Jaiz Anuar

DISCLAIMER: This note is intended for US recipients only and, in particular, is not directed at, nor intended to be relied upon by any UK recipients. Any information or analysis in this note is not an offer to sell or the solicitation of an offer to buy any securities. Nothing in this note is intended to be investment advice and nor should it be relied upon to make investment decisions. Cestrian Capital Research, Inc., its employees, agents or affiliates, including the author of this note, or related persons, may have a position in any stocks, security, or financial instrument referenced in this note. Any opinions, analyses, or probabilities expressed in this note are those of the author as of the note’s date of publication and are subject to change without notice. Companies referenced in this note or their employees or affiliates may be customers of Cestrian Capital Research, Inc. Cestrian Capital Research, Inc. values both its independence and transparency and does not believe that this presents a material potential conflict of interest or impacts the content of its research or publications.

Earnings Don’t Matter, Episode 9

In yet another installment of It’s Not About The Numbers Stupid, we present Qualcomm (NASDAQ:QCOM) earnings.

This earnings season speaks volumes about how sentiment has shifted in the market from unceasingly bearish last year to largely bullish this year so far. While mavens will have it that there’s an earnings crash coming, and with that will go the indices, thus far we can say that, yes, earnings have been weak (Tesla (TSLA)), poor (Microsoft (MSFT)) and downright awful (Intel (INTC)) but none of this has mattered too much to stocks.

Qualcomm reported last week and again the numbers were unimpressive – and the guide for their fiscal Q2 (that’s the quarter ending 31 March 2023) was both a wide range and at the midpoint another negative growth quarter.

Here are the numbers.

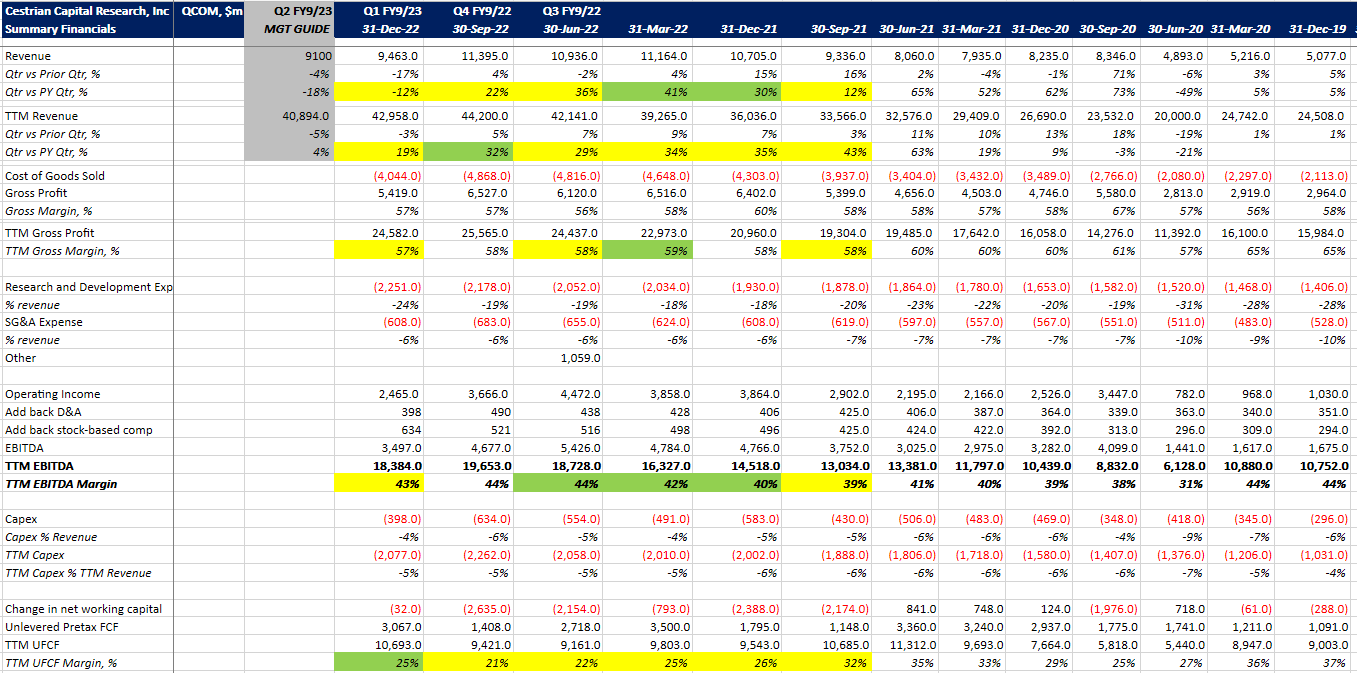

QCOM Fundamentals I (Company SEC filings, YCharts.com, Cestrian Analysis)

QCOM Fundamentals II (Company SEC Filings, YCharts.com, Cestrian Analysis)

A few highlights:

- Revenue growth was negative at -12% vs. the same quarter last year, and the guide at the midpoint is for -18% growth next quarter vs. the same period last year. That implies just 4% TTM revenue growth by next quarter.

- Gross margin is holding up fine at 57% (at Intel, gross margin is in freefall).

- TTM EBITDA margins strong at 43%

- TTM unlevered pre-tax FCF margins also strong and indeed improving at 25%, a result of very low capex and very strong working capital management in the quarter.

- Balance sheet remains perfectly fine at 0.5x TTM EBITDA by way of leverage and just shy of $5bn in liquid cash on hand.

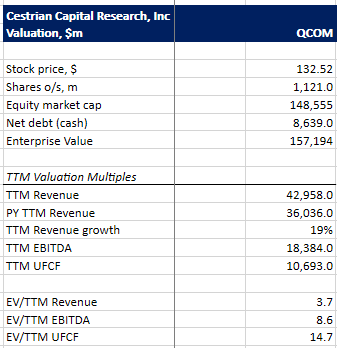

Valuation stands as follows:

QCOM Valuation Analysis (Company SEC filings, YCharts.com, Cestrian Analysis)

If QCOM’s fortunes are to reverse and growth tick back up again, then paying sub 15x UFCF for this name isn’t so bad.

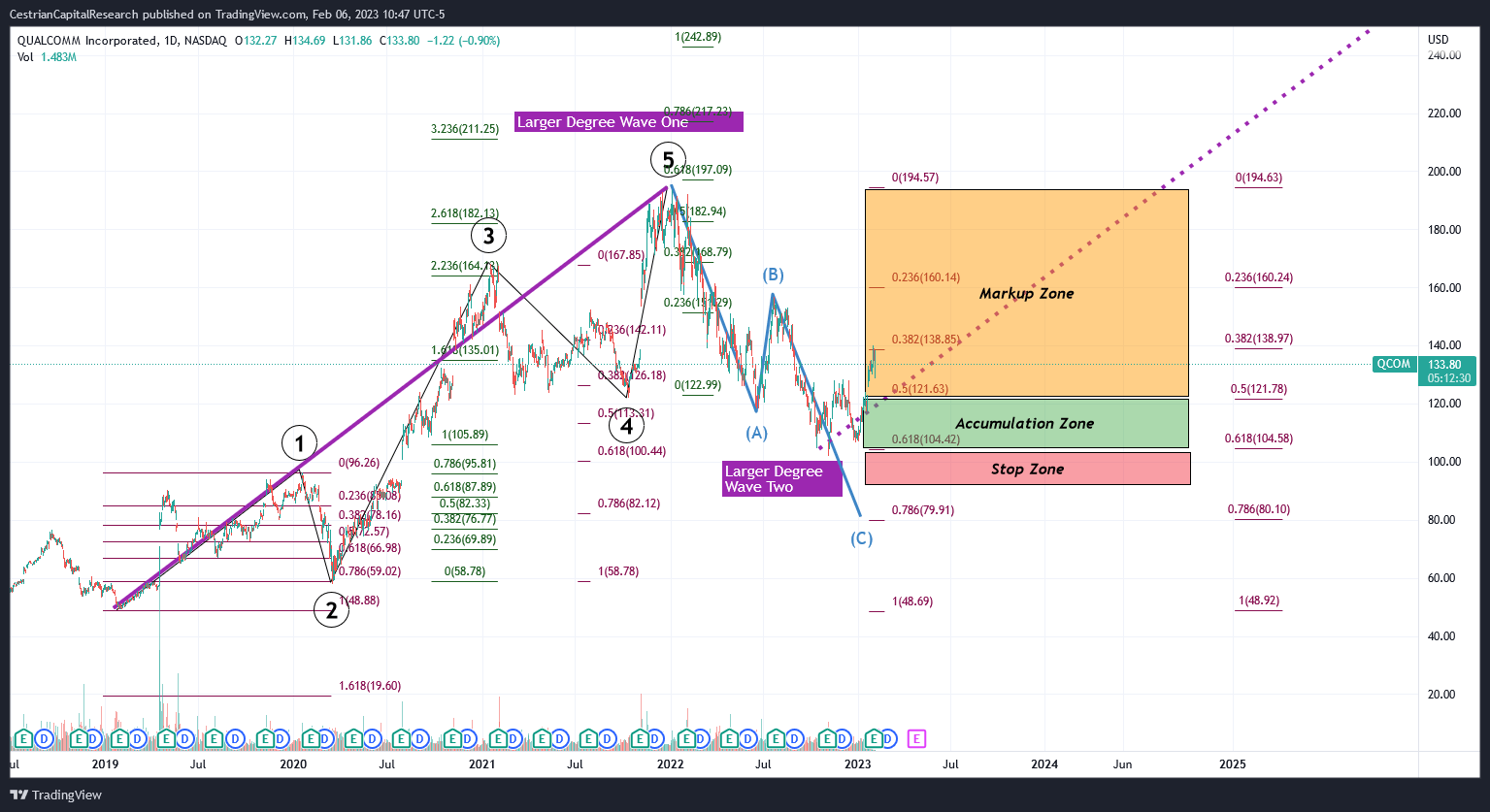

Let’s see what the stock chart may tell us. (You can open a full page version, here).

QCOM Chart (TradingView, Cestrian Analysis)

First of all, apologies for the explosion in a crayon factory above. But the detail is instructive, because it tells us that QCOM stock trades rather nicely to technical levels (which may mean it continues to do so … in which case one can make some informed guesses about where this next leg higher may end).

Like this:

- From the 2018 lows, QCOM puts in a 5-wave-up cycle peaking in late 2021, forming a larger-degree Wave One up. Those 5 waves up trade really well to typical Fib levels – .786 retrace into the COVID crisis Wave 2 down, a 2.236 extension up into the early 2021 Wave 3 highs, a .382 retrace into the 2021 Wave 4 lows, then the Wave 5 peaking right around the .618 extension of Waves 1+3 combined. This is fairly textbook stuff.

- Then we see a larger degree Wave Two down by way of that A-B-C correction, with the Wave Two finding support at the .618 retrace of that larger degree Wave One.

- Now we believe the stock to be in a larger-degree Wave Three up which should at least hit a new all-time high and more likely pass way up beyond that.

For now we believe the ideal risk/reward zone (our ‘Accumulate Zone’) is in the rear-view, though it’s not out of the question that the stock could revisit this band (between around $105-122) before moving higher once more.

We rate at Hold in anticipation of late money coming in to bid the stock up and push it to new all-time highs.

Cestrian Capital Research, Inc – 6 February 2023.

Be the first to comment