Pgiam/iStock via Getty Images

4Q Estimates & Consensus Ratings For 31 Big Banks

This post covers 31 big banks.

31 Large Banks (Ycharts)

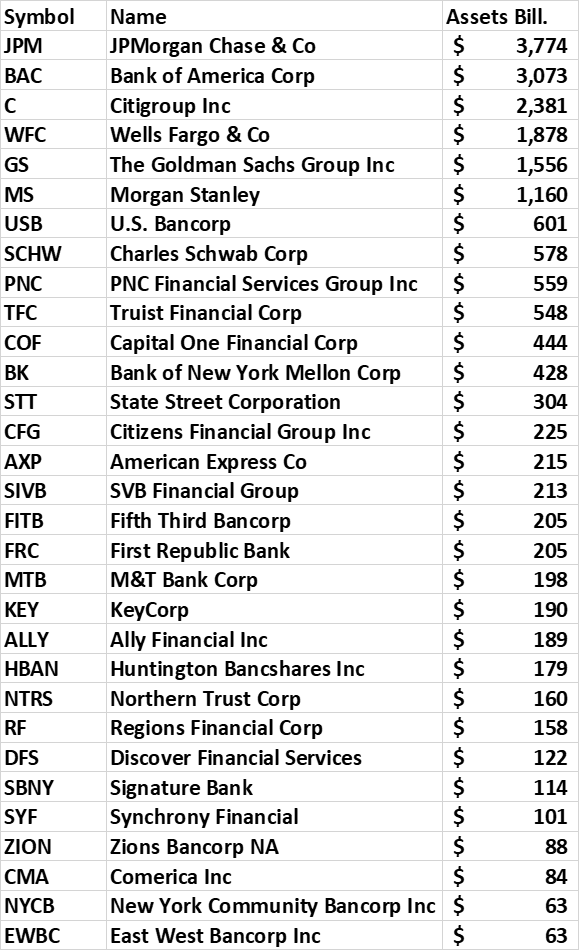

Analyst Coverage

Bank analysts heavily follow these big banks. The largest three are especially popular among Seeking Alpha writers who have rendered the following number of opinions over the past 30 days: JPM 16, BAC 15, and Citi 15.

Analyst Coverage (Ycharts)

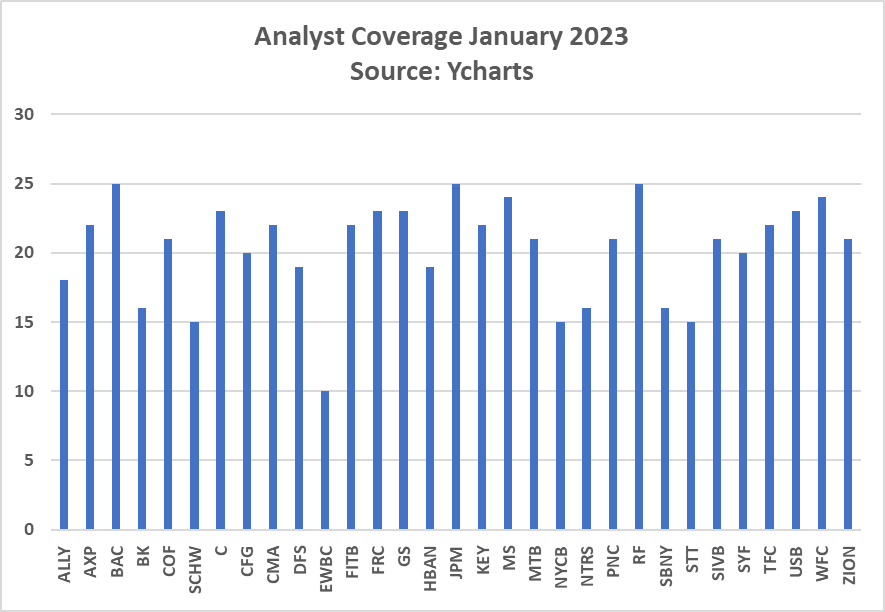

4Q analyst EPS Estimates Cheat Sheet

This coming Friday is a big day with JPMorgan Chase & Co. (JPM), Bank of America Corp (BAC), Citigroup Inc. (C), and Wells Fargo & Co (WFC) reporting.

Morgan Stanley (MS), and The Goldman Sachs Group, Inc. (GS) report January 17, followed the next day by PNC Financial Services Group, Inc. (PNC) and Charles Schwab Corp (SCHW). Truist Financial Corp (TFC) is scheduled to report on January 19. The last of the big ten banks to report 4Q earnings will be U.S. Bancorp (USB) on January 25.

Est EPS 4Q 2022 (Ycharts)

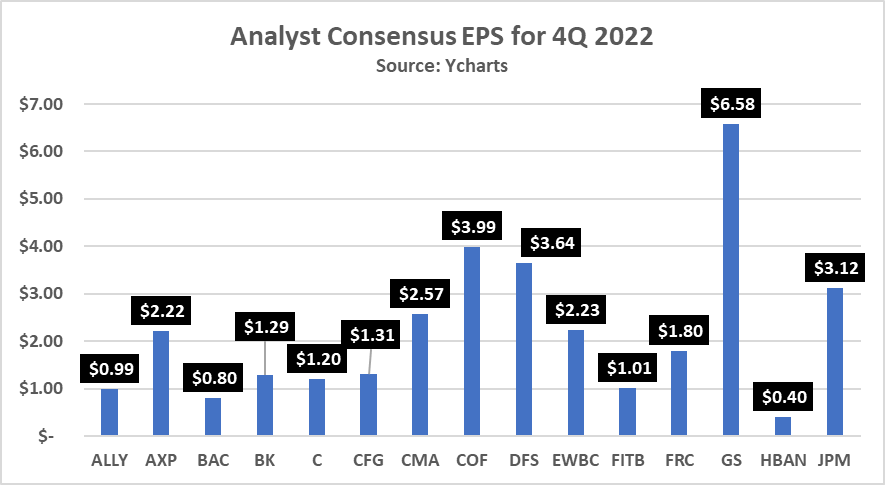

EPS Est. 4Q 2022 (Ycharts)

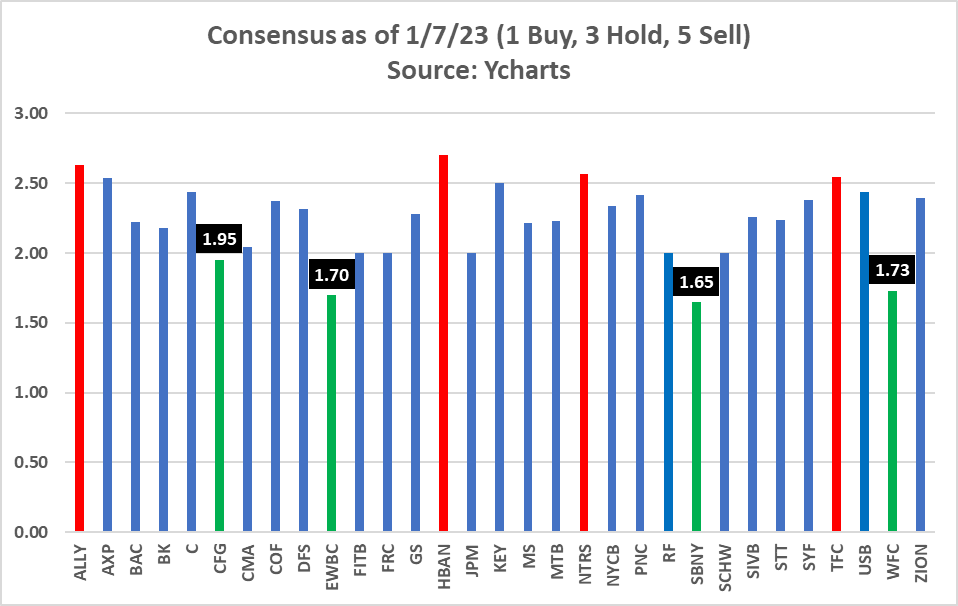

Consensus Opinions

Analysts’ favorite banks are Signature Bank (SBNY), East West Bancorp, Inc. (EWBC), Wells Fargo, and Citi.

Consensus (Ycharts)

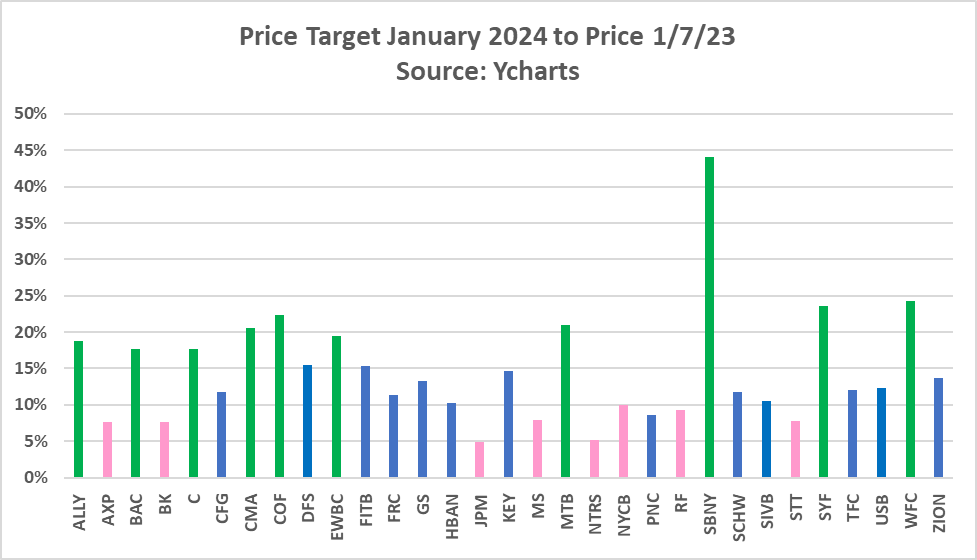

Price Targets January 2024

This next chart, at least theoretically, is the money chart. It shows consensus (average) price target one year from now as a percentage of a bank’s current price. Several key observations:

- Analysts expect all banks to show stock price appreciation a year from now.

- Median price improvement is 12%, average is 15%.

- Leading the way are Signature Bank, Wells Fargo, and Synchrony Financial (SYF).

- Expected bottom dwellers for the year ahead are Northern Trust Corp (NTRS) and JPMorgan Chase.

Jan 24 Price Target to Jan 23 Price (Ycharts)

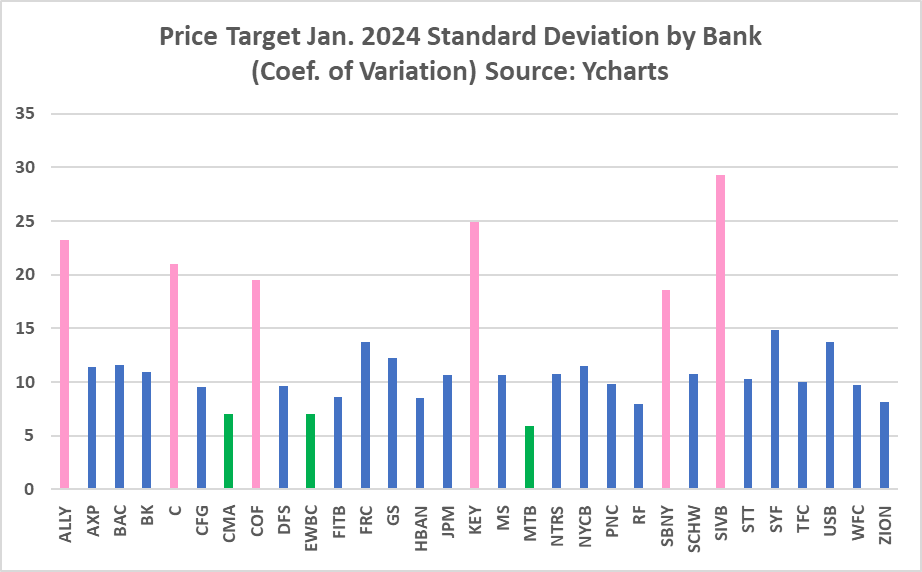

Beware: Lack of Consensus in the Consensus

I take the foregoing with a grain of salt for two reasons:

- Analyst consensus top picks in the past couple of years have been notoriously poor, a theme I may cover in an upcoming article. I say that not to pick on the analyst community, but to underscore how difficult it has been to predict bank earnings and stock price movement since COVID struck in its full fury during the first half of 2020. Some readers may recall that I analyzed the accuracy of bank analyst picks covering 2016-2020. Here is a link to that article.

- Perhaps even more important from an investor perspective, it is critical to realize just how little “consensus” there is in the consensus as the next chart shows. I have examined this theme in the past, and I do not recall seeing such a wide disparity in price targets (i.e., coefficient of variation) among bank analysts as we see in January 2024.

Banks noted with green bars show a fairly tight range of price target forecasts: M&T Bank Corp (MTB), East West, and Comerica Inc (CMA).

The banks noted with red bars show the widest variation. At the top of the list is one my long-time holdings, SVB Financial Group (SIVB). Following SIVB are three highly volatile banks (i.e., high beta): KeyCorp (KEY), ALLY Financial Group (ALLY), and heartbreak Citi.

Std. Dev. Price Targets Jan. 2024 (Ycharts)

Speaking of heartbreak, ALLY did just that to me during the first half of 2022 when I ambitiously sold Puts a couple times, a move I chronicled on these pages in February 2022. Not a good move as it cost me a pretty penny when I finally threw in the towel in June.

I suppose that’s my punishment for deviating from my investment policy of only investing in high-quality (banks with double-digit Risk-Adjusted Return on Equity). I am doubly troubled by my move since I had correctly warned myself (and other bank investors) in October 2021 to steer clear of banks having consumer loan concentrations and volatile funding. That said, the buybacks and capable management lured me in. My bad.

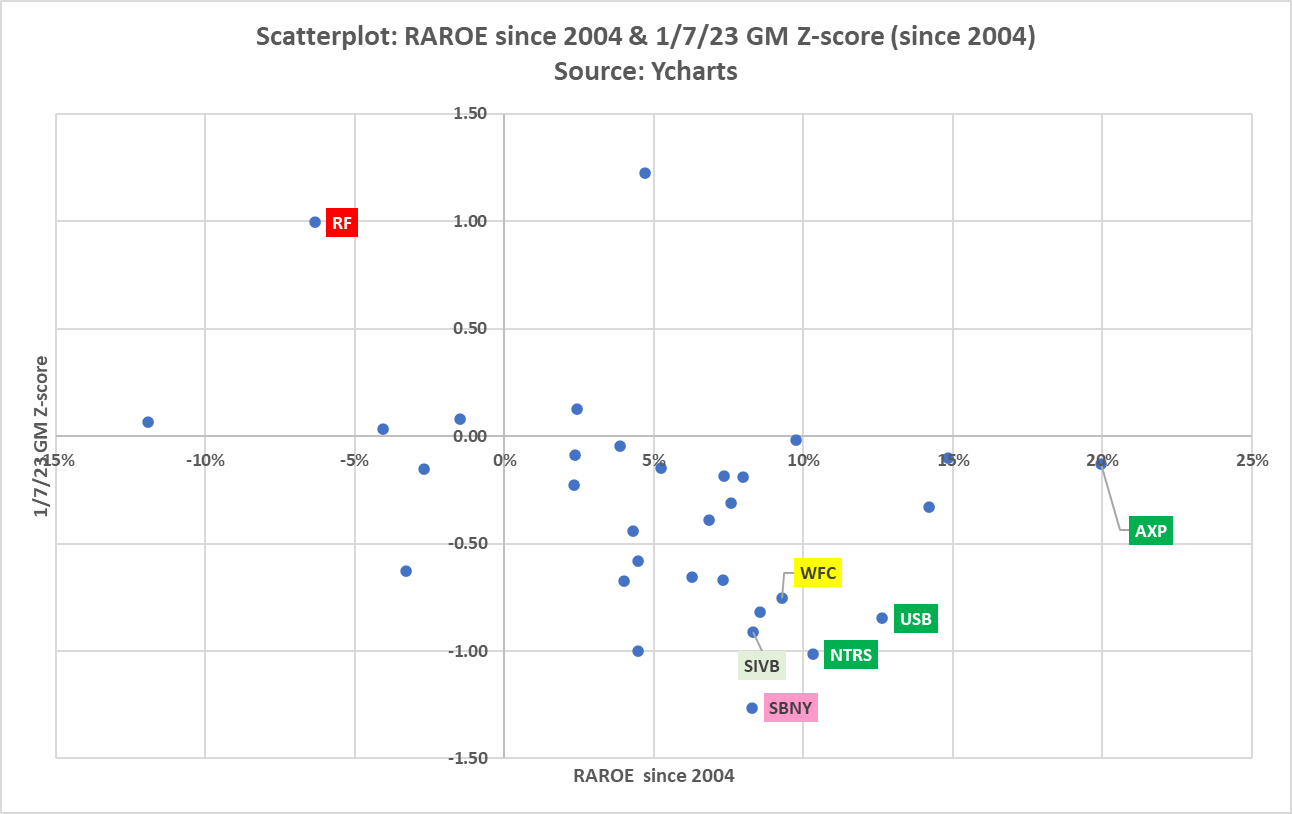

Favorite/Least Favorite Bank Investment

I am sticking with high-quality banks and avoiding banks mostly geared to the business cycle.

The scatterplot below shows two data points: X-axis the Risk-Adjusted ROE calculated as the average rolling four-quarter ROE by quarter since 2004 minus the standard deviation; the Y-axis is the January 2023 Z-score which is calculated as the product of the quarterly Price/Earnings ratio and Price/TBV since 2004.

Three banks look interesting: Northern Trust Corp (NTRS), USBank, and American Express Co (AXP). American Express is now on my watch list given its superior earnings history. Its forward P/E is close to 15x, which is modestly lower than its 20-year and 10-year average P/E of 17x. I will need to monitor AXP this year before buying.

RAROE and GM Z-score (Ycharts)

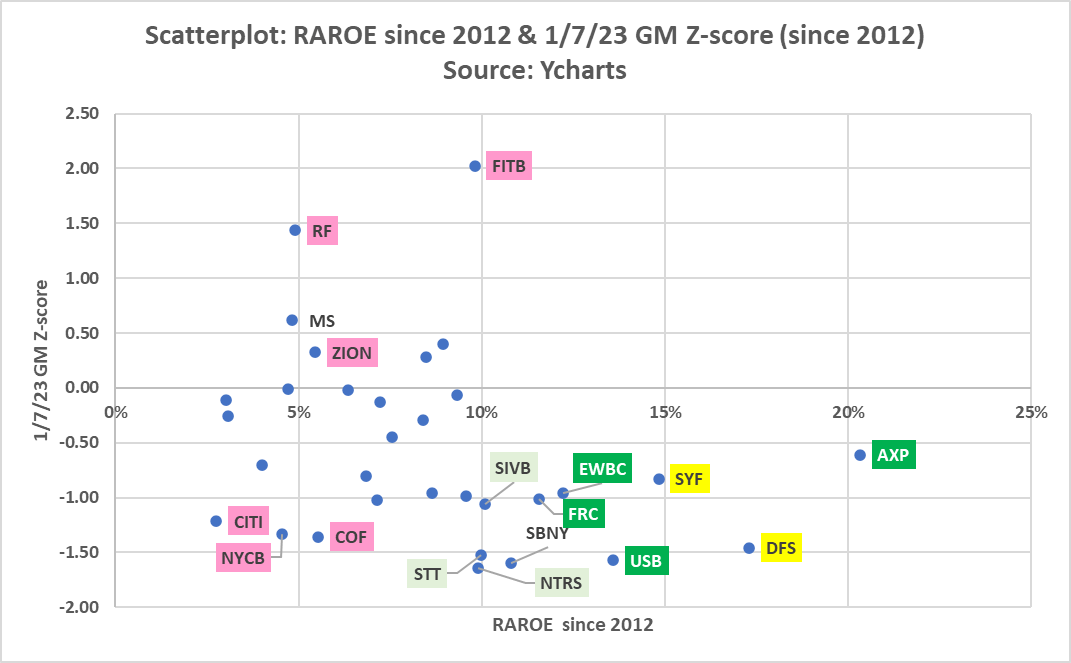

This next scatterplot is the same as the prior but, in this case, data covers 2012-2022.

The disadvantage of this view is that it excludes the harsh down-cycle of 2008-2009.

One advantage is that it includes banks like First Republic Bank (FRC), another long-time holding, which went public since 2010. Another advantage is that it gives some banks the benefit of the doubt; by that I mean, some banks have changed their business models, and presumably, are less vulnerable to a downcycle in the economy than they were in 2008-2009.

American Express, again, stacks up well on this chart as does USBank, East West, and First Republic. Card issuers, Synchrony Financial and Discover Financial Services (DFS) look downright cheap given their 10-year superior RAROE. But both are geared to the consumer, and I remain cautious as the economy is at risk of slowing and ultimately going into a recession.

RAROE & GM Z-score 2012-22 (Ycharts)

Buying BAC.PL and First Republic

Over the past month, I have nibbled on First Republic (<$120) and a Bank of America Preferred (BAC.PL) under $1200. My most current view of Bank of America was covered in September. I see both as long-term holds.

I am not selling banks at this time, but I am cautious, and conservative given where the Fed seems to be trying to take the economy.

Banks I am avoiding are the “have not” banks, those being banks with expensive, volatile funding and relatively high loan-to-deposit ratios. That said, at some point, probably this year, some of these banks may become attractive as turnaround opportunities. The best example is probably Capital One Financial Corp (COF), a bank I labeled a “Strong Sell” in September 2021 when it was selling for $157, not far from its Covid-induced high of $170+.

Big Questions

Heading into earnings calls this week, several questions are top-of-mind:

- Credit Quality? Examining Provision is always my first order of business.

- Funding Costs? Impact on net interest margin for the “Have” and “Have Not” banks.

- Unrealized Losses on Investment Securities? A huge issue for some banks, a big influence on ROE calculations, and possibly on EPS.

- Loan Growth? 2022 finally broke the long spell of moribund lending. But could that recent growth come back to haunt some banks in 2023-24?

Caveat

The foregoing is my opinion which I share for the purpose of getting feedback and questions that challenge my ideas and assumptions.

Every investor needs to do his/her own due diligence before investing as well as determine their risk profile. I am risk-averse, preferring to invest in the nation’s best banks which reliably earn returns exceeding cost of capital.

Be the first to comment