Extreme Media

Pharvaris (NASDAQ:PHVS) is a company very focused on developing therapies for all sub-types of hereditary angioedema (HAE’). Their pipeline looks like this:

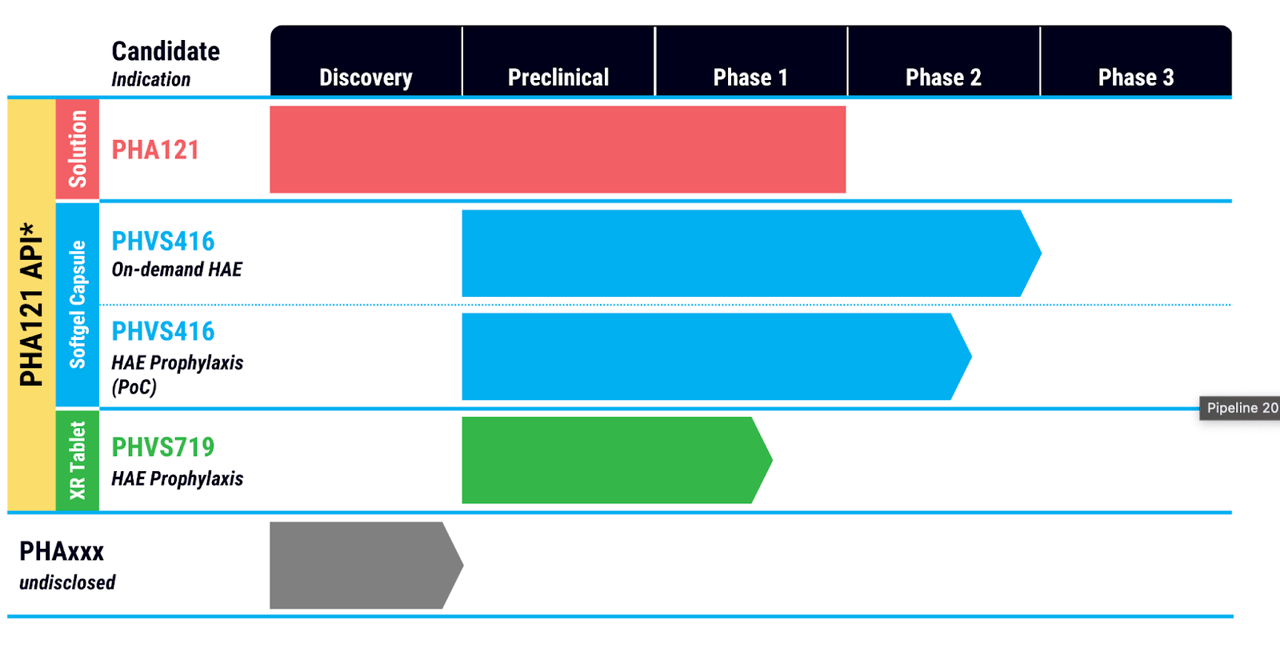

Pharvaris pipeline (Pharvaris website)

This is something new; although there are other companies targeting just one indication, I have not recently come across one with multiple molecules targeting just one indication. On closer look, however, you will see that PHA121 is the base molecule and 416 and 719 are just derivatives with different delivery and dosage schedules. PHA121 works by inhibiting bradykinin signaling through the bradykinin B2 receptor, which is downstream of other molecules targeting HAE, notably plasma kallikrein inhibitors.

Talking about competition, there are a number of kallikrein inhibitors already in the market. Here’s a list of some of these – Berotralstat (Orladeyo), C1 esterase inhibitor (Berinert, Cinryze, Haegarda). Conestat alfa (Ruconest), Ecallantide (Kalbitor), Icatibant (Firazyr) and Lanadelumab-flyo (Takhzyro). Of these, Icatibant is a bradykinin B2 receptor inhibitor just like PHA121. Other modalities include, most commonly, C1 esterase inhibitors, and also kallikrein inhibitors. C1 inhibitors occur naturally in the plasma and for decades was the main treatment modality. Here’s a long quote from rarediseases.org discussing the various treatment options:

In 2008, the Food and Drug Administration (FDA) approved Cinryze, a C1 inhibitor therapy, for routine prevention (prophylaxis) of attacks of spontaneous swelling (angioedema) in adolescents and adults with HAE. This is the first drug approved for this purpose in the U.S.

In 2009, FDA approved Berinert, to treat acute abdominal attacks and facial swelling associated with HAE in adults and adolescents. It is a protein product derived from human plasma. In 2016, FDA approved Berinert, as the first and only pediatric treatment for HAE. Also in 2009, FDA approved Kalbitor (ecallantide) to treat sudden and potentially life-threatening fluid buildup related to HAE. Kalbitor is a liquid that is intended to be injected under the skin of people age 16 and older with HAE.

In 2014, FDA approved Ruconest, a recombinant C1-esterase inhibitor for the treatment of acute attacks in adult and adolescent patients with HAE.

In 2017, FDA approved Haegarda (C1-esterase inhibitor) for administration under the skin to prevent HAE attacks.

Most recently, in 2020, FDA approved Orladeyo (berotralstat) to prevent attacks in patients 12 years of age and older with HAE. Orladeyo is an oral capsule taken one time per day.

Thus the question becomes: what differentiates PHA121?

According to the company presentation, PHA121 is:

- Convenient, orally available, small molecule

- Has higher potency and duration than previously observed for icatibant

- Can be used for both on-demand (acute HAE) and prophylaxis

If you compare these to Firazyr’s FDA approval label, it is:

- Indicated for treatment of acute attacks of hereditary angioedema (HAE’) in adults 18 years of age and older.

- An Injection, for subcutaneous use

So those are valid differences – one, that PHA121 can be used for both types of HAE, and two, it is orally available, which is only true for Berotralstat (Orladeyo) among all approved HAE medicines, and for KVD900 from rival KalVista among pipeline assets. However, the most important difference claimed by the company is “higher potency and duration,” and here the problem is that they do not have a direct comparison trial between the two molecules.

In August, PHA121 was put on clinical hold by the FDA, and the “decision was based on a review of nonclinical data.” Some analyst commentary from that time:

-

After discussions with the management, BofA analysts led by Tazeen Ahmad note that the PHVS continues to enroll and dose patients for the program outside the U.S.

-

The company has also submitted toxicology findings to the agency and has not observed any adverse events in the ongoing studies.

-

Citing previous drug approvals, the BofA team notes that the mechanism of PHA121 is de-risked and argues the full clinical hold could indicate the agency’s plans to rule out potential safety risks and understand the specifics of the drug.

That trial, RAPIDe-1, is still on hold in the US despite a Type A meeting, but published data from the trial anyway. The data showed that “PHVS416 met the main goals as an oral on-demand treatment for HAE attacks.”

Here’s some more update about the hold. I am putting this in quote because it is quite succinct:

In August 2022, the U.S. Food & Drug Administration (FDA) placed a hold on the clinical trials of PHA121 in the U.S. based on its review of nonclinical data • The agency requested that Pharvaris conduct an additional long-term rodent toxicology study and update the Investigator’s Brochure

Pharvaris participated in a Type A meeting with the FDA to discuss paths to address the on-demand and prophylactic holds

• A protocol for a 26-week rodent toxicology study has been submitted to the FDA for review

FDA has agreed to partially lift the clinical hold on on-demand

• Two remaining U.S. participants in RAPIDe-1 allowed to complete treatment of a final HAE attack per protocol

• All other clinical studies of PHA121 are currently on hold in the U.S.

Outside the U.S., the regulatory status remains unchanged for the CHAPTER-1 study and other studies, including long-term extension RAPIDe-2 study

• Pharvaris notified country-specific regulatory authorities in Canada, Europe, Israel, and the UK of the U.S. clinical holds

• All active sites outside of the U.S. continue to recruit participants in the CHAPTER-1 clinical study

The other question is the comparative difference between this and other modalities of HAE treatment. Which is better, C1 inhibitors, or kallikrein inhibitors, or bradykinin inhibitors. That is not an easy question to answer, and I can find no such head to head study. C1 inhibitors are generally not used for short term prophylaxis in the US. From what I understand of the material available to me, there’s not much difference in efficacy between the 3-4 modalities available to patients. Here’s an excerpt:

Though study protocol differences make direct comparisons of data difficult, the C1INH products, ecallantide and icatibant seem to have comparable treatment effects,[15,18,22,23] so that clinical efficacy does not seem to be a strong factor for distinguishing among them. With regard to safety, plasma C1INH products have a long and extensive history of safe use despite a theoretical risk of transmission of infectious agents. Some concern exists for allergic reactions to recombinant C1INH and ecallantide, but recent study data demonstrate this to be a greater concern for ecallantide, with its small but real risk of hypersensitivity reactions[15,24]. Icatibant appears to have an excellent safety profile to date, although clinical experience is somewhat limited. Route of drug administration is currently a distinguishing feature. C1INH products are presently approved only for intravenous use, which may present logistical challenges in some situations. There is considerable interest in the use of C1INH products subcutaneously; however, at present this remains in clinical development. Consequently, because of the unpredictability of HAE attacks, patients may face challenges in rapidly accessing IV products through clinics or emergency departments. Self-infusion programs and infrastructure are likely to improve this situation, though not every patient will be comfortable with this approach. Subcutaneous products may be attractive for many patients, but the risk of hypersensitivity reactions with ecallantide likely precludes home self-administration at present.

It appears that an oral B2R antagonist like PHA121 will have a place in the market, however, the distinguishing factor will be the mode of delivery and not efficacy or even safety directly. Like berotralstat, which is an oral kallikrein inhibitor, PHA121 could be an oral B2R inhibitor. Berotralstat made around a quarter billion dollars in 2022. That could be a ballpark figure for PHA121.

Financials

PHVS has a market cap of $354mn and a cash reserve of €198 million. R&D expenses were €14.1 million for the quarter ended September 30, 2022, while G&A expenses were €8.3 million. At that rate, they have a cash runway of around 10 quarters.

Bottomline

If the company gets its US clinical hold lifted after the 26 week rodent tox study, there should be some upside here. The company has a basic value proposition, and there’s a nice little niche market for the molecule in what is a $2bn+ worldwide market in HAE. Management has previous experience working with other HAE approved drugs, including icatibant, compared to which PHA121 may have 4x potency, per published data (see page 31 here). I would watch this closely.

Be the first to comment