James Pintar/iStock via Getty Images

By Alex Rosen

Strategy

PXJ, through its index the Dynamic Oil Services Intellidex Index, evaluates companies using multiple criterium, including: price momentum, earnings momentum, quality, management action, and value.

According to the fund prospectus, the index is composed of stocks of 30 U.S. companies that assist in the production, processing and distribution of oil and gas. The index may include companies that are engaged in the drilling of oil and gas wells; manufacturing oil and gas field machinery and equipment; or providing services to the oil and gas industry, such as well analysis, platform and pipeline engineering and construction, logistics and transportation services, oil and gas well emergency management and geophysical data acquisition and processing.

The fund and the index are rebalanced and reconstituted quarterly in February, May, August and November.

Proprietary ETF Grades

-

Offense/Defense: Offense

-

Segment: Industries

-

Sub-Segment: Oil Services

- Risk (vs. S&P 500): Very High

Proprietary Technical Ratings

-

Short-Term (next 3 months): B

-

Long-Term (next 12 months): B

Holding Analysis

PXJ, through its index, holds a basket of 30 individual stocks. The fund is entirely made up of U.S. companies, with a heavy weighting toward small cap value (27%) and small cap blends (35%). The largest sector by far is industrial services, which accounts for 62% of the total fund holdings.

Individually, the fund’s largest holdings are Halliburton (HAL) at 5.6%, Baker Hughes (BKR) at 5.4%, Schlumberger (SLB) at 5.3%, and TechnipFMC (FTI) at 5.3%.

Strengths

Long have we heard the stories of America’s crumbling infrastructure: bridges collapsing or on the verge of collapsing, tunnels leaking, an inadequate rail system, inner city streets over run with traffic. The list goes on. These areas are neglected, in part, because they aren’t profitable. The ROI of a bridge is small, and thus it is left to the government to build and maintain. Outside of the North East Corridor, Boston to Washington D.C., the passenger rail system is a big money suck. Amtrack admits to annual losses of $1 billion.

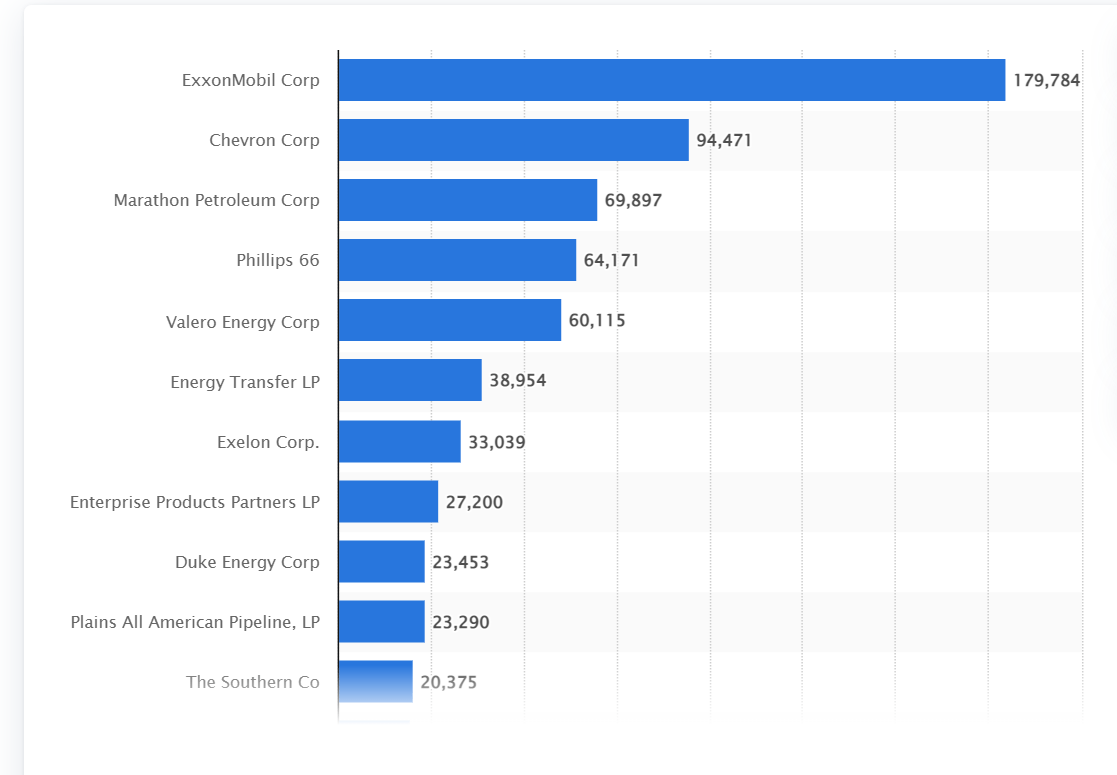

However the Energy Sector, with its billions and trillions in revenue, will do everything in its power to ensure that the operations run smoothly. The demand for U.S. energy exports is at an all-time high. With sanctions on major energy producers like Russia and Iran, instability in Venezuela and Nigeria, and capacity limits in Norway and the Middle East, the world is looking to the U.S. to help minimize the crisis and ease the demand burden.

U.S. energy infrastructure companies have heard the call and are working as fast as they can to meet that demand. Buoyed by a mass influx of cash, investment in the sector is expected to increase for at least the next ten years.

Record Revenue for U.S. Energy Sector Companies (Statista.com)

Weaknesses

The mass investment in Energy Infrastructure, especially fossil fuel infrastructure, is predicated on a continued increase in global demand. That increase is in part caused by sanctions and instability. The truth is, there is no shortage of oil and gas in the world. The shortage may be temporary, as the world has to choose between punishing so called bad actors, and providing affordable energy for its people.

The oil and gas industries’ ability to respond to sudden fluctuations in the demand curve is not a two way street. Once the taps are opened, it is very hard and expensive to close them. New infrastructure has to be used, or it becomes a drain on the books. If tomorrow demand decreases, the companies can’t just magically make all those new wells and platforms disappear. LNG plants don’t just shut down overnight. They need to be maintained and protected.

Opportunities

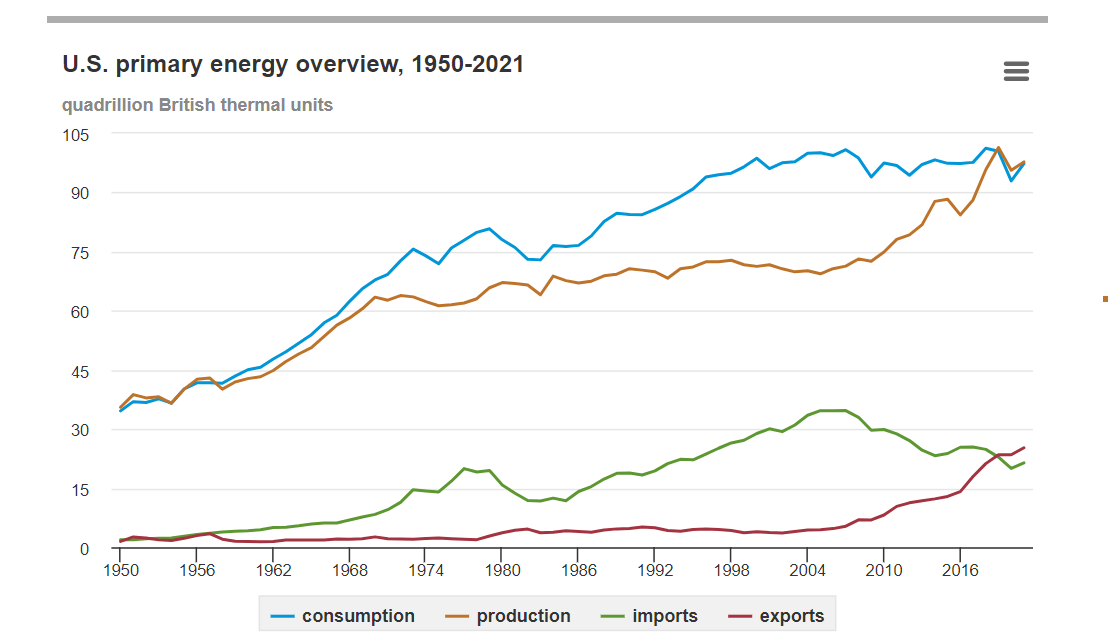

Right now, the demand is there, and the industry is responding to it. After suffering a prolonged slump due to COVID, the oil and gas industry is back with a vengeance. Combine that with the boycott of Russian gas and it is easy to see where the opportunity is. For the foreseeable future, demand will continue to remain high, and that will necessitate an expansion of the sector in the U.S. In 2019, the U.S. crossed over from net importer to net exporter, and while in the near future that may not continue, over the long term, the U.S. will be a net exporter.

U.S. becomes a net exporter of Energy (U.S. Energy Information)

Threats

Overproduction is always a risk in the Oil and Gas sector. Unforeseen events such as another global pandemic or a sudden change in political policies in Venezuela could suddenly cause the bottom of the market to fall out again. The industry is very volatile. The past ten years look like a roller coaster, with giant peaks and epic drops. Today’s response to demand could very easily look like tomorrow’s shuttered oil fields.

The wild ride that is oil prices over the past 25 years. (tradingconomics.com)

Conclusions

ETF Quality Opinion

Right now, demand is high, and PXJ is well positioned to capture the upside. The index is actively managed and rebalanced quarterly, so the likelihood of it being stuck with individual losers is small. As long as the external conditions remain the same, PXJ’s fundamentals will make sure it looks attractive to investors

ETF Investment Opinion

As mentioned above, the oil and gas market is extremely volatile. What was expected to be a record winter for oil prices has not quite been realized. Profits are still up, but they have definitely come off the highs of early 2022 as the worst fears about demand have not actually become a reality. For the time being, we rate PXJ a Hold, as we wait to see what happens in the Urals with Russia and Ukraine. If the war persists and drags other actors into it, then we might want to revisit this and move in a more bullish direction.

Be the first to comment