fizkes/iStock via Getty Images

Overview

My recommendation is to go long Phreesia (NYSE:PHR). PHR platform has strong value proposition that increases the value of the entire value chain. PHR’s platform is also seamlessly integrates into provider clients’ daily workflows, making it difficult to replace. In addition, PHR has recently expanded its addressable market by $1B by moving into the payer space with its new MemberConnect solution. The company’s strong Q3 2023 beat and raise, with continued strength in new logo growth and expansion in the life sciences segment, supports the growth potential of the company.

Business description

PHR provides hospitals and clinics with an effective toolkit for handling patient registration. The cutting-edge SaaS platform encourages patient participation in their healthcare and delivers a secure, hassle-free experience, all while empowering providers to improve the quality of patient care and increase operational efficacy.

Value-based reimbursement models adoption is a growth driver

There has been a shift in the U.S. healthcare system towards other payment models, like Value Based Care [VBC], in which providers take on more financial risk and are paid more for the quality of care they provide based on the outcomes for their patients. Recent regulatory programs like the Patients over Paperwork initiative targets to quantify patient participation and satisfaction to better reward doctors for good results in patient care. Interoperability, improved quality, and lowered overhead are three main goals of these initiatives. In the case of VBC, in order to be compliant with regulations, value-based payment [VBP] models need extensive documentation, reliable data, integrated payment capabilities, and cutting-edge analytics. The transition to APMs is bound to present healthcare providers with new challenges, some of which may be beyond their current capacity to handle without additional funding and personnel. A lot of healthcare organizations, I think, are adjusting to the new regulations and fretting over the extra time and money they’ll need to spend on complying internally.

PHR offers real-time insights required to enhance the VBC model, thereby mitigating these difficulties. In order to facilitate this, PHR make use of third-party clinical screening instruments and standardized patient-reported outcomes [PRO]. By using these PROs, PHR provider clients can better fill in care gaps, pinpoint effective treatments, and involve patients in their own care. Provider and staff productivity is enhanced by PHRs’ capacity to optimize the intake process and essential workflows, allowing for more efficient resource allocation to meet the needs of a VBC model.

Patient experience is becoming more important than ever

Patients, who are now expected to pay a larger proportion of healthcare expenses, have a vested interest in receiving better treatment, greater clarity regarding their costs, and more accessibility. Therefore, providers are making improvements to the patient experience and satisfaction a top priority in the battle to gain and keep new clients. In addition, as a result of rising competition and the advancement of more targeted therapies, the pharmaceutical industry is shifting its focus to the individual patient.

In my opinion, PHR is a game-changer in the healthcare industry because it leads to higher levels of patient satisfaction and education, greater efficiency, and higher quality care overall. Self-service patient intake is facilitated by PHR Platform’s mobile app which also enables providers to gain actionable insights. Through this, high patient utilization is made possible, which grants PHR and its clients access to patients at critical junctures in their care. PHR also assists patients in learning about applicable treatment options, which can lead to more involved interactions with healthcare providers. Furthermore, in today’s competitive, environment, PHR provides organizations with a useful medium through which to incorporate the patients’ feedback and demand into their business models.

Value proposition in a nutshell

PHR has a distinct value proposition for every target group. Patients benefit from PHR’s platform because it makes the entire intake procedure easier and provides them with more time and resources. Patients can take a more active role in their healthcare decision-making with the help of PHR because it provides them with more payment options and relevant information. The use of PHR helps medical practices streamline their processes, boost the productivity of their employees, increase their revenue, and improve both the quality of care their patients receive and their overall satisfaction with their care. Furthermore, PHR can provide more specific advertising and higher brand conversion for life sciences businesses.

Solution is mission critical

By integrating with other industry-leading Practice Management [PM] and Electronic Health Record [EHR] systems, which account for the vast majority of the total PM and EHR market, PHR is able to become an integral part of the daily workflows of its provider clients. As these integrations allow for the instantaneous exchange of clinical, demographic, and financial data, I believe this will increase the platform’s stickiness even further. As an illustration, after a provider client completes a personalized questionnaire, the data is automatically uploaded into their practice management [PM] or electronic health record [EHR], cutting down on administrative time. It will be more challenging for the provider’s organization to switch from the PHR platform if it is allowed to remain the de facto standard platform for an extended period of time. It will be a huge hassle to retrain all of the employees who rely on the platform on a regular basis, on top of the difficulty of migrating all of the digital assets.

Overtime, PHR should also be able to exert certain level of pricing power as customers have no choice but to pay, if not they have to rip and replace the entire system which is a major hassle.

Q3 2023 beat & raise indicates strength in growth

PHR had a great third quarter, posting a revenue and profit increase and beating expectations for the full year. An increase of 42% in new logos during the quarter was the most impressive statistic for me, as it showed that the product is still well-received by consumers. The life sciences sector also performed well, increasing by 33% despite headwinds from across industries.

With the help of the Insignia acquisition, PHR is able to move into the payer space, increasing its addressable market by $1 billion. This growth is being achieved by penetrating the health plan member enrollment market with the MemberConnect solution. For those 65 and up, MemberConnect helps them make informed decisions about the Medicare options that are right for them. To help patients better manage their health, MemberConnect also makes use of Insignia’s Privileged Access Management features. Similar to the current life sciences revenue model, which is based on digital engagement, PHR is compensated in a similar fashion. PHR is rebranding its Life Sciences revenue segment as Network Solutions in light of the new business addition. Together, I anticipate that the expansion of PHR’s client base will have a beneficial effect on the development of Network Solutions.

Forecast

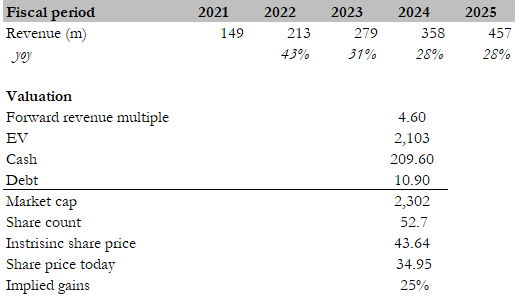

I believe PHR has 25% upside. My model indicates that it is worth $43.64 in FY24. The way I see it, PHR has a clear path to continue growing at a rapid rate, especially given that the growth momentum is still very strong based on the Q3 2023 earnings. I think the key reason is because of the strong value proposition that PHR provides to all stakeholders in the value chain. Such that, PHR increase the overall value of the value chain. Also, the acquisition of Insignia has further extended the growth runway by expanding the TAM by another billion dollars.

Using management FY23 guidance (low end of the range) and a similar growth rate over the next 2 years, I expect PHR to generate around $457 million in revenue in FY25. If we assume PHR to trade at the same forward revenue multiple, the stock is worth $43.64 in FY24, or 25% more.

Author’s estimates

Key risk

Competition intensification

The market for services like patient registration and billing is highly competitive. Patient intake services have low entry barriers on a fundamental level. A major EHR provider with comparable features could threaten the market share of PHR providers.

Conclusion

All links in the value chain benefit from the PHR platform’s compelling value proposition. The PHR platform is also extremely difficult to replace due to its seamless integration into provider clients’ daily workflows. In addition, PHR has a new MemberConnect solution that gives it a $1 billion TAM opportunity in the payer space. Growth prospects are bolstered by the company’s Q3 2023 beat and raise, which was driven by sustained strength in new logo growth and expansion in the life sciences segment.

Be the first to comment