SDI Productions

Education group Pearson (NYSE:PSO) has had a good run lately in the stock market.

I last covered the company in April with my bearish piece Pearson: Not Unlocking Much Value On Its Own. Since then, the shares have increased in value by 21%. However, I continue to see the shares as overvalued relative to the company’s earnings generation potential. Accordingly, I maintain my “sell” rating on the name.

Business Performance is Decent

While not stellar, recent business performance has been decent and arguably good.

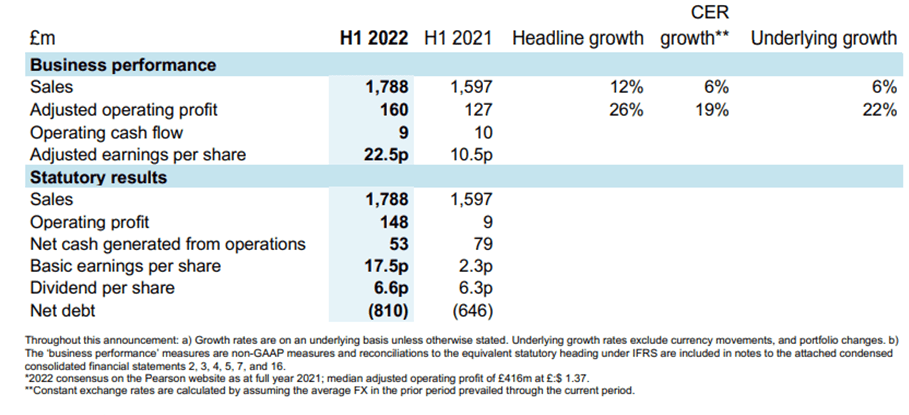

At the interim stage, sales were up 12% and earnings per share soared albeit from a low base last year.

company announcement

The company said after its third quarter that it expected to deliver sales and adjusted operating profit consensus expectations for the full year, with sales growth in the first nine months of 7% compared to the prior year period.

This is positive momentum for the business. But I do not think the results are great. I think some of the strong performance in the assessment and qualifications and English language learning divisions are basically clearing a post-Covid backlog, so expect sales growth in those divisions to slow sharply over the next couple of years. It is also worth noting that Pearson has struggled to convert sales into operating profits consistently, as shown in the first half results.

company announcement

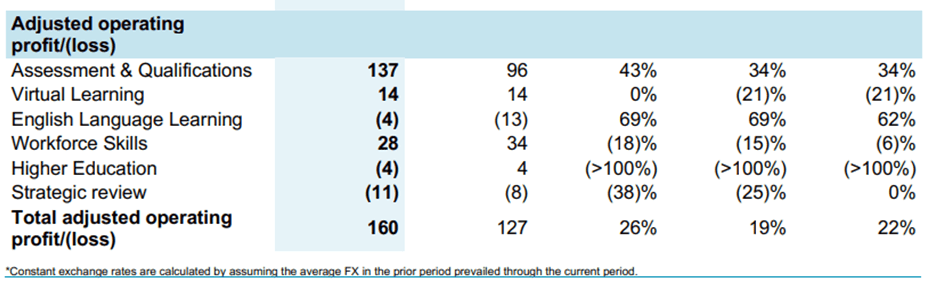

Has the company’s strategic pivot towards education in recent years worked? I think there is not yet sufficient evidence to say that it has. For example, virtual learning in the first half grew by double digits in percentage terms (a change in reporting segments means one can make no direct comparison to the prior year, though I think this growth was from a strong base) but adjusted operating profit was flat and the adjusted operating profit margin was a meagre 3.6%. Maybe a shift towards more virtual learning in coming years can help boost the top line, while lower costs can improve the bottom line. The company has identified cost savings of at least £100m for this year, on top of the efficiencies the company expects from its prior reorganisation of divisions.

However, none of this is yet compelling in my view. The strategy makes sense to me, but its long-term impact remains unproven and it is not clear how financially attractive the pivot to education will turn out to be. It has not yet delivered high growth, so I see it as premature for shares to be valued on the expectation that it will do.

Valuation Looks Stretched

Currently Pearson has a market cap of £6.6bn. Net debt at the end of June was £810m (up 231% in a year), meaning the enterprise value is £7.4bn.

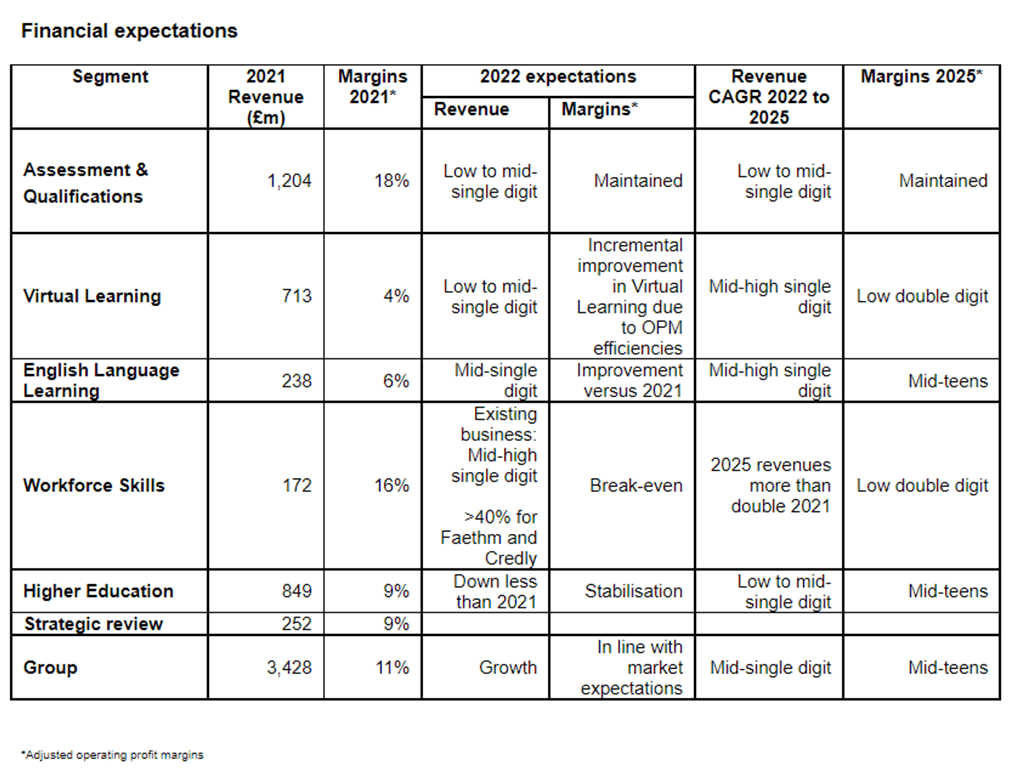

That looks high to me. Last year’s profits after tax were £160m, meaning the price to earnings ratio stands at 42. For the current year, the company outlook is for adjusted operating profit of £416m. But that is broadly in line with last year, when although the reported profit was £160m, the adjusted operating profit was £385m. So, if excluding adjustments and the operating profit level and focussing instead on basic reported earnings after tax, which I see as a more relevant measure, the prospective P/E ratio is likely in the mid-twenties to mid-thirties depending on the size of the adjustments. In recent history, Pearson has had a history of frequent substantial adjustments.

|

2015 |

2016 |

2017 |

2018 |

2019 |

2020 |

2021 |

|

|

Adjusted operating profit (£m) |

723 |

635 |

576 |

546 |

581 |

313 |

385 |

|

Profit (£m) |

823 |

-2335 |

408 |

590 |

266 |

310 |

160 |

|

profit as a % of adjusted operating profit |

114% |

-368% |

71% |

108% |

46% |

99% |

42% |

Table compiled and calculated by author using data from company annual reports

That P/E ratio looks rich to me. After all, the company’s track record is not brilliantly consistently and even its target foresees mid single digit compound annual revenue growth in the period 2022-25. Given a pandemic backlog, high inflation and years of strategic refocussing at the company, that does strike me as very exciting or worthy of a valuation premium which I think a P/E ratio like the current prospective one suggests.

company annual report 2021

Accordingly, I continue to maintain my bearish rating on Pearson. I am not bearish on the company overall, though continue to find it fairly unexciting: I simply think it is overvalued for what it is and the value creation opportunities it offers me as an investor.

Be the first to comment