Artur Nichiporenko

I like to reread the classics. It reminds me why I enjoy being an investor. Also, I like the enhanced clarity that comes with rereading these books and reinforces why I do what I do. After rereading “One Up On Wall Street”, I was fortunate to come across Preformed Line Products (NASDAQ:PLPC), a little gem of a business and the more I researched, the more I liked what I saw. Peter Lynch is an investing hall of famer who provided 29% annual returns for more than 10 years, made famous the investment philosophy known as “GARP,” which blends growth and value investing. “GARP” stands for Growth At A Reasonable Price and involves finding companies that are strongly growing and buying their stocks at reasonable prices while balancing the potential for share-price appreciation with value investing principles to help avoid overpriced investments.

When I was analyzing Preformed Line products, I was not only impressed by how well it was growing but surprised it was hardly covered by anyone on Wall Street! I guess this is where our opportunity lies. My firm belief is that an investment in PLPC looks relatively safer in this business than hundreds of other stocks that are trumpeted by Wall Street. In this analysis, I will try to point out the elements from the book and how well this business aligns with the values I understood from the book.

Investing in small companies

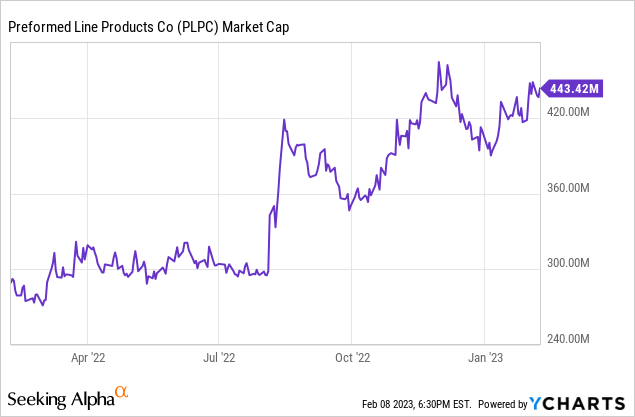

Small companies can have more upside and hence more room to grow. Peter Lynch would routinely go out of his way to find such opportunities. Preformed Line products has a long history but the company is still operating in the small cap space. This might not be the case for long. The company’s market cap appreciation in the last year alone has been more than 50% (Its total returns over the last three years has more than 2X outperformed the SP500 index). At a point in the near future, I expect this window to close.

Avoid hot stocks in the hottest industry and instead go for boring businesses

A major point in the book is hot stocks in hot industries (latest trend is anything AI) can give you quick returns but it can fade away quickly too.

If I could avoid a single stock, it would be the hottest stock in the hottest industry, the one that gets the most favorable publicity, the one that every investor hears about in the carpool or on the commuter train – and succumbing to the social pressure, often buys.

When I look at Preformed Line Products, it’s a business as boring as boring can get. It is a worldwide designer and producer of systems and products utilized in the construction and maintenance of overhead, underground, and ground-mounted networks for the telecommunication, energy, information, cable operator, and similar industries. PLP’s main products are designed to safeguard cables and wires. Additionally, the company provides hardware systems and mounting hardware for solar power applications.

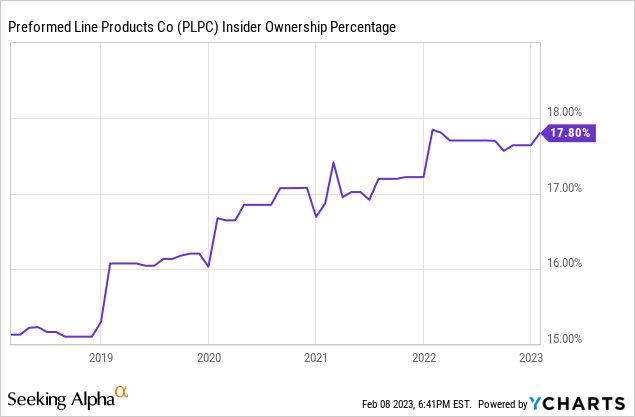

Insider buying

Insiders might sell their shares for any number of reasons, but they buy them for only one: they think the price will rise

While I see a number of insider buys over the last four years, the transactions themselves don’t seem significant. What I do see is high insider ownership and insiders continuing to hold over the long term. This is also a positive sign and indicates a high level of confidence in the company.

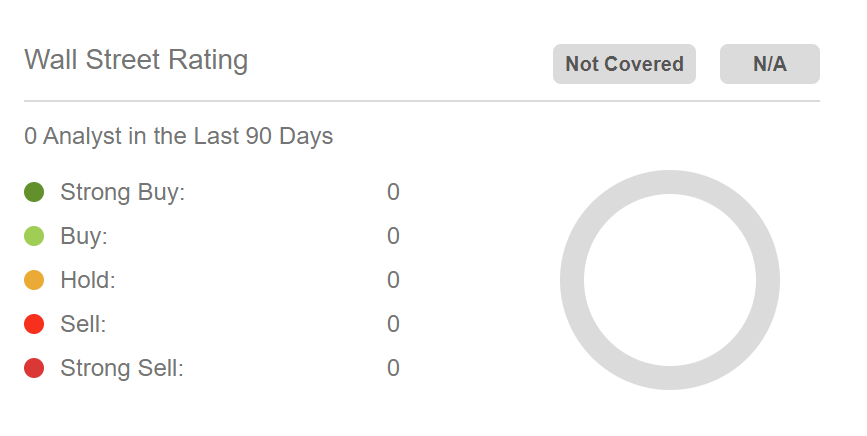

Analyst Coverage

The fewer the number of analysts that are covering, the more undiscovered the opportunity is and these are the types of overlooked opportunities that can have the most potential. Currently, this stock had no analyst coverage which demonstrates that this could be an undiscovered gem.

Seeking Alpha PLPC stock page

Growth, Earnings and Valuation

Peter Lynch viewed this as sort of a holy trifecta for investing in a stock. A growing company is good but is it growing faster than its valuation can keep up? That is key.

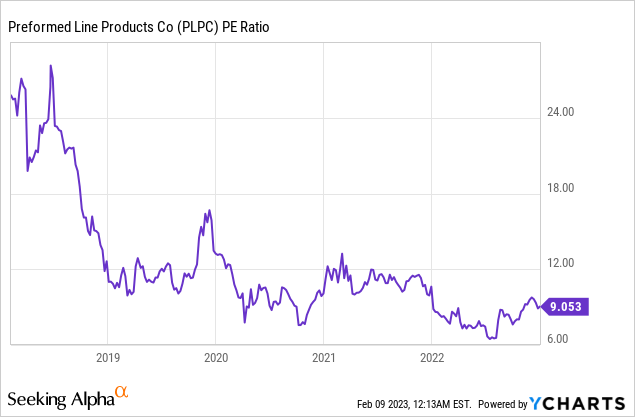

Growth has been unbroken for the last 5 years with an average revenue growth rate of 9%. The bottom line has also seen significant growth from 2017 with EPS being $2.47 and the trailing twelve months EPS coming at $9.2.

Its valuation is priced at 9X earnings and this has remained suppressed for a while now. Peter Lynch is also famous for the PEG metric, where you bring the growth rate and the PE ratio together which makes it a lot easier to compare growth and valuation. With a PEG ratio of 0.2, the stock is extremely favorable to buy at these levels in my view.

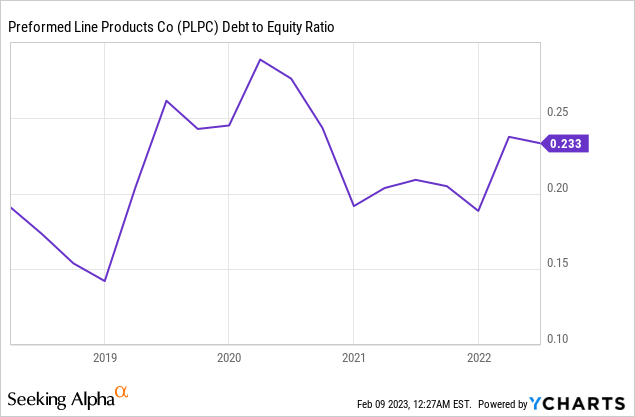

Company Debt

Investors should be particularly wary of high levels of bank debt. Looking at the debt to equity ratio, it is evident that Preformed has a strong balance sheet.

The stock also conforms to other favorable characteristics set by Lynch –

- Inventory is not growing and is under control

- Company is not engaging in “diworseification”. What this means is that firms sometimes engage in diversifying their business through acquisitions that hardly align with their core business (acquisitions made by the company in the past aligns well with their business)

- The company’s customer base is well diversified and spread across public and private utilities, communication companies and value added resellers. No single customer accounts for more than 10% of the company’s consolidated revenues

- PLPC has had a stable dividend payout and its dividend payments are thoroughly covered by earnings (low payout ratio)

Future outlook

PLPC’s future outlook remains bright as it plays a crucial role in the expanding worldwide electric power grid and 5G buildouts (its revenue mix is from utilities and telecom services providers). Demand fueled through utilities is evergreen as there is always a need to replace aging infrastructure and also to expand the grid to accommodate rising electrical demand. It has also forayed into renewable energy industry by providing products that help in the deployment and maintenance of solar and wind energy. Its product in the EV charging space is expected to benefit quite well considering the rise of electric vehicle revolution.

Why your portfolio needs this?

Most portfolios are over exposed to the movements of the SP500. PLPC’s low beta value of 0.7 suggests that this stock is less volatile and potentially less risky than the market as a whole. This is a good option for investors who are building a diversified portfolio, as they can help to balance out the risks of other, higher beta investments. But just because it’s low beta does not make it a good investment and that is why we looked at it through the lens of Peter Lynch and observed that it passes the rules set in his book.

Its long history (since 1957) as a company suggests to me that it has survived the worst and is a type of investment which is more suitable in terms of “buy and forget”. Its business model is simple and the simplicity of it reminds me of a quote from Warren Buffett:

I try to invest in businesses that are so wonderful that an idiot can run them. Because sooner or later, one will

I will be initiating a long position in PLPC and hope to bring the benefits of having this stock in my portfolio.

Be the first to comment