cagkansayin/iStock via Getty Images

This article is part of a series that provides an ongoing analysis of the changes made to Prem Watsa’s 13F portfolio on a quarterly basis. It is based on Watsa’s regulatory 13F Form filed on 2/14/2022. Please visit our Tracking Prem Watsa’s Fairfax Financial Holdings Portfolio series to get an idea of his investment philosophy and our previous update for the fund’s moves during Q3 2021.

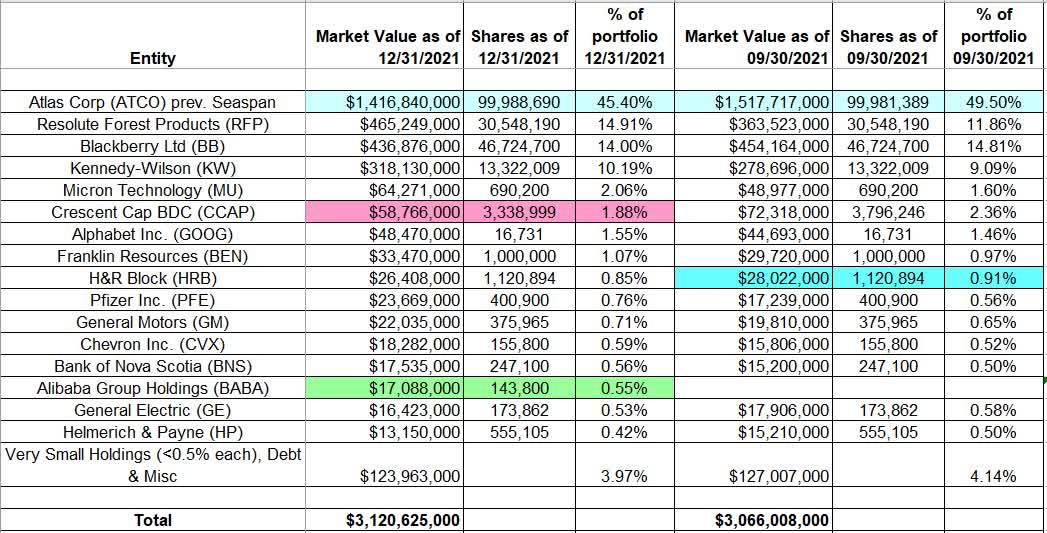

This quarter, Watsa’s 13F portfolio value increased marginally from $3.07B to $3.12B. There are 63 securities in the portfolio, but it is concentrated among a few large stakes. The focus of this article is on the larger (greater than 0.5% of the portfolio each) equity holdings. The top three positions are Atlas Corp, Resolute Forest Products, and Blackberry. Together, they account for ~74% of the entire 13F portfolio.

Note: Fairfax Financial’s (OTCPK:FRFHF) 13F holdings only represent a small portion of their overall investment portfolio. The total size as of Q4 2021 was ~$52B of which ~$22B is in cash and short-term positions. Prominent equity allocations include investments in Greece, India (OTCPK:FFXDF) and Africa (OTCPK:FFXXF). They have a huge position in CPI linked derivative contracts ($62B notional amount, $0.7M fair value, ~1.75 years average maturity) designed to protect against global deflation. FRFHF currently trades at ~$549 compared to Book Value (Q4 2021) of ~$631 per share. The equity portfolio was 100% hedged starting from around 2003 but those were removed in Q4 2016.

New Stakes:

Alibaba Group Holding (BABA): BABA is a 0.55% of the portfolio position established this quarter at prices between ~$112 and ~$178 and the stock currently trades below that range at ~$104.

Stake Increases:

Atlas Corp. (ATCO) previously Seaspan Corp: ATCO is currently the largest 13F stake at 45.40% of the portfolio. It came about because of exercising 38.46M in warrants in July 2018 and the same amount in January 2019 at $6.50 per share. The stock currently trades at $13.22. Q1 2020 saw a ~30% stake increase due to Atlas Corp’s reorganization and acquisition of APR Energy. Last four quarters have seen minor increases. They have a 47.2% ownership stake in the business. There was a marginal increase this quarter.

Note: In January 2019, Fairfax added $500M more in a structure like the first tranche made in March 2018 (debt + warrants converted early). Total investment is $1B – $500M each in equity (38.46M warrants * 2 converted at $6.50 per share) and debt. The early conversion of warrants in July 2019 resulted in Fairfax also getting 25M in 7-year warrants exercisable at $8.05 per share.

Stake Decreases:

Crescent Capital BDC (CCAP): CCAP is a 1.88% of the portfolio stake purchased in Q1 2020 at prices between $6.21 and $17.10 and the stock currently trades at $17.67. This quarter saw a ~12% trimming.

Note: Regulatory filings since the quarter ended show them owning 2.96M shares (9.6% of the business). This is compared to 3.34M shares in the 13F Report.

Kept Steady:

Resolute Forest Products (RFP): The large (top three) RFP stake is now at ~15% of the portfolio. The position was first established in Q4 2010 when it was named Abitibi Bowater and the stake has since been more than doubled. Over the years, their net investment in RFP was $745M ($24.39 per share) and the current value is ~$368M ($12.04 per share). Their ownership stake is just under ~39% of the business.

BlackBerry Ltd (BB): BB is Watsa’s second-largest position at ~14% of the portfolio. The stake was first purchased in 2010 at around $50 for 2M shares. The position was aggressively built up to 46.7M shares in the following years. Their net cost on a fully converted basis is ~$10 per share and the stock currently trades at $6.80. There has only been very minor activity in the last nine years.

Note: In Q4 2013, Fairfax co-sponsored a cash-infusion of $1B through convertible debentures ($10 conversion price earning 6% interest) – they financed $500M of that transaction and the remaining was funded by a consortium of other investment funds. In Q3 2016, those shares were redeemed, and new ones issued ($605M in 3.75% debentures convertible at $10 due 11/13/2020) to the same entities in a private placement. On 9/2/2020, those were redeemed, and new ones issued ($330M in 1.75% debentures convertible at $6 due 11/13/2023). Assuming full conversion of these debentures, Fairfax would beneficially own ~16.4% of the business (~102M shares).

Kennedy-Wilson Holdings (KW): KW stake is a large (top five) ~10% of the 13F portfolio position. Q4 2016 saw a ~40% increase at prices between $20 and $23 and that was followed with a ~8% increase in Q1 2018. KW currently trades at $23.79.

Note 1: Regulatory filings since the quarter ended show them beneficially owning 26.37M shares (13.8% of business). This is compared to 13.32M shares in the 13F report. The increase is due to 13M warrants (7-year term, $23 strike) they received as part of a $300 investment in perpetual preferred stock (4.5% dividend).

Note 2: The original 2010 stake was from a private placement for Kennedy Wilson convertible preferred stock. The total investment from that point through Q3 2016 was $645M. Since then, they have invested another ~$85M. By EOY 2015, they had already received distributions of $625M and so the net investment was ~$105M. That is compared to current market value of ~$317M.

Micron Technology (MU): MU is a ~2% portfolio position that saw a ~60% stake increase in Q1 2019 at prices between $31 and $44. The position was increased by ~115% in Q1 2020 at prices between $34.50 and $60. The stock currently trades at $72.14. Q1 2021 saw marginal trimming while next quarter there was a minor increase.

Alphabet Inc. (GOOGL): GOOG is a 1.55% stake purchased in Q1 2020 at prices between $1057 and $1527 and it now goes for ~$2666. There was a ~22% stake increase in Q4 2020 at prices between $1415 and $1827.

Franklin Resources (BEN): The ~1% BEN position was established in Q1 2020 at prices between $15.30 and $26.25 and it is now at $26.28.

H&R Block (HRB): HRB is a small 0.85% of the portfolio position established in Q1 2021 at prices between ~$15.50 and ~$22. Last quarter saw a ~45% stake increase at prices between $23.35 and $26.30. The stock is now at $26.63.

General Motors (GM): GM is a small 0.71% position. Q3 2018 saw a huge ~370% stake increase at prices between $33.50 and $40. The stock is now well above that range at $39.35.

Bank of Nova Scotia (BNS): BNS is a small 0.56% of the portfolio position established in Q4 2018 at prices between $49 and $60 and the stock currently trades at $69.65.

General Electric (GE): GE was a minutely small stake as of Q1 2018. Q2 2018 saw a ~160% stake increase at prices between ~$102 and ~$122 and that was followed with a one-third further increase next quarter at prices between ~$90 and ~$114. Q4 2018 saw another ~30% increase at prices between ~$54 and ~$110. The stock currently trades at $89.74, and the stake is at 0.53%.

Note: The prices quoted above are adjusted for the 1-for-8 reverse-stock-split in July.

Chevron (CVX), Helmerich & Payne (HP), and Pfizer Inc. (PFE): These very small (less than ~1% of the portfolio each) stakes were kept steady this quarter.

Note: Greek allocation in the investment portfolio primarily consists of Eurobank (OTCPK:EGFEY) (OTCPK:EGFEF) and Praktiker. Grivalia Properties merged into Eurobank in Q2 2019 and Watsa’s 52.4% stake got converted to Eurobank shares. Fairfax now owns ~31% of Eurobank. Their overall investment was ~$1.16B.

The spreadsheet below highlights changes to Watsa’s 13F stock holdings in Q4 2021:

Prem Watsa – Fairfax Financial’s Q4 2021 13F Report Q/Q Comparison (John Vincent (author))

Be the first to comment