kate_sept2004

Realty Income (NYSE:O) is one of the world’s leading real estate investment trusts, with a market capitalization of roughly $45 billion. The company has consistently grown, with a dividend yield of roughly 6%, and a reputation as the monthly dividend company. As we’ll see throughout this article, the company is a valuable long-term investment opportunity.

Realty Income Overview

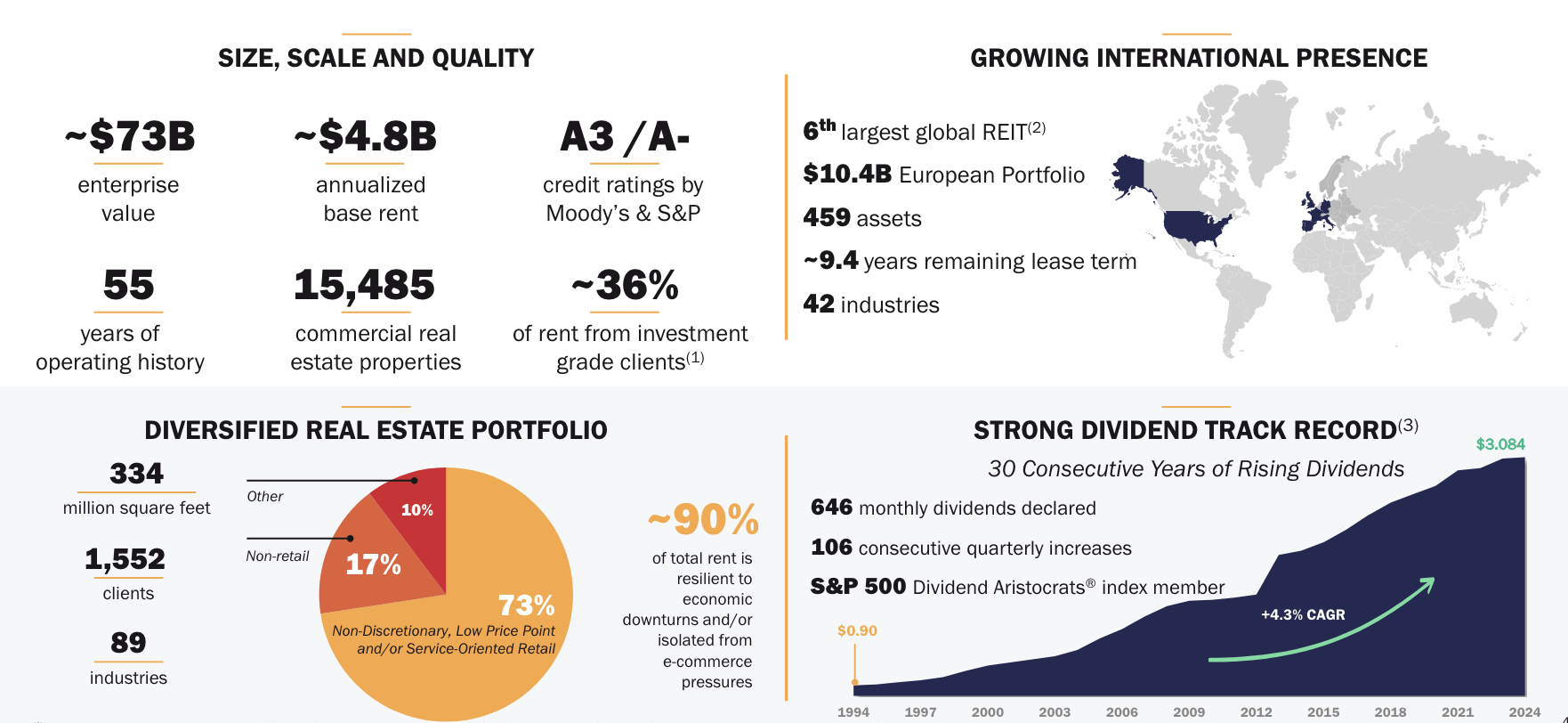

The company has become one of the largest REITs in the world, with an enterprise value of more than $70 billion.

Realty Income Investor Presentation

The company earns strong rent, with almost $5 billion in annualized base rent, diversified across the U.S. and Europe, with a massive European portfolio worth more than $10 billion. The company has more than 15 thousand properties, and an incredibly strong A3/A- credit rating. The vast majority of the company’s portfolio is non investment-grade large clients.

However, that’s not a concern given the strong diversification. The company is committed to shareholder returns, with a monthly dividend and regular quarterly increases to the tune of ~4% annualized. Combined with an almost 6% yield, that means that long-term investors will see strong and long-term growing returns.

More importantly, the company operates in a massive industry (REITs) which means it has a very long pipeline for continued growth.

Realty Income Q1 2024 Results

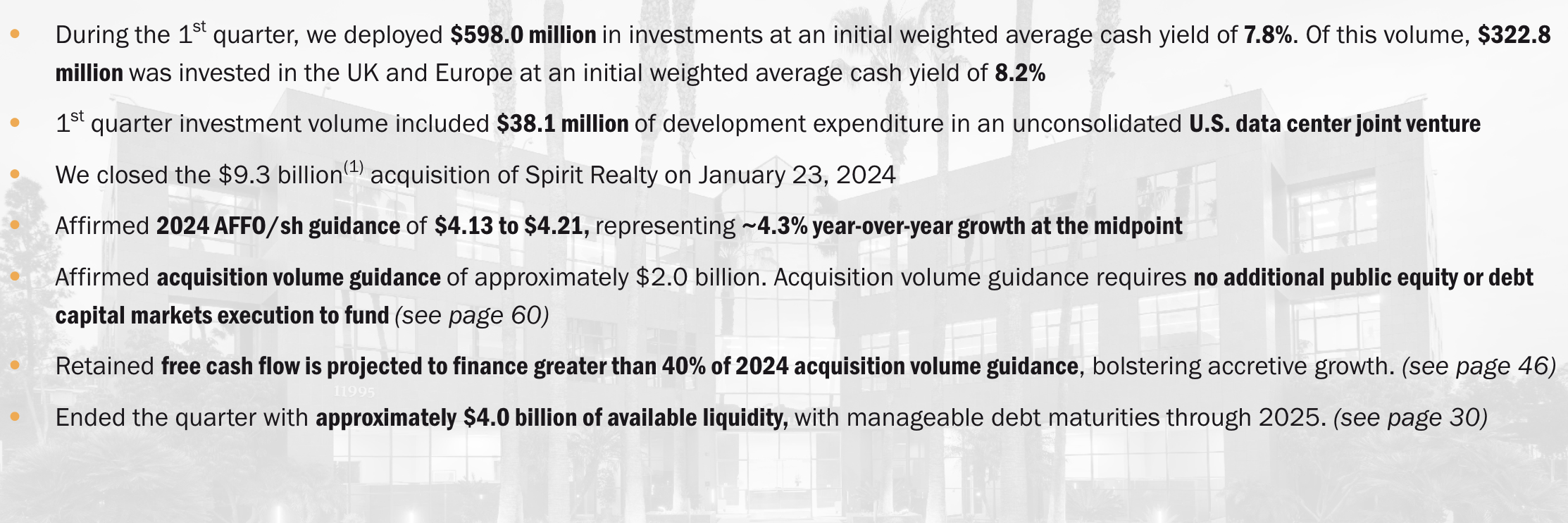

The company had strong performance in the quarter taking advantage of higher interest rates, which means strong cash yields.

Realty Income Investor Presentation

The company deployed almost $600 million at roughly 8%, earning a similar, but slightly higher yield with the more than half of the money which was deployed in the UK and Europe. The company also closed the massive, more than $9 billion acquisition of Spirit Realty. The company expects ~$4.15 / AFFO / share, 4% YoY growth and putting it at ~8% yield.

Realty Income is never going to be an investment that becomes a ten-bagger in just a few years. However, it can reliably generate a strong and growing dividend.

Realty Income Expansion Potential

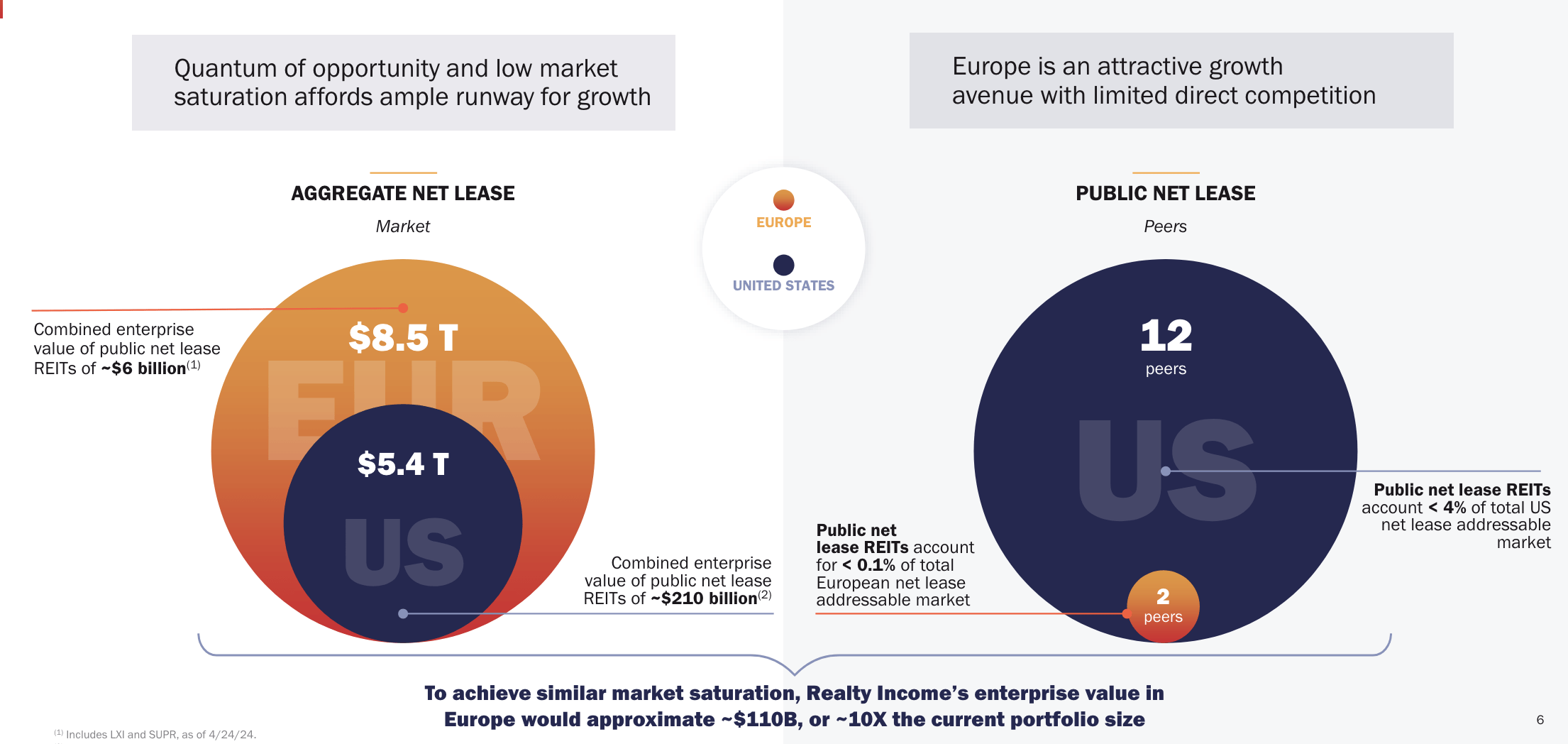

One of the concerns among large companies as they continue to grow is whether they cap out in size. That’s much less of a concern for REITs.

Realty Income Investor Presentation

The total market size for the company is $5.4 trillion US, and the company has expanded to Europe and become one of the largest REITs there. In Europe, the company sees a potential market size of $8.5 trillion, more than 50% larger than the US, with much less penetration from REITs. The company’s minimal peers enable much faster expansion.

Realty Income Balance Sheet

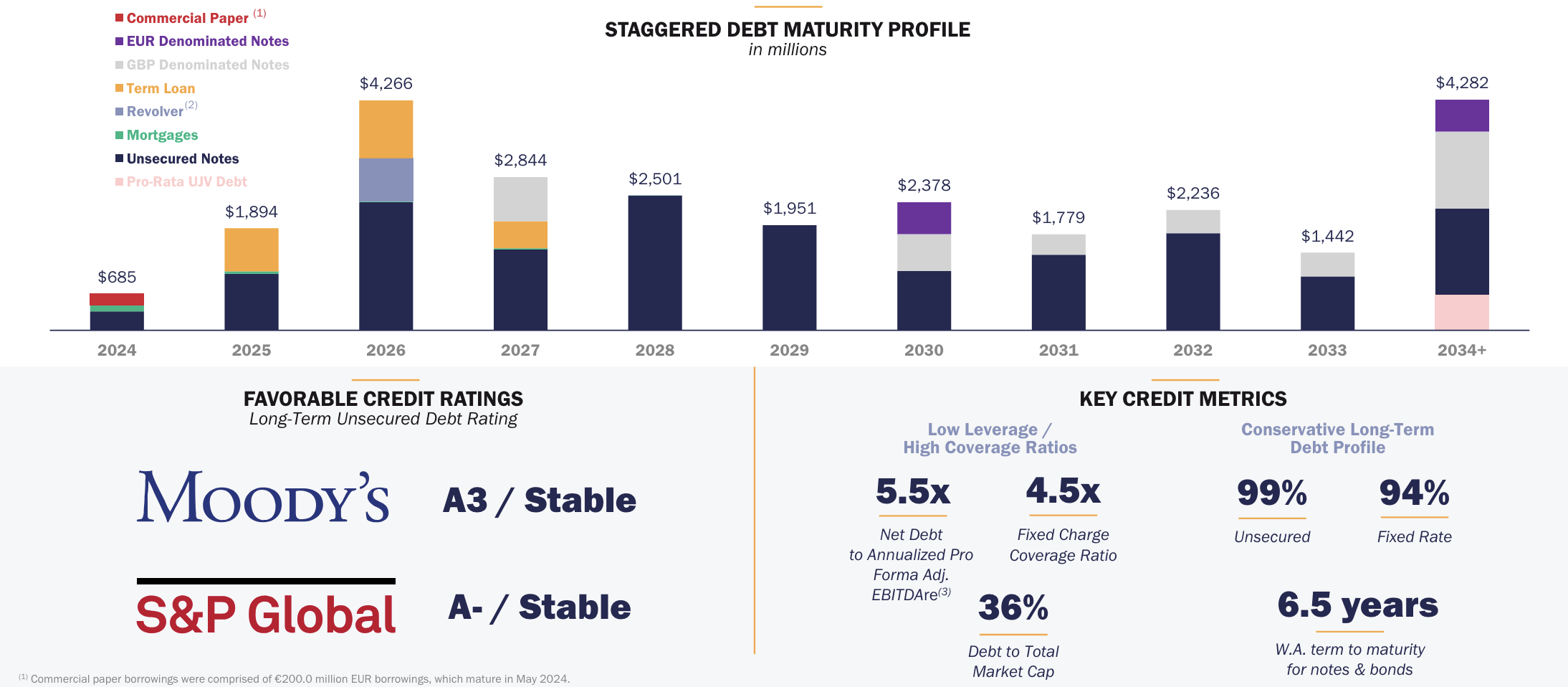

The company’s balance sheet shows its relevant strength, although it does have significant debt that will need to be rolled over.

Realty Income Investor Presentation

The company has a 36% debt to total market cap ratio and a 4.5x fixed charge ratio. The vast majority of its debt is fixed rate, with its more than $20 billion in debt having a ~6.5-year weighted average term to majority. In the next 5-years, counting the remainder of the current year, the company has ~$12 billion in debt.

In a world where interest rates remain higher for longer, the company might have to roll over a substantial amount of its debt to higher interest rates.

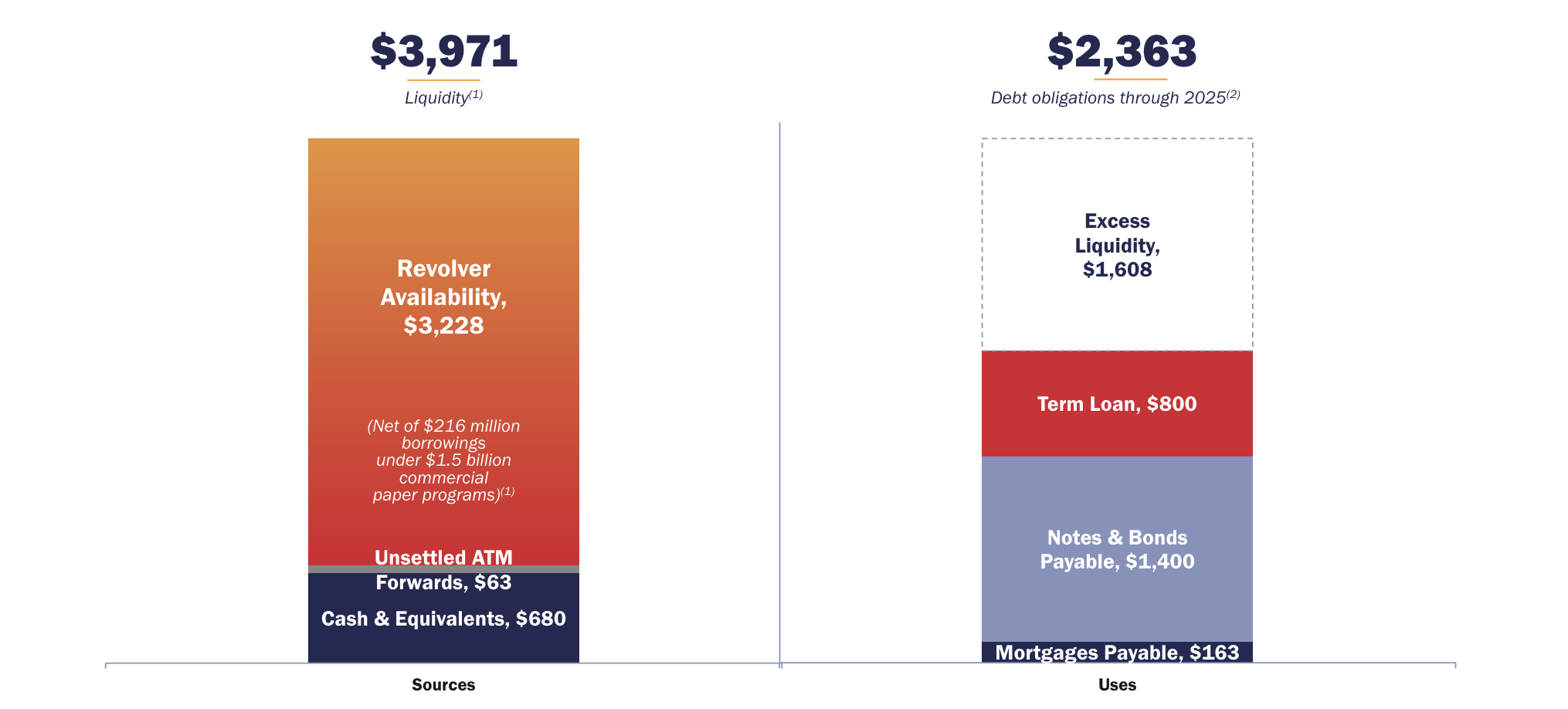

Realty Income Investor Presentation

The company does have a significant amount of liquidity through year-end 2025, which could protect it from substantial volatility in the market. That’s relevant and exciting to see, however, it doesn’t guarantee that the company could handle any sort of protracted downturn. That’s something worth paying close attention to.

Realty Income 2024 Guidance

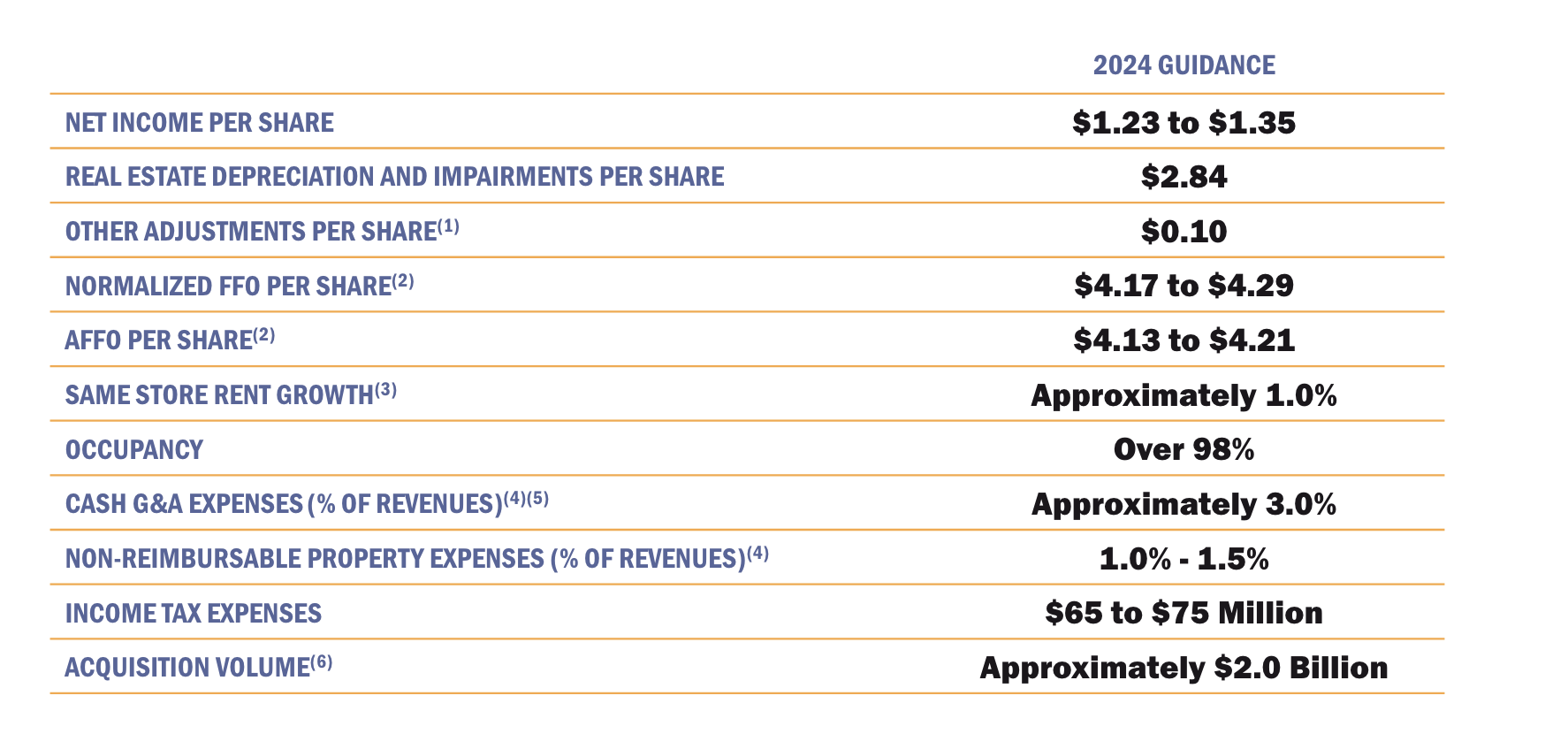

The company’s 2024 guidance shows its strong cash flow and commitment to continued shareholder returns.

Realty Income Investor Presentation

The company expects to earn net income per share of ~$1.3, a relatively low yield, however, real estate depreciation and other adjustments also help its per share earnings. Its AFFO per share number is at $4.2 / share, or just under 8% with same store rent growth at 1% and occupancy at more than 98%. It expects expenses as a % of revenues to be incredibly low, at 4-4.5%.

The company expands to continue investing heavily in growth, with roughly $2 billion in acquisition volume. The key takeaway here is that Realty Income is a strong investment with reliable and long-term growing cash flow. There are higher yielding investments, but few that have the low risk and reliable cash flow.

Thesis Risk

The largest risk to our thesis is the company’s need to continue borrowing money to grow in a high-yield environment. A high cost of borrowing today that doesn’t result in long-term cap rate increases could hurt the company’s ability to continue generating growing dividends. That’s worth paying close attention to.

Conclusion

Realty Income has a strong dividend yield, with a reputation of a monthly dividend company and an almost 6% dividend yield. The company has grown its dividend yield on a quarterly basis and remains committed to future growth. We expect the company to be able to comfortably do this. The company is continuing to expand with acquisitions, especially in Europe.

Our view of Realty Income is in some ways a bond or an annuity. It’s incredibly well diversified with a massive portfolio of rent collection, and it showed an ability to weather Black Swan events such as a COVID-19. We don’t expect it to hit the double-digit yield we sometimes look for on other investments, but we expect it to provide reliable long-term growing cash flow.

Be the first to comment