Narong KHUEANKAEW/iStock via Getty Images

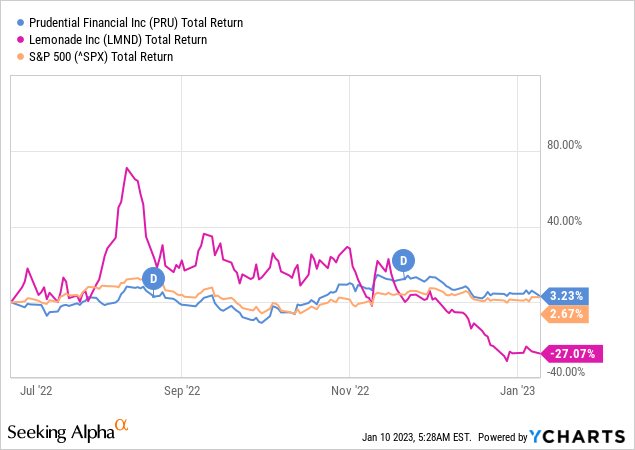

In our last article, Buy Prudential And Go Drink Lemonade, about six months ago, we recommended a pair trade of buying Prudential Financial, Inc. (NYSE:PRU) and shorting Lemonade, Inc. (NYSE:LMND).

In the time that followed, PRU stock slightly outperformed the S&P 500 Index (SP500) on a total return basis, whereas LMND stock lost over 27%. All in all, investors following our recommendation would have made over 30% in total return.

Today we revisit our recommendations.

Changes in PRU since our previous article

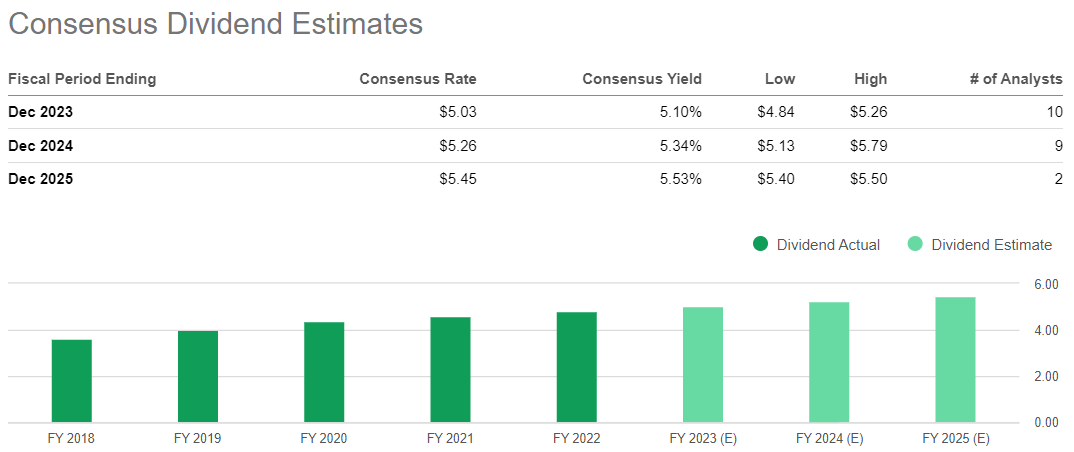

Since our previous article, both EPS expectations for FY22 as well as expected PRU dividends for 2023 went down, while the interest rates (together with expected investor return) went up. As a result, we currently see Prudential as fairly valued at around $105/share, which suggests about 8% upside potential and warrants a HOLD recommendation.

Dividend Estimates (Seeking Alpha)

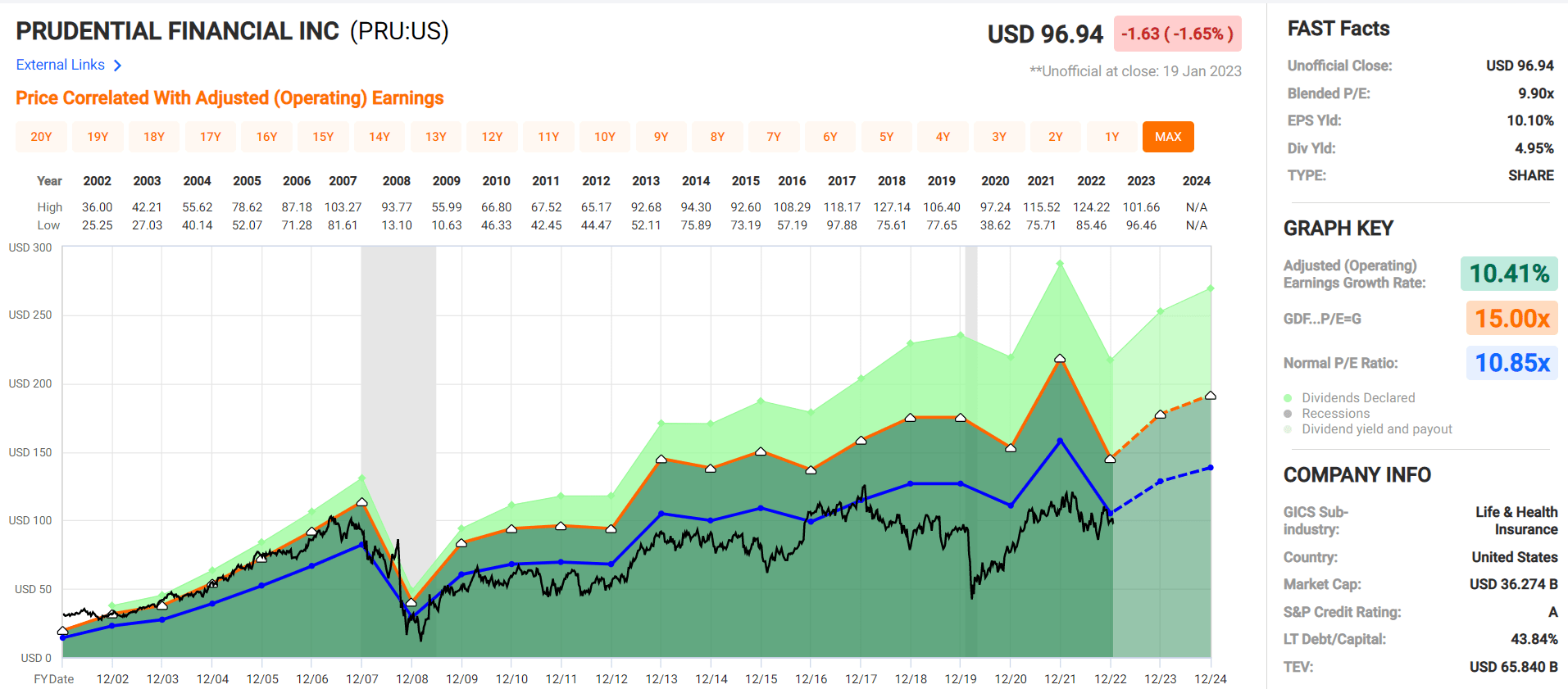

According to FAST Graphs, PRU is trading just below its normal P/E, as it almost always has since the 2008 financial crisis.

FastGraphs

Prudential Q3 22 results were dragged down by PGIM earnings, contributing only 15% to company’s total EPS. Should PGIM earnings recuperate in the future, it would be worth giving our valuation another look.

To watch: PGIM Earnings in PRU FY22 numbers to be announced on February 07, 2023 after market close.

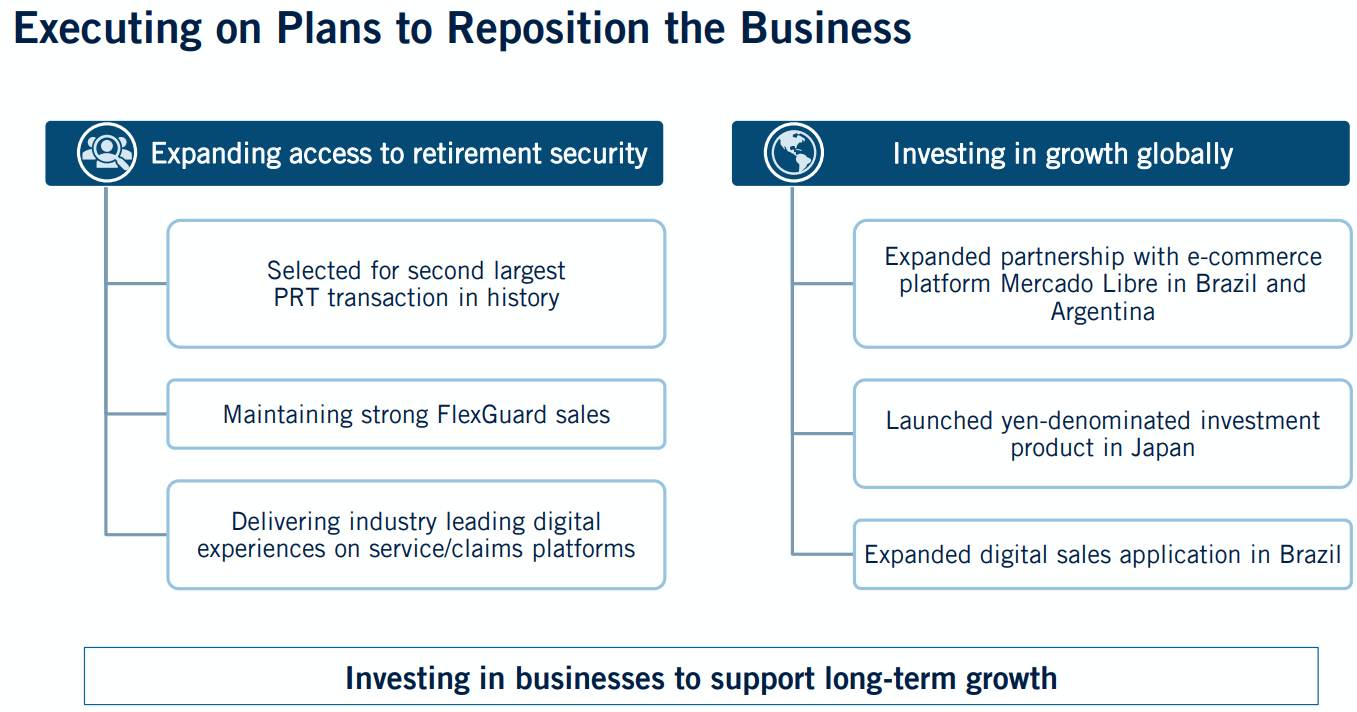

Prudential Financial Inc. – Strategic Perspective

Prudential is working on its strategy to become a higher growth, less market-sensitive, and more capital-light business system.

These goals to be achieved through the following initiatives:

- Higher growth: by divesting Korean and Taiwanese business and investing more in emerging markets such as Brazil and Argentina as well as PGIM;

- Less market-sensitive and more capital-light products: offering products without a guarantee, like FlexGuard and looking for ways to de-risk the back book in life insurance business.

Prudential

Prudential has over $5bn in liquid assets, which it can use to reposition itself on the market using inorganic growth. We remain confident on Prudential’s ability to execute on its strategy.

Changes in LMND since our previous article

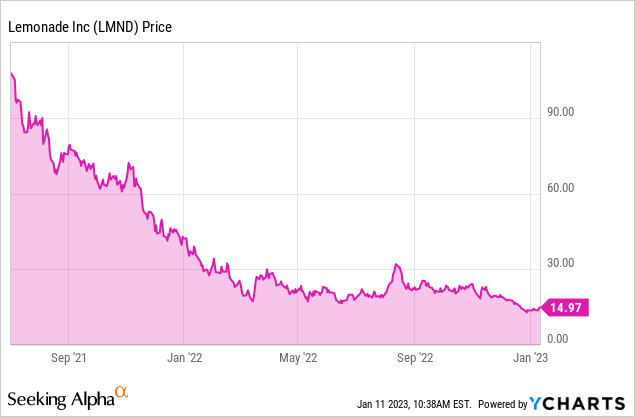

We started covering Lemonade in March 2021, when LMND stock was trading at $83. Since then, LMND has lost 83% of its value and is currently trading at $13-$14 per share. From a unicorn with $5.4bn market cap, Lemonade has turned in a cash-burning ex-unicorn with a market cap hovering around $1bn.

However, despite losses in the share price, the company has actually exceeded its revenue guidance for 2022, demonstrating exponential revenue growth (partially organic, partially due to Metromile acquisition).

Lemonade Acquires Metromile in July 2022

Metromile was a car insurance provider with licenses in 49 states (but 65% of business in California) and extensive car trip precision data. The acquisition by Lemonade was paid in stock (7.3m LMND shares), while allowing Lemonade to acquire $165m of Metromile’s cash balance. This acquisition gave Lemonade a jump start in the car insurance market, as they build on ten years of Metromile’s data instead of gathering and evaluating the data from scratch.

Lemonade’s revenues are expected to approach $250m for FY22 (compared to the previous estimate of $205m). Unfortunately, for every dollar that Lemonade generates in revenues, it loses even more in net income. However, the expected losses for FY22 have slightly improved from $5.5/share in July 2022 to $4.83/share in January 2023. This is by no means an indication for future profitability, which is still not in the cards for the next several years.

Chewy Partnership goes online in Spring 2023

In October 2022 Lemonade announced its new partnership with Chewy – a platform for pet owners, which will offer Lemonade’s pet insurance starting from Spring 2023. Lemonade will not be an exclusive pet insurance provider, however, company’s management is very optimistic about reaching 20 million Chewy customers. The deal, just like the Metromile acquisition, saves Lemonade cash, since Chewy will be compensated primarily in LMND’s equity for the revenues Lemonade generates on the platform.

Management expects Lemonade to break even mid 2026

In November 2022 Lemonade’s management published a base case scenario, where Lemonade is expected to achieve profitability by mid-2026.

Lemonade

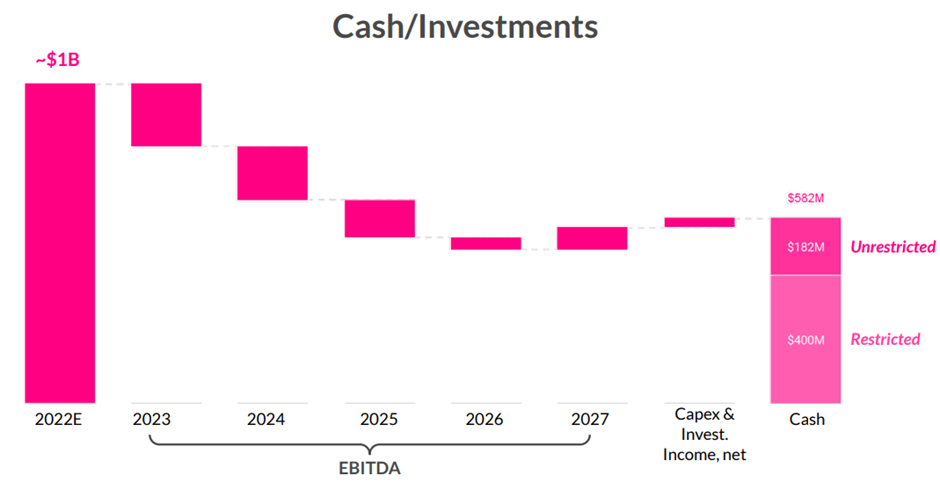

Lemonade’s balance sheet, notably $1.1bn in cash and equivalents at the end of Q3 22, seems to be able to weather future losses and management believes “our existing capital to suffice until we’re profitable.” In fact, Lemonade’s management stated that they deliberately plan to slow down the company’s growth to 20% p.a. so that the cash would suffice till profitability.

Gross Loss Ratio drives Lemonade’s Losses

The rate at which Lemonade loses money has actually increased in Q3 22 ($1.37 loss per share) compared to Q3 21 ($1.08). The main reason behind it was a steep increase in net loss and adjustment expense. Company’s Gross Loss Ratio amounted to 94% in Q3 22, up 17% pts y-o-y and above company’s target of around 70%.

Management focuses on the following tasks to tackle Lemonade’s losses:

- Adjusting premiums in line with inflation and loss ratio;

- Cross-selling its products;

- Increasing efficiency by further improving APIs.

During its Investors Day in November 2022, Lemonade unveiled several interesting ways it addresses Loss Ratio, e.g., fraud algorithms detecting more than $100m in fraudulent claims or Watchtower program tracking the weather and wildfires and automatically halting marketing in affected areas. Another example was Computer vision and Natural Language Processing detecting risky homes for underwriting or telematics for minimizing adverse selection. As a result of all these measures, Lemonade expects its loss ratio to go down in the future quarters.

To watch: Gross loss ratio in LMND FY22 earnings, which are to be announced around February 22, 2023.

Lemonade – Strategic Perspective

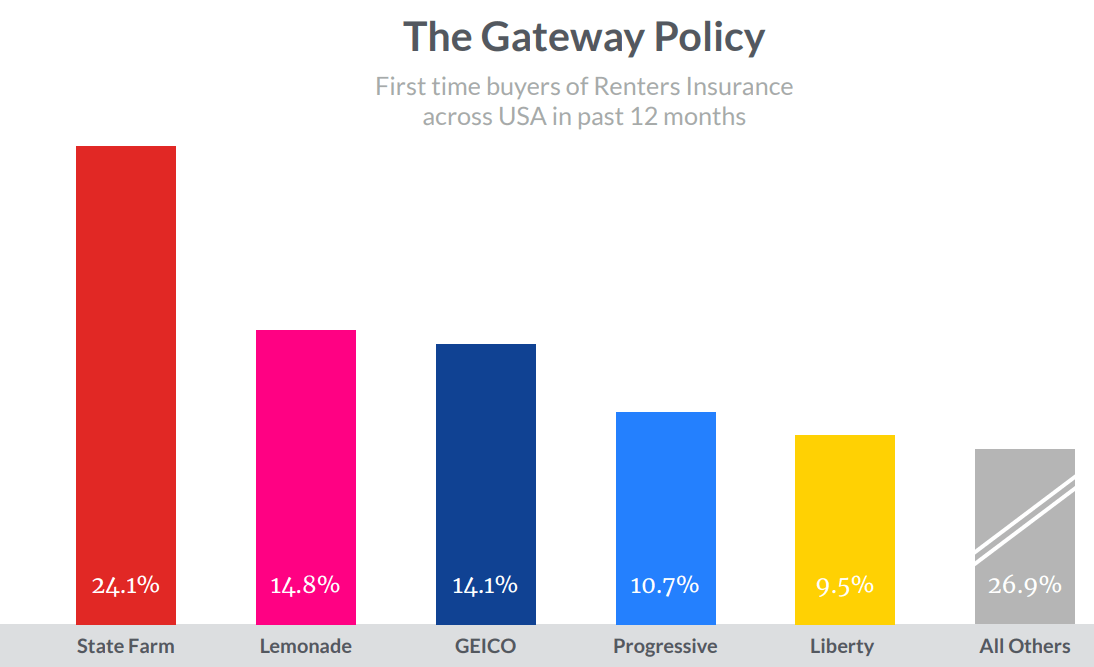

Recent study shows that more and more consumers are shopping for their insurance products online. For example, more than 40% of U.S. consumers last year searched for life insurance products either online or using an app. That is exactly the market that Lemonade is targeting. And they have achieved some encouraging results, namely almost 15% of first-time buyers of rents insurance picked Lemonade. Lemonade’s market share is even higher across the buyers under 35 years of age.

Lemonade

One of the cornerstones of Lemonade’s strategy is customer delight – which the company generates by simple insurance purchase via app, quick and friendly claim settlement via a chatbot. The second part of the strategy is using AI to reduce costs, which includes better-targeted marketing expense, more precise risk assessment and pricing, e.g., using telematics or fraud detection. As we have discussed above, Lemonade is currently struggling with both parts of its strategy. On one hand, according to company’s management, the growth has to be limited to 20% for the cash to suffice. On the other hand, gross loss ratio shows that Lemonade is not making money on its insurance products.

Valuation

In our previous articles, we set LMND’s target price to $13-$18. That’s where the shares landed in the past several months as the tech stock bubble burst.

In general, when investors value the company, they value the future free cash flows. Lemonade is targeting $250m in revenues in 2022 and given its limits on the growth rate, it will take the company a while (namely till 2030) just to reach $1bn in revenues. On the profitability side, Lemonade’s management is currently targeting profitability in mid 2026. Therefore, currently we have a very small insurance player, that generates more losses than revenues and valuing it using discounted cash flow (“DCF”) analysis would not render much value.

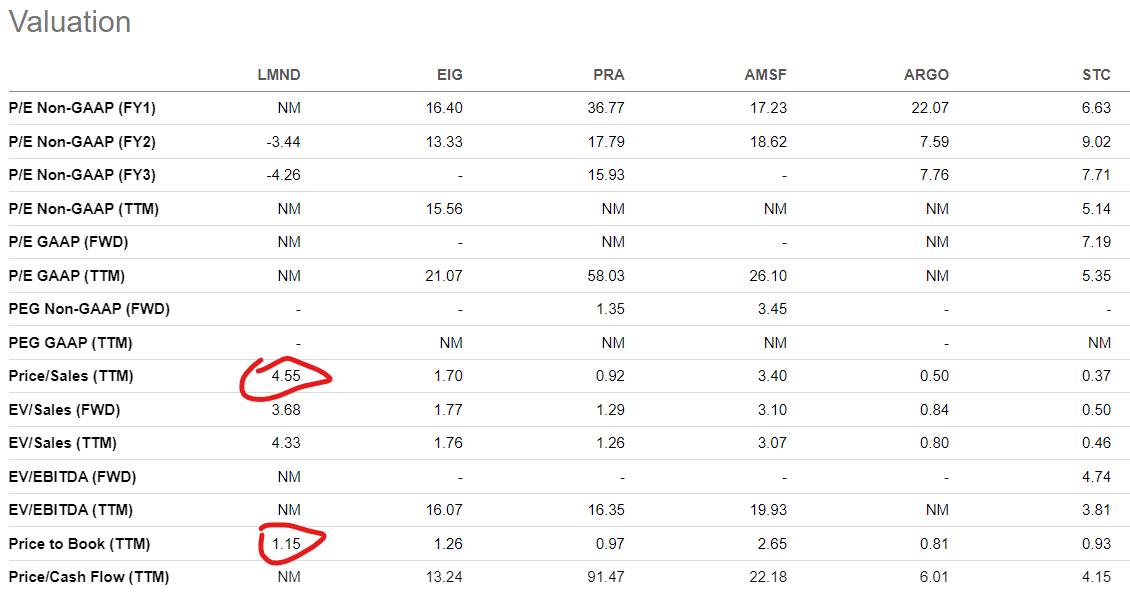

In our opinion it is still quite early to prophesize multi-billion revenues for Lemonade and the profitability at the level of major insurance companies. Currently Lemonade is valued at its cash, which constituted $1.1bn, out of which around $300m is restricted. On a Price/Book ratio, Lemonade is trading roughly in line with its peers as selected by Seeking Alpha. However, as the company burns through cash, this ratio will decline.

On a P/Sales ratio, LMND is trading at a much higher ratio than its peers, however, it doesn’t have a full effect of Metromile acquisition, which we estimate at roughly 30% of current sales.

Seeking Alpha

Therefore, it looks like LMND’s valuation has gone down to earth in the past six months. Given company’s heavy losses and declared limited growth in the next years, we issue a HOLD recommendation for the stock.

Conclusion

We believe that Prudential Financial, Inc. is currently fairly valued, however, we will watch for potential earnings surprise and dividend increases.

As for Lemonade, Inc., its valuation seems to be down-to-earth at the moment. Despite some exciting developments, in our view, the company still lacks a clear profitability roadmap.

Be the first to comment