PonyWang

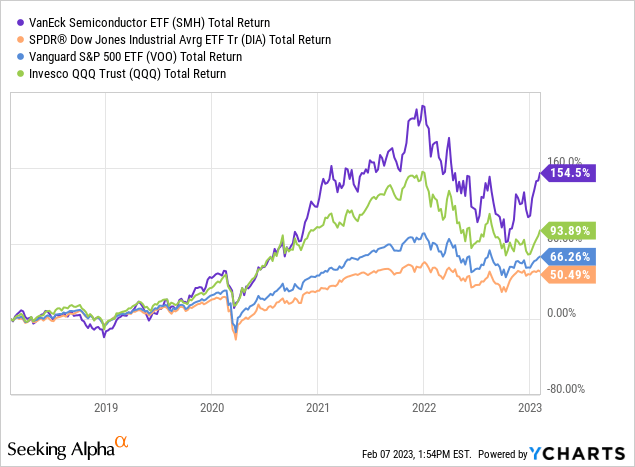

As you may know, semiconductor stocks have come roaring back this year after being mauled by the 2022 bear market. Indeed, the Van Eck Semiconductor ETF (SMH) – frequently cited as the market’s semiconductor “standard” – is up 25%-plus YTD. Whether or not this is simply a bear market rally or has further to go from here, I honestly couldn’t tell you. What I do know is that the semiconductor sector will be one of the most critical and strategically important sectors in the 21st Century and will deliver excellent long-term returns for investors. As proof, consider that over the past five years – and despite the brutal 2022 bear market in semis – the semiconductor sector as measured by the SMH ETF has significantly outperformed the DJIA, the S&P500, and the Nasdaq-100 (as represented by the (DIA), (VOO), and (QQQ) ETFs, respectively):

That being the case, today I’m going to take a look at the Invesco Dynamic Semiconductors ETF (NYSEARCA:PSI). The main difference between the PSI ETF and the SMH ETF is that SMH is a global fund, and holds arguably the best semiconductor company on the planet – Taiwan Semiconductor (TSM). On the other hand, the PSI ETF holds only companies based in the United States. Yet it too has a very strong long-term performance track record.

Investment Theme

In addition to the obvious performance advantages of investing in the semiconductor sector (as shown in the graphic above), another reason is the pervasiveness of semiconductor use across a host of fast growing global markets: EVs, data centers, high-speed networking, 5G smartphones and 5G infrastructure, IoT, high-performance computing (“HPC”), and application specific hardware accelerators to run custom AI/ML algorithms on “big data” – just to name a few.

Now, the semiconductor sector is roughly divided into three categories: Companies that design semiconductors, companies that fabricate semiconductors, and companies that design, build, and service equipment to make semiconductors. A good semiconductor ETF should hold companies in all three categories. With that as background, let’s take a look at the PSI ETF to see how it has positioned investors for success going forward.

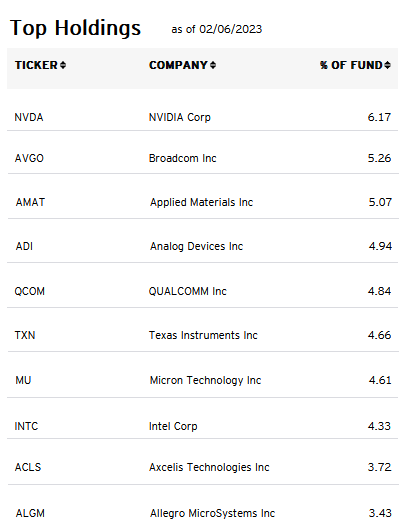

Top-10 Holdings

The top-10 holdings in the Invesco Dynamic Semiconductors ETF are shown below and were obtained directly from the Invesco PSI ETF homepage, where you can find more detailed information on the fund and its holdings. The top-10 holdings equate to what I consider to be a moderately diversified 47% of the entire 30 company portfolio:

Invesco

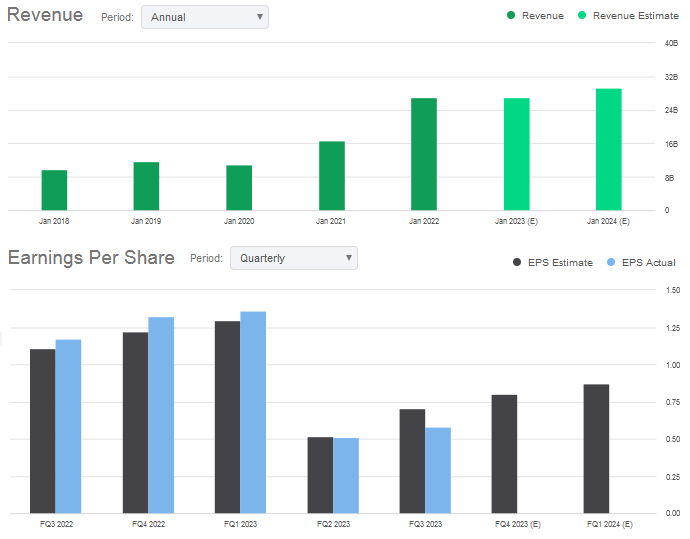

The #1 holding with a 6.2% weight is NVIDIA (NVDA). After a rocketing 54% higher YTD, Nvidia is now only down 10.5% over the past 12 months. That said, the stock – at pixel time trading at $221 – is still down from a high around $334 set back in November of 2021. After a big jump from 2020 to 2020, the company – which designs high-performance semiconductors for the graphics, gaming, AI, and HPC markets – is expected to deliver relatively flat revenue growth for full-year FY23, but is expected to get back on the growth track in FY24:

Seeking Alpha

However, and despite the big pull-back in shares over the past year or two, Nvidia still trades at a relatively rich P/E of 64x forward earnings.

Broadcom (AVGO) is the #2 holding with a 5.3% weight. Broadcom, arguably the global leader in high-speed networking and a leading Apple (AAPL) supplier, is one of my favorite stocks in the entire technology sector. That’s because – for at least the third year in a row – Broadcom has sold out its entire annual capacity at the beginning of the year and CEO Hock Tan famously has instituted a “no cancellation” policy. You make an order with Broadcom, you take the shipment and you pay the bill – simple as that. Add that to the fact that Broadcom is a high-margin free-cash-flow generating machine, and you have the makings of another very good year in 2023.

Broadcom and Apple are likely in negotiations right now considering their last two-year contract is about to expire. Despite the media attention Apple got by claiming it was going to design-out some critical Broadcom components, as I pointed out in a rather popular Seeking Alpha article, Apple will likely find out that designing/testing/verifying complex analog and custom mixed-signal designs will be much harder than the M1/M2 (mostly digital) processor chip designs it has been successful doing in the past (see CEO Shakedown: Hock Tan Vs. Tim Cook). That is, expect Broadcom to soon sign another large and beneficial two-year agreement with Apple that keeps its large product margins relatively intact. Meantime, Broadcom continues to be one of the best dividend growth companies in the entire S&P 500 (annual dividend=$18.40/share for a 3.06% yield). Despite the company’s excellent financial returns, the stock currently trades with a forward P/E of only 14.8x. The stock is a steal here.

Semiconductor equipment makers Applied Materials (AMAT) and Axcelis Technology (ACLS) – in aggregate – have an 8.8% weight in the portfolio. Semi-equip companies should do very well over the coming years as more and more companies are re-shoring new state-of-the-art semiconductor fabs in the United States as a result of the Biden Administration’s CHIPS & Science Act. All these fabs will need new equipment. Meantime, note that Axcelis has doubled since my Seeking Alpha BUY rated article in October of last year (see Axcelis: Bucking The Semiconductor Trend On Strong EV Adoption Of SiC).

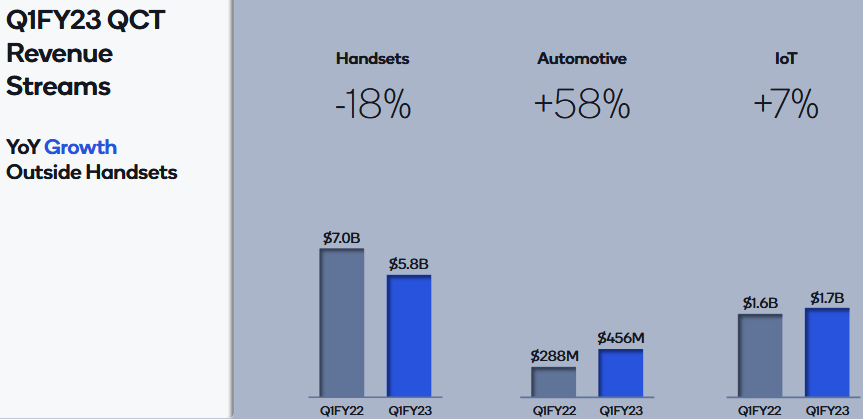

The #5 holding is Qualcomm (QCOM) with a 4.8% weight. Qualcomm released its Q1 earnings report last week and it was arguably a mixed-bag: Non-GAAP EPS of $2.37 was a $0.02 beat, but revenue of $9.46 billion (-11.6% yoy) came in $110 million light. Indeed, QCOM’s strategy to diversify its revenue stream away from handset chips – while improving – still has ways to go:

Qualcomm

As can be seen, QCOM’s automotive segment is growing revenue nicely (IoT much less so), but the 18% decline in handset revenue is still the 100-lb gorilla in the room. That said, the company hopes its recently announced Snapdragon 8 Gen 2 will reverse that slide. QCOM is down 22% over the past year and currently trades with a forward P/E = 14.3x (similar to Broadcom, but without the nice yield). Apple also is attempting to design-out QCOM parts from its iPhones.

The #8 holding, Intel (INTC), has been a complete disaster over the past year (-40%). I predicted this back in February of 2021 (see 2 Reasons Taiwan Semiconductor Has The Jump On Intel). However, as of my last article on PSI in November, Intel was not in the ETF’s top-10 list. That being the case, it would appear the PSI ETF was a buyer of Intel shares on the big dip. INTC now yields 5.1% but could easily see a substantial cut in the dividend sooner rather than later.

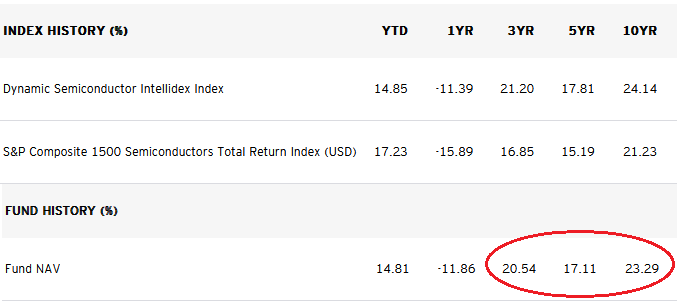

Performance

As mentioned earlier, the PSI ETF has a very strong long-term performance track record. As can be seen below, the three-year, five-year, and 10-year average annual returns are stellar:

Invesco

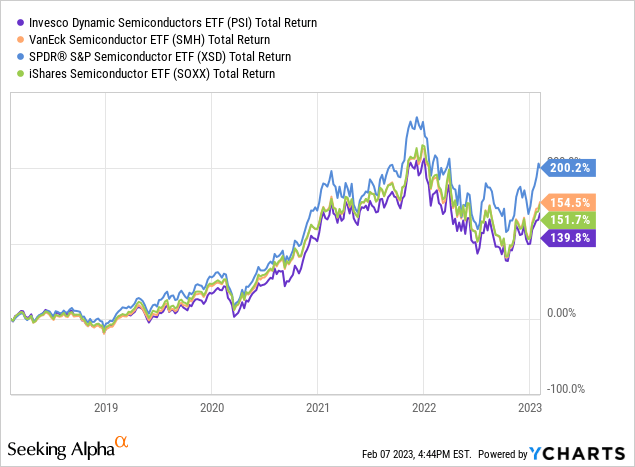

The graphic below compares the PSI ETF’s five-year total returns with that of some of its competitors: the SMH ETF, the SPDR S&P Semiconductor ETF (XSD) and the iShares Semiconductor ETF (SOXX):

As can be seen in the graphic, as good as the PSI ETF has performed, it’s at the bottom of the pile and the XSD ETF has performed much better – with five years returns a whopping 45% higher.

Risks

The PSI ETF is not immune from the global macro-environment: China’s COVID/re-opening, high inflation, higher interest rate environment, Russia’s continuing horrific war on Ukraine, and on-going global supply chain disruptions. On the other hand, Morningstar gives the PSI ETF a five-star rating.

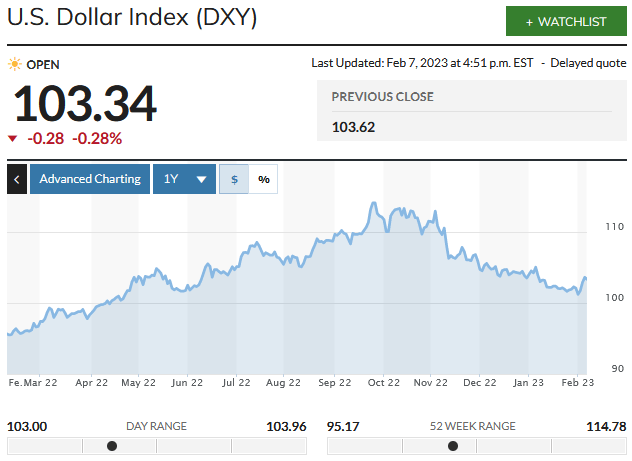

A big risk going forward is that the U.S. Dollar index, after a relatively big decline from its peak last September, turns back higher. This could happen if the Federal Reserve hikes interest rates faster and/or farther and longer than the market otherwise expects:

MarketWatch

Indeed, the bump higher you see on the far right-hand side of the graphic above is a result of the hot-jobs report last week – with the inference that the Fed might have to raise interest rates higher for longer than otherwise would have been expected. This is important because most all of the companies in the PSI portfolio have extensive overseas sales, and if the US dollar is strong, that makes for a big foreign currency headwind when it comes to translating those foreign sales back into their home (i.e. US dollar) currency.

As for the holdings, I don’t like the big weight in Nvidia given its sky-high valuation (although NVDA’s massive YTD rally is likely why the stock has risen to the #1 holding to begin with). I also don’t like the weighting in Intel. In fact, I’d go so far to say (if the ETF wasn’t based on a tracking index …) that the ETF would be better off selling both NVDA and Intel (or at least reducing the weighting by half) and putting the proceeds into Broadcom.

Summary and Conclusion

While the PSI ETF has a very strong performance track record, the XSD ETF has been beating the pants off it. One reason is that the XSD ETF’s expense fee is 20 basis points less than the PSI ETF (0.35% vs. 0.55%). The XSD also has higher weighted positions in smaller and faster growing semiconductor companies as compared to PSI. XSD also has a much lower weight in Intel (2.5%). PSI is an attractive investment, but I rate it a HOLD and give the BUY to the XSD ETF.

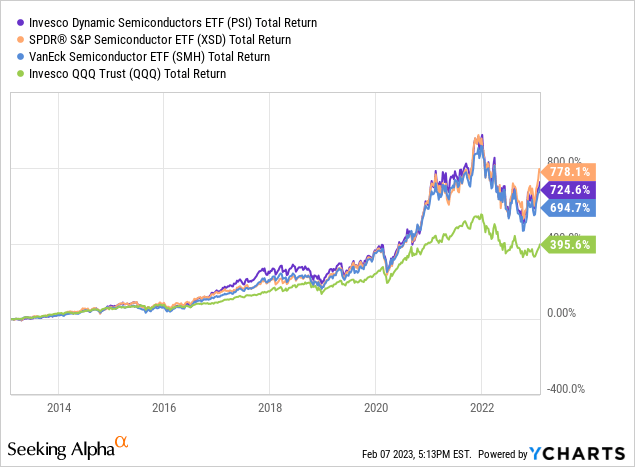

I’ll end with a 10-year total returns comparison of the PSI ETF vs. the XSD and SMH ETFs, and I added the triple Q’s just for a comparison of how much the semiconductor sector (all three of these ETFs) have out-performed the Nasdaq-100 by a mile:

Be the first to comment