bymuratdeniz/iStock via Getty Images

Not much worked in 2022. That is no surprise to anyone who has studied investment returns and economic environments. The only reliable sector for positive returns in a surging inflationary environment is energy. Also, a basket of commodities is known to be the most reliable and most robust inflation hedge. Commodities delivered in 2021 (exponentially) and in 2022. And due to the rising rate environment duration mattered. Long durations assets such as long bonds and growth stocks were hit hard in 2022. Value stocks, often found in the bigger dividend payers, outperformed the market in 2022.

2022 was impossible to predict. We had another ‘black swan’ with the unfortunate and tragic invasion of Ukraine. And you might suggest that it was not a black swan event, as war is a ‘normal’ part of human and political behavior. So call it a dark grey swan perhaps. A war in Europe was certainly not expected. It changed and shaped everything.

Heading into 2022 I wrote in a post…

Barring any black swan event, 2022 might shape up to be a solid year for investors. (A black swan is an unpredictable and catastrophic event, such as the pandemic.) However, we are never free of risks. The main risk might continue to be troublesome inflation, and that could lead to the necessity of more aggressive rate hikes.

Yes, troublesome inflation was THE story of 2022. The fight against inflation was the most powerful economic force in play. We experienced the most aggressive rate hike path in history.

Here’s the 2022 U.S. rate hike path:

- 0.5%: up 25 bps on March 17

- 1%: up 50 bps on May 5

- 1.75%: up 75 bps on June 16

- 2.5%: up 75 bps on July 28

- 3.25%: up 75 bps on September 21

- 4%: up 75 bps on November 3

- 4.50%: up 50 bps on December 15

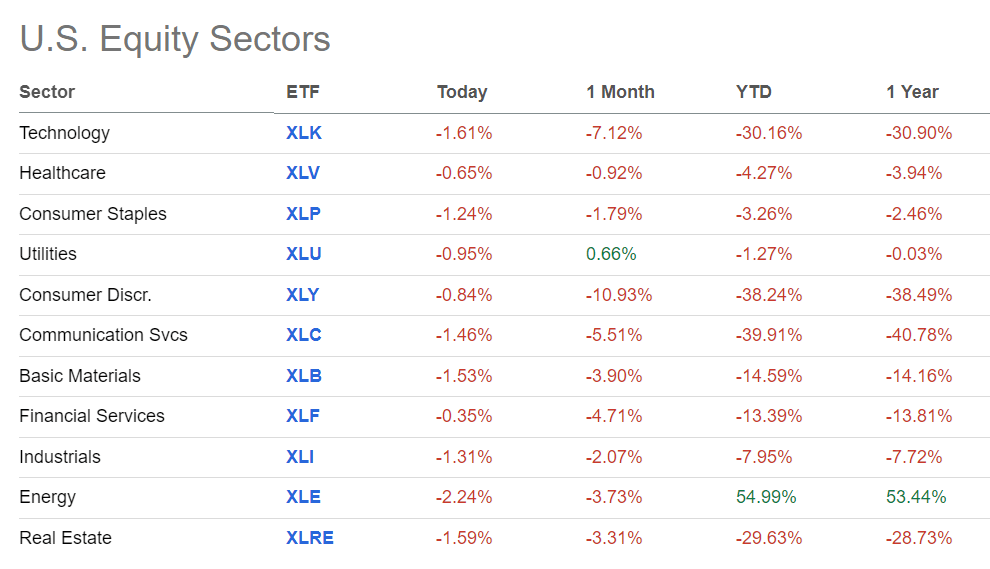

Asset and sector returns for 2022

I recently offered a roundup of asset and sector returns in a post for MoneySense.

U.S. stocks (IVV) are down more than 21% year-to-date, in price terms-on track for the worst year since 2008 and the fourth-worst since 1957.

Here are the returns of key markets from Canadian-dollar exchange-traded funds (ETFs).

- U.S. stocks down 12%

- International developed stocks down 8.7%

- International emerging stocks down 14%

And here’s the sector returns on Seeking Alpha, to December 28.

Asset returns in 2022 (Seeking Alpha)

Year to date and over the last year energy stands alone as the only sector to put in a positive performance. That’s no surprise if you read my Seeking Alpha post – Stocks don’t work for inflation.

During the stagflation era of the 1970’s and early 1980’s, only the energy and REIT sectors offered positive real returns. Gold (GLD) and commodities (DBC) also delivered in that period.

We’re still waiting for REITs to do their thing. In 2022, there are fears of the effect of higher borrowing costs on REITs. Plus the threat of recession is weighing on the sector.

Commodities have delivered in 2021 and in 2022. In fact that commodities ETF increased over 200% from January of 2021 to the peak in June of 2022.

Only the traditional inflation fighters worked in 2022. And those who hedged were treated to some very generous returns.

And for the record, I put oil and gas stocks on the table in October of 2022. On Seeking Alpha I had a look at the ridiculous dividend growth from our oil and gas stocks.

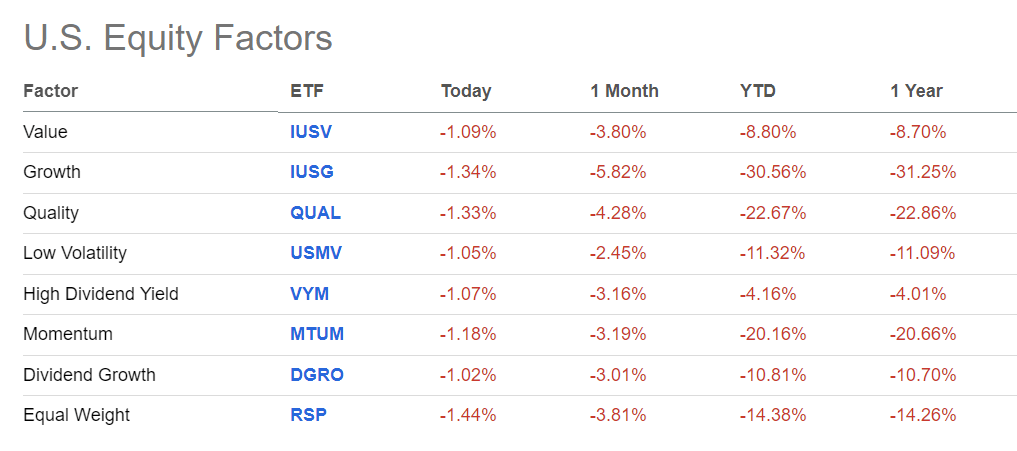

Equity factors in 2022

Factor returns in 2022 (Seeking Alpha)

It is no surprise that shorter duration assets (including shorter duration equities) performed better in 2022. In a rising rate (and higher rate) environment investors say ‘pay me now’. They want current generous earnings and dividends.

I continually put that theme on the table throughout 2022. And there was more value in the high dividend space (VYM) in the U.S. Better performance followed that favorable valuation. At one point in 2022 the high yield space had a PE ratio that was twice as favorable compared to the S&P 500.

In Canada we also experienced the value affect in the high dividend space.

In a recent post, Michael Fitzsimmons had a look at the Vanguard ETF (VDY:CA).

Canadian High Yield ETF is overweight financials and energy.

I know that ETF well. I worked on the marketing and communication materials when the fund was launched in Canada. We hold that in my wife’s accounts, from inception in 2013. That ETF that beats the Canadian market (XIU:CA). And the ETF has beat U.S. stocks and U.S. dividends ETFs such as (SCHD) from 2021 through 2022.

VDY has bested SCHD by 6% on an annual basis during 2021-2022 (not including currency effects).

We would expect Canadian stocks to outperform U.S. stocks in periods of higher inflation. Here’s a snippet from the worst of the stagflation era.

Canadian stocks outperformed U.S. stocks by:

- 18% in 1977

- 23% in 1978

- 26% in 1979

When the U.S. markets get overheated, Canadian and International stocks can step in. From 2000 to 2007, Canadian stocks returned 8.7% annual vs 1.6% for U.S. stocks. International outperformed the U.S. market as well.

For U.S. stocks in 2022 they may have suffered from the double whammy of overvaluation and a stock market that is not inflation friendly. Heading into 2023 it’s reasonable to suggest some of the valuation froth has been removed from the U.S. stock market.

A good year for all-weather portfolios

Given our overweight to Canadian stocks and with additional exposure to energy stocks and commodities, our returns have clocked in at over 3% year to date, and near 9% over the last year. We have not felt inflation.

Our U.S. stocks have held up better than the market.

While stock markets can beat inflation over longer periods, that’s of little help to a retiree who lives more in the moment, with the portfolio typically exposed to more short term risks. We need to protect. And in my opinion that includes protecting the portfolio from near-term inflation risks. The all-weather portfolio models help greatly in that regard.

And while typical all weather models use bonds and cash, gold and commodities to manage the economic regimes, one can use stocks to build the all-weather portfolio. Defensive stocks are also selected to help the cause in bear markets.

Here’s stocks for the retirement portfolio.

In that post you’ll find that I’m a fan of ‘the more weapons the merrier’. We can combine stocks that are strategically arranged in concert with bonds, cash and commodities. That might be the path to the most SWAN-friendly arrangement in retirement.

SWAN = Sleep Well At Night

And here’s a post on How To Position Your Portfolio For 2023. It’s possible that much of what worked in 2022 will again lead the way in 2023. We don’t know what we will get. But to that article I would add…

Today, the markets are starting to look to the ongoing economic damage caused by a higher rate environment. We don’t know the rate path and we don’t know the economic damage.

But the market makers will pay attention to the earnings decline and GDP decline. Earnings (market) typically decline by 15% to 20% in recessions. Reality will matter, at times.

The inverted yield curve has predicted 8 of the last 8 recessions.

Thanks for reading. Please hit the Like button if you liked this post. And we’ll see you in the comment section. I try to reply to most comments.

Be the first to comment