10’000 Hours/DigitalVision via Getty Images

Could the horrifically poor sentiment in the chipmakers finally be turning? In our opinion, sentiment is still negative, but not nearly as poor as it was just a month ago. We assert this as traders, because we came in a few weeks ago to do some trading in a number of the semiconductors. Quick gains were had on such buys, and it was because we believed earnings season would provide some clarity on the near-term outlook which would alleviate anxiety.

We were partially correct, as earnings in the sector were largely better than expected, while the outlook given by many were decent. Still, the action in semiconductor stocks continues to be marginally weak. While these stocks are off the lows, so is the overall market. However, we like buying these stocks on the next market dip, which we believe could be in the next few weeks, before a ramp into New Year. We think you can build a trading position into some of these names. One stock in the sector we do like again is Advanced Micro Devices, Inc. (NASDAQ:AMD). We think the market has priced in much of the slowdowns and negative macro risks, and if the market draws back like we suspect, you should scale in. Let us discuss.

BAD BEAT Investing

The play

We like scaling into stocks for trades. Here is the thing. Generally speaking, barring a complete collapse, this approach works well to build a position. Often, the worst case is you only get one or two legs, and still make money. We despise buying all at once for a trade. It is just bad business. At times, the company hiccups and the stock can take, so we do embrace stops when trading, but often these are triggered just 10% of the time, on average.

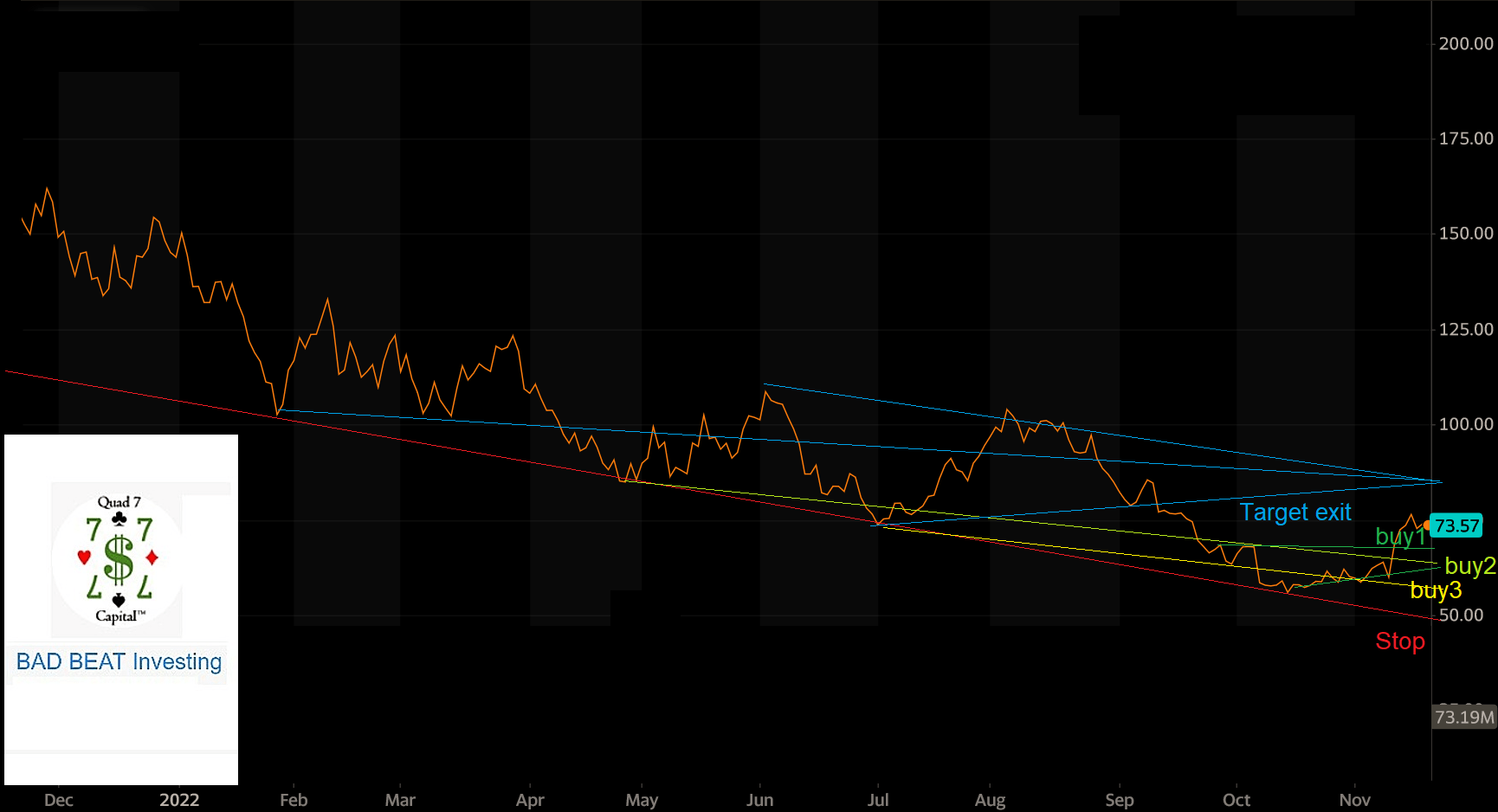

Here is how we think new money should trade:

Target entry 1: $72-$73 (25% of position)

Target entry 2: $65-$65 (35% of position)

Target entry 3: $58-$659 (40% of position)

Stop loss: $50

Target exit: $83.

Options consideration: We love selling puts to define entry here. Volatility is reduced, so call options work too, we like $75 or $80 strikes at least 6 months out.

Discussion

The above play is a sample of exactly the types of trades we feature in our service. Now look, AMD, and semis, it has been tough. The market is discounting a ton of bad news in our opinion, and AMD as a stock has been cut by 2/3rds since reaching all-time highs. It has been just downright painful for folks who bought and held. This is simply an unloved sector with some fundamental. The cycle is still slowing while demand has cooled, and to make matters, worse pricing has been weak, too. However, all of this is now priced in here, down nearly 70% from the highs to the lows this cycle. We have recovered a little, so let the market get wonky on the next piece of data it does not like and then do some buying. Earnings are going to dip, along with revenues, but the valuation has improved.

Recent performance was mixed however

The chaos began about a year ago. Q3 earnings that were just reported were mixed. That’s really all you can say about the results, however as you know the company had preannounced its Q3 a month ago. The results were below consensus. Revenue was $5.57 billion and actually increased 29.2% year-over-year, driven by decent growth across all segments from last year, but it did drop $1 billion sequentially from Q2. AMD’s GAAP gross margins fell to 42%, a decline of 610 basis points year-over-year and down 400 basis points from Q2. Adjusted gross margins (accounting for Xilinx) were up 50%, actually up 200 basis points year-over-year, but still down 400 points on an adjusted basis from Q2.

Operating income still quite strong, but yes, well down from the peak

As the revenues and adjusted margins expanded, the company saw a year-over-year increase in operating income in Q3. You would have thought we were heading for losses the way the market has acted, but there were sequential declines. The market’s concern is that it does not know how much further weakening there will be. We think we are closer to a bottom than you may think. While there are predictions left and right, we think demand accelerates after we get through any recession we may have. Right now, the economy is still humming, but there are definitely demand concerns.

That said, AMD operating income expanded and was a strong $1.26 billion, or 23% of revenue, up from $1.05 billion or 24% a year ago. One are the company needs to focus on is controlling operating expenses which jumped 47% from a year ago. Net income was $1.1 billion, up from $893 million a year ago, but down huge from $1.7 billion in Q2. Earnings per share fell, however, to $0.67 vs. $0.73 last year. It was far weaker than expected and that is why the company (rightfully in our estimation) pre-announced much of the quarter. But why was it so bad?

Results below expectations due to slowing PC demand

Slowing PC demand was a key factor, and it may be a number of quarters before we see increased demand, and certainly not until we emerge from whatever sort of recession we run into in 2023. It was ugly. The client segment revenue fell 53% from the Q2 peak, and dropped 40% year-over-year to $1 billion. But it was not all bad news folks. Revenue was flat from Q2, but up 14% year-over-year to $1.6 billion in gaming. Xilinx helped the embedded segment actually grow 4% growth sequentially from Q2. Data center revenue remains a huge positive and it rose 8% sequentially increase and a strong 45% year-over-year to $1.6 billion.

The sky is certainly falling, isn’t it? We digress.

It matters not where we have been but rather where we are going, and the forward guidance is pretty strong

It really does not matter where we have been, even if the stock had lost two-thirds of its value from the peak. It matters where we are going. There will be another few quarters of macro challenges for sure. With that said, we think if this market takes the stock back, you scale in as we have prescribed. This is because the Q4 outlook, in our opinion, was largely better than anticipated.

Management guided $5.2-$5.8 billion for revenue which suggests the sequential declines in the top line at the midpoint would cease. If they hit the midpoint this would be a 14% increase vs Q4 2021. Should things go smoother than expected it would be solid growth. Within this range, 2022 revenue would be $23.2-$23.8 billion, which is a pretty sizable 43% drop or worse potentially if below the midpoint from 2021. Our opinion is that this is priced in.

What we see going forward is continued PC demand being weak but ongoing growth in data center and the embedded businesses. The unknown will be cost-cutting measures. We hope these can be managed beyond expectations, and thereby widening margins. Currently margins are expected to be 51% in Q4, which we view as positive. We see Q4 EPS coming in at $0.65-$0.78.

Cash, debt, and big time repurchases

Look, there is debt on hand, but there is a ton of cash, too, and there is a lot of cash flow here still. The balance sheet is in great shape. At the end of Q3, cash was $5.6 billion. Cash from operations were $965 million compared to $849 million a year ago, while free cash flow was $842 million compared to $764 million a year ago. We also like the shareholder-friendly use of cash. Cash was used to reduce debt, and to repurchase shares. We see this continuing. In Q3, the company bought back $617 million of stock in Q3, and that follows AMD repurchasing $920 million of its stock in Q2, boosting shareholder value.

Take home

The market priced in disaster, but AMD stock is up off the lows. We like the balance sheet and the strong management team here. More pressure may come in 2023, but we like starting to buy here as we have prescribed. If markets hiccup badly, you could get a full position of Advanced Micro Devices, Inc. in a short time period, and profit from the rebound. It is what we do.

Be the first to comment