Marcus Lindstrom

QuantumScape Corporation (NYSE:QS) is slated to report its FQ4’22 earnings release on February 15, as it staged a remarkable recovery from its late December lows. Bulls could point to the company successfully shipping its “first 24-layer prototype lithium-metal battery cells” to its automotive partners in December, lifting buying sentiments.

Analysts on its previous FQ3 earnings commentary were looking for more information on the ability of QuantumScape to deliver its prototype as a critical milestone toward its commercialization phase.

Despite that, the pre-revenue solid-state battery maker remains far from volume production. In addition, Morgan Stanley (MS) highlighted that “much work is needed to achieve commercial ramp,” adding that investors should also brace themselves for further dilution in the future.

Accordingly, QuantumScape had expected to start 2023 with “over $1 billion in liquidity.” Notwithstanding, according to the revised consensus estimates, QuantumScape is expected to report accumulated free cash flow (FCF) of -$1.2B through 2024, even before its projected commercial ramp in 2025 (and that’s still a big if).

Therefore, it’s pretty easy to understand why QS remains one of the short-sellers favorites with short interest as a percentage of float of nearly 24%.

As such, QS bulls likely still face significant structural headwinds, as QuantumScape still needs to prove its manufacturing prowess on its nascent technology.

Despite that, there’s little doubt that QuantumScape is riding massive secular tailwinds in EVs, which are still in a relatively early stage in their adoption. China is the clear leader, with DIGITIMES highlighting a penetration rate of 35% by 2023. However, the US is still in the nascent stage of its adoption, with EV share of new sales hitting the 6% mark in 2022.

Therefore, QuantumScape could leverage the massive potential in EV adoption if it could prove its commercial viability and production ramp capability by 2025.

QuantumScape sees the opportunity to widen its adoption to consumer electronics with its solid-state batteries. It highlighted that the “key selling point for consumer electronics is the ability of battery cells to run with zero externally applied pressure.”

In addition, management stressed that the “consumer electronics market has easier specifications compared to automotive,” which could leverage the company’s “scientific breakthrough of achieving zero applied pressure.”

Is it important? We believe so. If QuantumScape could achieve an earlier adoption through consumer electronics, it will also expand its use cases for its battery technology. However, it’s still too early to assess the potential benefits as management has yet to present the economics of such a breakthrough and commercial ramp to investors.

Moreover, QuantumScape also has competitors in the consumer space working on using solid electrolyte for consumer IoT devices. For example, Bloomberg reported in a recent article that Imprint Energy “created a donut-shaped battery” which is undergoing trials with Sensos (SONY) and Renesas (OTCPK:RNECF).

With that in mind, QS short-sellers were likely caught in a massive turnaround in broad market sentiments in 2023 as the market lifted the valuations of consumer discretionary and technology stocks.

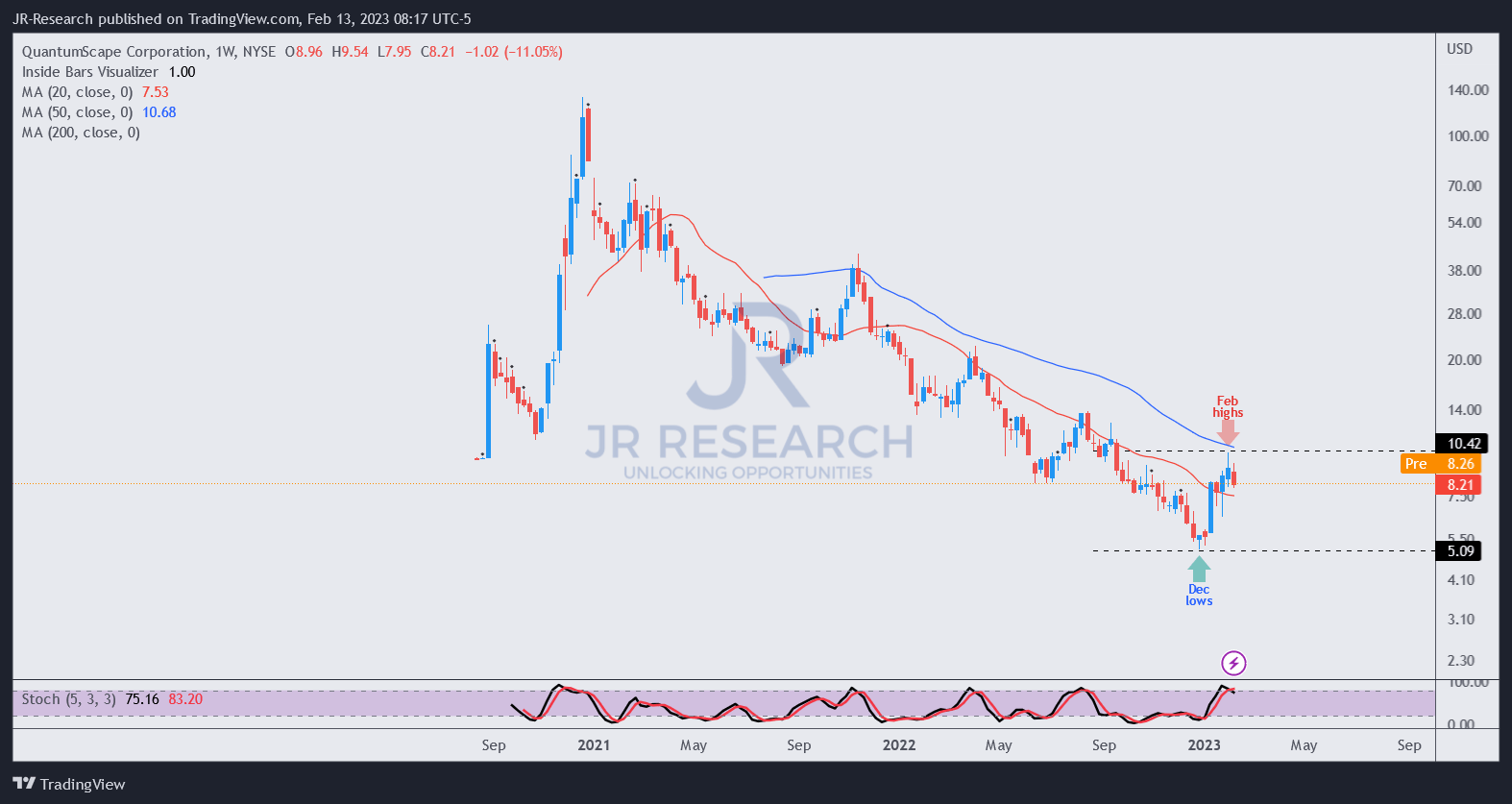

Accordingly, QS recovered more than 100% from its December bottom through its February highs. Therefore, should investors who missed buying its December lows consider an opportunity to jump on the bandwagon now?

QS price chart (weekly) (TradingView)

Given QuantumScape’s unprofitable business model and is nowhere close to profitability, it’s challenging to model the company’s expected FCF through 2025.

Coupled with the complexity of potential capital infusion, investors who bought QS likely didn’t expect to see near- to medium-term returns. Also, those who chased its highs in 2021 have either bailed or likely already given up on the remaining positions.

Our assessment suggests that there are better ways to play the EV revolution. Investors can consider investing in automotive OEMs or leading EV makers like Tesla (TSLA), as they are profitable. Otherwise, investors can consider semiconductor players with a growing automotive business, such as Nvidia (NVDA) or Qualcomm (QCOM). Investors can consider automotive-focused semi-players such as Texas Instruments (TXN) or even ON Semiconductor (ON).

However, if you managed to capitalize on the recent bottom in QS, we believe it’s an opportune time to cut exposure, given the significant surge.

Rating: Sell (Revise from Hold).

Be the first to comment