EtiAmmos

Thesis

The Quadratic Deflation ETF (NYSEARCA:BNDD) is the sister fund of the Quadratic Interest Rate Volatility and Inflation Hedge ETF (IVOL). BNDD is supposed to offer investors a positive return during deflationary times:

The Quadratic Deflation ETF is a fixed income ETF that seeks to benefit from lower growth, deflation, lower or negative long-term interest rates, and/or a reduction in the spread between shorter and longer term interest rates by investing in US Treasuries and options. As a secondary goal, the Fund seeks to adhere to Environmental, Social and Governance (“ESG”) principles by excluding investments in issuers that are involved in and/or that derive significant revenue from, certain practices, industries or product lines and by increasing the representation of underrepresented groups in the governance of ETFs. The Fund is actively managed and does not track an index

If an investor does no work and just goes by the bombastic fund names, then it should buy IVOL when inflation is supposed to increase, and get into BNDD during deflationary times:

Deflation is when consumer and asset prices decrease over time, and purchasing power increases. Essentially, you can buy more goods or services tomorrow with the same amount of money you have today. This is the mirror image of inflation, which is the gradual increase in prices across the economy.

However, both funds have long bond positions in their composition, and funnily enough BNDD is the one that has taken a correct positioning in CMS flatteners. BNDD has managed to outperform significantly its main component, the Vanguard Long-Term Treasury ETF (VGLT), and shockingly has outperformed IVOL in the past six months.

The fund manager has made sure the names of the funds are very bombastic but disconnected with reality. An investor would have fared better in the past six months by adding a deflation protection fund to their portfolios rather than an inflation one.

Composition/Holdings

The fund has a dual factor composition:

Composition (Annual Report)

Most of the vehicle is invested in the Vanguard Long-Term Treasury ETF, while a small portion of 6.9% is constituted by bought options on the 2Y-30Y spread relationship in the Treasury curve. We will get into that a bit more below.

1) First Risk Factor: the Vanguard Long-Term Treasury ETF

- Is a long Treasury bond index

- Includes U.S Treasuries with a maturity of 10 years or more

- Currently has an average effective maturity of 23.4 years

- It represents a long duration bond fund

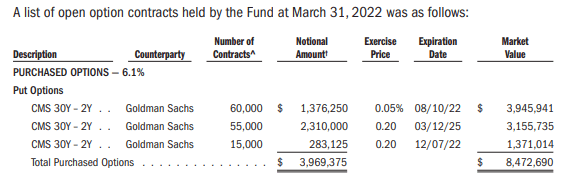

2) Second Risk Factor: bought options on the 2Y-30Y spread relationship

- The fund bought CMS options from Goldman Sachs on the 2Y-30Y spread relationship

Option Holdings (Annual Report)

- The Annual Report does not outright identify the taken position (flattener or steepener), but from the fund description above and its performance versus VGLT outright, we are of the opinion that it was a flattener – i.e. the fund was betting the net yield in 2Y Treasuries versus 30Y Treasuries is going to converge

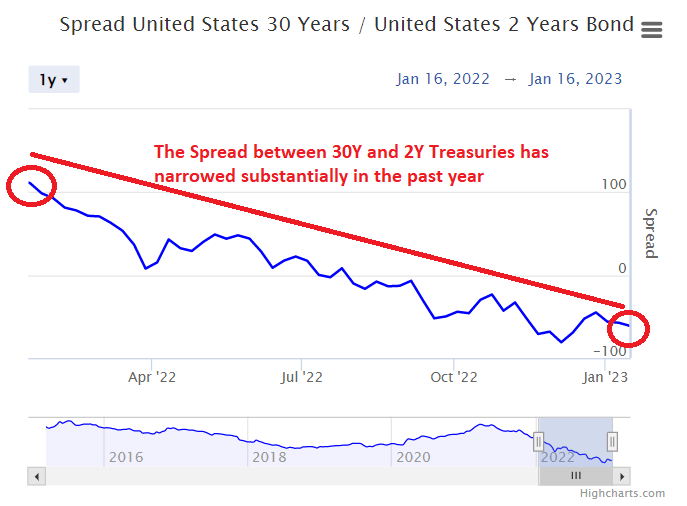

CMS Spread (WorldGovernmentBonds)

- The 2-year U.S Treasury yield is now higher than the 30-year one, due to a substantial curve inversion

- The shape of a yield curve in a normalized environment is upward sloping, with the concept of term premium embedded in the respective slope

Performance

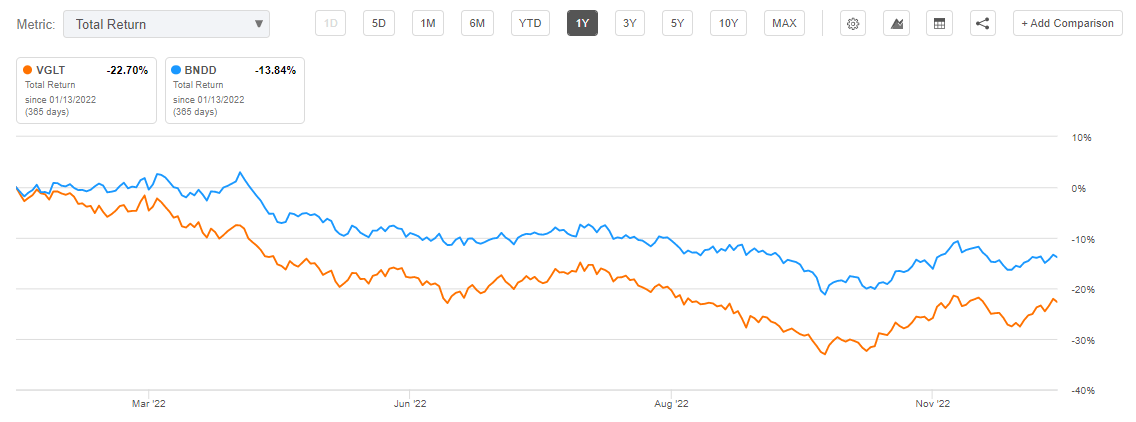

The fund is down substantially in the past year:

Total Return 1 Year (Seeking Alpha)

BNDD is down over -13% in the past year, but has outperformed an outright full VGLT position (its main holding). The reason for this outperformance seems to be the positioning in the 2Y-30Y CMS options. The options seem to have been betting on the spread to narrow, and it has gone negative.

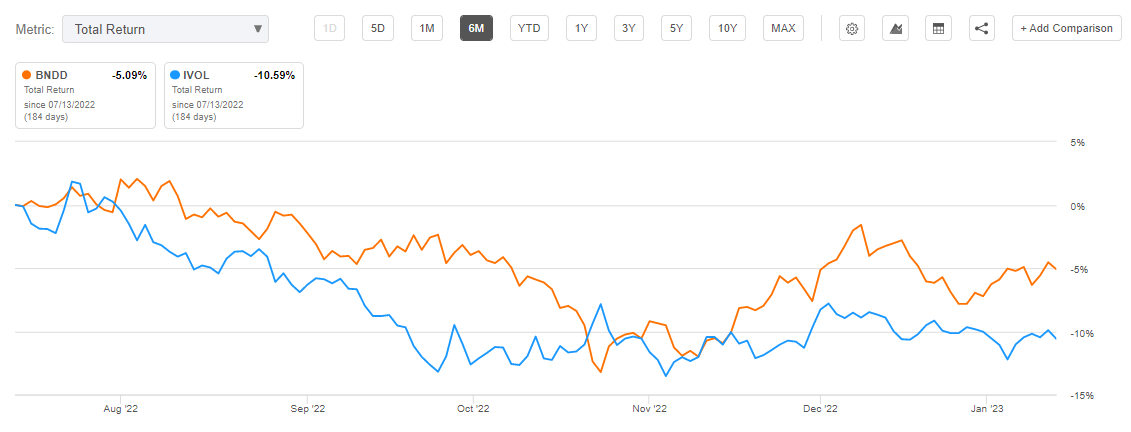

However, what is very interesting to us is the relationship between this ‘deflation’ fund versus its ‘inflation’ peer (IVOL) which we covered here:

Total Return 6-Months (Seeking Alpha)

We can see that BNDD has outperformed by a substantial amount in the past six months. So let us frame this in English – in a highly inflationary environment like today’s, a ‘deflation’ fund has massively outperformed an ‘inflation’ one. Maybe the fund manager should think about switching names between the two!

Ultimately both funds are long U.S. Treasuries (outright or inflation protected), and take a position in the spread of two points in the curve. BNDD has outperformed due to the correct positioning on the 2s30s CMS options, while IVOL has underperformed due to the erroneous 2s10s positioning.

Conclusion

The Quadratic Deflation ETF seeks to benefit from lower growth, deflation, lower or negative long-term interest rates, and/or a reduction in the spread between shorter and longer term interest rates. The fund has a dual factor composition, with most of the holdings invested in a long U.S. Treasuries bond fund, namely VGLT. VGLT is long Treasuries with an effective maturity of 23.4 years, and has been pummeled in the past year. BNDD has managed to outperform VGLT by its 2s30s options position, with the spread between the two points in the curve going into negative territory in the past year. What is more shocking is that the ‘deflation’ fund BNDD has managed to significantly outperform its sister ‘inflation’ fund IVOL in the past six months.

The takeaway here is that a retail investor needs to understand the build of a fund by reading relevant name specific research (ideally ours) and not go by the nameplate bombastic fund name. It can be very misleading as we have seen above. We feel most of the curve move for this monetary cycle is over, and BNDD will have a positive performance in 2023 driven by the long bond position via VGLT. Please read our encompassing view on the long end of the curve here. Depending on what the fund manager does on the 2s30s position, that could be a detractor (we feel the curve will not stay inverted for too long).

Be the first to comment