rvimages/iStock via Getty Images

Investment Thesis

Peloton (NASDAQ:PTON) is about to report its fiscal Q2 2023 results next Wednesday, premarket.

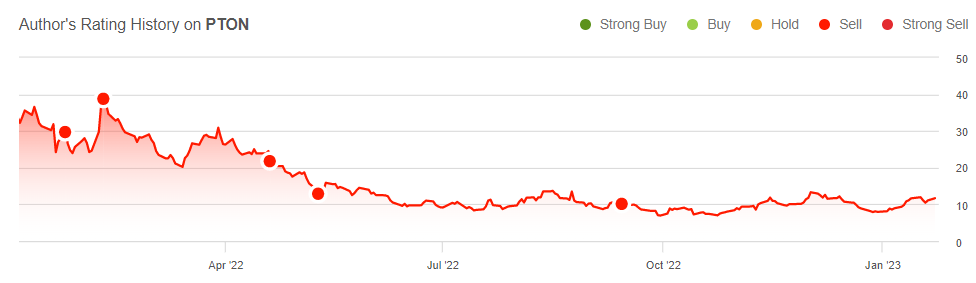

Let’s face it, an investment in Peloton has been a complete failure. What’s more, I’ve been adamantly recommending that people sell this stock for a year, so I know Peloton has been a disaster.

Author’s rating on PTON

But here’s the problem:

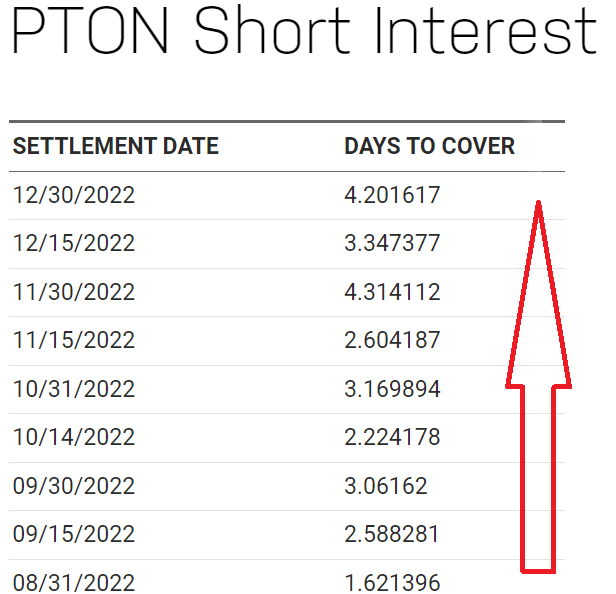

PTON days to cover short

I contend that this short position has been excessively crowded as Peloton prepares to announce its fiscal Q2 2023 earnings because everyone is unambiguously bearish on this name.

Consequently, I’m actually raising my sell recommendation to a hold. Here’s why.

Telling Me Something I Didn’t Know

Let’s see if any of these ring a bell.

- Peloton was a covid winner.

- Peloton’s business model is broken.

- Everyone that wanted a Peloton already has a Peloton; sometimes even two.

- Peloton’s balance sheet holds more than $600 million of net debt.

In fact, this last item is genuinely serious.

According to Peloton’s debt agreement, its $750 million term loan will mature in November 2025 rather than November 2027 if the company still owes the $200 million convertible senior notes by that time.

Simply put, even if we disregard the ultimate question of whether or not Peloton’s business will ever be viable enough to become a solid free cash flow generating business, there’s a substantial likelihood that its senior notes get converted to equity in 2 years, creating yet another overhang and potential shareholder dilution in two years’ time.

I get it! An investment in Peloton has not worked out.

Peloton’s Vision To Get Us Excited

Peloton’s Chief Content Officer Jennifer Cotter and her team are charged with overseeing streaming content.

With everything arguably failing for Peloton, Cotter and her team are striving to figure out new ways to drive engagement and resonate with its members.

Rather than going for the ”usual” suspects, Peloton is trying a new strategy with different types of instructors.

And I’ll be upfront and admit that I have no idea if any of Peloton’s strategies will ultimately work. My argument here is that neither does anyone else.

Accordingly, a few unexpected happy surprises and fireworks can occur when a stock becomes heavily shorted.

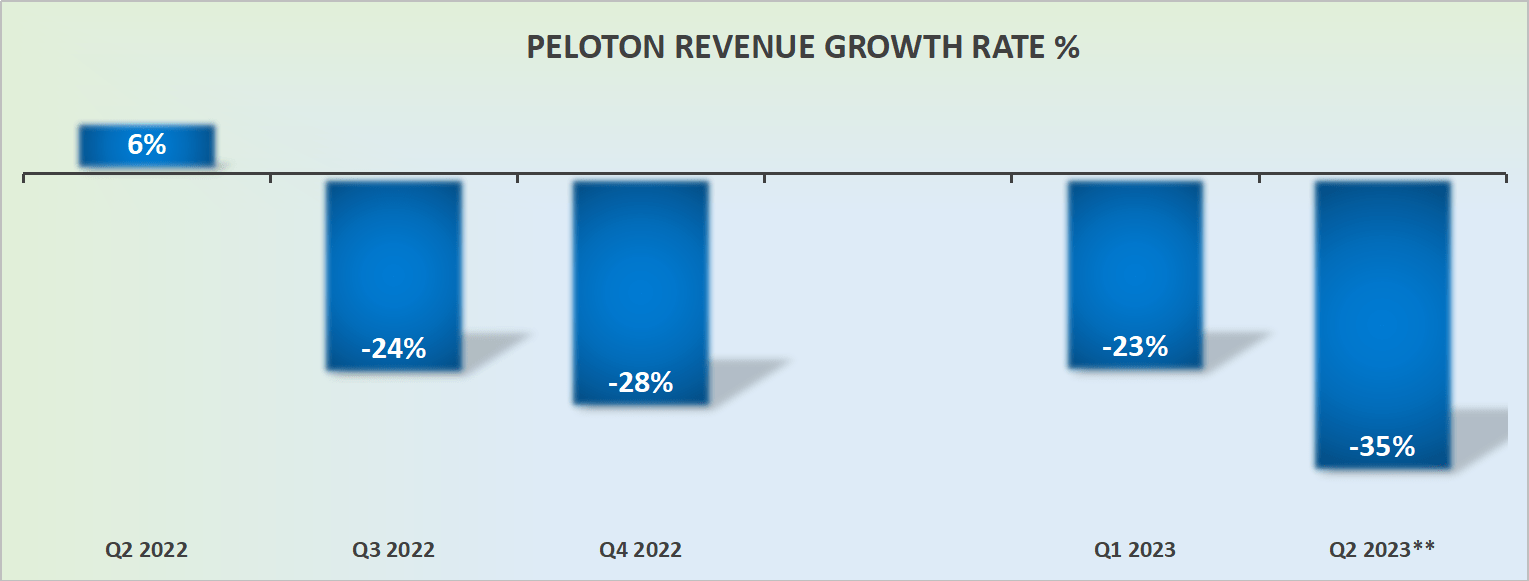

Revenue Growth Rate Comparables Will Get Easier

PTON revenue growth rates

Next, we know that Peloton’s fiscal Q3 2023 will leave a lot to be desired. But we also know that with each progressing quarter after fiscal Q2 2023, the y/y comparables get a lot easier.

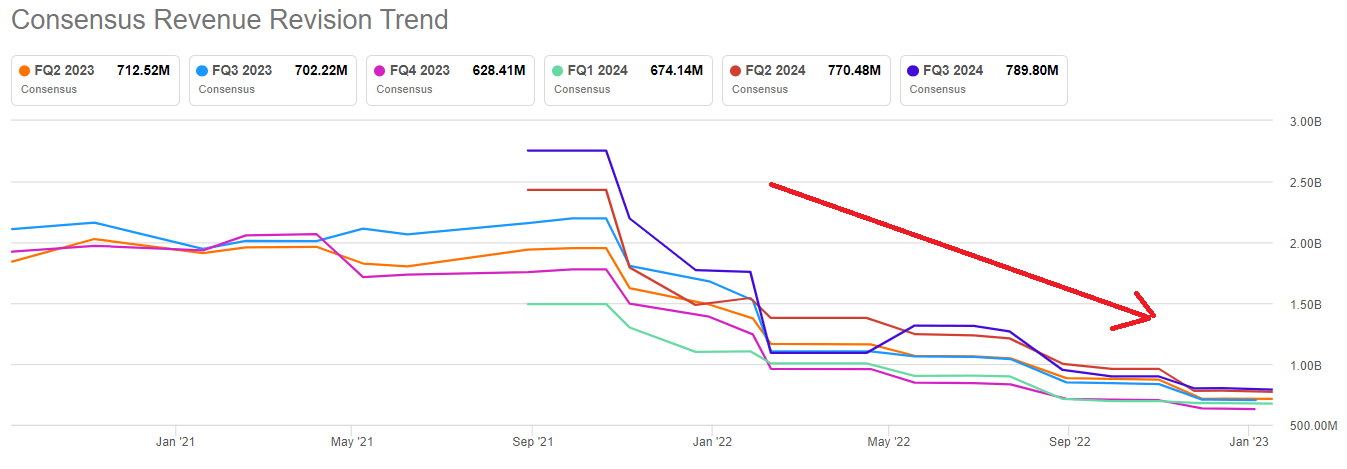

Indeed, I argue that analysts following this stock are also too bearish at the moment.

PTON analysts’ revenue estimates

What you see above is an unambiguous negative view on Peloton’s revenue growth rates.

Clearly, we get it! Peloton shouldn’t be invested in as a long-term buy-and-hold opportunity. But this doesn’t mean that it’s an outright short at this level either.

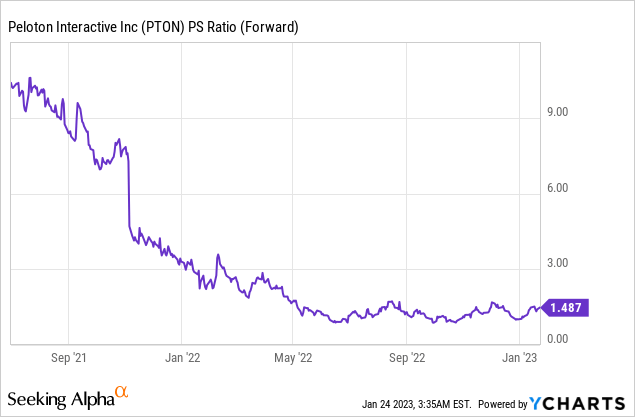

PTON Stock Valuation — Clearly Not A Bubble Stock

As you can see above, Peloton’s multiple to sales has compressed significantly in the past 12 months. After the lockdown period and after all the enthusiasm for its brand evaporated, Peloton’s multiple continued to compress with time.

Put simply, I argue that few investors have anything but negative views left on this stock.

Investors are giving no credence to the idea that some members may not churn out quite as aggressively as the Street expects. After all, the way that Peloton attempts to make money is not through its bike sales, right? It’s through its subscription service.

The Bottom Line

There’s so much to dislike about an investment in Peloton. Not only is its balance sheet in a perilous state, but management appears eager to sell out of their holdings at seemly any price.

Finwiz, insider sales

As you can see in the table above, it’s not just one person, but various people in the C-suite who are clearly not putting their money where their mouths are, but in fact, seemingly looking to diversify away from Peloton.

In sum, I get all the negatives facing the stock. But since I get it and you get it, that’s why I believe it’s time to remove my sell recommendation on this stock, because this short is now too crowded.

Be the first to comment