eyecrave/iStock via Getty Images

Investment thesis

Ready Capital Corporation (NYSE:RC) closed a fantastic 2021 with record net income, loan originations, CRE originations and acquisitions, and distributable income. Even with a slight dividend increase in 2022 and a more moderate growth, the payout ratio can remain healthy. In my opinion, despite these great growth figures, this is already priced into the current valuation and RC is fairly valued. This makes the company not a primary investment target for growth or value investors but income-seeking investors will find it attractive with an above 11% dividend yield and stable fundamentals.

Business Model

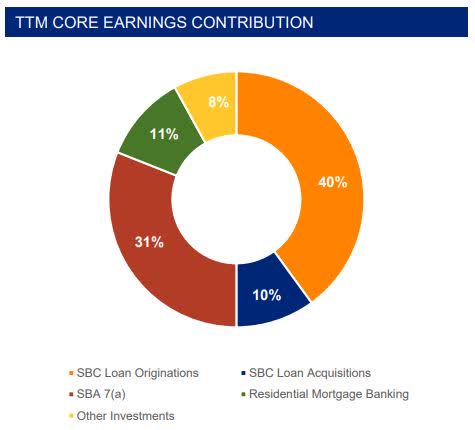

Ready Capital is a non-bank real estate and small business lender that has provided over $3 billion in capital nationwide. The company offers capital to real estate financing deals mainly to multifamily and commercial real estate. RC operates through three segments: SBC Lending and Acquisitions; Small Business Lending; and Residential Mortgage Banking. Although RC is classified as a mortgage REIT only approximately 11% of its revenue comes from the Residential Mortgage Banking segment. However, the company is in a strong position in multifamily lending via SBC product offerings. In addition, RC is also strong not only in organic growth but M&A’s as well. 6 completed acquisitions in the last 6 years fueled RC’s balance sheet. The latest one has just been completed in mid-March with stockholder approval for RC to acquire Mosaic.

2022 March Presentation

Financials & Earnings

Q4 results

“Ready Capital’s record fourth-quarter results concluded an exceptional year highlighted by record originations in our SBC and SBA 7(A) lending businesses, growth in our equity and debt capitalization, and strong credit performance” commented Thomas Capasse, RC’s Chairman and CEO.

It is a strong and fair statement as their ROE is above 12% ttm (above 18% for Q4) way higher than the mREIT sector average. The book value per share grew by 1.93% in Q4 from $15.06 to $15.35 per share. In addition, from the first quarter of 2021 to the fourth quarter of 2021 BV per share could grow by 3.09% while their net income grew by 85.47% in the same period. Net income grew from $45.8 million in Q3 2021 to $53.2 million in Q4 2021. Comparing Q4 results of 2020 and 2021 RC could almost double its net income in just a year. With the Mosaic merger, I am convinced that this growth rate can be sustained for the next 2-3 quarters relatively easily.

Valuation

It is very interesting at the moment because there are factors that suggest RC is a bit undervalued and there are factors that suggest it is fairly valued. Let’s start with the positive factors: the company has a Return on equity of 12% ttm while the mREIT industry average is 7%. RC’s forward non-GAAP P/E ratio of 6.8 is well below the sector median of 10.69. Let’s see the factors that indicate RC is fairly valued: taking a look at the share price it is in the upper part of the 52-week range and RC’s price return is almost identical to the S&P 500’s returns in 2022. The company’s price to book ratio is 0.99. Comparing the price to book value to the whole mortgage REIT sector, we can see that RC’s P/B is among the top 30% of all publicly traded mREITs (There are 41 publicly traded mREITs and 10 of them have higher P/B ratios than RC) so we can say the company is fairly valued based on this sole factor.

Company-specific Risks

In my opinion, the company’s success highly depends on its ability to effectively analyze potential acquisition and origination opportunities in order to assess the level of risk-adjusted returns that the management should expect from any particular investment. This is a major factor since RC is keen on M&A since on average they did 1 M&A every year in the last 6 years.

Another risk factor worth noting is the loan portfolio concentration in Texas and California. It represents approximately 19.2% and 14.3% of RC’s total loans as of December 31, 2021. The majority of these loans (58%) in the SBC lending and acquisitions segment are multifamily real estate loans. In addition, many of their borrowers are self-employed. Self-employed borrowers may be more likely to default on their mortgage loans than salaried or commissioned borrowers and generally have less predictable income. Moreover, (as you would expect from any REIT) their real estate investments, including any properties acquired by them through foreclosure, are relatively illiquid and difficult to buy and sell quickly.

As of December 31, 2021, the average loan-to-value of RC Commercial’s originated portfolio was 79%. The weighted average LTV of their acquired loans was 54%. If such SBC loans with higher LTV ratios become delinquent, the company may experience greater credit losses compared to lower-leveraged properties.

My take on RC’s dividend

Current dividend

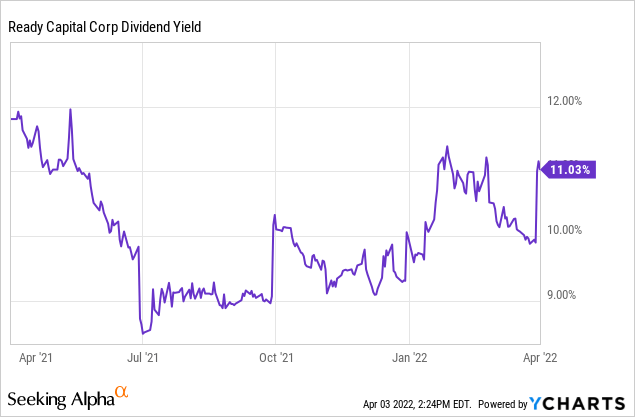

RC has been paying consecutive dividends for 8 years 3 years less than the sector average. Ready Capital is yielding at 11.03% which is relatively high compared to the last 9 months. Above 11% is considered a great dividend based on the last 8-9 months. You could only buy RC above the current yield approximately 5-6% of the time. In addition, the last 4 year’s average dividend yield is 9.29% so 11.03% is truly a great yield.

The company has been raising its dividend for 1 consecutive year and the last raise was in the second half of 2021 when the management raised back the dividend above pre-pandemic levels.

Future sustainability

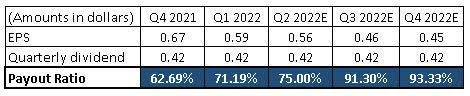

Despite being a mortgage REIT, RC has a well-covered dividend. The payout ratio is likely to increase a bit in the second half of the year. I calculated with the estimated EPS figures and the payout ratio will still be in the healthy and safe zone for income-seeking investors. Analysts do not calculate any dividend increase for 2022 however I see a slight possibility that the management could increase the dividend by $0.01 to $0.43 per share just to build up another year of consecutive dividend growth.

The table is created by the author. All figures are from the company’s financial statements and SA Earnings Estimates.

Final thoughts

Based on RC’s valuation it is safe to say that the company is fairly valued with great and strong fundamentals and with better than mREIT average ROE figures, and great M&A decisions. The million-dollar question is: for how long this exceptional growth can be sustained? My answer is that for the next 2-to 3 quarters it is absolutely real but if the management can continue this M&A policy over the next year or two this exceptional growth might be sustained (of course not the doubling net income every year). I am not planning to buy RC as a growth or value investor but as an income investor it can add dividend value to my portfolio with its dividend yield is above the 11% threshold. I would be happier with a $14-ish share price but a bit above $15 is also acceptable if we think long term.

Be the first to comment