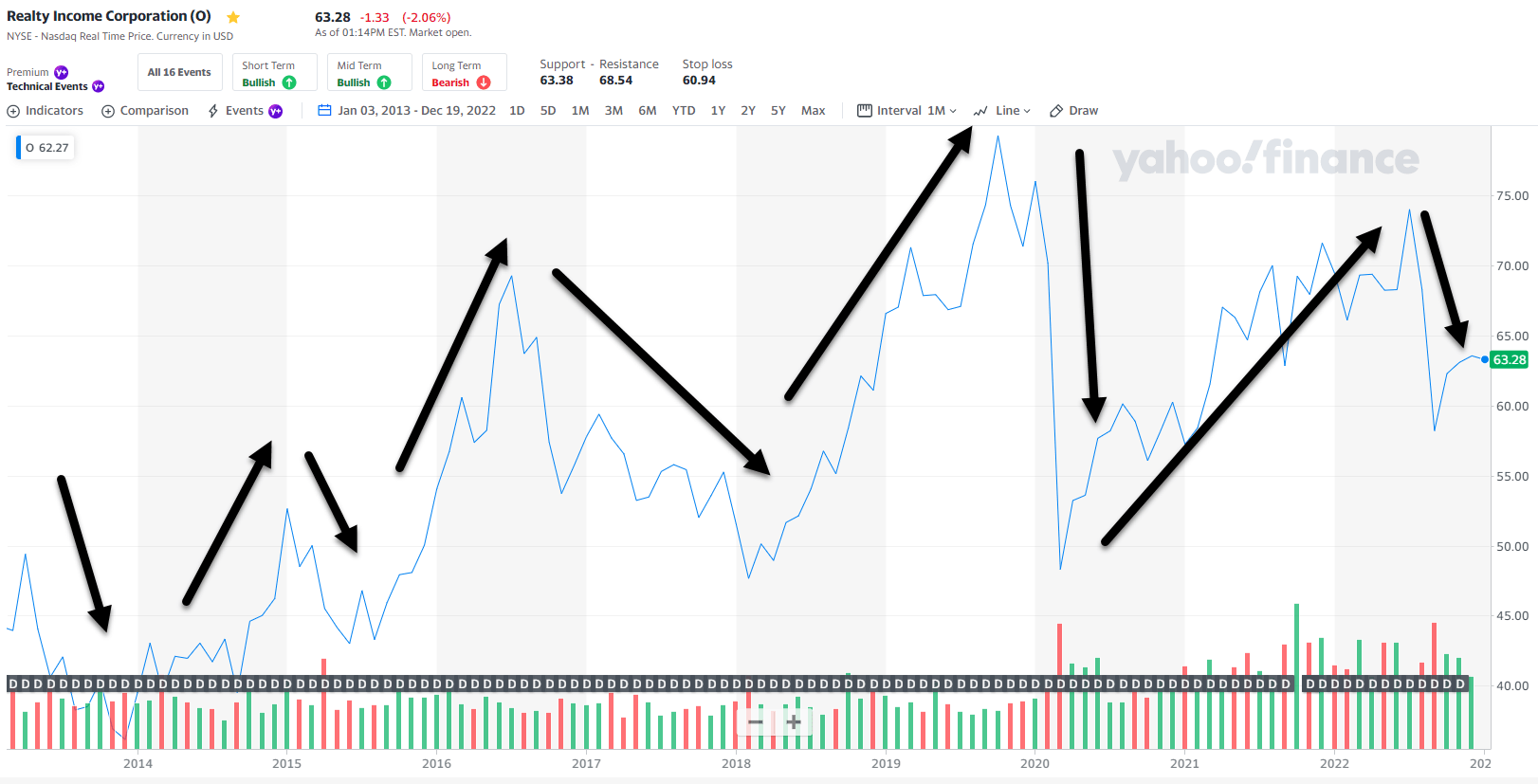

What do you think about when you see a stock that looks like this?

Yahoo Finance

Scary, right?

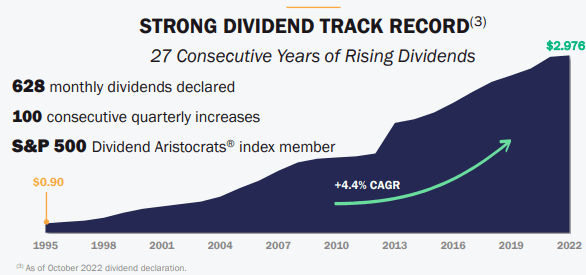

But what if I showed you a chart that looks like this?

Realty Income Investor Presentation

That’s hard to grasp, right?

Why does a stock that moves up and down like a roller coaster also generate one of the most stable and predictable dividends on the planet?

The Answer can be explained by the legendary investor, Warren Buffett:

Ben Graham, my friend and teacher, long ago described the mental attitude toward market fluctuations that I believe to be most conducive to investment success.

He said that you should imagine market quotations as coming from a remarkably accommodating fellow named Mr. Market who is your partner in a private business. Without fail, Mr. Market appears daily and names a price at which he will either buy your interest or sell you his.

Even though the business that the two of you own may have economic characteristics that are stable, Mr. Market’s quotations will be anything but.

For, sad to say, the poor fellow has incurable emotional problems. At times he feels euphoric and can see only the favorable factors affecting the business. When in that mood, he names a very high buy-sell price because he fears that you will snap up his interest and rob him of imminent gains.

At other times he is depressed and can see nothing but trouble ahead for both the business and the world. On these occasions he will name a very low price, since he is terrified that you will unload your interest on him.”

There you have it, Mr. Market has “incurable emotional problems.”

But wait, it gets even better,

“But, like Cinderella at the ball, you must heed one warning or everything will turn into pumpkins and mice: Mr. Market is there to serve you, not to guide you.

It is his pocketbook, not his wisdom, that you will find useful. If he shows up some day in a particularly foolish mood, you are free to ignore him or to take advantage of him, but it will be disastrous if you fall under his influence.

Indeed, if you aren’t certain that you understand and can value your business far better than Mr. Market, you don’t belong in the game. As they say in poker, “If you’ve been in the game 30 minutes and you don’t know who the patsy is, you’re the patsy.”

Do you get it now?

Mr. Market is these to serve you folks, not to guide you, and I’m going to tell you why my No. 1 holding, Realty Income (NYSE:O), has all of the ingredients for something very, very special.

A Look Back In Time

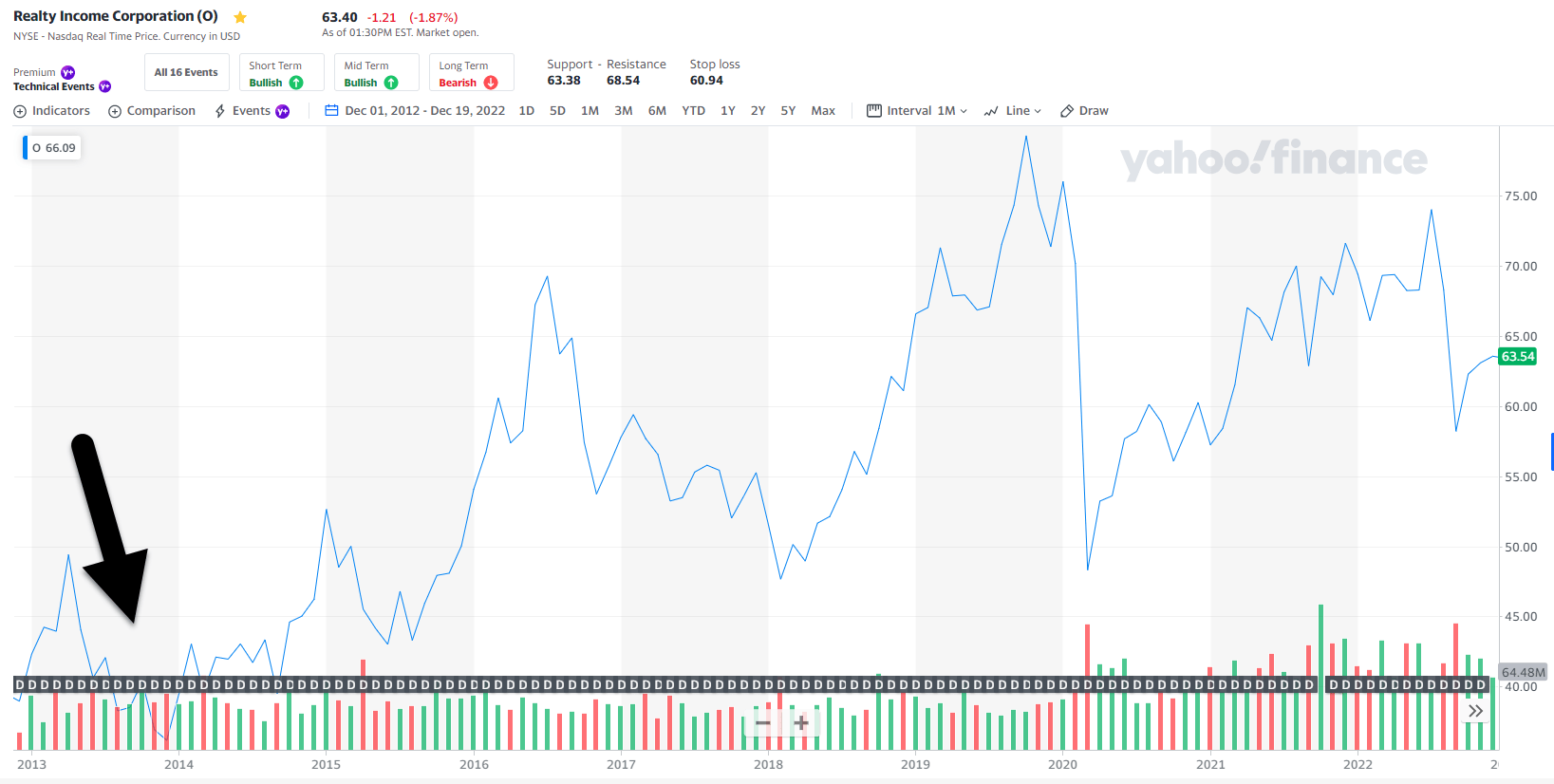

Back in 2013, just as the world was beginning to emerge from a global financial crisis, the Federal Reserve announced that it planned to progressively decrease the amount of quantitative easing implemented after the Lehman Brothers collapse in 2008.

This resulted in a slowdown in the purchase of government bonds, and many REIT shares, including Realty Income, began to decline, as shown below:

Yahoo Finance

That my friends is the same pattern that we’ve seen over the last nine years, and with the exception of the Global Pandemic, every pullback has been as a result of Mr. Market’s anxiety as it relates to net lease REITs and rising rates.

So, this should be nothing new whatsoever, and in fact, Realty Income’s previous CEO discussed it in his 2012 Annual letter to shareholders,

“We might think of the past 30 years as being akin to an easy downhill ski run with evenly packed powder and little to block one’s progress. Eventually, however, we do get to the bottom of the hill, which is where we may be right now with interest rates and there seems to be no chairlift in sight.

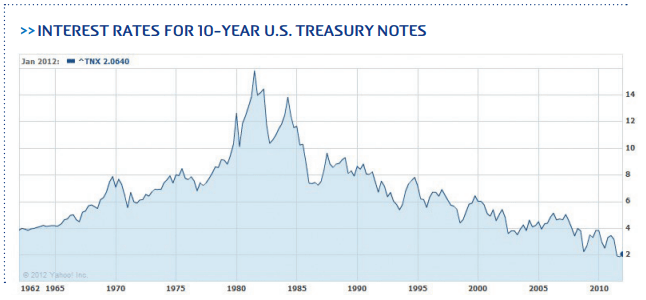

A compelling graphic illustration of where interest rates have been, since 1962, is shown in a chart that tracks the history of interest rates for 10-year US Treasury notes, a leading benchmark for what other lenders charge. This chart depicts the story of a steady, downward trajectory of interest rates from their peak of over 15% in 1982 to a low of 1.9% by the end of 2011.”

Realty Income 2012 Annual Report

I find this chart and the letter from Lewis extremely relevant given the fact that Realty Income was preparing for this interest rate cycle for over a decade. It’s proof that the company has been stress-testing and preparing for this new interest rate paradigm for years and years…

So why is Mr. Market so fearful?

As Buffett said, Mr. Market has “incurable emotional problems.”

What’s Changed Over The Years?

I’ve been a shareholder in Realty Income for around a decade and I did business with the company before that, when I was a net lease developer. So I can attest firsthand the evolution of the business model…

When Lewis was CEO (in 2011) the company had 2,600 properties:

Realty Income 2012 Annual Report

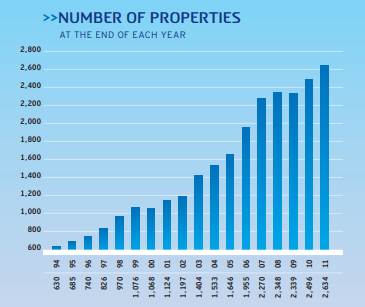

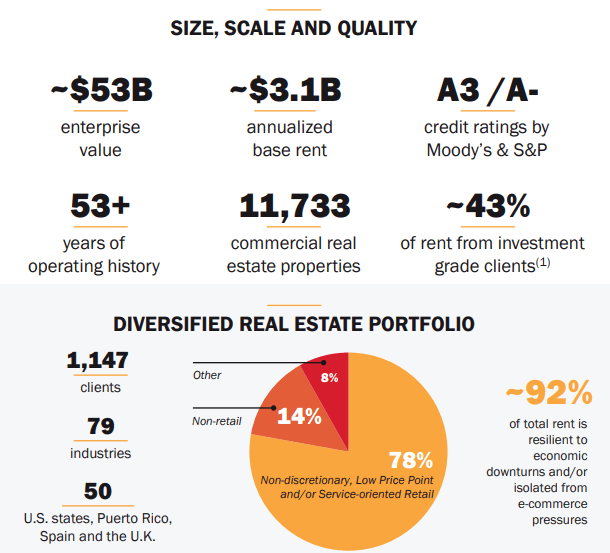

Today the company is an S&P 500 constituent with a portfolio of more than 11,700 properties:

Realty Income Investor Presentation

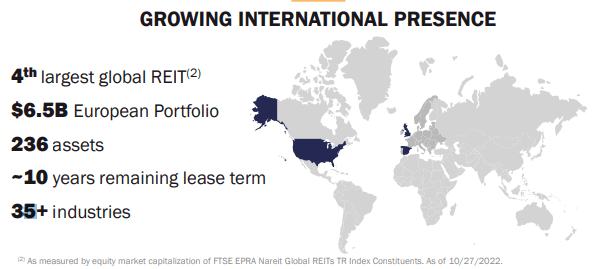

In addition, the company has expanded into Europe with a $6.5 Billion portfolio that includes 236 assets:

Realty Income Investor Presentation

Needless to say, Realty Income has become a dominant force in the net lease sector, in which scale is a prime differentiator. Because of this scale advantage, Realty Income can selectively pursue large-scale sale-leaseback or portfolio transaction opportunities without creating financing contingencies or concentration risks.

For example, the company recently closed on the purchase of the Encore Boston Harbor Resort and Casino for $1.7 billion at a 5.9% cash cap rate. The transaction was consummated under a 30-year triple net lease with favorable annual escalators.

Pro-forma for the transaction, Realty Income’s exposure to the gaming sector is expected to be < 3.5%, preserving prudent diversification.

In addition, this deal validates the growth profile of the business model and demonstrates that its growth opportunities are unconstrained by industry, property type or geography and in alignment with Realty Income’s investment criteria.

Also, anyone who believes that Realty Income is not growing may have “incurable emotional problems” because the pipeline is virtually infinite.

Just last week the company closed on the $894 million CIM Real Estate Trust portfolio that has around 48% investment grade rated tenants at a cap rate of ~7.1%.

So, in the first few days of 2023 the company has put just under $1 billion in the books, compared to its 2022 acquisition closings that totaled ~$6.9 billion (guidance was $6 billion).

There aren’t many REITs that can knock down $1 Billion acquisitions, yet Realty Income can do it in their sleep…

But Realty Income Isn’t Growing?

Blah, blah, blah…

That’s what Mr. Market thinks…

Consider the fact that around two-thirds of earnings growth is driven by external revenue, not the same as same store revenue. And in fact, that’s the case for all net lease peers.

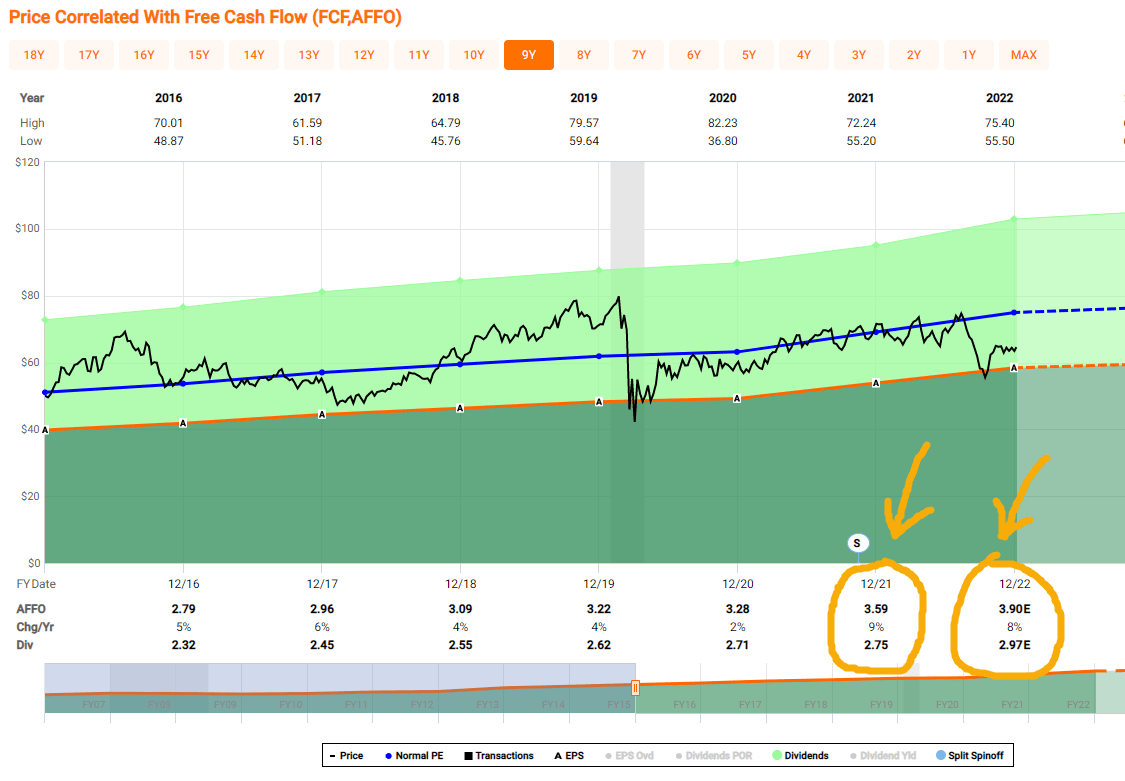

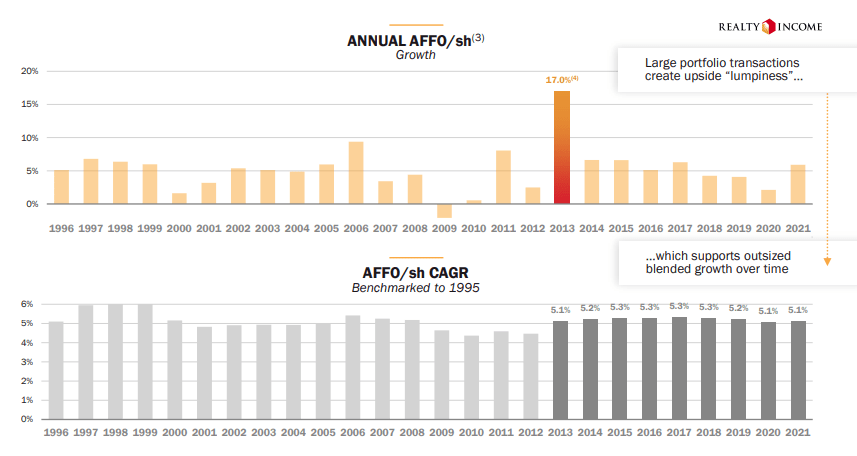

See below: midpoint AFFO per share growth for O in 2022, that’s anything but decelerating growth:

FAST Graphs

And when you consider growth, compared to peers, Realty Income has generated positive growth in 25 out of 26 years, and that’s through periods of rising rates and a global pandemic.

Realty Income Investor Presentation

Clearly, we’re dealing with the rule of scale here, in which to move the needle Realty Income must source more volume… but remember, the company is not taking on more incremental risk whatsoever. The primary thing the investor (or prospective investor) should be concerned with is the growth per unit of risk.

Once again, just one year (out of 26 years) with negative growth and that was during the Great Recession (when Realty was less diversified, not A-rated, and not a member of the S&P 500). And this juggernaut is ripe to continue to consolidate, Sumit Roy, current CEO, pointed out on the Q3-22 earnings call:

“M&A is something that one should absolutely consider, especially if it’s a 100% stock deal and you don’t have an over-reliance on the public markets on the debt side to help finance. And if your relative cost of capital is stronger, which in our case, under most circumstances, it is, and that is something that would be very attractive to us.”

Hmmm. Spirit Realty (SRC)?

As far as I’m concerned, investors should be willing to pay up for Realty Income because they are taking on less risk. It simply boils down to your goal and tolerance for risk…

The Ultimate SWAN

Once again, going back in time to Tom Lewis’ CEO letter from 2012,

“It’s easy to see in this chart how we might have come to believe that debt was the savviest way to finance both business and personal asset purchases. However, no matter what we came to believe, the use of debt carries risk. And periods of prolonged low interest rates, like the period we’re in right now, inevitably create economic imbalances that are often smoothed out by periods of adjustment that can be both prolonged and difficult.

More importantly, the period of declining interest rates eventually ends and at some point rates starts to rise. At that point, in a highly leveraged society, the pain of higher rates can be significant. So, what might we expect in terms of interest rates in the years ahead?

…Should rates return to the average rate on the 10-year Treasury for the last 60 years, that could increase interest rates by 4% or so. And finally, there is some probability of very high interest rates, as the chart on the previous page shows, similar to what occurred in the late 1970’s and early 1980’s where inflation accelerated dramatically.

So what does it mean for all of us if interest rates were to go up for some or all of the companies out there? It means that for companies with a lot of leverage, when they go to refinance their existing debt, it could be very painful and could remove a good deal of their cash flow to pay higher interest costs.

Should this occur for some of our tenants it could make it harder for them to pay rent. It could also have an additional impact on consumer spending, should individuals have to pay meaningfully higher interest on their debts.”

Once again, this was written around a decade ago, and here we are today…

…where Realty Income is much larger, much more diversified, much stronger (A- rated), and is a Dividend Aristocrat…

Yet, Mr. Market is still spooked…

“…[A]n investor will succeed by coupling good business judgment with an ability to insulate his thoughts and behavior from the super-contagious emotions that swirl about the marketplace. In my own efforts to stay insulated, I have found it highly useful to keep Ben’s Mr. Market concept firmly in mind.” Benjamin Graham

FAST Graphs

Remember, in the short-run the stock market is a voting machine; in the long-run the stock market is a weighing machine.

Stock prices will fluctuate day-to-day. But over many years, stock prices will reflect the true intrinsic value of the underlying business.

In today’s market environment, it’s especially important to remember this fact – and to always think of Mr. Market.

Happy SWAN Investing!

Author’s note: Brad Thomas is a Wall Street writer, which means he’s not always right with his predictions or recommendations. Since that also applies to his grammar, please excuse any typos you may find. Also, this article is free: Written and distributed only to assist in research while providing a forum for second-level thinking.

Be the first to comment