Robert Way/iStock Editorial via Getty Images

PVH Corp. (NYSE:PVH) is a fashion conglomerate. The company owns the Calvin Klein and Tommy Hilfiger brands.

This article covers the company’s 1Q24 results and earnings call. The results showed revenues down 10%, particularly in wholesale, Europe, and Tommy Hilfiger. This was expected based on the company’s previous guidance, and PVH beat consensus in revenue and EPS. On a more positive note, margins were up, and EBIT was up compared to the same quarter last year despite lower sales. The company raised its EPS guidance for the year to $11 to $11.25.

This is also my first article on PVH. I believe the company has several quality characteristics: high brand equity, a good focus on intangibles, a diversified global revenue base, and a good strategy for this challenging macroeconomic period. On the other hand, its financial leverage is a little high, and the company seems to have exhausted its growth avenues.

In terms of valuation, I think PVH’s is attractively priced. The company trades at a P/E of 11x on the low range of its FY24 guidance. This is generally an attractive multiple for a company of PVH’s characteristics. Furthermore, the company’s earnings have room for improvement if the macroeconomic conditions improve, particularly in Europe.

Challenged 1Q24 results, in line with expectations

PVH’s results for 1Q24 were not good, with revenues down 10%.

About 3% of that decrease was generated by the sale of a group of small brands (Warner’s, Olga, and True&Co) in late 2023.

The remaining decrease was concentrated in Tommy Hilfiger International (down 14% YoY), particularly in Europe. Europe’s macroeconomy is challenged, and PVH is trying not to become overly promotional, which impacts its sales but helps maintain margins. The company calls this strategy maintaining the “quality of sales.” Although the results in Europe might be macro-driven, the company also announced the removal of its Tommy Hilfiger Global CEO and PVH Europe President, indicating that some of the problems might be generated internally.

Calvin Klein, on the other hand, saw flat revenues, with growth in North America (4%) offset by lower International sales (down 2%).

The wholesale channel was the most impacted, with revenues down 17%, again impacted by the sale of brands (6%) and Europe. In the case of Europe, PVH had determined that it would decrease the availability of its products in digital marketplaces (4Q23 call).

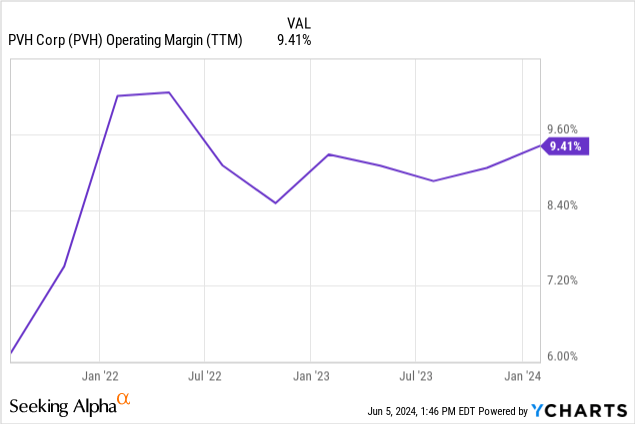

On the profitability front, things looked much better. Gross margins were 350 basis points higher, which is understandable given the decrease in the wholesale channel. Inventories decreased 22%, indicating a healthy outlook for future quarters. SG&A was $50 million lower than last year, which meant that despite the decrease in sales, EBIT was higher this quarter ($205 million) than last year ($198 million). The margin improvement was particularly strong at Calvin Klein, which, despite flat revenues, increased EBIT by 30%. This was offset by a 25% decrease in Tommy Hilfiger’s profits.

Looking ahead, the company is still expecting challenges in Europe and wholesale. Management commented on the call about the Fall 2024 order book being down, blaming wholesale cautiousness. The company expects an improvement by the Spring 2025 collection, which should impact revenues in late 2024 and early 2025.

A leader apparel company

In this section, I review some of the aspects I like and don’t like about PVH.

Leading brands: Calvin Klein and Tommy Hilfiger are leading global apparel brands. An indication of this is that the brands have close to 45 million followers on Instagram. This is a figure similar to Ralph Lauren, with close to 60 million followers across brands and platforms.

Global footprint: 65% of PVH’s revenues (according to their FY23 10-K) were generated outside the U.S. This evidences that the brands have global appeal. The company does not disclose how much of its International revenue is generated in Europe versus Asia, but given the challenges in 1Q24, it appears that Asia is still less developed.

Great brand investments: A fashion company has to invest in the brands, or it will lose cultural relevance. I believe PVH is investing in the right intangible assets. You can see some of the celebrities they have hired to promote their collections on their investor relations website. For example, last year, Calvin Klein made a campaign with Jeremy Allen White before he was awarded Best Actor in many film festivals for his participation in The Bear. This year, Tommy Hilfiger went to the Met Gala, an important fashion event, accompanied by the K-Pop group Stray Kids, who has 30 million Instagram followers. Other recent collaborations include Jennie Kim, Jung Kook, Kendall Jenner, and Zendaya. The company recently named a new Creative Director for the Calvin Klein Collection, and announced that the brand would return to hosting runway shows next year.

Low growth potential: I believe apparel brands can saturate their markets at some point, which seems to be the case for PVH already. The company’s growth slowed down in the mid-2010s. Avenues for growth are limited. Expansion to DTC generally can increase revenues, but may not translate to operating profits. According to PVH’s FY23 10-K, about 50% of their sales already come from DTC. The international markets also seem to have been exploited, with 65% of revenues coming from there. Finally, the company is recovering some licenses (like outerwear from G-III Apparel), but just like DTC, this movement can increase revenues but not necessarily operating profits.

A little leveraged: As of 1Q24, PVH had $2.15 billion in long-term debts against only $346 million in cash. This level of leverage is high for an apparel company because apparel is highly non-discretionary and suffers from operational leverage. The company mentioned a refinancing on the 1Q24 call, but without mentioning the terms. The refinancing bonds are the 2029 unsecured green bonds issued in April, with a 4.125% coupon. The proceeds were probably used to redeem the 3.625% 2024 bonds. These are good refinancing terms, although we will need to wait for the 1Q24 10-Q to find the effective yield (inclusive of face value discounts). The company still has to repay or refinance $500 million, maturing in 2025, with a coupon below 5%.

Valuation

In the 1Q24 release, PVH’s management reaffirmed their guidance of revenues down 10% for the year (to $8.3 billion), with operating margins of 10.5%. EPS guidance was elevated to between $11 and $11.25 per share.

I believe the company’s guidance is conservative, considering that revenues are expected to decrease and that the guided margin is above TTM operating margins but below 1Q24 margins (already at 11%).

Today, PVH has a market cap of $6.25 billion, which added to about $1.8 billion in net debt, result in an EV of $8.05 billion. Compared to management’s operating income guidance of $870 million, or NOPAT of $696 million (using a guided effective tax rate of 20%), this results in an EV/NOPAT of about 11.5x. A similar multiple arises from comparing a stock price of $123 with a guided EPS of $11 per share or a P/E ratio of 11.2x.

I believe these multiples represent an opportunity. The reason is that PVH has quality characteristics mainly related to the equity of its brands, its correct intangibles investment strategy, and its correct pricing strategy (preferring to lose sales in wholesale than to overly promote its products). These qualities provide for upside opportunity if the macro environment improves, particularly in Europe. The multiple also compensates for the risks of the stock, namely its exposure to a non-discretionary sector such as apparel and its financial leverage.

I generally believe that a company with low long-term growth prospects, capable management, manageable leverage, and stable earnings deserves a multiple of 10x to earnings. In this case, PVH has most of the characteristics above, except for stable earnings. Its multiple is a little higher than 10x as well. However, I believe these are compensated by the fact that the multiple is based on earnings generated during a challenging scenario and that the company has good brand equity.

Conclusion

PVH’s results in 1Q24 showed big challenges in the European and Tommy Hilfiger businesses. Part of the challenges could be explained by the macro and part by company mistakes. PVH replaced its executive for Europe and for Tommy Hilfiger to address these mistakes. On the margin side, a disciplined pricing strategy has allowed the company to protect operating income despite falling sales. I believe this strategy allows the company to recover sales at accretive margins if the economy improves in Europe.

Today, PVH Corp. trades at P/E and EV/NOPAT ratios of around 11.5x, based on the company’s conservative guidance for FY24. I believe these multiples are opportunistic, considering the company’s quality characteristics (namely, high brand equity, good intangible investments, and correct pricing strategy). This low multiple provides upside opportunity in case the macroeconomy improves, and also downside protection if it worsens further.

For that reason, I believe PVH Corp. stock is an opportunity and a Buy at these prices.

Be the first to comment