mdesigner125/iStock via Getty Images

Co-Produced with Treading Softly

If you’ve spent any time in Florida, as a resident, not a visitor, you are likely very aware of when Hurricane season begins and ends. You’ll be inundated with radio ads, billboards, and tv commercials reminding you that should a storm hit and utilities, etc. become unavailable that “the first 72 are on you.“

Simply put, you need to have the supplies and means to make it at least 72 hours without rescue or help after a storm, big or small. After that, emergency aid and emergency services should be available to help you. Life wouldn’t be comfortable, but you won’t be in life-ending danger any longer, or so the thought goes.

So, with a storm on the horizon in the eyes and minds of many of my astute peers, I want to ensure that you all get prepared for a potential storm. To do so, I am continuing to add quality and recurring, and high-yield income generators to my portfolio. They are time-tested companies and investments, which will generate income in good or bad times. All while you can sit back and ride out the negativity, perhaps enjoying your favorite business and listening to a crackling fire.

Let us dive in.

Pick #1: ARCC- Yield 9.2%

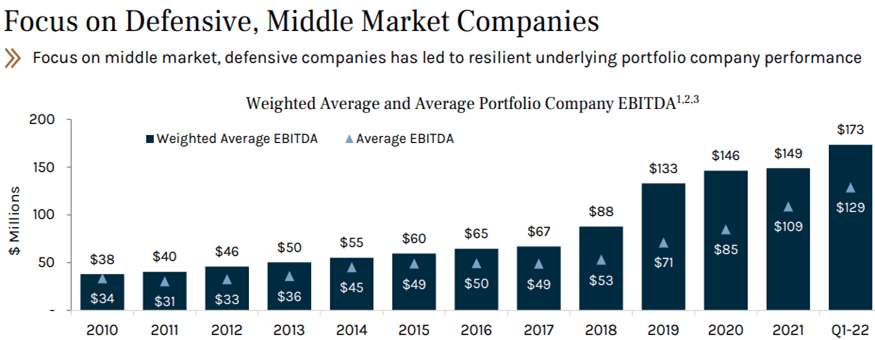

Ares Capital (ARCC) is a BDC (Business Development Company) that invests in “upper middle market” companies. Over the years, as ARCC has grown, it has shifted to focus on larger middle-market companies with a weighted average EBITDA of $173 million. (Source: Ares Capital Corporation’s 2022 Analyst Day).

Ares Capital Corporation’s 2022 Analyst Day

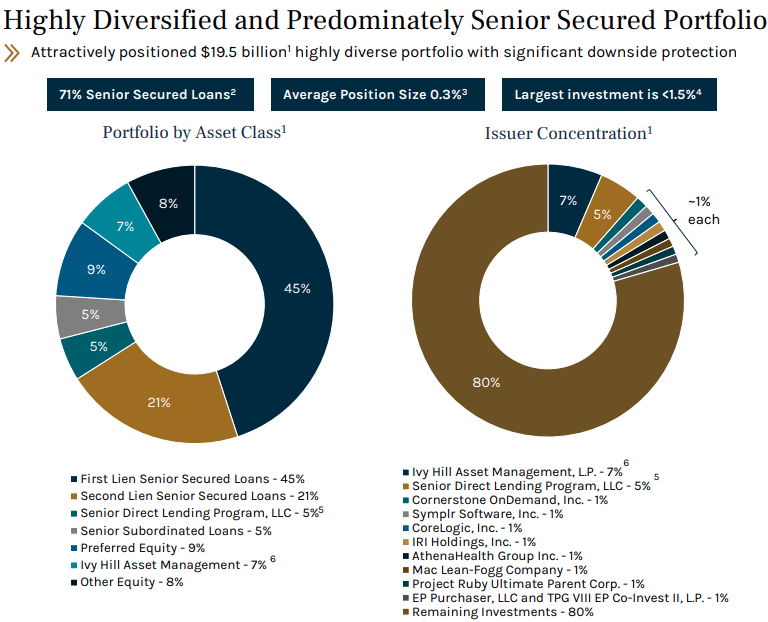

Due to its size, ARCC is able to invest in larger companies without sacrificing diversification. ARCC’s average position size is just 0.3% and its largest single investment is less than 1.5% of its portfolio.

Ares Capital Corporation’s 2022 Analyst Day

As a BDC, ARCC makes a combination of debt and equity investments. Debt investments pay regular recurring interest and provide ARCC a position high in the capital stack. The equity investment provides upside for ARCC, above and beyond the potential return of the debt investment.

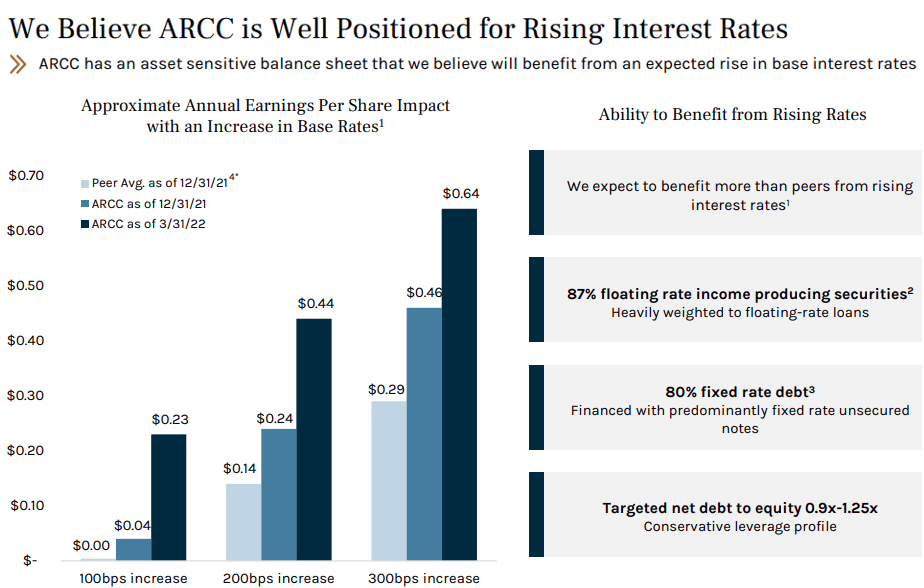

What about rising rates? A lot of investors want to avoid debt when rates are rising. As a result, ARCC is now trading near 52-week lows. This kneejerk reaction is exactly the wrong direction, as rising rates are perfect for ARCC’s investing strategy. ARCC primarily owns floating rate loans, while ARCC borrows primarily at a fixed rate. Every tick-up in interest rates is more money in the bank for ARCC.

Ares Capital Corporation’s 2022 Analyst Day

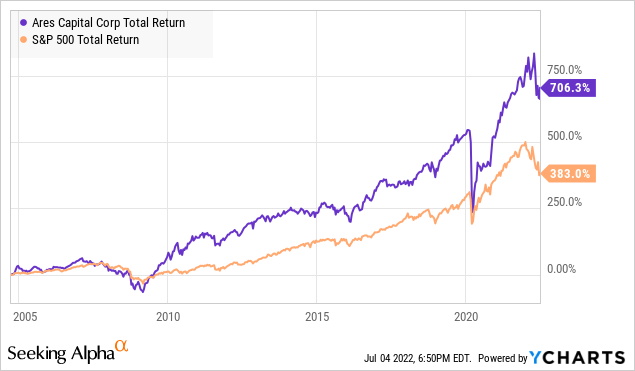

ARCC has consistently outperformed, beating the S&P 500 since IPO, while paying investors generous dividends.

Currently, ARCC is trading at a slight 1% discount to book value ($19.03). ARCC usually trades at a 10-15% premium to book value. As a real blue-chip in the BDC sector, when ARCC is trading at a discount, I’m happy to snag some more shares.

This year, ARCC will see significant tailwinds from rising interest rates. If a recession does hit, ARCC has a proven track record of navigating the Great Financial Crisis and COVID – both times coming out the other side stronger than ever.

Pick #2: CIM C/D Preferreds – Yield 9.7%

Lately, in our High Dividend Opportunities chat, I’ve been talking a lot about the opportunities among preferred shares. Preferred shares are equity that is senior to “common” equity. They receive a pre-determined dividend and are usually callable after a certain date at the company’s discretion. When called, investors receive the “par” value. This puts preferred in a position where they are technically equity, but are also a fixed-income investment.

REITs are a great sector to hunt for preferred shares because they are required to distribute the majority of their taxable income and REITs generally have high levels of cash flow. Since preferred shares get paid in full before the common shares can receive even a penny in dividends, they are a lower-risk way to invest in mortgage REITs.

Chimera Investment Corporation (CIM) is an example of a mortgage REIT we would rather invest through the preferred.

CIM invests in mortgages, generally, mortgages that are “seasoned” and are about 10 years old. CIM has been under pressure because of its interest rate risk and its credit risk.

Interest rate risk is simply the reality that higher interest rates cause lower book value. A mortgage yielding 4% is a more attractive investment when Treasuries are 1% than it is when Treasuries are 3%. So as the price of Treasuries moves, the value of CIM’s mortgages changes as well and this has been a headwind to book value.

The other pressure has been credit risk. Meaning their cash flow is dependent on borrowers actually paying their mortgage. Some in the market think we’re headed to a recession and since during the last recession people didn’t pay their mortgages, it’s natural to fear that again. Even though aside from the mortgage crisis, historically people have paid their mortgages even in the midst of a recession. The funny thing about people, they prioritize having a roof over their head!

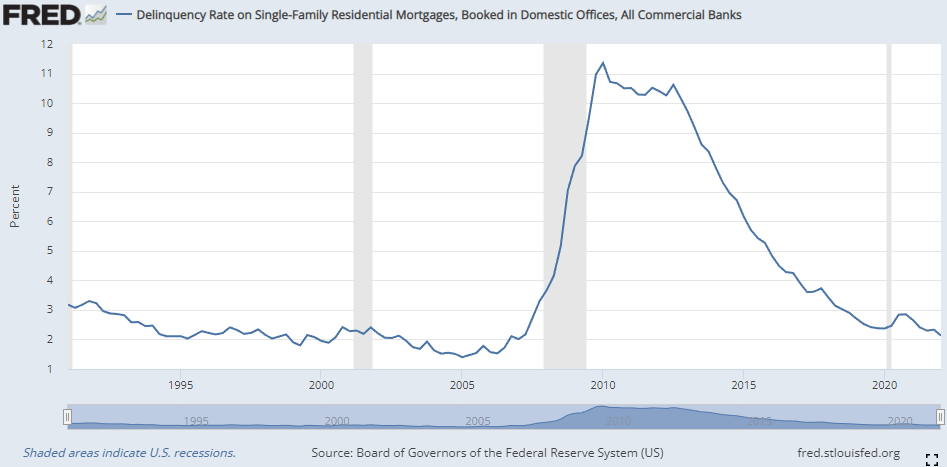

Prior to the Great Financial Crisis, mortgages were seen as a safe-haven investment that investors wanted to own through tough times relative to other types of debt. Here is a look at mortgage delinquency rates since 1990. (Source: Fred Economic Data)

Fred Economic Data

Note that it remained quite low even throughout the dot-com bust. The strength of mortgages in a poor economy at that time was one of the drivers of Wall Street’s confidence that mortgages were invincible, inspiring the recklessness that led to the mortgage crisis. Despite history, the more recent experience still weighs heavily on people’s minds even though it was very unusual.

Today, we don’t see a setup that is at all similar to 2006 when folks were getting 120%+ loan to value mortgages, refinancing to pay their credit card debt, using a ton of adjustable-rate mortgages, etc.

The main risk to CIM is a repeat of the foreclosure crisis. We don’t see that as likely. That crisis occurred because of unique conditions. It is far more normal for mortgages to see only small rises in default rates. People like having a roof over their head, it’s one of those bills they will go to extreme lengths to pay.

For the preferred, I think they are safe to hold even through another foreclosure crisis. CIM was one of the survivors of the foreclosure crisis. It’s well-capitalized and while the mortgage market is going to be challenging with mortgage rates so much higher, it is also going to be full of opportunities for the companies that are capable of buying more mortgages and CIM is one of the companies that can buy more.

Yet we can expect mortgages to remain volatile as rates rise and Wall Street tries to handicap recession risk. For this reason, I prefer the preferred for increased stability. Especially the “fixed-to-floating” preferred which will have a rising dividend if interest rates continue to rise.

The two fixed-to-floating rate preferreds are:

- Chimera Investment Corp. 7.75% Series C Fixed-to-Floating Rate Cumulative Redeemable Preferred Stock (CIM.PC)

- Chimera Investment Corp. 8.00% Series D Fixed-to-Floating Rate Cumulative Redeemable Preferred Stock (CIM.PD)

CIM-C and CIM-D are great holds that provide hedging against rising interest rates. CIM-C starts floating in September 2025 and CIM-D starts floating in March 2024. If they converted to floating today, CIM-C would yield about 7% and CIM-D would yield about 7.6%. It is a good idea to ladder your floating rate exposure so that not all of your investments convert to floating rates at the same time.

For those who already have enough exposure to fixed-to-floating preferred, CIM-A is a fixed alternative that is trading at a good price!

Dreamstime

Conclusion

By buying into preferred securities, like the CIM offerings, or a premier BDC, like ARCC, we can enjoy the outsized income, rain or shine. These income generators can help us ride out any storm that may come, from a position of strength and relaxation.

Having lived through multiple hurricanes, I can attest that riding out the storm in a strong, reliable home vs. a weaker one can make a massive difference in one’s level of anxiety and worry. Create a portfolio that generates the income you are looking for to pay for your lifestyle.

Retirement should be a time of relaxation and enjoyment, pursuing the opportunities you want to pursue, without having to carry your worries, stress, and anxiety regarding your financial security and stability. So I like to lay a foundation of strong income generation and build my lifestyle upon that base. This allows me to know my lifestyle will not be toppled by a passing storm.

That’s income investing. That’s the beauty of the Income Method.

Be the first to comment