Darren415

Investment Thesis

Pioneer Natural Resources (NYSE:PXD) is eager to return excess free cash flow back to shareholders via large combined dividends. This is the company’s focus. Meanwhile, I lay out the puts and pulls that have led to the oil market ending 2022 in a surprising lull.

My investment case is that even with a potential global recession in 2023, it’s very likely that oil prices will remain above $60 WTI. A figure that is high for a recessionary environment.

However, at this WTI price, PXD will not only be profitable but able to sustain its large dividend payout.

Big Negative Surprise for Oil

If this time last year I told you that the already tight oil market would have an unprecedented supply shock that would see supply being restricted, and that still, oil prices would finish the year towards the low end of where 2022 started, you would have struggled to believe this.

We all knew that the oil supply market is extremely tight. There were all kinds of theories floating around that even if OPEC wanted to ramp up supply, it would struggle.

Indeed, after several years of under-capital investment, there were some analysts arguing that OPEC would struggle to meet its own quotas. But has this insight mattered in the slightest in 2022? No. And you know why?

Because the trouble facing the oil market has very little to do with the supply side of the equation.

The major issue facing the oil market is on the demand side of the equation. Simply put, there’s a lot of noise and hypotheses facing the oil sector. And yet, when all is said and done, the oil sector has left many investors stumped.

So, what to do?

I believe that the solution for investors lies in PXD’s dividend program.

Capital Allocation Framework

In the section above, I provide a taste of some of the dynamics that took place in 2022. There were all the reasons why oil should be moving higher.

Nevertheless, despite all those bold, opinionated, and often well-articulated reasons for why oil prices should be closer to $100 WTI than $60 WTI, here we are; much closer to the low end of this range.

Moreover, this is what investors appear to be putting less emphasis on. But where I strongly believe is the bull case for PXD.

And this is, even at $60 WTI, PXD is still going to be substantially profitable. And not only profitable but able and willing to return a healthy dividend to shareholders.

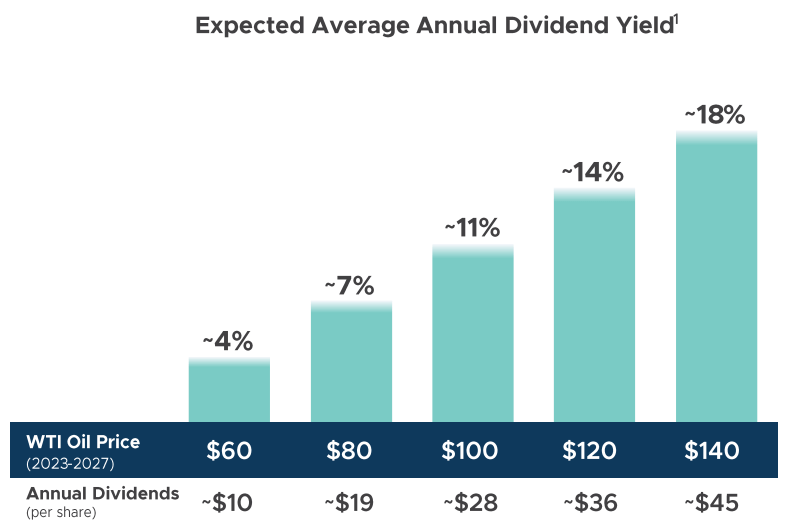

PXD Q3 presentation 2022

- At $60 WTI, investors will get approximately a 4.5% yield.

- At $70 WTI, investors will get approximately a 6.4% yield.

Simply put, as a point of fact, investors will still get a fair dividend in 2023, even if oil prices simply muddle along in the $65 to $75 WTI range.

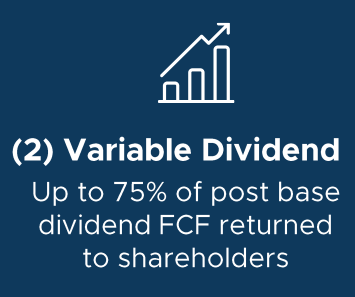

PXD Q3 presentation 2022

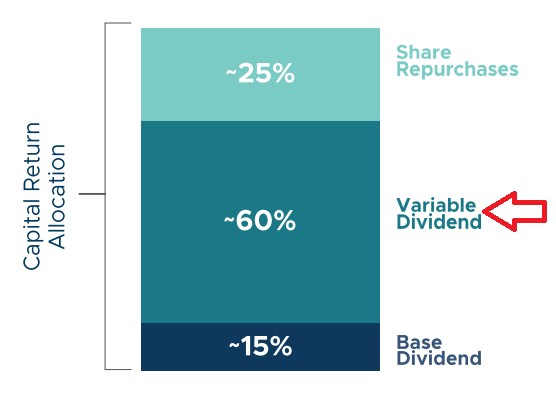

Above we see an expression of PXD’s dividend allocation strategy.

PXD has a base dividend that I believe could reach $4.85 in 2023 — a 10% increase from 2022, something that is well within the realms of possibility and even probabilities.

For this 10% estimate, I’ve gone back and looked at some of the combined base plus special dividends over the past 4 years, as you can see below.

PXD dividend history

And what you see is that over the past several years, PXD has dramatically increased its dividend payout.

Plus, on top of that, PXD will also continue to repurchase its shares in 2023. Thus, even if the share repurchases are not the needle-moving part of the bull case, it’s still better to have them than not.

PXD Stock Valuation – Approximately 7x Next Year’s Free Cash Flow

As I alluded to throughout, a potential global recession is likely to be on the cards in 2023.

And despite this event, most analysts are still expecting WTI prices to remain around $60 to $90 WTI. And if you think about it, this is a very high price for oil, particularly during an economic contraction.

PXD’s free cash flow in 2022 will probably end up at around $8 billion. Consequently, if we assume a more muted outlook for 2023, let’s work off the assumption that PXD reports around $7 billion of free cash flow in 2023.

That puts PXD’s valuation at close to 7x this year’s free cash flow. That’s clearly not an over-extended valuation by any stretch.

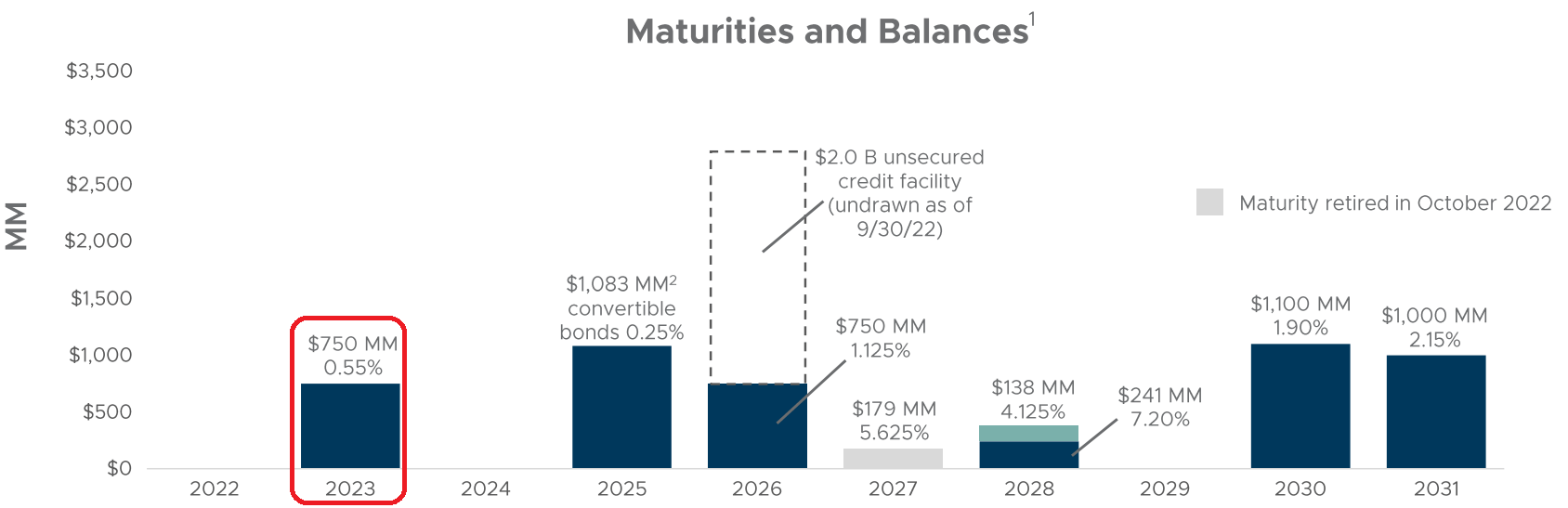

PXD Q3 presentation 2022

Also, keep in mind that PXD will retire its senior notes for 2023 and after that, it won’t have any further maturities until 2025. Hence, PXD’s balance sheet will not restrict its capital return program.

The Bottom Line

I put the bulk of my investment case on PXD’s dividend. I suspect that PXD’s base dividend will increase by 10% in 2023. By my estimates, PXD’s base dividend in 2023 will reach $4.85 per share.

PXD Q3 2022 presentation

Further, via its special dividend, I believe that PXD’s special dividend will reach around $15 per share, amounting to around 7.3% yield for its special dividend.

Thus, investors buying the stock today will get a total yield of around 9.5%. Not to mention any upside from an increase in intrinsic value, as PXD uses any remaining free cash flow to pay down debt or repurchase shares.

Be the first to comment