Eoneren/E+ via Getty Images

When I last revisited Portman Ridge (NASDAQ:PTMN) back in January, it was an update to one of my very first articles on Seeking Alpha. In that article, I reviewed how this small cap BDC (business development company) had completed a series of mergers and acquisitions over the previous three years and has turned around the portfolio to position for future growth. They also raised the dividend in November and completed a 1-for10 reverse stock split in August 2021.

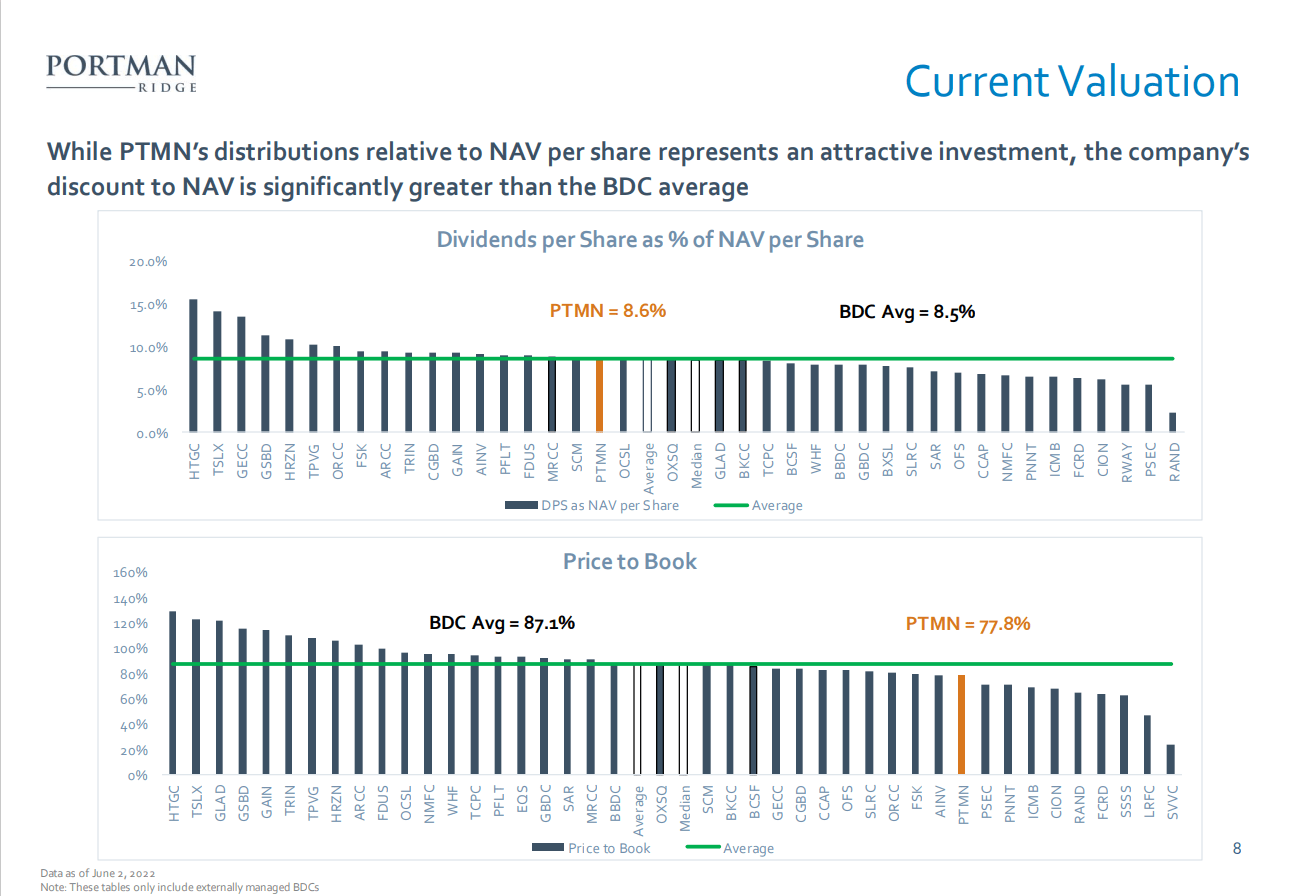

Since January the dividend was raised again in March, this time from $0.62 to $0.63 per quarter. At the current closing price of $23.02 on Friday June 24, 2022, the forward yield sits at about 11%. The stock is trading at a discount to NAV which means that the yield on NAV is actually closer to 8.6% (as of June 2), which is comparable to other BDC yields. But because the stock is trading at a discount to NAV of more than 20%, the dividend yield offers a more attractive investment than its peer (externally managed) BDCs. This slide from the June investor presentation illustrates the attractive valuation offered by PTMN at today’s price.

PTMN Current Valuation (June Investor presentation)

When considering the price to book it may also be prudent to evaluate what has happened in the past, but also understand that the business has changed in recent years. Previously, going back 5 years or more, PTMN traded at a substantial discount to NAV (book value) most of the time.

However, with recent changes to the portfolio and growth of the business via M&A activity, the past one-year period has looked different with the stock trading closer to 90% of NAV. That was the case at least until the past few months, when the trend reversed again as shown in this chart from SA.

PTMN Price to Book value (Seeking Alpha)

Like many other BDCs that I follow, the first few months of 2022 have not been kind to the market price. The current portfolio includes more than 82% senior secured loans. With industry diversification focused on mostly non-cyclical industries with high FCF generation, the portfolio is positioned nicely to withstand rising rates and inflationary pressures. Nonetheless, the market offers the shares at a good price with the current 21% discount to NAV. I would recommend scooping up some shares before the market fully recovers from its current malaise.

Comparison to Peer BDCs

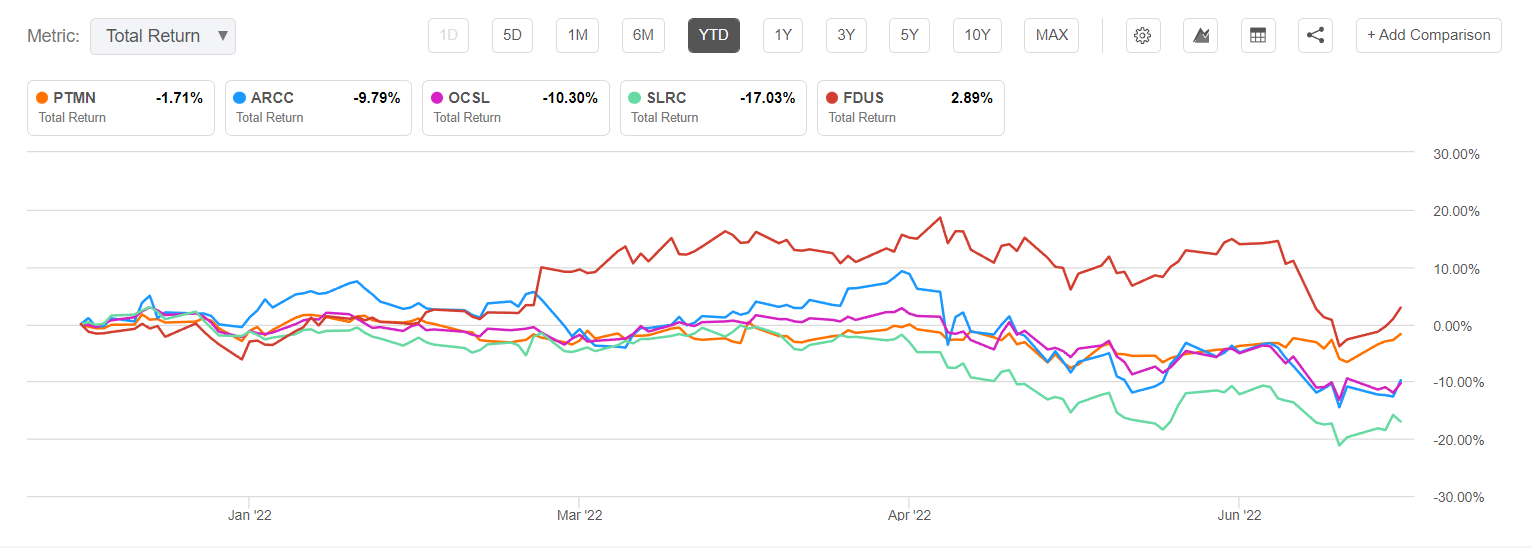

There are many BDCs in the universe of investments, but I decided to compare PTMN to several that I own or follow closely, and which are also externally managed. Scott Kennedy does a much better job than I do of comparing BDCs so you may wish to read his take on ARCC and several of its peers to learn more about the details of each of them. For purposes of this article, I chose to compare PTMN with Ares Capital Corp (ARCC), Oaktree Specialty Lending (OCSL), Fidus Investment (FDUS), and SLR Investment (SLRC), which I recently analyzed here.

The YTD total return indicates that only FDUS has performed better so far in 2022, and only by a bit.

Peer BDC comparison (Seeking Alpha)

Comparing several key factors for PTMN and some peer BDCs gives us an indication of what the current valuation is with respect to portfolio size, distribution yield, discount to NAV and past returns.

|

Ticker |

Total AUM |

Yield |

Discount |

3-yr TR (NAV)** |

YTD TR |

|

PTMN |

660M |

11% |

-21% |

3.09 |

-1.7% |

|

FDUS |

847M |

8.80% |

-12% |

19.09 |

2.9% |

|

OCSL |

2.75B |

9.90% |

-13% |

12.57 |

-10.3% |

|

ARCC |

19.4B |

9.60% |

-8% |

13.85 |

-9.8% |

|

SLRC |

2.6B* |

10.90% |

-26% |

5.8 |

-17.0% |

|

* post-merger with SUNS |

|||||

|

** 3-yr TR with dividends reinvested (source CEFdata.com) as of March 31, 2022 |

|||||

Source: author spreadsheet

For what it’s worth, all 5 of the BDCs mentioned above are ones that I either own currently or have recently owned and I would consider each of them a Buy at current prices, which represent significant discounts to NAV in most cases. Even ARCC, which typically trades at a premium to NAV is a strong buy at an 8% discount.

PTMN Portfolio Profile and Q122 Highlights

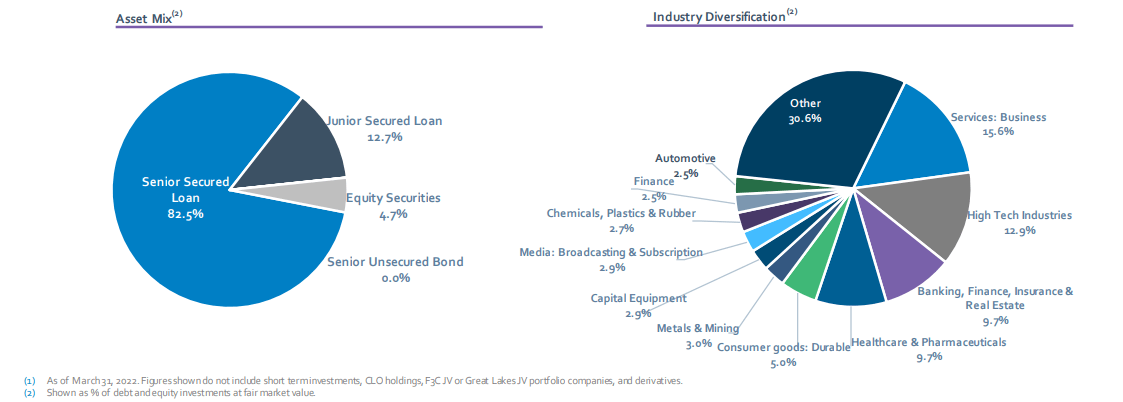

As I mentioned above, PTMN is relatively small compared to peers but is well diversified in terms of industries represented in its portfolio.

Portfolio Properties (June investor presentation)

As stated in the June investor presentation, the company’s investment objectives include:

Focus on direct origination of senior secured debt investments to the middle market; target portfolio company EBITDA between $10-50 million

Deliver strong and sustainable risk-adjusted returns to stockholders

Reduce CLO exposure over time and opportunistically

The Q1 2022 results included relatively flat NAV movement from $280.1M in Q421 to $278.3M in Q122, despite market volatility and other macroeconomic and geopolitical factors. Total investment income for the first quarter was $16.9M and NII was $7.9M ($0.82 per share), more than covering the distribution of $0.63. In addition, 22,990 shares were repurchased at a cost of $545,000. On a net basis, leverage stood at 0.97x as of March 31, 2022. Asset coverage has seen steady improvement.

Leverage and Asset Coverage (June investor presentation)

Unrestricted cash and cash equivalents totaled $20.5M with restricted cash of $63.1M as of March 31, 2022. Par value of outstanding borrowings was $352.4M with $34.4M of available borrowing capacity under the Senior Secured Revolving Credit Facility, and another $25M available under the 2018-2 Revolving Credit Facility.

Management commentary from the May 10 press release on the first quarter results included a discussion of the restructuring of their borrowing agreement:

Ted Goldthorpe, Chief Executive Officer of Portman Ridge, stated, “Despite operating in an environment with rising interest rates, market volatility, and the war in the Ukraine, we reported a relatively unchanged NAV per share for the first quarter, reduced our non-accruals, and maintained our dividend of $0.63 per share. While many of our peers have seen raised interest rates on their lines of credit and outstanding debt, we have been able to restructure our agreement with JPMorgan Chase and lower the interest rate, shift from LIBOR to SOFR, and extend the maturity date by 2 ½ years. Although investment activity and originations were lower in the first quarter of 2022 as compared to the second half of 2021, a sector-wide trend, subsequent to quarter end we have deployed approximately $35 million of our available cash in new investments and have a pipeline of an additional $20 million to $30 million we expect to deploy before the end of the second quarter.

With the overall market continuing to decline since that report, there were likely some opportunities to deploy some of that additional capital in the second quarter.

Ratings

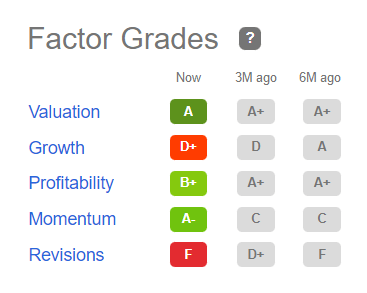

Wall Street analysts currently have 1 Strong Buy and 1 Hold rating on PTMN. The SA Quant rating is a Hold with an F factor grade for revenue and earnings revisions, and a D+ for Growth. The revisions include 1 Up and 1 Down revision for both Revenues and Earnings over the past 3 months, so not sure I agree with the F rating.

PTMN quant factor grades (Seeking Alpha)

The NAV growth seems to have stalled somewhat in 2022 as well and that may be why the Growth factor grade is not great. But many peer BDCs have also seen slowing growth in the first half of 2022 as inflation and rising rates have led to some concerns about an impending recession. So far, however, the credit market has remained stable, and some signs that inflation has already reached a peak are starting to appear. On the other hand, consumer sentiment reached a record low in June, so we may not have seen the end of the bear market just yet.

Is the Reward Worth the Risk?

That is the key question for any investment, and in my opinion PTMN has been taking all the right steps to grow the portfolio with primarily first-lien debt in a diversity of industry sectors. They have managed the balance sheet effectively in the past couple of years and are in position to deploy some additional capital during the downturn.

But if the current market environment continues to deteriorate and businesses begin to limit spending and reduce hiring or start to reduce the workforce, then prospects for continued portfolio growth will be negatively impacted. All BDCs will see the effects, and some will take a larger hit than others. With the relatively small amount of assets under management, the NAV for PTMN may be hit harder than larger BDCs like ARCC.

The distribution appears to be safe for now but if the NAV continues to decline into the second and third quarters it may not be possible to maintain the $0.63 quarterly dividend. The current discount to book value is pricing in some of that risk already. Depending on your personal risk tolerance and investment objectives, I would recommend adding in small lots to minimize the risk of further price drops should they occur.

Be the first to comment