Fahroni

Over the past year or so, the automotive retail space has not been considered by many investors to be particularly appealing. Rising interest rates and a potential slowdown in the economy has led to serious concerns regarding the future of automotive retail in the near term. For value investors, this has created some interesting opportunities, one of which involves Penske Automotive Group (NYSE:PAG), a firm that sells vehicles, provides collision services, and more. For the most part, fundamental data reported by the company has been quite positive. Although we have seen some weakness reported recently, sales, profits, and cash flows have been generally on the rise. In the near term, I fully suspect that we will see some weakness in the company’s operations. But it’s also true that shares of the business still look quite affordable at this time. Because of this and in spite of the fact that the stock is on the pricey end of the spectrum relative to similar firms, I would make the case that the company still offers investors with some upside potential from here. And as such, I have decided to keep the ‘buy’ rating on its stock for now.

A great ride so far

Over the past year or so, there are few companies that I have written about as much as I have written about Penske Automotive Group. Having said that, the last time I did assess the firm was in an article published in July of 2022. In that article, I talked about how the firm had continued to significantly outperform the broader market. At that time, financial performance achieved by the firm remained robust but fears were beginning to mount regarding the economy more broadly. Relative to similar firms, shares of the company did look pricey. But that did not change the fact that I viewed the business as being undervalued. This led me to keep the ‘buy’ rating I had assigned the stock previously in place, a rating that indicates upside potential that should exceed with a broader market could achieve over the same window of time. So far, the market seems to have agreed with me. While the S&P 500 is up 5.8% since the publication of that article, shares of Penske Automotive Group have generated a return for investors of 11.5%. Since I first wrote about the company in October of 2021, the return disparity is even greater, with shares returning 20.1% compared to the 7.4% decline experienced by the broader market.

Author – SEC EDGAR Data

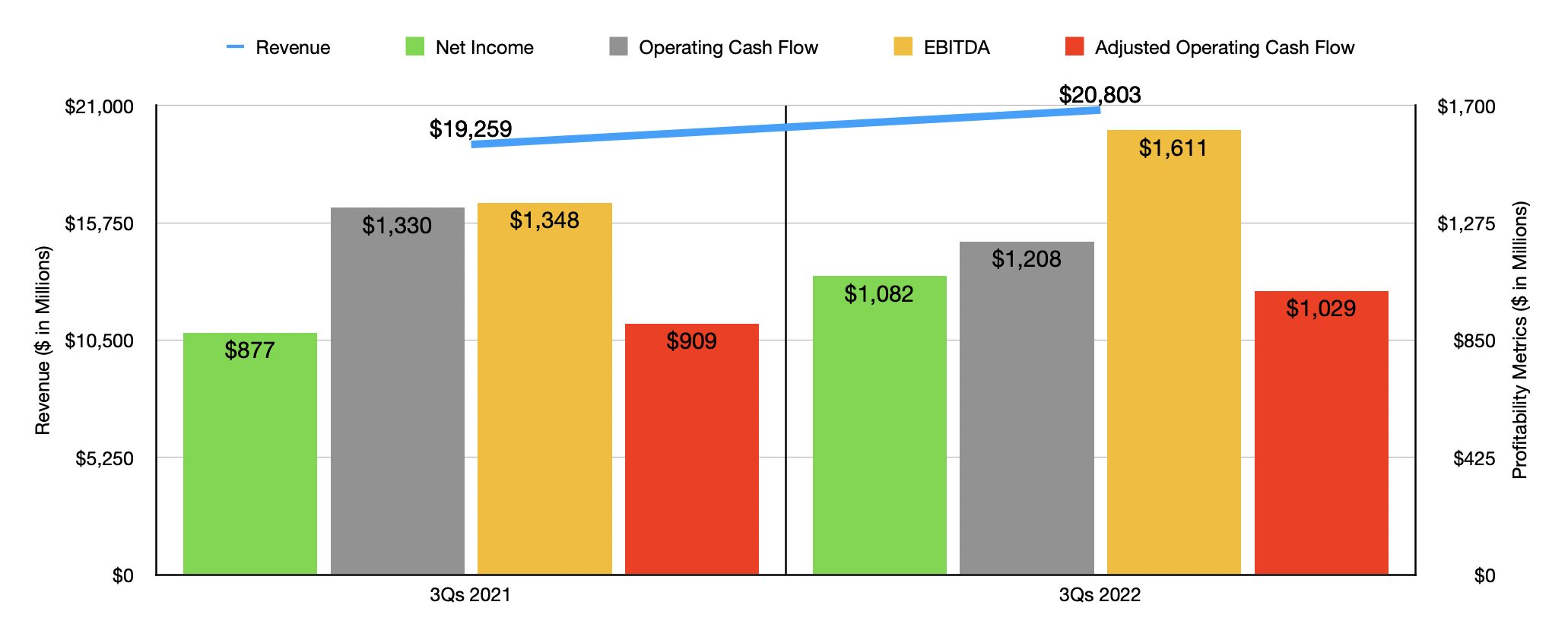

To best understand why the company continues to outperform the market, I need only point to financial results covering the 2022 fiscal year so far. During the first nine months of the year, sales came in at $20.80 billion. That’s 8% higher than the $19.26 billion generated the same time one year earlier. This growth in sales was driven largely by robust revenue from the company’s used vehicle operations. Total revenue in the first nine months from this unit came out to $7.02 billion. That’s 9% higher than the $6.44 billion reported the same time one year earlier. This came even as the number of retail units sold contracted by 0.9% and was driven, instead, by an average increase in pricing per unit of 10%. The company also benefited from an 11.7% increase in service and parts revenue, with sales rising from $1.60 billion to $1.79 billion. Another key driver was the retail commercial truck dealership portion of the company, with sales skyrocketing 46.2% from $1.11 billion to $1.62 billion. In addition to seeing a 36.1% rise in new retail unit sales, the company also saw revenue per unit climb 7.4% year over year. Meanwhile, finance and insurance revenue for the company jumped by 10.8%, rising from $583.8 million to $646.8 million. This is not to say that everything for the company was great. New vehicle sales, for instance, declined by 2.9%, with a 9.3% increase in pricing more than offset by an 11.2% decline in new retail units sold.

For the most part, this increase in revenue brought with it improved profitability. Net income of $1.08 billion beat out the $876.5 million reported the same time of the 2021 fiscal year. It is true that operating cash flow worsened, falling from $1.33 billion to $1.21 billion. But if we adjust for changes in working capital, it would have risen from $909 million to $1.03 billion. And finally, EBITDA for the company also improved, rising from $1.35 billion to $1.61 billion.

Author – SEC EDGAR Data

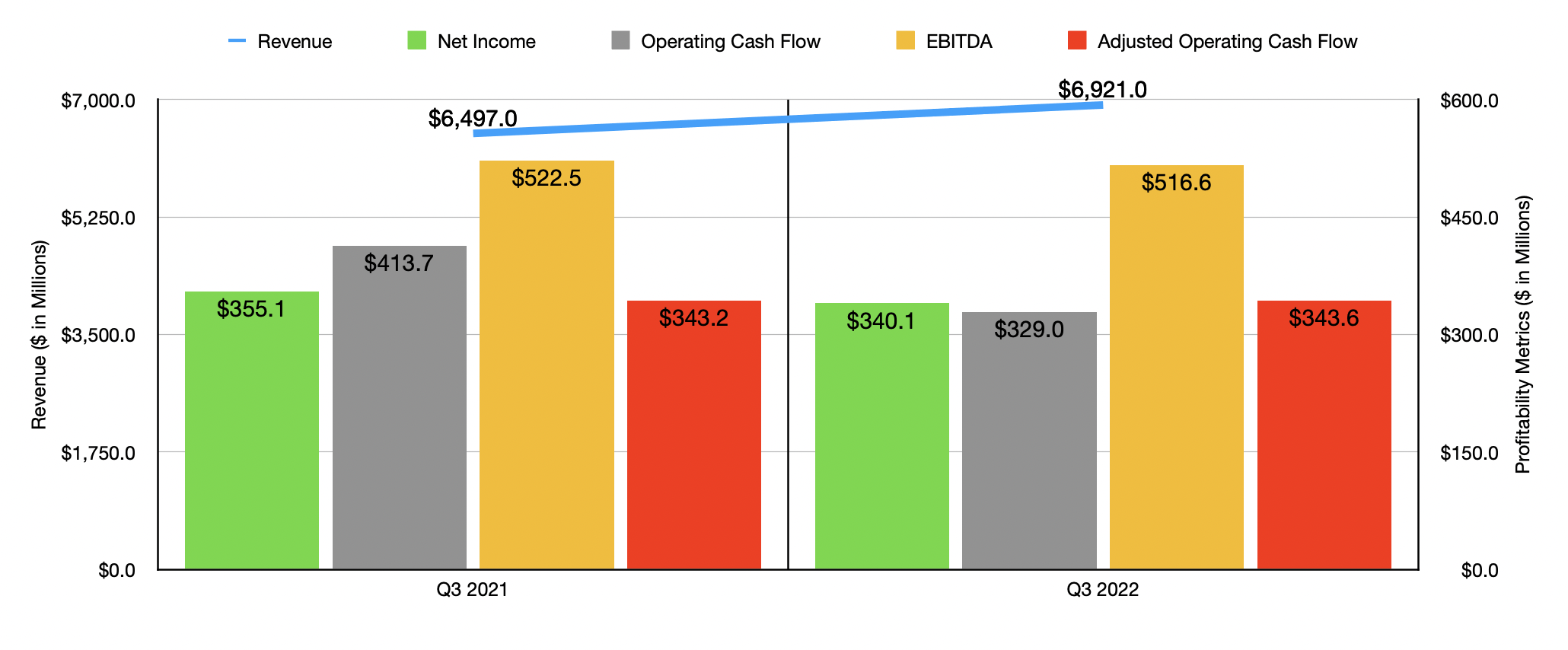

Although this data looks generally positive, it should be mentioned that the firm has shown some weakness as time has gone on. To see what I mean, we need only look at data for the third quarter of 2022. Sales there did increase year over year, climbing from $6.50 billion to $6.92 billion. Surprisingly, new vehicle sales actually grew by 5.3% while used vehicle sales dropped by 4.1%. While this is great to see, all of the growth associated with new retail unit sales was driven by acquisition activities. Same-store new retail unit sales actually fell 6.4% year over year. Low inventories and high prices impacted new and used sales alike. During this time, the company also reported some problems when it comes to profitability. Net income, for instance, shrank from $355.1 million to $340.1 million. Much of this pain seems to have come on the used vehicle side, with gross profit shrinking 37.9% year over year as consumers have hit their limit when it comes to what they can spend. Other profitability metrics have largely followed suit. Operating cash flow dropped from $413.7 million to $329 million. Even if we adjust for changes in working capital, it would have risen only modestly from $343.2 million to $343.6 million. Meanwhile, EBITDA for the company also decreased, dropping from $522.5 million to $516.6 million. These recent troubles have not stopped the company from buying back a significant amount of stock. From the start of 2022 through October 25th, the firm bought back 6.4 million shares for a combined $675.1 million.

Author – SEC EDGAR Data

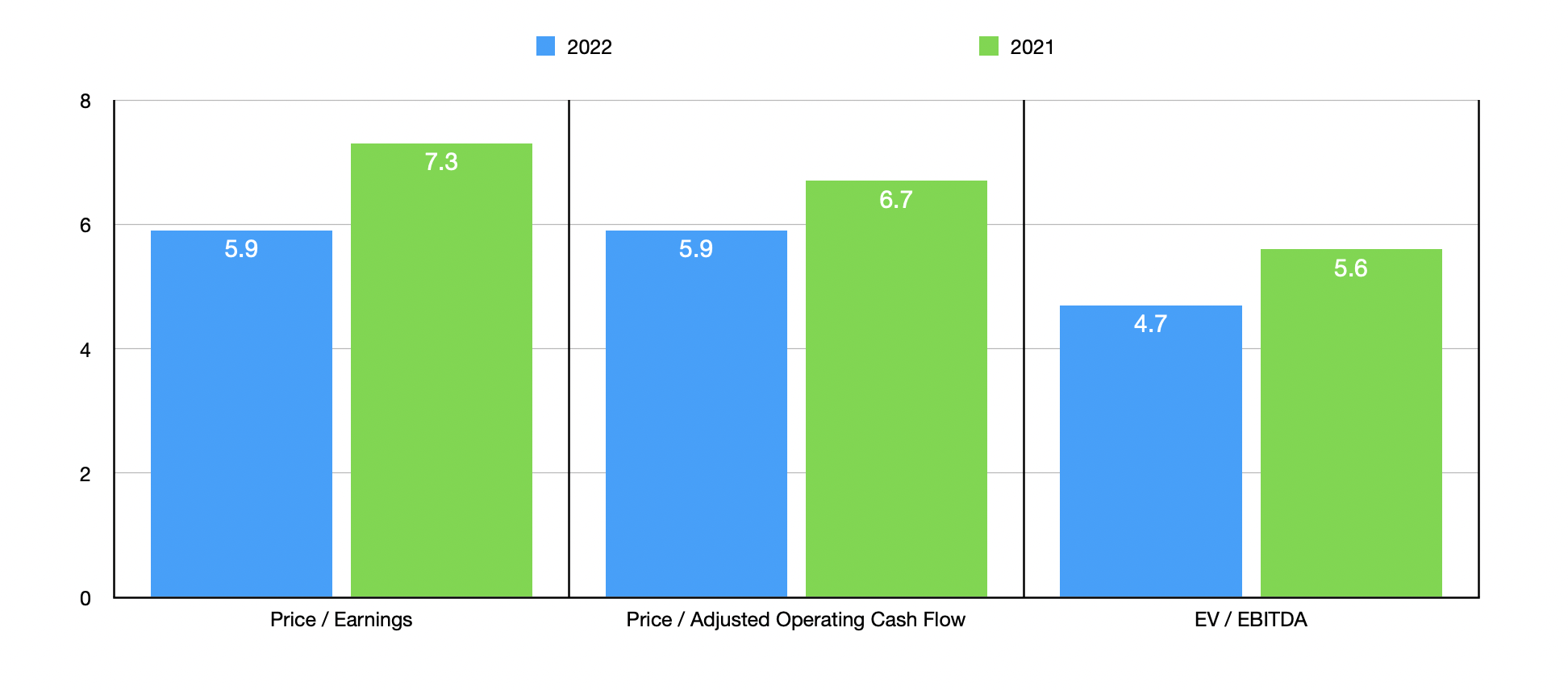

Management has not provided any real guidance when it comes to 2022 in its entirety. But if we annualize results experienced so far, we should anticipate net income of $1.47 billion, adjusted operating cash flow of $1.46 billion, and EBITDA of $2.19 billion. Based on these figures, the company is trading at a forward price to earnings multiple of 5.9, a forward price to adjusted operating cash flow multiple of 5.9, and a forward EV to EBITDA multiple of 4.7. As you can see in the chart above, the firm does look cheaper using the 2022 estimates than if we were to use the data from 2021. But not much cheaper. As part of my analysis, I also compared the company to five other automotive retailers. On a price-to-earnings basis, these companies ranged from a low of 4.6 to a high of 5.4. Because of this, it came in as the most expensive of its group. Using the price to operating cash flow approach, the range was from 3 to 24.4, with four of the five companies cheaper than our target. The only lens through which the company looks cheap compared to its peers is the EV to EBITDA multiple, with its peers trading between 4.5 and 6. In this scenario, only one of the companies is cheaper while another is tied with it.

| Company | Price / Earnings | Price / Operating Cash Flow | EV / EBITDA |

| Penske Automotive Group | 5.9 | 5.9 | 4.7 |

| AutoNation (AN) | 4.6 | 4.5 | 4.5 |

| Lithia Motors (LAD) | 5.2 | 24.4 | 6.0 |

| Sonic Automotive (SAH) | 5.4 | 3.0 | 6.0 |

| Asbury Automotive Group (ABG) | 5.4 | 4.9 | 5.9 |

| Group 1 Automotive (GPI) | 4.6 | 4.6 | 4.7 |

Takeaway

Based on the data provided, I must say that I continue to be impressed by the fundamental data and share price performance achieved by Penske Automotive Group. The company is a solid operator and its market, and I suspect that the long-term trajectory of the business will be just fine. We are seeing some signs of weakness right now and I suspect that picture will worsen before it gets better. For investors who don’t like volatility at all, now might be a good time to consider looking elsewhere for opportunities. But given how cheap shares are and the high probability that fundamentals will eventually revert back to healthy levels again after the storm has passed, I believe that a soft ‘buy’ rating is still appropriate at this time.

Be the first to comment