Justin Paget

I have been evaluating my current investments and going through my watchlist to try to find timely investment opportunities. While this includes regular stocks, the selloff in several REIT sectors in 2022 has me taking a closer look at several REITs that were expensive in the past couple years. One of the REITs that has been on my watchlist for most of 2022 is Prologis (NYSE:PLD). To be honest, the whole industrial REIT sector has been on the watchlist for a while, and Terreno Realty (TRNO) was my first addition in the sector to my Roth IRA this year. I’m hoping to make my Roth contributions earlier this year, and if there is a buying opportunity in shares of Prologis, I will be adding the REIT to my portfolio.

Investment Thesis

Prologis is the 800-pound gorilla of the industrial REIT sector and has created impressive returns for investors over the last decade. They have industrial properties around the world, but the US is still the dominant piece of the portfolio. They have grown rapidly in recent years, organically and through acquisition, and the dividend has continued to grow at a double-digit pace as well.

The yield now sits at 2.8%, but if you prioritize dividend growth, Prologis should definitely be on your watchlist or in your portfolio. The valuation isn’t cheap (it almost never is) at a price/FFO of 22.2x, which is basically in line with the average multiple from the last decade. I’m hoping to buy shares in coming months below $100, which would put the multiple below 20x and the yield over 3%, which would give investors some margin of safety. Heading into 2023, my watchlist is not as long as it was a couple years ago, but Prologis is definitely in the top 5.

Q3 Update

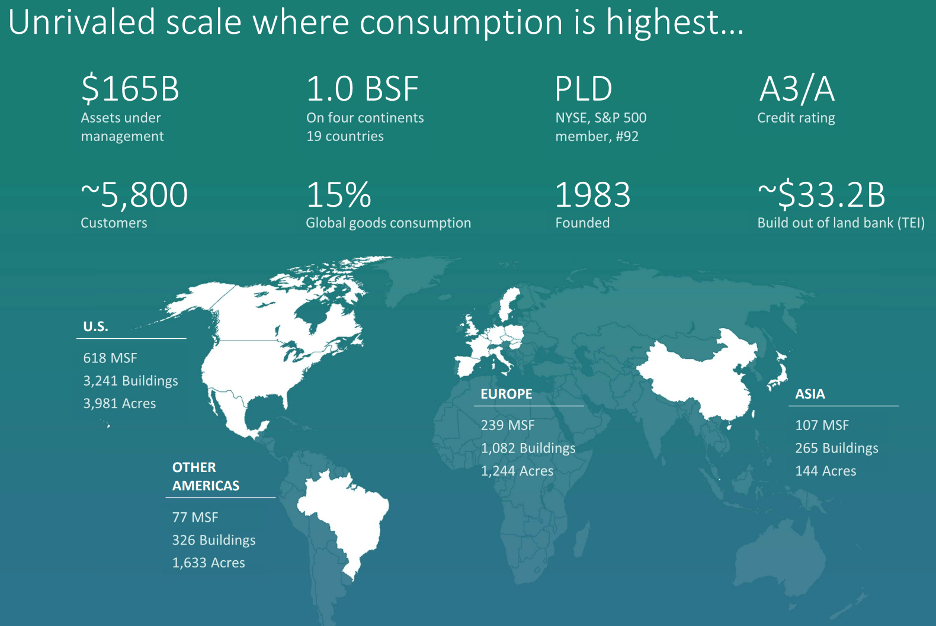

For the investors that aren’t familiar with Prologis, the REIT is the largest in the world with a $106B market cap. While most REITs focus exclusively on the US, Prologis has expanded its footprint across the world. The US is still the largest portion of the portfolio by far, with the segment accounting for 82% of Prologis’ net operating income. They typically focus on high barrier to entry areas in and around large cities, like New York/New Jersey on the east coast and the major metropolitan areas in California.

Prologis Overview (prologis.com)

While it’s not completely focused on the California market like Rexford Industrial Realty (REXR) for example, the major California markets make up a meaningful portion of the company’s assets. The Southern California market accounts for nearly 18% of net operating income, while the Bay Area is just over 7%. That’s a quarter of the company’s NOI, so it was worth mentioning. Other major US markets make up significant chunks as well, but outside of New York/New Jersey at 8%, there isn’t much that comes close.

I skimmed the most recent 10-K and there were a couple things that caught my attention. The first was the closure of the Duke Realty acquisition in October. While I can’t complain about the REIT adding to its already impressive asset base, I have seen a couple things that make me think they probably overpaid for the acquisition at $23B. Either way, it’s in the rear-view mirror now. The other thing I noticed was the solid balance sheet, more specifically the interest rates Prologis is able to borrow at. A weighted average interest rate below 2% allows the company access to cheap capital at a rate well below the rate of inflation. With shares down over 30% in 2022, shares are certainly more attractive today than they were 12 months ago, but that doesn’t mean shares are cheap.

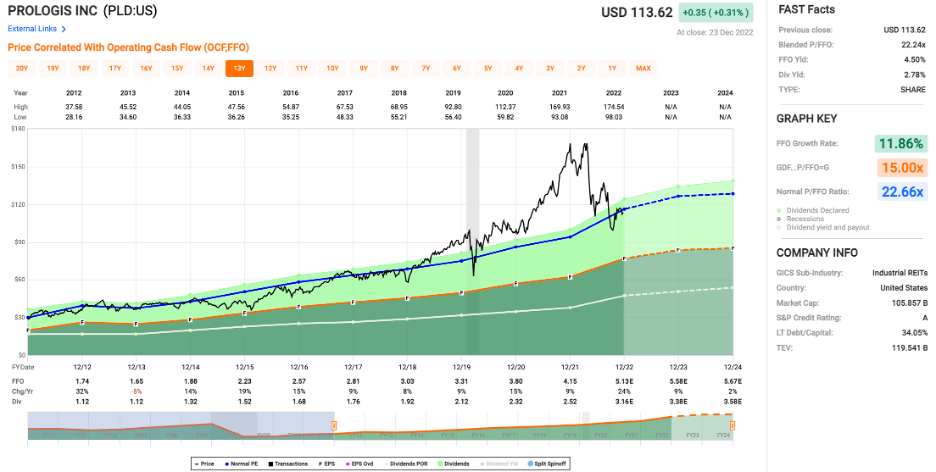

Valuation

Prologis has spent most of the last decade trading at a premium multiple. The growth trajectory of industrial real estate and consistent FFO/share growth are the main reasons I see for that. The average multiple has been a price/FFO of 22.7x. Shares today are a smidge below that at 22.2x. I don’t think investors can count on much multiple expansion from here (you could maybe argue for a 25x multiple), so most of the performance will be driven by FFO/share growth.

Price/FFO (fastgraphs.com)

While I currently have no position in Prologis, I would love an opportunity to pick up shares below $100. I missed it last time when shares dipped below that mark in October because I didn’t have any cash in my Roth at the time, but if the cash is there and we see another dip, I plan to buy shares. It would put the price/FFO below 20x, the yield a bit over 3%, and while that isn’t a huge margin of safety, I think it would be good enough to start a position. Another reason that shares have commanded a high multiple in recent years is the impressive dividend growth starting in 2014.

Dividend Growth

One of the things that surprised me with Prologis this year was the massive dividend hike. I had Prologis on my watchlist going into 2022, but I certainly wasn’t expecting a 25% hike from a quarterly payout of $0.63 to $0.79. Based on the timing of previous dividend increases, we are due for another one with Prologis’ first dividend of 2023. I think we will probably see a double digit raise, but I would be surprised if we saw another hike of 20% or more. The yield for Prologis currently sits at 2.8%, which might not draw a ton of investors looking for current income, but I like the potential for double digit growth for years to come.

Conclusion

Over the last handful of years, certain REIT sectors have consistently outperformed. In 2022, outperforming sectors like industrial, cell tower, and self-storage struggled, and it has created a buying opportunity. Prologis is no exception with shares down 30% in 2022, but it wasn’t surprising considering the nosebleed valuation from a year ago. Today, shares are much more attractive at a price/FFO multiple of 22.2x. I’m hoping for a dip below $100, which would give me the margin of safety I’m looking for and a yield over 3%. Prologis belongs on the watchlist of every dividend growth investor, and I’m looking to add it to my portfolio in coming months.

Be the first to comment