mphillips007

Alone among social media stocks, Pinterest (NYSE:PINS) is enjoying a rare moment in the sun. The common interest-based social media network has enjoyed a generous rally since late summer, which was additionally compounded by a favorable Q3 earnings release that showcased both a healthy beat to top-line results and a recovery in the user base.

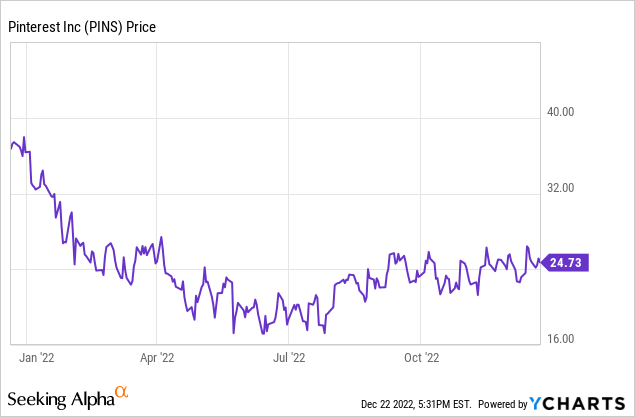

Year to date, shares of Pinterest are still in a bear market, down ~30%. This is still quite a bit better than mega-cap Meta Platforms (META), down 65% on the year, and similarly-sized Snap (SNAP), which has shed more than 80% of its market value this year.

Pinterest bulls would argue that the company has managed to stay afloat because it is a site where users are “purchase oriented” – and so being more targeted, the company has been able to hold on better to advertiser demand. Though this may be true, I still think Pinterest carries substantial risk.

In particular, here are three key risks I see for Pinterest heading into 2023:

- User trends are finicky. Pinterest rallied on Q3 results, which showcased a 12 million sequential net add in users. At the same time, y/y user counts are still down; in addition, the company’s prior-year seasonality has users peeling off in the fourth quarter of the year.

- Social media is notoriously fad-based. More to the point above – the social media landscape is littered with sites that were once popular. As has been shown with new entrants like TikTok, it doesn’t take long for a new site or app to catch fire and cannibalize existing ones.

- Relative to social media peers, Pinterest doesn’t seem as quick to slash expenses. The company announced in December that it has made a minor layoff of part of its recruiting staff and is slowing down hiring, but it has not made the deep layoffs that many of its Silicon Valley peers have. The company’s most recent quarterly results show substantial expense growth in excess of revenue growth, with adjusted EBITDA margins taking a huge hit.

On top of this, I view Pinterest’s valuation as already quite heady. At current share prices near $25, Pinterest trades at a market cap of $16.77 billion. After we net off the $2.67 billion of cash on Pinterest’s most recent balance sheet, its resulting enterprise value is $14.10 billion.

Meanwhile, for next fiscal year FY23, Wall Street consensus is expecting Pinterest to generate $3.23 billion in revenue, representing 15% y/y growth (data from Yahoo Finance). In my view, this is aggressive considering total MAU growth is flat. This would imply an increase in ad rates (unlikely as companies retrench their marketing budgets and demand for advertising continues to soften) or, more likely, ad load – in the absence of user growth. Regardless, even if we take consensus figures at face value, the company’s resulting valuation multiple is 4.4x EV/FY23 revenue – which I find to be aggressive for mid-teens growth, considering there are a number of tech stocks trading at ~2-3x forward revenue multiples that are growing much faster (examples are Asana (ASAN), FSLY (FSLY), Sumo Logic (SUMO) – all of which are on my buy list, far ahead of Pinterest).

All in all: I wouldn’t trust the latest rebound on Pinterest. Continue to stay on the sidelines here; or if you were invested in this stock, lock in your gains and redeploy the capital elsewhere.

Q3 download

Let’s now review Pinterest’s Q3 highlights to point out the trends that the market cheered on.

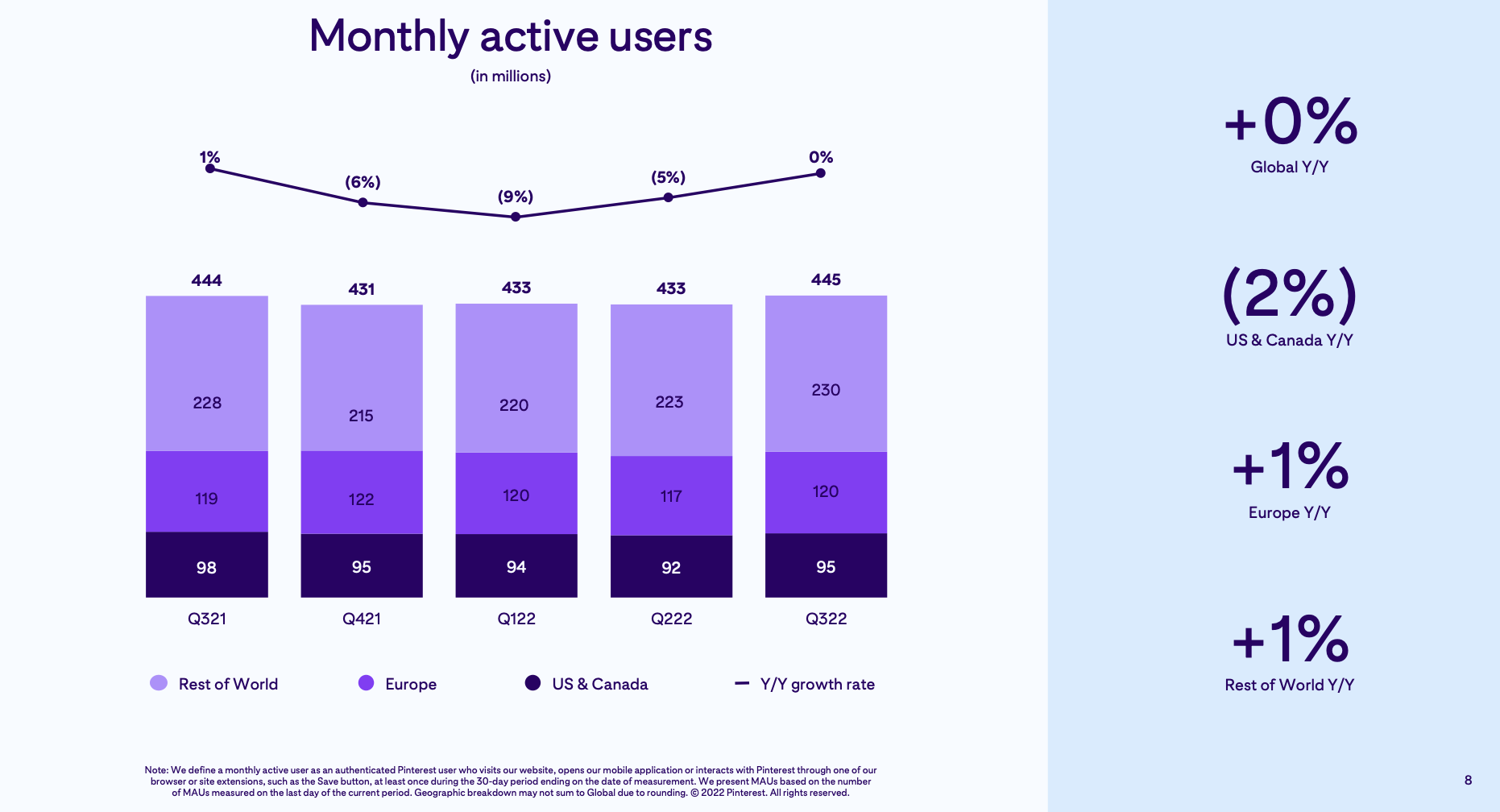

In Q3, total MAUs were flat y/y to 445 million, but added 12 million net-new MAUs sequentially versus Q2. Unlike the past few quarters, the even better news here is that the company saw U.S. and Canada users grow by 3 million sequentially (though still down -2% y/y); given these users generate the highest ARPU, trends in this key region are closely monitored. This is the first quarter since Q1 of 2021 that the company has achieved sequential growth in this region.

Pinterest MAUs (Pinterest Q3 earnings deck)

Bill Ready, Pinterest’s CEO, credits the company’s new content algorithms as the driver behind the boost in engagement. Per his prepared remarks on the Q3 earnings call:

On personalization, we’re creating much more relevant experiences for users by combining the unique first party signal on our platform, with advancements in machine learning to recommend highly relevant content to users. In Q3, this work was a meaningful driver of our return to seasonal sequential growth and global and U.S. and Canada models.

It also resulted in year on year improvement in engagement, as measured by metrics such as sessions, impressions and SES. In fact, sessions in Q3 grew meaningfully faster than now’s, which indicates that we are deepening engagement with our users. We believe growing sessions should drive multiple top-line benefits, such as reducing user churn, improving overall monetization and growing revenue per user.

We’re also making Pinterest more relevant to users by leveraging our unique human curated content, and upgrading our overall content ecosystem. In short, we want to we want content that not only inspires users, but also helps them make do or buy things.”

We should be careful here, however: we saw users drop off from Q3 to Q4 last year, and Pinterest has historically shown that its MAU counts tend to shift quickly from quarter to quarter.

We note as well that the company has cited double-digit growth in Gen Z users, and that growth has accelerated from Q2. While this is a good long-term metric for Pinterest (that is, if Pinterest survives into the so-called “long term”), Gen Z’s currently limited wallet power (loosely defined as those who are currently now between 10-25 years old) may stint the desirability of Pinterest as an advertising venue.

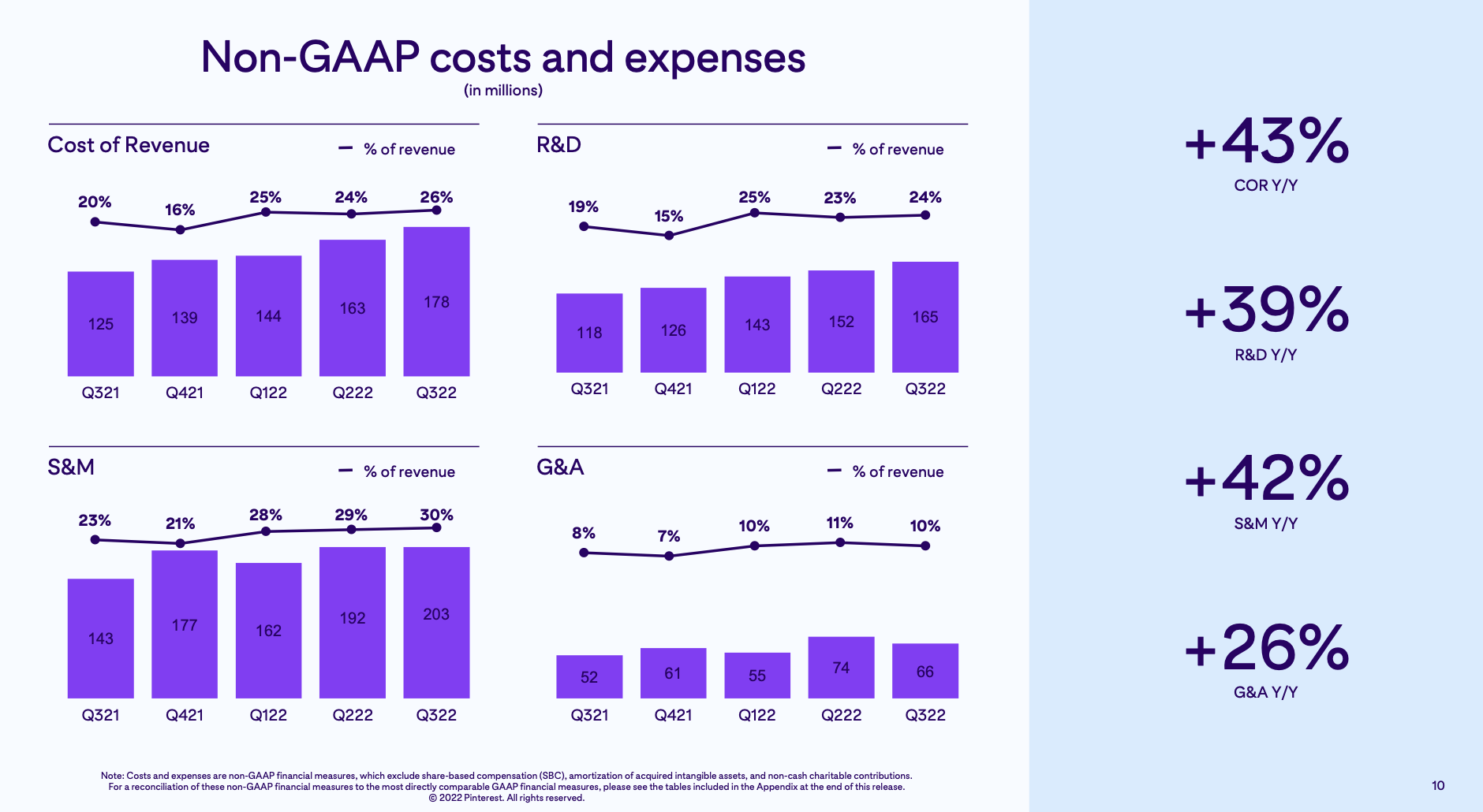

Next, we should turn to Pinterest’s expense growth. As shown in the chart below, R&D costs grew 39% y/y, sales and marketing costs grew 42% y/y, and general and administrate costs grew 26% y/y: all far faster than the 8% y/y revenue growth that Pinterest notched in Q3. Cost of revenue also inflated by 43% y/y, driven by the company’s investments in site personalization that it credited for this quarter’s user boost.

Pinterest expense growth (Pinterest Q3 earnings deck)

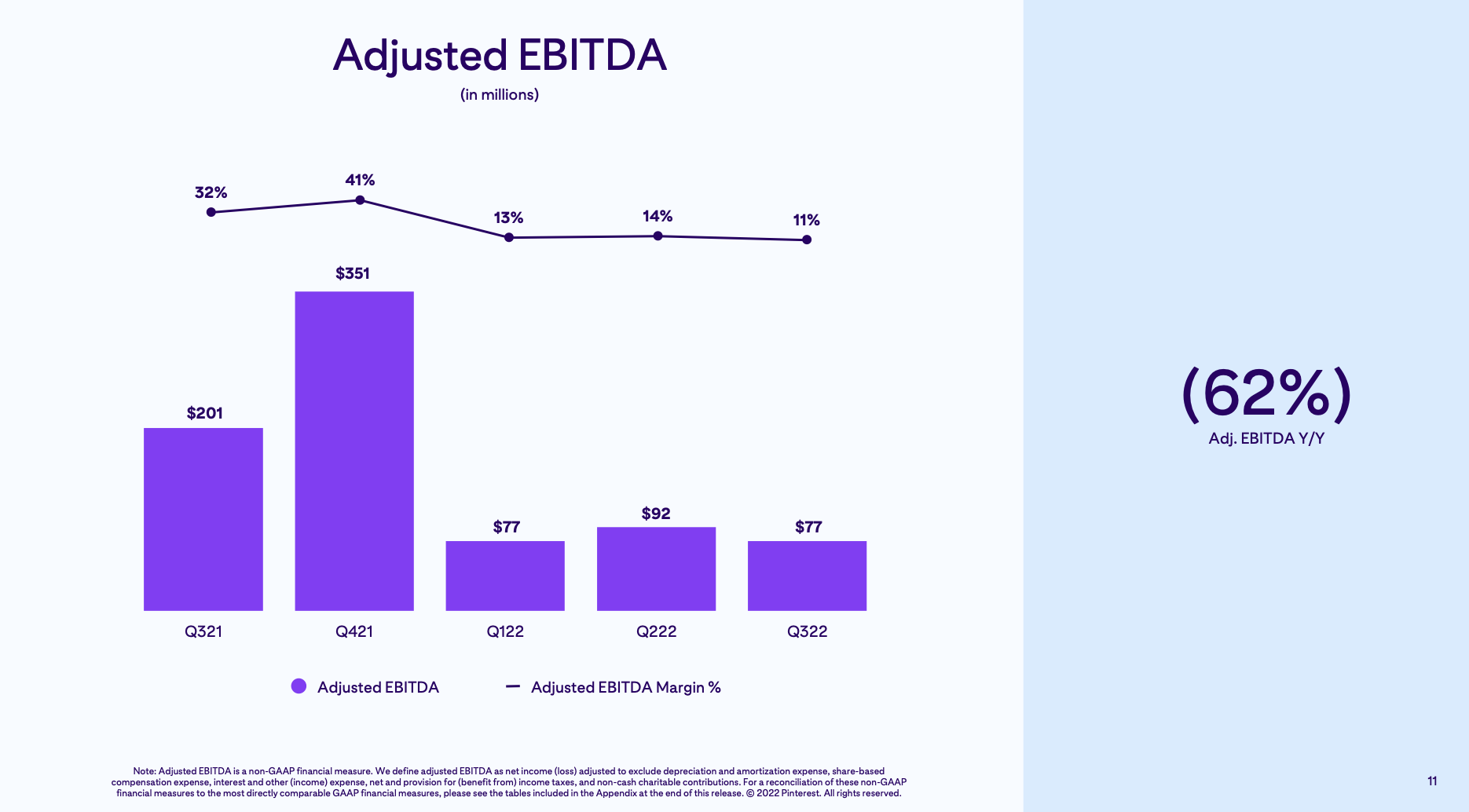

The net impact on profitability was disastrous, with adjusted EBITDA falling -62% y/y to $77 million, and adjusted EBITDA margins of 11% losing 21 points relative to 32% in the year-ago Q3:

Pinterest adjusted EBITDA trends (Pinterest Q3 earnings deck)

Amid a more risk-averse market, I think Pinterest’s huge margin declines and hesitancy to enact broader layoffs will be a major sticking point for investors in 2023.

Key takeaways

With its recent outperformance, I see little reason to stay invested in Pinterest. I think rival Meta (META) is a much better value stock to bank on for a rebound; as are countless enterprise software stocks that are currently underwater.

Be the first to comment