Bet_Noire

In a recent article, I explained that my car’s license tag has the word “MOAT,” which symbolizes the goal of our research firm, Wide Moat Research.

Of course, I’m referring to “economic” moats, not physical moats, but they both serve a valuable purpose, as explained by Warren Buffett,

What we’re trying to do,” he said, answering a question from the audience, “is we’re trying to find a business with a wide and long-lasting moat around it, surround — protecting a terrific economic castle with an honest lord in charge of the castle.”

Our primary objective when analyzing stocks is to determine the key structural advantages that protect them from competitors, just as physical moats protect castles from enemies. Although the list is not exclusive, we’ve determined that economic moats arise from at least one of seven sources of competitive advantages:

- cost advantage (low-cost provider)

- scale advantage

- intangible assets (branding, trademarks, etc.)

- switching costs (very costly for customers to switch)

- regulation (regulation that makes it harder for competitors)

- network effect (more users = more value)

- digital (large, engaged audience).

Once you find a business with a large moat around it, the next stage in Buffett’s process is to try and figure out what’s keeping the moat intact:

“But we are trying to figure out what is keeping — why is that castle still standing? And what’s going to keep it standing or cause it not to be standing five, 10, 20 years from now. What are the key factors? And how permanent are they? How much do they depend on the genius of the lord in the castle?”

Prologis – The Business Model

Prologis, Inc. (NYSE:PLD) is a global leader in logistics real estate with a focus on high-barrier, high-growth markets.

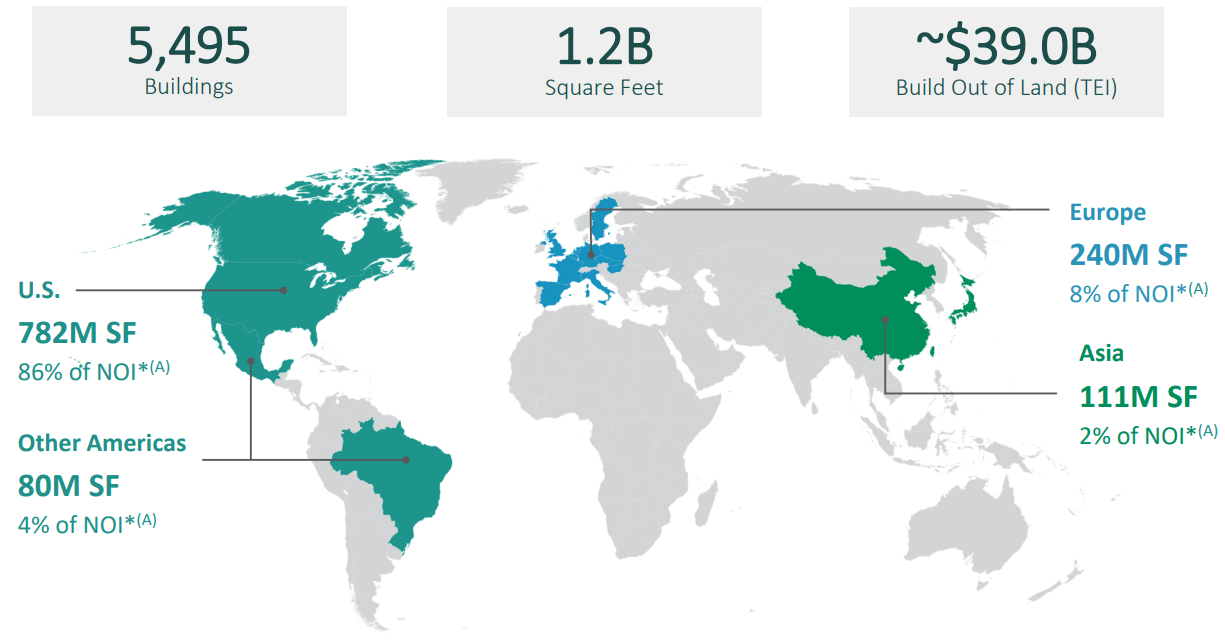

As of Q4-22, the company owned or had investments in (on a wholly owned basis or through co-investment ventures) properties and development projects expected to total approximately 1.2 billion square feet (113 million square meters) in 19 countries.

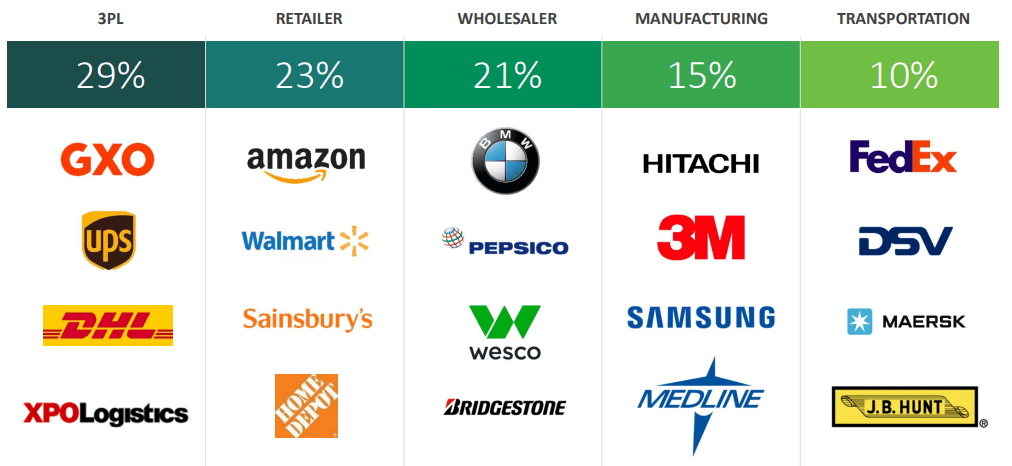

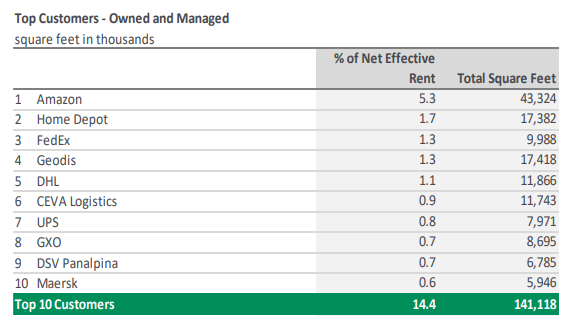

Prologis leases modern logistics facilities to a diverse base of approximately 6,600 customers principally across two major categories: business-to-business and retail/online fulfillment.

On October 3, 2022, Prologis completed the acquisition of Duke Realty Corporation for approximately $23 billion (through the issuance of equity and the assumption of debt).

PLD Q4-22 Investor Presentation

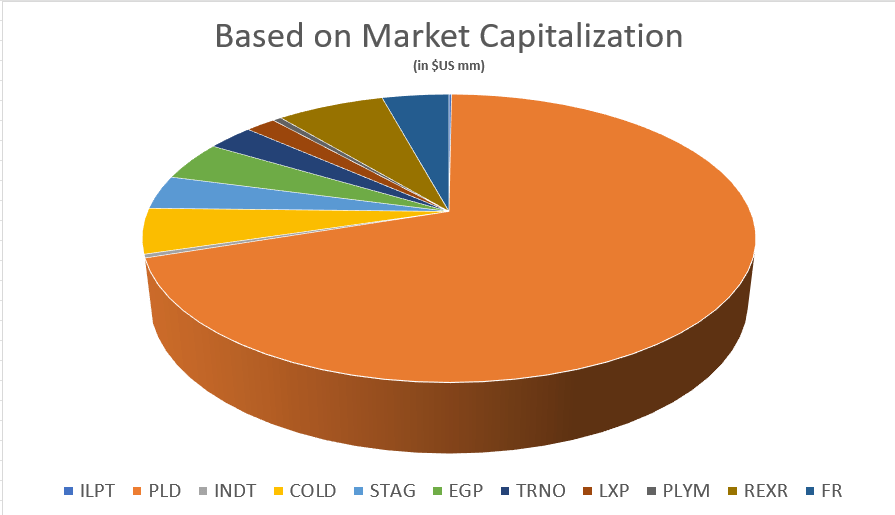

With 5,495 properties and over 1.2 billion square feet, Prologis is one of the largest real estate investment trusts (“REITs”) in the world, with a diverse customer base focused on consumption.

CUSTOMER MIX BY UNDERLYING BUSINESS, PROLOGIS

PLD Investor Presentation

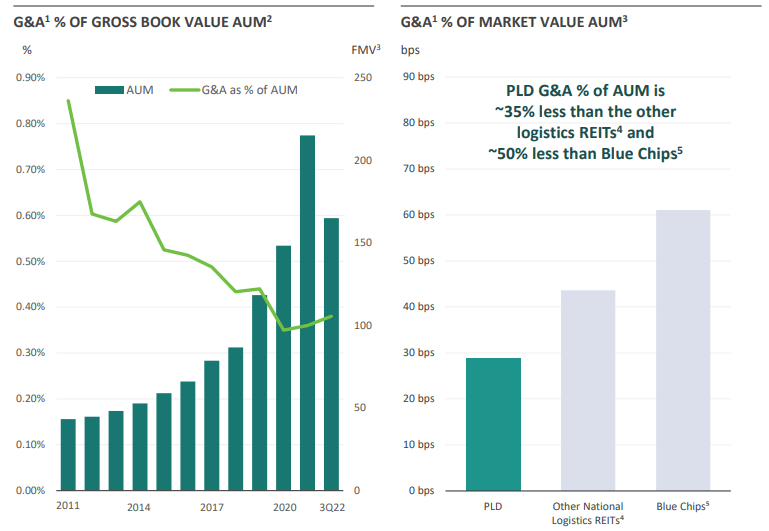

MOAT ADVANTAGE: Prologis has tremendous scale advantage in which early investments in technology infrastructure have produced synergies from strategic acquisitions. Also, Prologis has reduced G&A as percentage of gross book value assets under management (“AUM”) from 85 bps to 38 bps since 2011.

PLD Investor Presentation

As viewed below, you can see that Prologis is the 1000-pound gorilla in the Industrial REIT sector, double the size of all of the peers combined.

iREIT on Alpha

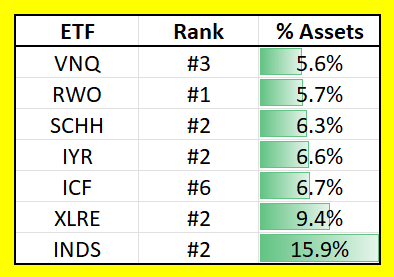

Most of the larger REIT ETFs (exchange-traded funds) own Prologis as viewed below:

iREIT on Alpha

Prologis’ portfolio is concentrated in major port markets for global trade, regional distribution markets, and large population centers.

The portfolio concentration is about 80% in the Americas, 10% in Europe and the remainder in Asia. Prologis also operates the largest industrial property fund platform for large institutional investors.

PLD Investor Presentation

Fortress Balance Sheet

As I explained in a recent article, “the best moats and castles – that stand the test of time – are called “fortress” companies. They have rock-solid fundamentals that make their business models sustainable.” This leads me to the next…

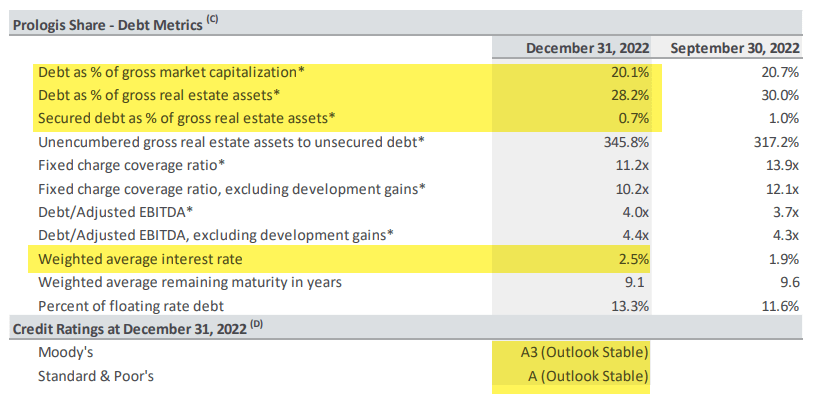

MOAT ADVANTAGE: Prologis has exceptional cost of capital advantage with strong access to the debt markets that have remained challenging for many issuers.

In Q4-22, the warehouse juggernaut has successfully executed a number of transactions, raising over $1.1 billion at an interest rate below 3%, including $700 million of new unsecured borrowings out of Japan and Canada.

The company’s credit metrics are excellent, as it has maintained over $4 billion of liquidity at year-end with borrowing capacity across Prologis and the open-ended funds of $20 billion (due to the balance sheet growth from the Duke acquisition).

Prologis is one of just seven A-rated REITs, and total debt as a percentage of assets (as of Q4-22) was just 28%.

PLD Investor Presentation

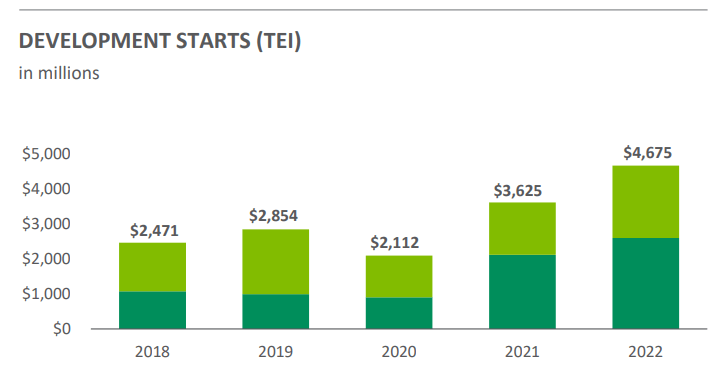

Prologis’ development pipeline stands at $565 million square feet, and the expectation for the year is that the pipeline will decline. Deliveries will put modest upward pressure on vacancies from 3.3% today towards 4% later in 2023. The company said on its latest earnings call:

“… new development starts are slowing in response to the market environment, which will reduce vacancies in late 2023 or 2024. In Europe, we expect deliveries to outpace absorption by approximately 30 million square feet, expanding the current 2.6% vacancy rate to approximately 3.5%.”

PLD Investor Presentation: Dark Green is US and Light Green is Outside US

Investments remain heavily focused on development as the pipeline is 29% pre-leased at +5.7% average stabilized yields in 2023. Given the current cost of capital (equity yield of 3.6%) and $4 Billion in liquidity, we believe Prologis will continue to opportunistically utilize its balance sheet to drive earnings per share.

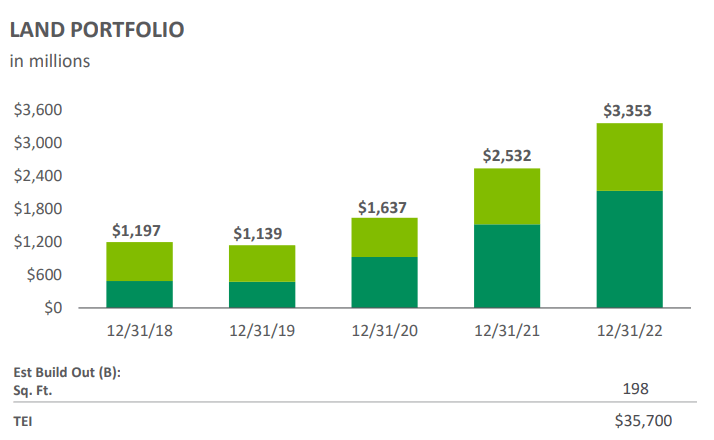

In addition, Prologis is sitting on an attractive land bank that consists of over $3.3 Billion across the globe:

PLD Investor Presentation

Attractive Pricing Power

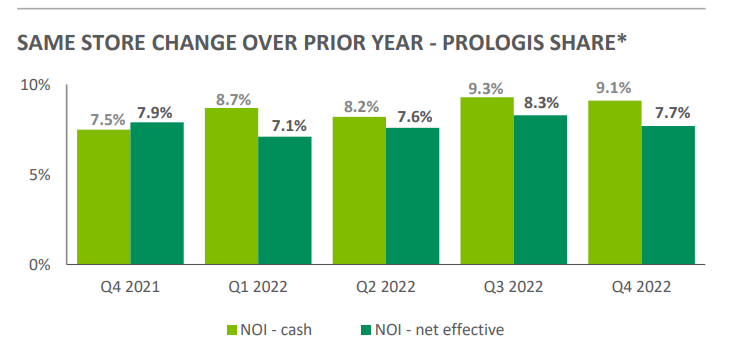

Prologis turned in a solid report card in Q4-22, with cash SS NOI growth relatively stable at +9.1%, and the company said on the earnings call that it has high visibility over its forecast +9.0% cash SS NOI growth as the majority of its 2023 leasing has been addressed.

PLD Investor Presentation

The company projects market rent to grow +10% in 2023, which could further expand leasing spreads that are currently trending in the high 70% to low 80%.

Pricing power is likely to remain favorable as development completions will likely have a modest impact on vacancy given the resiliency of demand and Q4-22 new development starts (declining 33% in the U.S. and 45% in Europe in response to the market environment).

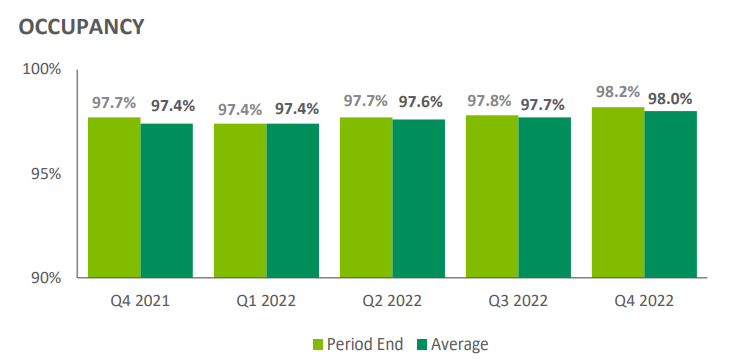

Occupancy came in at 98.2% at the end of Q4-22. Vacancy should be low in 2023 into 2024.

PLD Investor Presentation

Prologis expects 10% overall U.S. rent growth in 2023 with outperformance in coastal markets. Management noted the spread between coastal and non-coastal rent growth is typically 300-500bps and expects a wider spread in today’s environment.

Prologis expects core funds from operations (“FFO”) (excluding promotes) to range between $5.00 to $5.10 per share. At the midpoint of guidance, this represents approximately 9.5% growth over 2022. Including promotes, Prologis guides a range of between $5.40 to $5.50 per share.

In short, the historical low vacancy rate and high rent growth are likely to buffer Prologis from recession effects and allow the company to continue to grow its dividend robustly as it has done over the last several years.

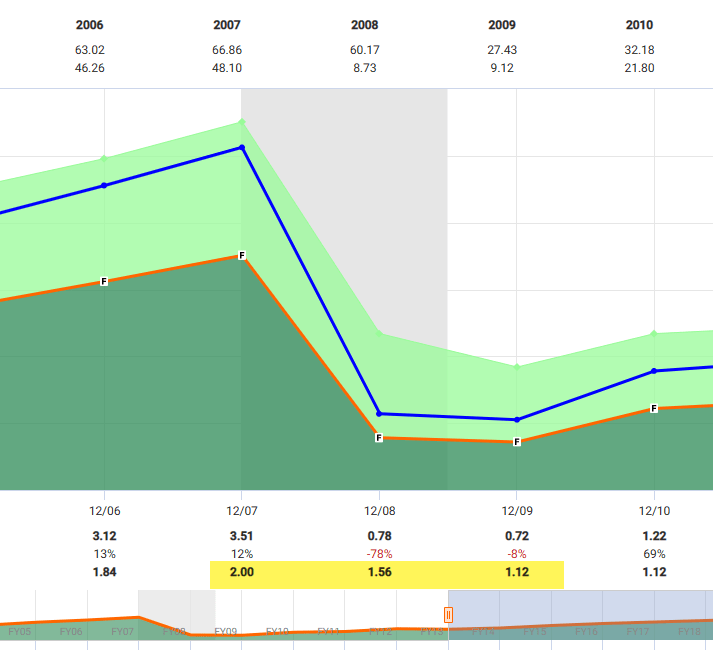

As seen below, Prologis cut the dividend in the Great Recession, from $2.00 per share to $1.12 per share:

FAST Graphs

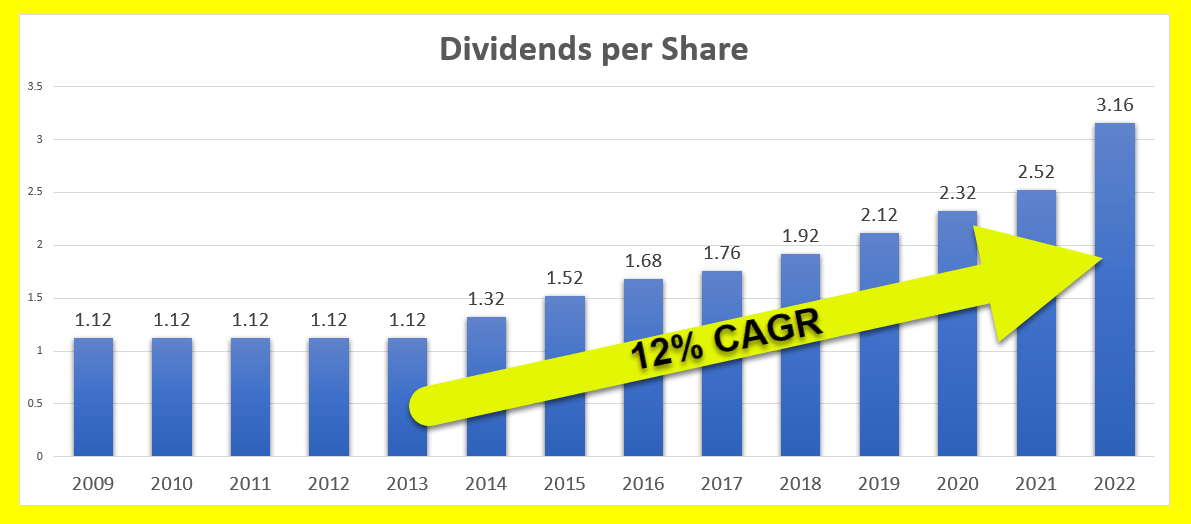

However, it has rebounded, and since 2013 Prologis, Inc. has grown the dividend by an average of 12% per year, as viewed below:

iREIT on Alpha

Buy Like Buffett

When selecting stocks, Warren Buffett pays careful attention to a business model that he understands, not just in terms of what the company does but also “what the economics of the industry will be 10 years down the road, and who will be making the money at that point.”

He is “also looking for enduring competitive advantages,” which is the same thing as the width of the moat. In this article, I have highlighted a few primary advantages of Prologis, Inc., and of course now we must determine whether there’s an adequate margin of safety.

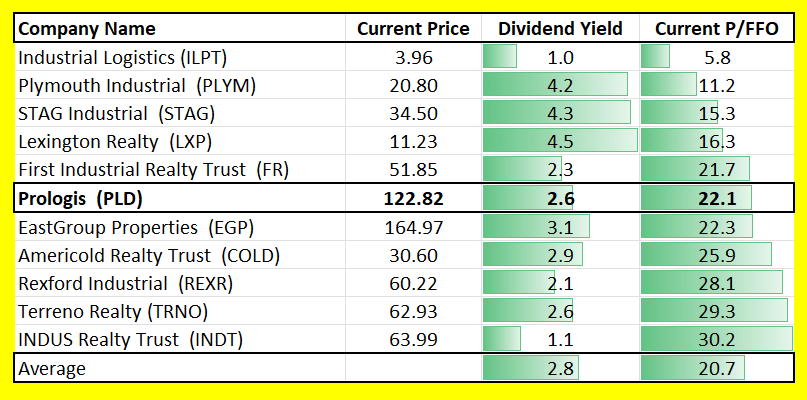

iREIT on Alpha

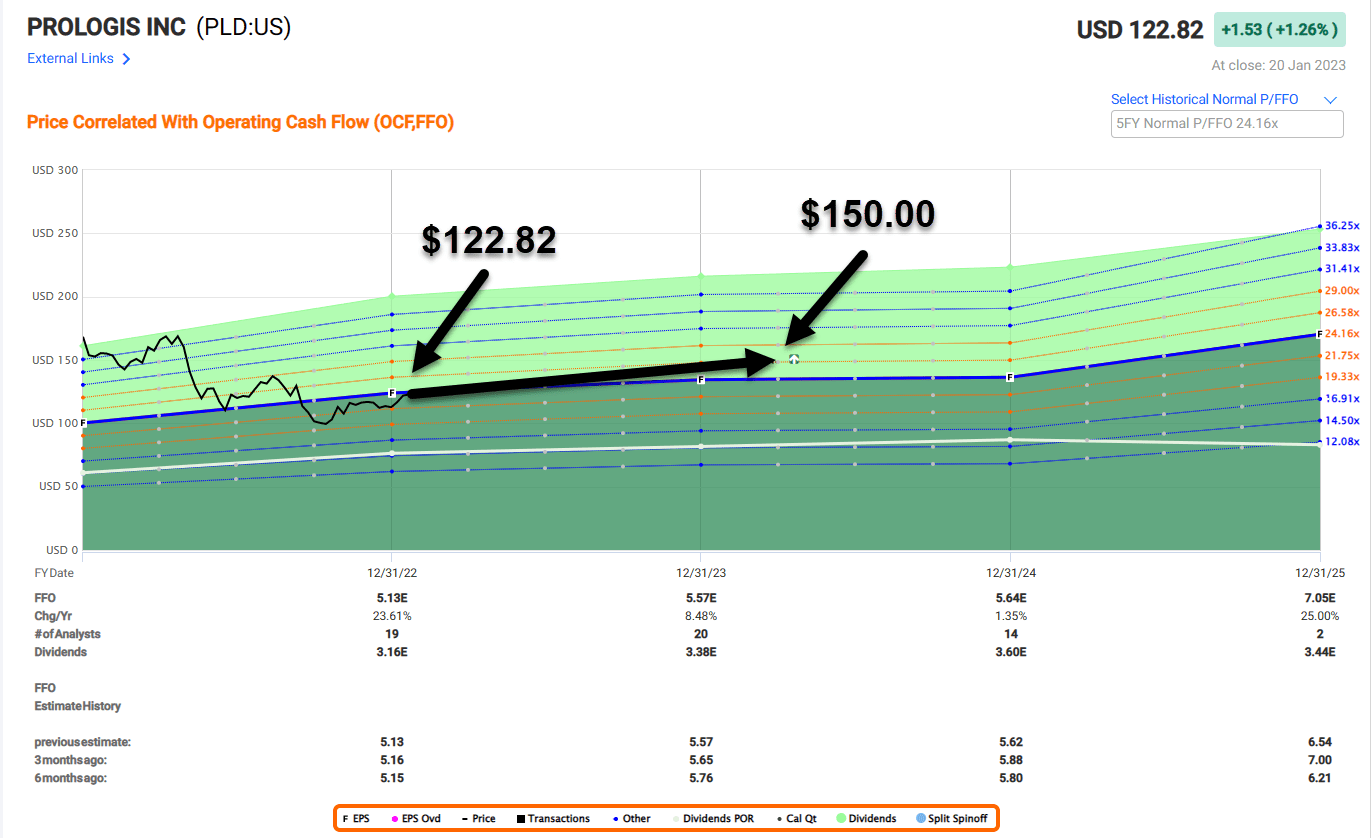

As you can see (above), Prologis is trading at $122.82 per share with a P/FFO of 22.1x and dividend yield of 2.6%.

Clearly this does not make the company the cheapest REIT in the sector, but remember Prologis is the only A-rated industrial REIT and enjoys a dominating scale advantage.

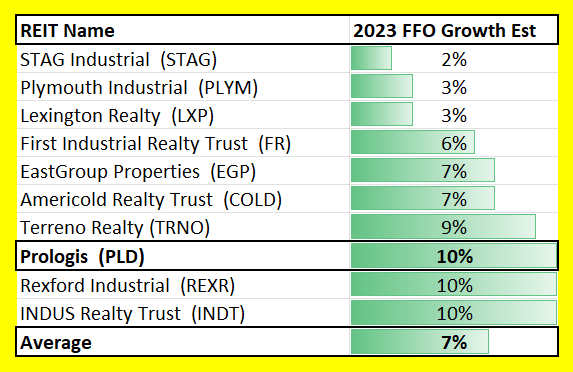

As viewed below, Prologis is expected to grow by ~10% in 2023, which makes this REIT one of the most attractive.

iREIT on Alpha

Prologis now trades at $122.82, and we put a $150.00 (Q1-24) target on shares which results in a total return projection of around 20%.

Keep in mind that I recommended PLD shares back in October 2022 (and subsequently bought shares myself). Since then, PLD shares have returned over 16%.

We consider Prologis one of the best “wide moat” REITs in our coverage spectrum, and I’m happy for it to have gained a substantial foothold within my retirement portfolio. Prologis, Inc. is clearly a textbook moat and fortress story!

FAST Graphs

Be the first to comment