Richard Drury

Investment Thesis

I last reviewed the Invesco Dividend Achievers ETF (NASDAQ:PFM) on September 22, 2022, concluding that although its fundamentals looked strong then, it operated in a crowded dividend ETF space, making its 0.53% expense ratio challenging to justify. While that remains the case today, PFM has delivered solid total returns since that article was published. Generally, high-dividend ETFs like the Schwab U.S. Dividend Equity ETF (SCHD) performed poorly, while lower-yielding funds like PFM and the Vanguard Dividend Appreciation ETF (VIG) did better.

Seeking Alpha

For this article, I took a fresh look at PFM’s spot in the dividend ETF space by examining key fundamental factors like growth, value, and quality. I was surprised that PFM offered an acceptable balance on these metrics, and although its expense ratio is a major deterrent for me, it’s still a solid choice. I look forward to presenting my findings in more detail below, and I hope to answer any questions you have in the comments section afterward.

PFM Overview

Strategy Discussion

PFM tracks the NASDAQ US Broad Dividend Achievers Index, whose primary requirement for constituents is to have at least ten consecutive years of increasing annual dividend payments. The Index follows a modified market-cap-weighting scheme with a maximum 4% weighting per stock, and it generally has low turnover each year. According to PFM’s annual report, turnover was 8-28% from 2019-2023, and I think this will appeal to passive investors. This feature allows investors to potentially build a portfolio around PFM without having to worry about the impact of its annual reconstitutions.

Still, the number of qualifying stocks each year isn’t static. One significant recent change was the addition of Apple (AAPL), which brought better earnings and dividend growth prospects to the Index, not to mention improvements in total returns. In contrast, the ProShares S&P 500 Dividend Aristocrats ETF (NOBL) requires 25 years of dividend growth, so it will be a long time before the Index has any meaningful exposure to Apple and most other Technology stocks. Microsoft (MSFT) is six years away, while Broadcom (AVGO) and Apple won’t join until 2036 and 2039, respectively.

Composition Differences

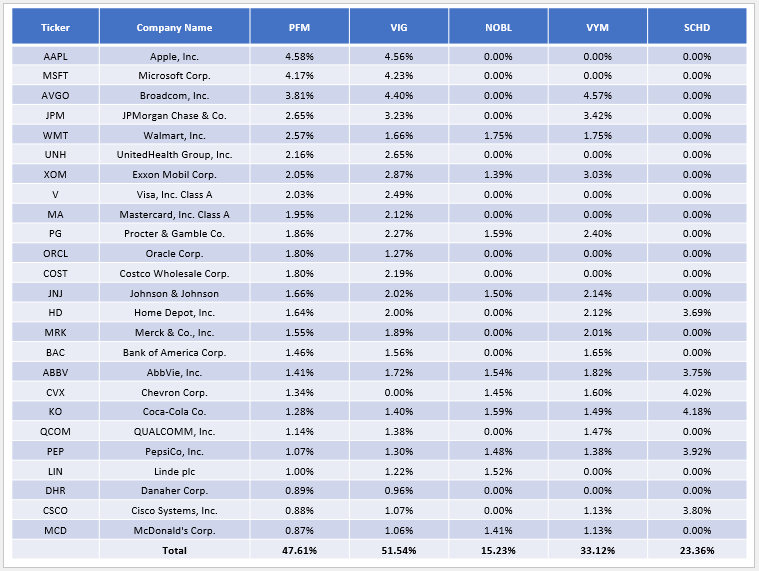

I want to highlight the composition differences between PFM and four other dividend ETFs: VIG, NOBL, the Vanguard High Dividend Yield ETF (VYM), and SCHD. As shown below, PFM’s top 25 holdings total 47.61%, and VIG is the most similar, with 51.54% allocated to these stocks. NOBL is the most different at 15.23%.

The Sunday Investor

These composition differences help explain recent results. With at least some exposure to low-yielding growth stocks, PFM and VIG delivered decent returns. In contrast, NOBL has little exposure to Technology stocks, and SCHD only considers stocks in the top 50% by dividend yield after its initial screen for ten consecutive years of dividend payments (not growth). With its modified market-cap-weighting scheme, SCHD’s selection process tilts heavily toward large-cap value, while PFM is somewhere between value and blend.

PFM Analysis

Dividends

It’s reasonable to assume that since PFM tracks an Index of stocks that have increased dividends for at least ten consecutive years, the ETF will also deliver dividend growth each year. However, ETFs are not individual stocks. Instead, they represent a basket of stocks, and other factors can influence the dividend payments shareholders receive, including:

- rebalancings, which involves selling top-performing, low-yielding stocks

- reconstitutions, which may add low-yielding stocks like Apple

- fund expenses, which directly reduce distributions

- the timing of when new ETF units are created or redeemed

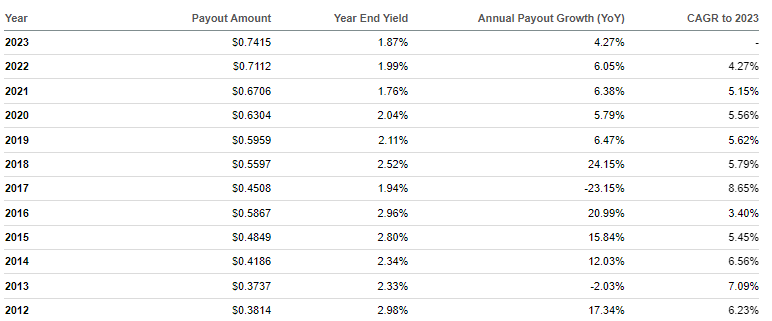

The last point is often overlooked, but consider the following scenario. As of December 31, an ETF with 10 million shares has received $20 million in underlying dividend payments for Q4 that it plans to distribute to shareholders on January 15 ($2 per share). However, in anticipation of a large dividend payment, 2 million new shareholders buy the ETF before the ex-dividend date, diluting the payment to $1.67 ($20 million / 12 million shares). I suspect this happened to PFM in 2013 and 2017 when dividend growth was negative.

Seeking Alpha

In short, an ETF’s dividend cut does not indicate that its constituents also cut their dividends. Regardless, investors are made whole, with the $0.33 per share difference in the example above flowing through to the ETF’s NAV. For this reason, I’m less interested in PFM’s historical dividends and more interested in the dividend consistency, growth, safety, and yield features of its current constituents. You might be familiar with Seeking Alpha’s Factor Grades for these metrics, and I’ve normalized and weighted them on a ten-point scale for hundreds of U.S. Equity ETFs. Below is how PFM ranks on these metrics in the large-cap value category, which includes 97 ETFs.

- Dividend Consistency: 8.62/10 (#6/97)

- Dividend Growth: 8.28/10 (#9/97)

- Dividend Safety: 8.27/10 (#6/97)

- Dividend Yield: 4.40/10 (#89/97)

In a nutshell, PFM looks excellent for dividend consistency, growth, and safety but terrible for yield, a metric that looks even worse after considering its expense ratio. Given the limited number of year-to-year changes, shareholders must accept this setup or look elsewhere if high income is an objective.

PFM Fundamentals By Sub-Industry

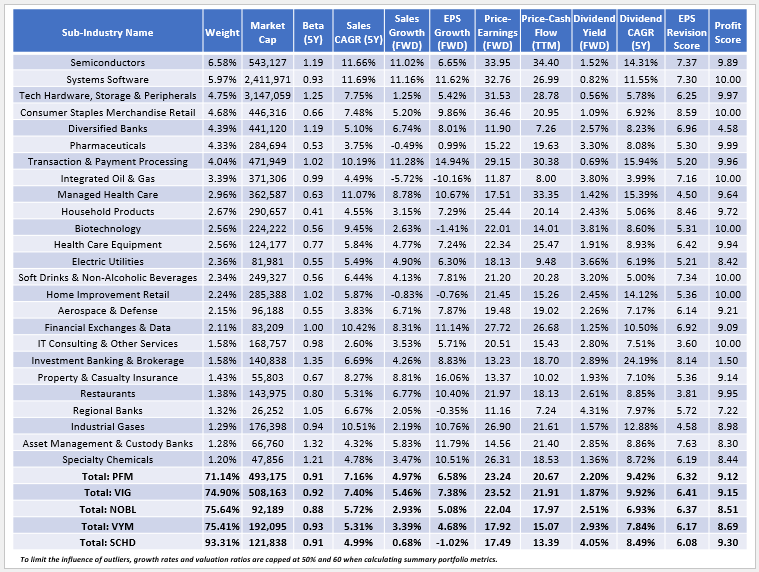

A different way to examine PFM is by looking at its composition by sub-industry. Under this view, PFM’s top 25 total 71.14%, slightly less than VIG, NOBL, and VYM. Therefore, despite holding 424 stocks, many are inconsequential. For instance, the bottom half (212) comprises just 4.42% of the portfolio.

The Sunday Investor

Here are four additional observations to consider:

1. PFM’s weighted average gross dividend yield, also known as the Index yield, is 2.20%. After subtracting its 0.53% expense ratio, the expected dividend yield is only 1.67%, which is close to the fund’s 1.73% trailing dividend yield. Notably, VIG holds lower-yielding stocks but due to its lower expense ratio, shareholders end up with a slightly better 1.81% expected dividend yield. At the opposite end is SCHD, with a 4.05% Index yield or 3.99% expected dividend yield.

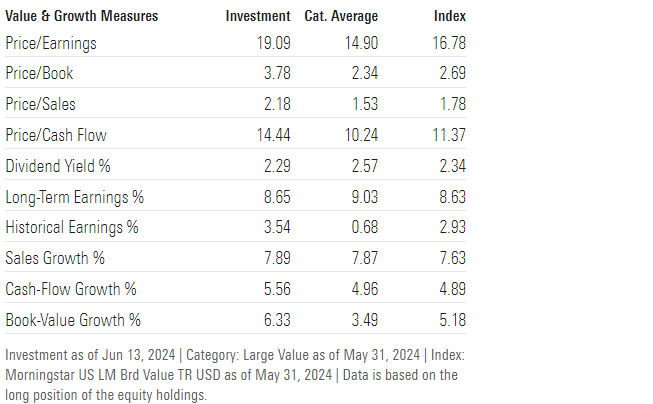

2. Like with VIG, PFM’s lower-yielding stocks boost its growth profile, a feature desperately needed to avoid significant underperformance in growth-favored markets. SCHD shareholders realize this now, though the writing was on the wall for a couple of years for those monitoring estimated sales and earnings per share growth trends. PFM’s estimated growth rates are 4.97% and 6.58%, respectively, about 0.5-1% lower than VIG. In exchange, PFM trades at a slightly more favorable valuation: 23.24x forward earnings under the simple weighted average method and 19.13x under the harmonic weighted average method used by sites like Morningstar. My calculation matches Morningstar’s (19.09x), but the following table reminds us that PFM is high vs. the 14.90x category average.

Morningstar

For those who prefer rankings, PFM’s forward P/E ranks #86/97 among the large-cap value ETFs I track. VIG, NOBL, VYM, and SCHD rank #87, #83, #39, and #35, and generally, their valuations compensate investors for less growth. The outlier is SCHD, whose -1.02% estimated earnings growth rate is the fourth-worst in the category, making it a one-sided value play.

3. PFM’s constituents have increased dividends by an annualized 9.42% over the last five years, in line with VIG’s and 1-3% better than NOBL, VYM, and SCHD. As discussed earlier, ETF distributions don’t always reflect this growth rate, but dividend growth is happening, and it’s probably close to the best you can get in the current environment. PFM offers sufficient growth, consistency, and safety but lacks the yield to make it suitable for income investors.

4. One of PFM’s best features is its high quality. Recall how the Index does not use direct quality screens. Still, ten consecutive years of dividend growth and a market-cap-weighting scheme are two indirect features that result in a profit score that ranks #22/97 in its category. PFM’s 9.12/10 profit score, which I derived using Seeking Alpha Profitability Grades, is well supported with metrics and category rankings as follows:

- Return on Assets: 9.71% (#19/97)

- Return on Equity: 26.22% (#15/97)

- Return on Total Capital: 14.86% (#18/97)

- Net Margin: 18.97% (#14/97)

However, VIG ranks better on all these metrics. I’m struggling to see how PFM justifies charging 0.53% per year in fees when VIG, a similarly constructed ETF with almost identical fundamentals, is available for only 0.06%.

Investment Recommendation

It’s difficult to criticize high-quality funds too much, as they likely will perform well over the long run. However, VIG has a highly similar composition and fundamentals, and since its 0.06% expense ratio is much more affordable, I can’t recommend readers buy PFM. Therefore, I have assigned a “hold” rating, and I look forward to answering your questions in the comments below.

Be the first to comment