DNY59/E+ via Getty Images

By Rob Isbitts.

Strategy

Invesco 1-30 Laddered Treasury ETF (NASDAQ:PLW) aims to deliver a pure bond “ladder” in U.S. Treasury securities. In other words, it owns Treasuries that mature from 1 to 30 years in the future. It only invests in coupon-paying Treasury Notes and Bonds, not T-Bills, Zero-Coupon bonds or Treasury Inflation-Protected Securities (TIPS).

Proprietary ETF Grades

-

Offense/Defense: Defense

-

Segment: Bonds

-

Sub-Segment: US Treasury

-

Correlation (vs. S&P 500): Low

-

Expected Volatility (vs. S&P 500): Low

Holding Analysis

PLW currently holds 28 bonds. Every maturity year is represented from 2023 through 2052, except that 2033-2035 are currently excluded. The exchange-traded fund (“ETF”) holds roughly equal-weighted positions of about 3-4% per maturity year, except for 2031 and 2036, which are overweighted at about 8% and 9% of fund assets, respectively. Those larger-weighted positions carry coupons averaging nearly 5%, so that helps boost PLW’s average coupon rate. All bonds mature on February 15 of the maturity year and were issued on that same date in the year the U.S. Treasury issued them. Thus, this is a true equal-timed ladder.

Strengths

U.S. Treasuries are still considered the highest-quality, most reliable securities on the planet. So a ladder of them carries the same implied safety level, when it comes to the potential for the bonds to mature on time, and at full “par” value. The laddered approach can potentially smooth out some of the volatility in different parts of the yield curve.

PLW is offered by Invesco, a solid ETF provider, which oversees a consistent, time-tested ladder process here.

Weaknesses

Bonds fluctuate in price, as investors found out in 2022. In fact, since longer-term bonds, even Treasuries, can fluctuate tremendously in price, investors should not look at PLW as the same thing as owning bonds individually. While owning individual bonds still comes with price fluctuation, when owned individually and not through an ETF, the choice to sell or hold to maturity is up to the owner. PLW holds bonds to maturity, so every February 15, part of the ETF’s holdings mature and is replaced by another bond, which becomes the longest-maturity bond in the fund. This mechanical process may be considered a weakness to those used to creating their own ladders, or may be viewed as a convenience to others.

Opportunities

The general nature of PLW as a bond ladder ETF was far less interesting to us a year ago. But now, after the sharpest rate-rise in Treasuries in modern history, things are getting very interesting in previously boring bond land. While we still view the Treasury market as being unsettled, as investors grapple with the rate shock of 2022, there will come a point where owning an across-the-board allocation to USTs will be an opportunity to earn both yield and profit.

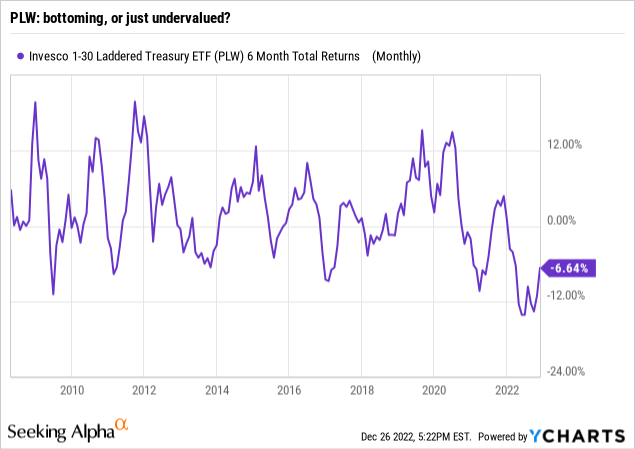

As the chart above shows, PLW is coming off of the worst 6-month period in its 15-year history. The ETF lost more than 12% in 6 months, including income payments received. And the fact is, PLW’s 10-year annualized return is a mere 0.75%. That is quite pathetic, but wholly explained by the Fed’s suppression of interest rates and its support of risk-assets over US Treasuries.

But now, the bond market may be marching to its own tune. That is already sparking investor interest in USTs in a way we have not seen in recent memory. And, with an average coupon of about 3.9% and an average bond price of about $96 (versus $100 par value), the total return outlook for PLW is as strong as it has been in a very long time.

Threats

However, the fact remains that we may be in the middle innings of the rise in long-term bond rates. The yield curve is still highly “inverted” which means that short-term bond yields are much higher than long-term yields. That is not a normal condition, and it is our belief that until it is reversed, bond risk remains (as well as stock market risk).

In addition, U.S. Treasury Secretary Janet Yellen and others have cited concerns about liquidity in the Treasury market. That problem is real, and it could prompt another period in which we see UST rates jack up higher, and bond prices falling. That is the biggest current threat to PLW in our view. The silver lining: if that comes to pass, it could make PLW an ideal ETF to own after that occurs.

Proprietary Technical Ratings

-

Short-Term Rating (next 3 months): Sell

-

Long-Term Rating (next 12 months): Hold

Conclusions

ETF Quality Opinion

PLW is near the top of our watchlist for 2023. The question is, when in 2023 will PLW be a Buy, or will it be 2024? We are patient types, and will rely on bond market events and our technical analysis to determine when it is safe to into the PLW water.

ETF Investment Opinion

In the meantime, if an investor owns PLW and is reluctant to sell it because it is a long-term laddered bond holding, we would not argue strongly against that. However, just know that while the underlying investments in PLW are Treasury-level quality, the price of PLW could easily fall a lot more in this cycle. That won’t stop some of the highest dividend payments in a long time from coming out of PLW. But it would erode principal on top of the 20% loss this ETF has suffered during 2021-2022. That’s why it is a Sell to us for now, but one we are tracking carefully for at least an intermediate-term upgrade in the foreseeable future.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment