Frazao Studio Latino

In this article, we revisit the Flaherty & Crumrine Preferred Income Opportunity Fund (NYSE:PFO). We recently moved part of our preferred allocation to PFO from the Cohen preferred CEF suite (e.g., PTA, LDP, PSF) which we have held over the last couple of years. PFO is trading at a 6.5% yield and an 11.6% discount.

Our key takeaway is that a partial rotation into the Flaherty suite makes a lot more sense now for three reasons. First, the correction in longer-term rates since 2021 means these funds are less exposed to a rate backup due to their longer-duration exposure in the sector. Two, all the valuation premium the Flaherty funds have enjoyed prior to around 2023 has disappeared and even reversed, making them much more attractive. And finally, now that the Fed is poised to start cutting rates, the fund’s net income should start to reverse its steep drop since 2022.

As we discuss below all of these factors hinge on a critical difference between Flaherty and other preferred CEFs – their lack of interest rate hedges. This feature explains both why the Flaherty funds were so popular up to around 2022 and also explains why they crashed and burned since then, disappointing many investors who got used to viewing them as “best in class”. This, once again, highlights the danger of viewing any CEF as “best in class” without understanding the core features which can impact performance in different market environments.

Fund Snapshot

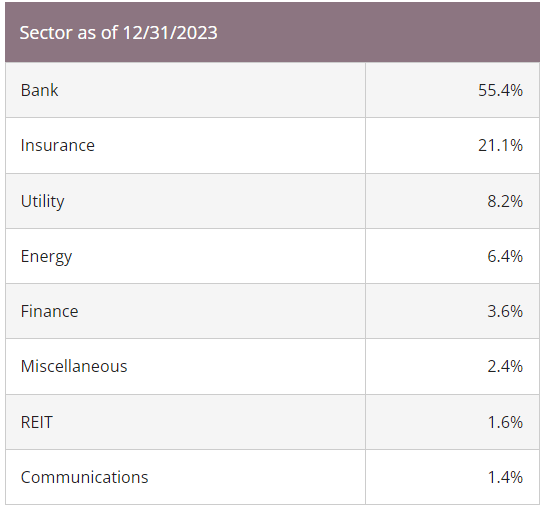

PFO has a relatively standard profile for a preferred CEF. Its top sector allocations are in financials (banks and insurance companies) alongside smaller positions in utilities and energy.

Cohen

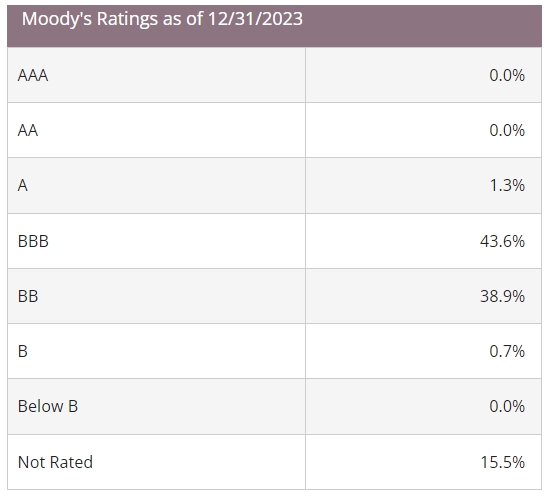

The rating profile is about half in BBB’s – the lowest investment-grade rung with the rest mostly in sub-investment-grade securities.

Cohen

Our Thinking Now

In our view, a rotation within the preferred CEF sector is beginning to look more compelling. Our Income Portfolios have only had exposure to Cohen-preferred CEFs (with the exception of tactical positions in Nuveen term CEFs JPI and JPT) after they were formed at the end of 2021.

Our Income Portfolios were set up during ZIRP or the Fed’s zero policy rate environment. The reason we have favored Cohen CEFs was due to their interest rate hedges. And although other fund families such as Nuveen and First Trust preferred CEFs also carry hedges, Cohen hedges are larger relative to their portfolios and were executed at a more favorable point in time.

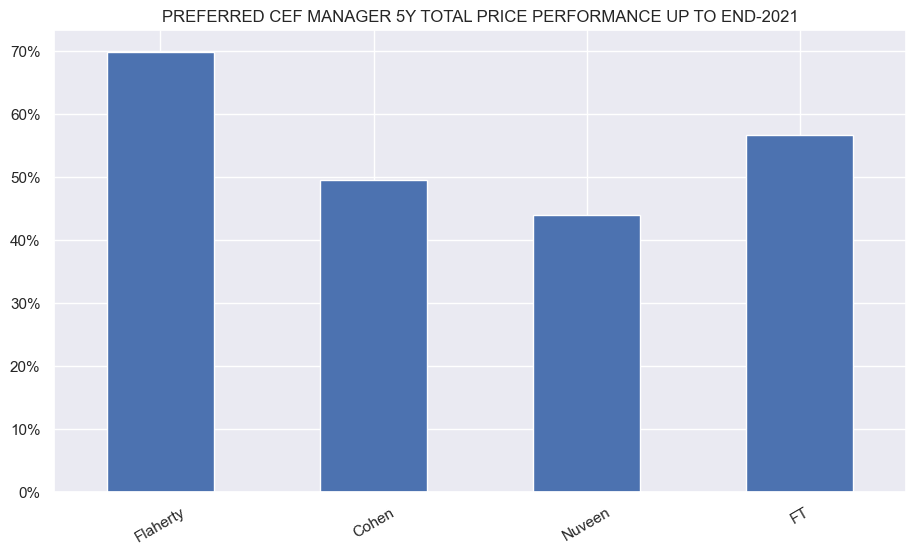

Flaherty funds benefited from a net income, total NAV and valuation perspective when rates were low and/or falling. We can see that for the 5Y period through 2021, they outperformed other “pure” preferred CEF families (we exclude the John Hancock funds as they also have significant corporate bond holdings).

Systematic Income

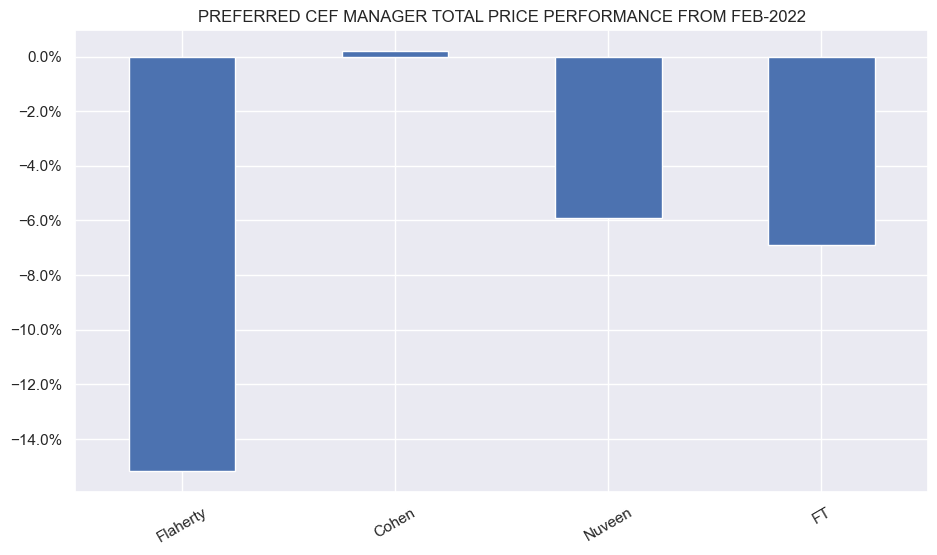

However, when interest rates started to rise, all of the tailwinds of the Flaherty funds turned into headwinds. We can see that from February 2022, when rates started to rise, Flaherty funds were now on the back foot.

Systematic Income

As a result, the Flaherty funds significantly cut their distributions by around 30% from their peak a few years ago. By contrast, the two Cohen funds which we have tended to hold fared much better. LDP cut its distribution by around 8% over the same period while PTA actually raised it.

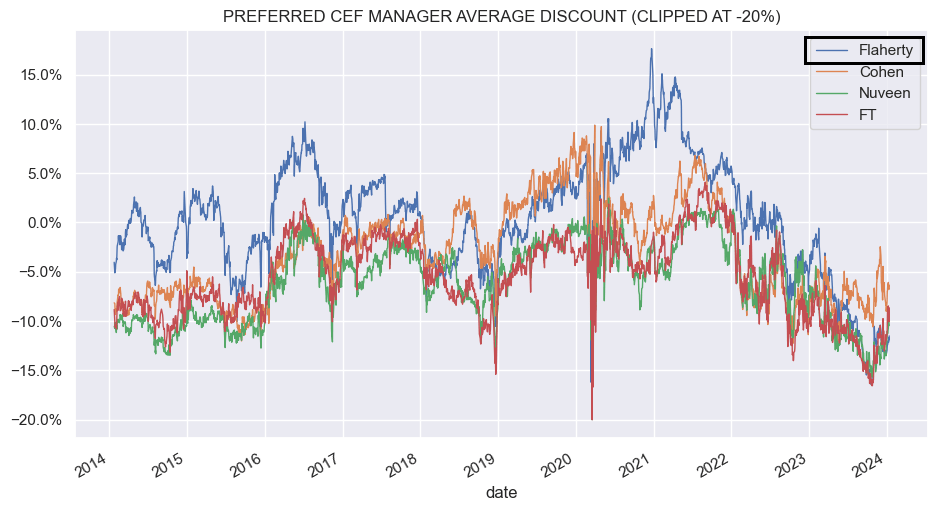

This turn in fortunes made itself felt in valuations as well. As the chart below shows, Flaherty funds (blue line) used to trade at a much tighter discount/higher premium than the other fund families. Around 2023 this changed so that the funds are now trading at the widest average discount.

Systematic Income

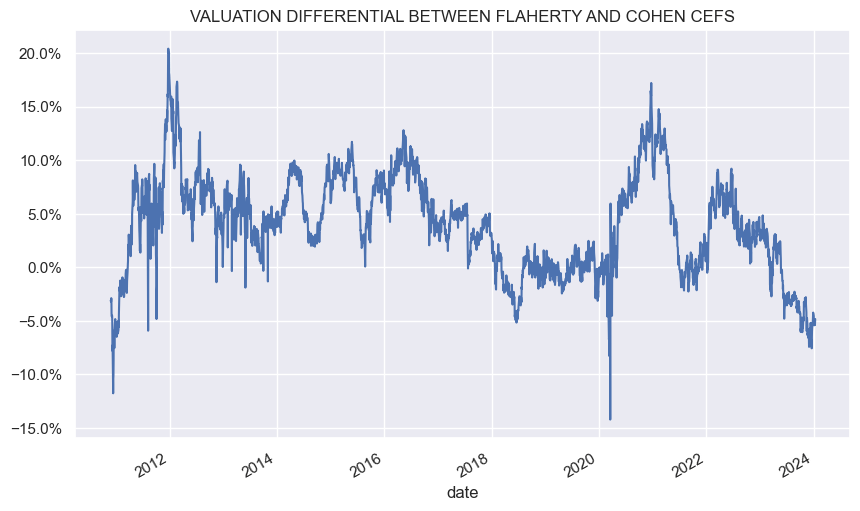

This chart shows the differential between the Flaherty and Cohen fund families more clearly. Flaherty fund used to trade at a 5% premium to Cohen funds, however, as they began to struggle from rising rates, that premium turned to a 5% discount.

Systematic Income

Since we’ve had some success with our Cohen fund allocation in the sector, the obvious question is why shift the strategy now? The answer is both obvious and nuanced.

The obvious bit is that first, longer-term rates are unlikely to keep moving higher at the same pace as they have been starting in 2022. And second, the Fed looks to be at the end of its hiking process and is expected to start cutting rates later this year. The trends that have benefited the Cohen funds at the expense of their Flaherty counterparts look to be either reversing or stopping.

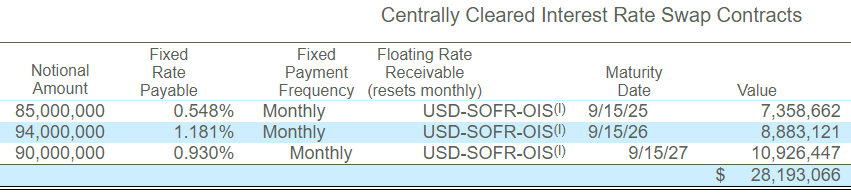

However, Cohen funds are still enjoying a much lower cost of leverage than the Flaherty funds as their hedges are still in place and it will take some time until they become uneconomical. And this is where the nuanced bit comes in. It has to do with how hedges appear on the funds’ balance sheets. In short, the Cohen hedges are already in the NAV. Let’s take a look at the hedges of the Cohen fund LDP. The fund’s swap position as of June was worth $28m or about 5% of its then NAV.

Cohen

This 5% will go to zero over time as the interest rate swaps roll down and mature. In other words, as LDP benefits from a low cost of leverage, it loses the value of its swap portfolio – dollar for dollar. The cheap cost of leverage is already baked into the NAV and this means that investors don’t have to stay with the fund to benefit from its low cost of leverage. Today’s NAV already includes that benefit until the maturity of the swaps. In other words, investors rotating from Cohen funds can, in some sense, take the hedges with them when they sell their positions.

This implicit monetization of the Cohen fund hedges as well as the fact that the Flaherty funds have a better market setup means investors with Cohen fund positions should give Flaherty funds another look after a disappointing couple of years.

Takeaways

By rotating from Cohen funds to Flaherty funds, investors can achieve three wins. First, the move monetizes the value of the interest rate hedge embedded inside Cohen funds as they are already in the NAV.

Two, the rotation potentially sets investors up for net income gains across the Flaherty suite if the Fed delivers on its expected rate cuts. Just as the Flaherty funds cut their distributions sharply when the Fed started to hike rates, we would expect them to raise the distribution once cuts materialize. The market is pricing in 5-6 cuts over the next 18 months.

Chatham

Three, the valuation picture has turned upside down with Flaherty funds going from hero to zero in a short span of time. This was primarily due to the combination of distribution cuts and worse total NAV performance given the absence of rate hedges. With a more sensible longer-term rate profile we don’t expect Flaherty funds to underperform as much as they have in the last couple of years.

In our view, a partial rotation to the Flaherty suite makes a lot of sense for investors who have been allocated to the Cohen suite in the preferred CEF sector. For investors who are initiating new positions in preferreds, it’s important to highlight that preferred credit spreads are relatively tight while longer-term Treasury yields have declined significantly from their recent peak. This suggests that we could easily see a small correction in the sector over the medium term.

ICE

Be the first to comment