SimoneN/iStock via Getty Images

This is a Z4 Energy Research pre call note. For a background piece on ProFrac (NASDAQ:PFHC) please click here. For a background piece on U.S. Well Services (NASDAQ:USWS) click here.

Our summary table:

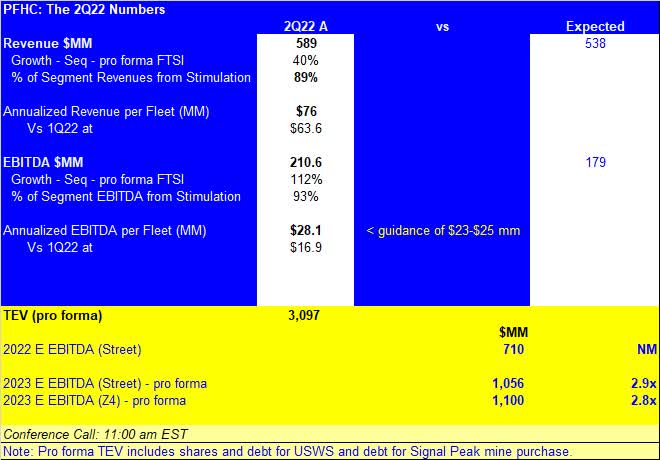

PFHC 2Q22 Summary Table (Z4 Energy Research)

A few notes on the table: The sequential comparisons noted in the table above assume a full quarter of FTSI results in Q1 2022 instead of just results from the March 4th closed acquisition. Comparisons to the previously reported Q1 results were up 70% for revenue and up 100% for reported EBITDA. As previously noted, management has worked to improve FTSI profitability and is now benefiting from its greater scale relative to fixed costs.

We would also highlight that Street consensus EBITDA reflects an annualized EBITDA per fleet estimate for Q2 2022 of $23 mm, which was the low end of management’s range from the Q1 2022 report. Our sense would be that a couple of quarters of outperformance right out of the IPO gate should at least push analysts towards accepting mid-point type guidance. It’s clear looking ahead that the Street is still too low for 2H22 and likely 2023 as well.

Guidance:

Management is guiding 3Q22 activity to an average of 31 fleets, flat with the Q2 2022 level. PFHC is also deploying the first of their own electric fleets this quarter, with 2 more to deploy in 4Q (not counting the step change higher in e-fleets from the pending USWS acquisition).

Favorite Quote Watch 1: “There are no current plans to reactivate any conventional or dual fuel fleets for the remainder of 2022.”

- Z4 Comment: We like discipline and that comment speaks to the retire and replace pillars of their strategy. We’d like to get a better feel from the call on whether or not the e-fleets will be wholly or partially incremental, over time, relative to the 31 conventional fleets operating now.

Favorite Quote Watch 2: “The Company also expects incremental improvement in third quarter results, as compared to the second quarter attributable to further bundling of materials with our pressure pumping services, continued pricing improvements, and the anticipated deployment of our first electric fleet.”

- Z4 Comment: Current Street estimates for 3Q22 on 31 fleets works out to an annualized metric of $26.4 mm, nearly $2 mm per fleet below the Q2 level, which doesn’t taken into account the “further incremental improvement noted in the preceding sentence. On the call, we would like to hear about the spread between their Tier IV DGB fleets and the new e-fleet pricing as well as their thoughts on just how long they plan to contract the new fleets for and how much of a discount to current spot this more guaranteed utilization would represent in light of super tight frac market conditions. Regardless, we repeat that consensus is overly conservative for 2H22 and 2023.

Lastly, the company tightened 2022 capex higher from a prior range of $240 to $290 mm to a new range of $265 to $290 mm due to higher activity levels and costs. We’d like management to give a window into 2023 spending on a maintenance plus growth thoughts basis.

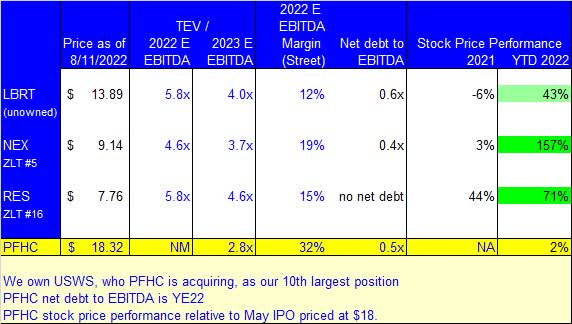

Valuation and Peers:

The US Well Services acquisition remains on track for a 4Q22 close. In the wake of the acquisition, PFHC will be the largest player in e-frac with a combined 12 e-fleets, all of which will be in a position to command premium pricing in 2H22 and likely throughout 2023. They’ll also be the 2nd largest overall completion company, with 44 active fleets in the U.S.

Our sense is that the modest debt they will incur with the acquisition and the newness of the name to market (they IPO’d in May) has left them trading at a substantial discount to their primary peers despite strong EBITDA margins that are set to get stronger as tight frac market conditions persist.

For now, our 2023 EBITDA estimate remains unchanged at $1.1 B (the Street has come up to nearly meet us since our last update) and we expect multiple expansion over the course of the next several months close to 4.0x yielding a near-term upside target of $27 with a more reasonable for the sum of their parts (high margin, lowish debt, young and premium priced fleet) 4.5x multiple driving a $31 target.

Z4 Energy Research

Knock On Impact: The strong quarter and outlook are also positive for USWS who they are acquiring in a stock for stock transaction at a post USWS reverse split-adjusted 0.3366 PFHC for each USWS share. The $27 PFHC target, disregarding any arb spread, translates to just over $9 for USWS while the $31 level would yield a nearly $10.50 expectation. To repeat, this is not our view for today to be sure, but for the potential, for PFHC, over the next 6 to 12 months.

Nutshell: Stronger than expected quarter that should be viewed in light of their stock price under-performance since the IPO. Estimates are too low and should track higher after the call. The name trades at a significant discount to the group while sporting best-in-show EBITDA margins and a premium price garnering large, modern frac fleet. We don’t own PFHC, but USWS holds the 10 position in the Z4 Long Term portfolio.

Be the first to comment