grandriver

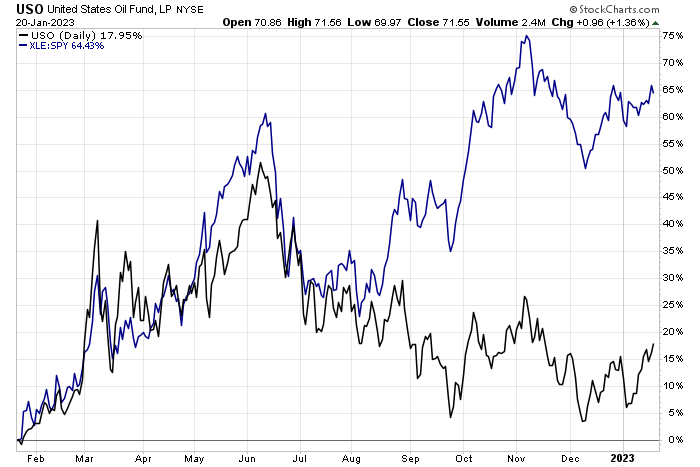

Oil prices have rallied sharply since the first week of the year. WTI currently hovers in the low $80 after dipping to near $70. What’s been frustrating for energy equity bulls, though, is that the Energy sector ETF (XLE) has underperformed the broad market since early November. A recent shift favoring growth stocks over value and cyclicals comes after the best year for value since 2000.

Energy shares remain a bargain, though, as the sector is the cheapest on a forward P/E basis according to FactSet. Let’s dig into one fracking firm to see if shares are indeed on the cheap.

Oil Rallies, Energy Stocks Still Below the November Peak (vs SPY)

Stockcharts.com

According to Bank of America Global Research, ProFrac Holding Corp (NASDAQ:ACDC) is a growth-oriented, vertically integrated, and innovation-driven energy services company providing hydraulic fracturing, completion services, and other related products/services to North American E&Ps. Founded in 2016, ProFrac was built to be the go-to service provider for the most demanding fracturing needs. ProFrac seeks new technologies to reduce emissions and increase efficiency in what has historically been an emissions-intensive component of tight oil/gas development.

The $3.5 billion market cap Energy Equipment & Services industry company within the Energy sector does not have positive trailing 12-month GAAP earnings and does not pay a dividend, according to The Wall Street Journal.

Back in November, the firm reported Q3 results that showed net income of $143 million and impressive YoY revenue growth of 256%. Unfortunately for the bulls, that was a near-term peak for the stock price, but the firm remains on the growth hunt as evidenced by a recent acquisition of operations in the Eagle Ford shale region.

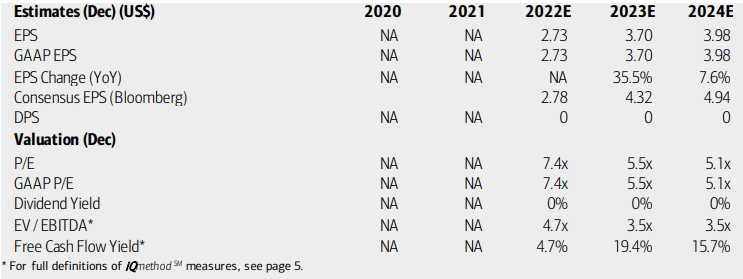

On valuation, analysts at BofA see earnings rising more than 35% this year but then moderating to below 8% by 2024. Investors should be on guard for peak earnings and multiples in the coming quarters following strength in oil prices over the last year and a recent pullback and consolidation of WTI in the $70 to $90 range. Still, the Bloomberg consensus forecast is actually more upbeat than what BofA expects.

Being a young growth-oriented firm, dividend payments to shareholders are not in the cards with this small-cap energy name. What’s positive, though, is that ProFrac’s free cash flow is seen as being very high this year and still robust as conditions normalize in 2024.

With low operating and GAAP earnings multiples and a dirt-cheap EV/EBITDA ratio, I see strong value in ACDC shares at these levels. Downside risks are seen should the U.S. slip into recession and ACDC’s high exposure to energy prices relative to its fracking peers. Another possible risk is the firm’s leverage.

ProFrac: Earnings, Valuation, Free Cash Flow Forecasts

BofA Global Research

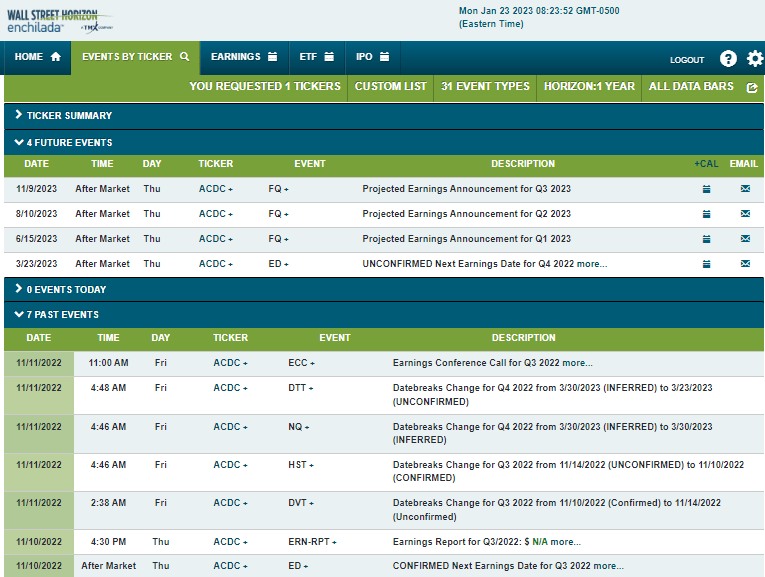

Looking ahead, corporate event data from Wall Street Horizon show an unconfirmed Q4 2022 earnings date of Thursday, March 23. The calendar is light on volatility catalysts aside from the reporting date.

Corporate Event Calendar

Wall Street Horizon

The Technical Take

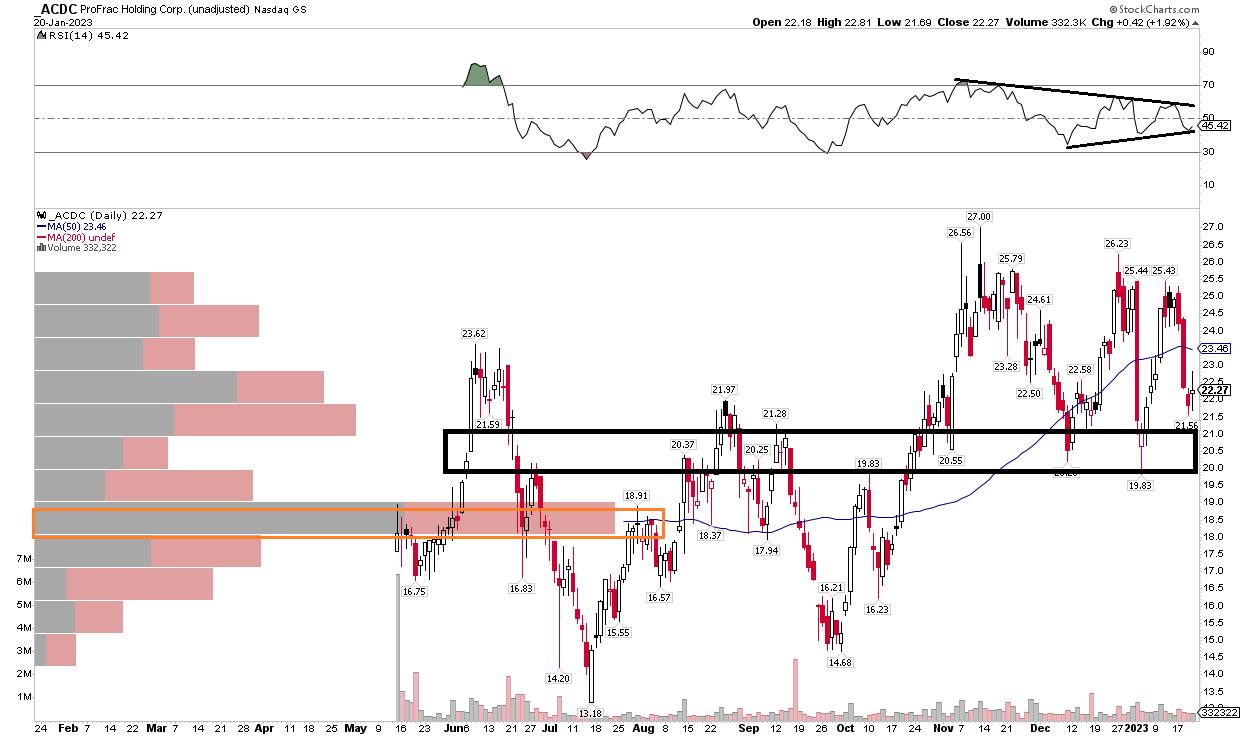

After going public last year, ACDC has established a trading range. I see a broad support/resistance zone in the $20 to $21 range, but also notice there is significant volume by price just under $19 that should represent support on a further pullback.

Bigger picture, I would like to see the stock rise above the $27 level to new highs to support the case for a sustained uptrend in the stock. Additionally, notice how the RSI momentum indicator shapes up – it’s currently consolidating, indicating a significant move in the share price could be in the offing.

Overall, so long as the stock is above the $18 to $19 area, I think a long case is warranted.

ACDC: Shares Above Support, Consolidating Momentum

BofA Global Research

The Bottom Line

ACDC is a compelling risk-on value case. With high free cash flow and low valuation multiples, I see long-term upside, but much depends on how oil and natural gas prices evolve for this aggressive company. Shares have outperformed the broad market since its IPO, and I see some technical support.

Be the first to comment