Vanit Janthra

Another revision by Plug Power Inc. (NASDAQ:PLUG) for the company’s FY22 outlook at its business update yesterday (January 25).

The revision is significant, as management updated that it expects revenue growth of 45% to 50% for 2022, down from its initial projections of 80% growth. It’s even below the marked-down consensus estimates of 67% revenue growth, likely disappointing investors who expected better execution.

Keen investors should recall that CEO Andy Marsh & team had already downgraded their outlook for hydrogen production before their FQ3 earnings release.

As such, the recent revision likely stunned investors, calling into question the company’s execution ability. Why is it critical? Because Plug Power remains an unprofitable company that’s still finding its footing as a leading manufacturer in the green hydrogen space.

While the company highlighted a better-than-expected FY23 outlook, we believe investors will likely discount the company’s projections, given the macroeconomic headwinds.

Accordingly, Plug Power’s revised FY22 forecasts suggest Q4 revenue growth of about $260M, up 61% YoY. However, that’s way off the Street’s consensus of $336M, up 108% YoY, which was supposed to have been “de-risked.”

Management attempted to assuage analysts on the call during its business update that it has the confidence to meet its FY23 revenue projection of $1.4B.

Plug Power attributed the “tougher than expected” Q4 to its product launch cadence and attendant supply chain challenges but assured investors and analysts that “these issues have been overcome.”

Notably, management accentuated that it has not revised its backlog, suggesting that the company is confident that revenue recognition is deferred, not canceled.

In addition, management highlighted it’s ramping capacity in line with its expectations for 2023, which could lift its gross margins to 10% (exceeding consensus estimates of 9.4%). Notably, the company is expected to commence production on its Georgia facility, a model case for its future, larger-scale expansion projects in “New York, Texas, Tennessee, and Louisiana.”

Management is also confident in its clarifications on the Inflation Reduction Act (IRA) and Production Tax Credits (PTC), expecting an announcement in Q2.

Also, the company’s medium- and long-term roadmap remains unchanged from the basis discussed in our November article.

So, how should investors assess the outcome of Plug Power’s business update relative to their expectations for the company’s prospects in 2023?

First, investors must pay close attention to its supply chain visibility since it significantly hampered Plug Power’s execution in 2022. Management highlighted that it will soon be partnering with suppliers who will be manufacturing products hand-in-hand with the company.

As such, investors should expect Plug Power to discuss these partnerships moving ahead and how they could help alleviate its supply chain snafus to improve its revenue runway.

Second, we believe the macroeconomic backdrop could be improving, even though the Fed is expected to remain hawkish. The company highlighted its robust balance sheet, closing FY22 with “around $3 billion in cash.” With the Fed near the end of its rate hikes, with the potential for an earlier-than-expected pivot, it could shift the project financing dynamics in favor of Plug Power.

Third, the natural gas cost headwinds that hampered its cost of production in 2022 are expected to be less significant in 2023. Accordingly, natural gas futures (NG1:COM) are down more than 70% from their August 2022 highs.

While Plug Power was reticent to revise its margins projections for now, we believe it’s prudent to reflect near-term execution risks as it ramps production.

Notwithstanding, we believe the overall headwinds look less ominous for the company in 2023.

The question is whether market operators have anticipated the potentially more constructive outlook?

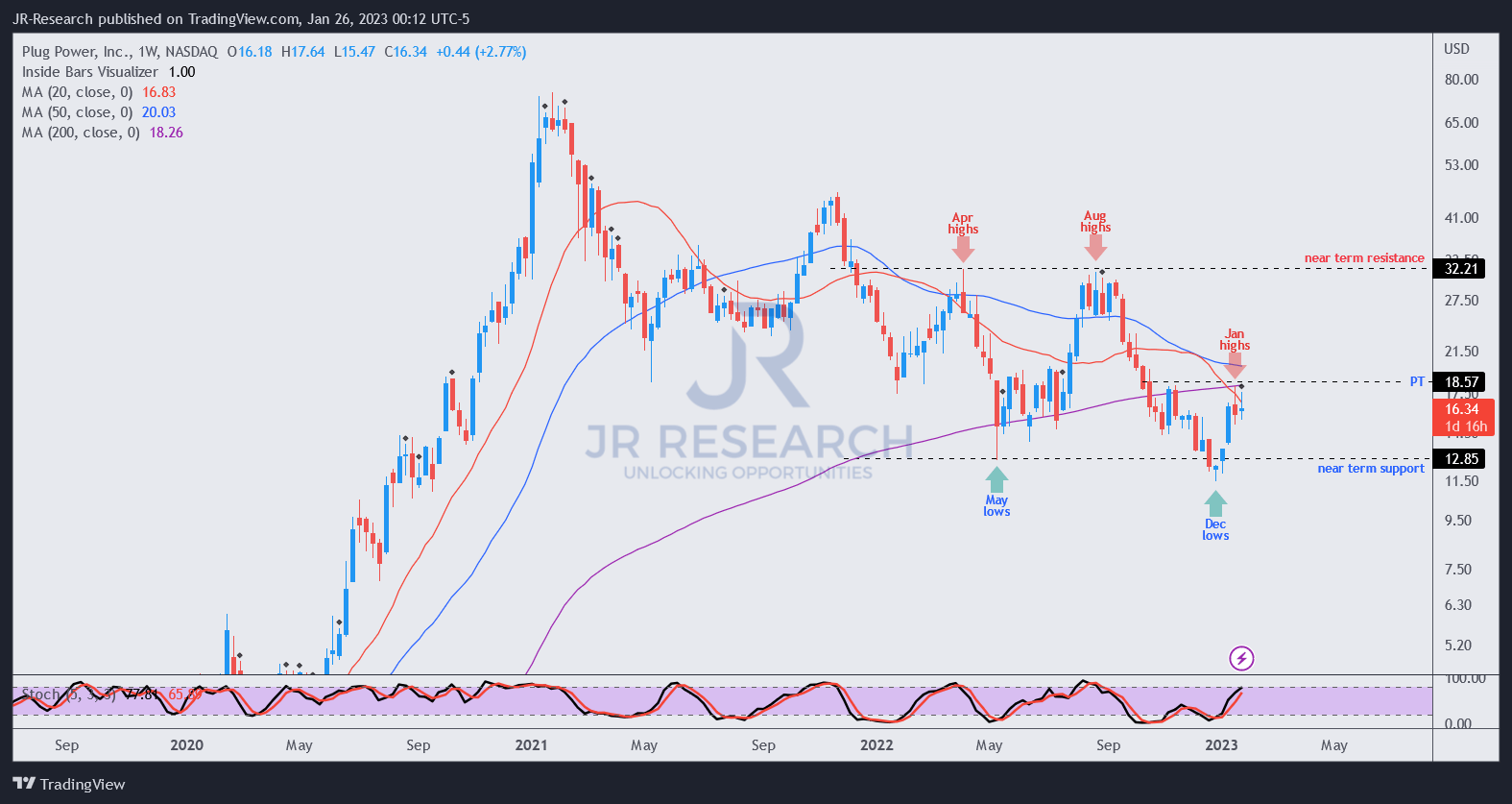

PLUG price chart (weekly) (TradingView)

PLUG’s destruction from its August highs saw it fall nearly 65% toward its recent December lows.

It’s a stark reminder for investors who bought into the momentum spike following the IRA announcement never to chase hype for an unprofitable company.

However, PLUG has recovered nearly 60% toward its recent January highs in a few weeks.

Investors should be able to appreciate the importance of improved reward/risk from picking pessimistic buy points such as its December bottom.

With PLUG heading back into overbought zones, and signs of another top appearing, we believe it’s prudent to hold back the buy trigger for now. Savvy investors have likely anticipated a more constructive outlook in 2023, with the focus now on Plug Power’s execution.

And on that point, we are still waiting for the company to demonstrate its consistency and abstain from substantial negative surprises. Until then, we believe PLUG remains a speculative position.

Rating: Hold (Revise from Speculative Buy).

Note: As with our cautious/speculative ratings, investors must consider appropriate risk management strategies, including pre-defined stop-loss/profit-taking targets, within an appropriate risk exposure.

Be the first to comment