Kyryl Gorlov/iStock via Getty Images

Investment Thesis

Peabody Energy Corporation’s (NYSE:BTU) business is very roughly 50% thermal coal and 50% met coal.

Given that the natural gas market has recently shown a considerable weakness, it’s probably good news that only half the business is exposed to thermal coal.

However, the real bull case isn’t actually focused on thermal coal or met coal prospects. The bull case is one of return of capital.

Expectations and Reality

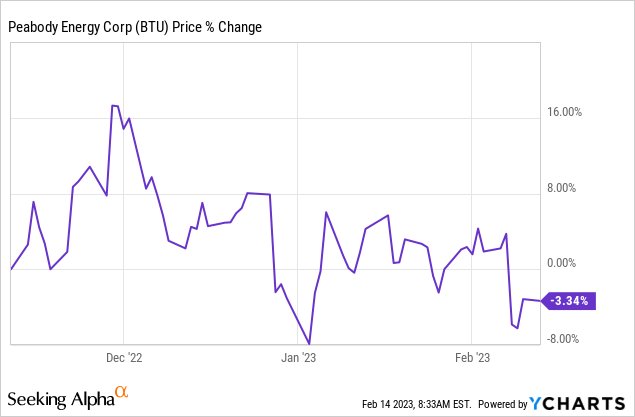

Let’s be honest. An investment in Peabody has been relatively poor in the past 3 months.

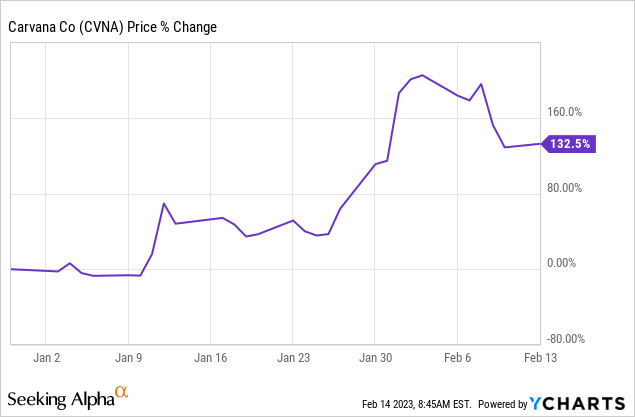

While many investors are talking about “going to the moon” in stocks that are sometimes described as “junkier stocks” or “high beta,” and even sometimes stocks that appear “lucky” enough to be on the verge of bankruptcy are going up very strongly, meanwhile Peabody’s share price hasn’t really gone anywhere.

For example, here I highlight Carvana Co. (CVNA). But I am confident that you know others, too.

That being said, let’s now turn to discussing expectations. Because after all, close to 0% return in 3 months isn’t really much to complain about. Not when we come to terms with the capital return problem.

Capital Returns “Problem”

As I’ve argued for months, sooner or later Peabody Energy Corporation will be in a position to retire its senior secured notes.

And once that happens, there are a few technical hurdles in the way, before Peabody will be able to increase its capital return to shareholders.

As a reminder, part of the agreement that Peabody had when it emerged from bankruptcy was that Peabody would not return capital to shareholders until the debt on its balance sheet was taken care of. And that has now happened this quarter.

What Peabody is left with is a net cash position of approximately $1 billion. Put another way, more than 25% of Peabody’s balance sheet is made up of cash.

Consequently, I believe that at some point before next quarter, Peabody will put in place the necessary measures to start returning substantial capital to shareholders.

Hence, the capital return “problem.” Will Peabody return capital to investors as a special dividend? Or via buybacks? Or a combination of the two? Alas, this is a good problem to have.

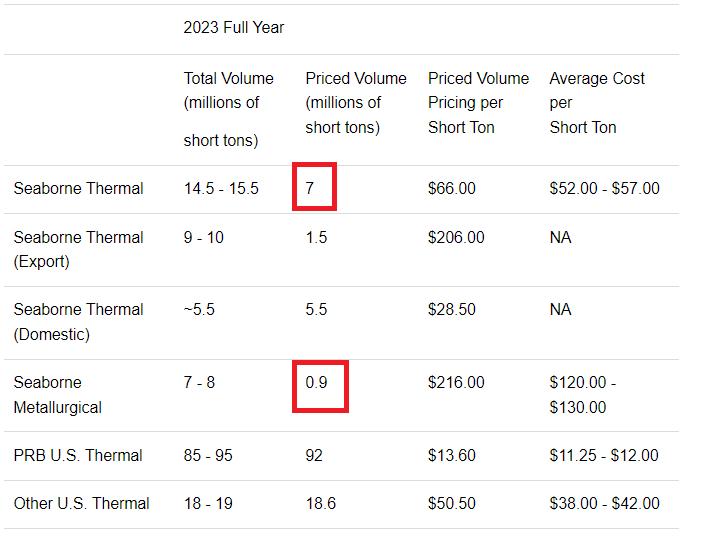

2023 Guidance Discussed

Peabody 2023 guidance

As the table above shows, Peabody Energy Corporation has already locked in approximately half of its thermal coal production.

Given that natural gas competes with thermal coal as an energy source, when taken together with natural gas having shown significant weakness in the few weeks, I believe this hedging will actually be beneficial to shareholders.

According to my own estimates, I believe that Peabody will probably end up reporting at least $1 billion of free cash flow in 2023. Essentially in line with 2022.

How to Think About This Sunsetting Industry

I will not be drawn into either the bull or the bear camp on coal. There are fierce and vicious proponents on either side, including those that believe that we should abandon the use of thermal coal immediately, without giving much (or any) consideration to scalable and cost-effective alternatives.

While on the other side, there are some bulls that believe that coal is a growth industry.

I believe I’m somewhere in the middle. That being said, despite being in the middle of the argument, that doesn’t detract from the fact that the need for coal is very much alive and well. And these strong free cash flows are yet another reminder that beyond the narratives, there’s the tangible free cash flow.

The Bottom Line

As we stand right now, Peabody Energy Corporation’s market cap is less than $4 billion. The business is likely to report close to $1 billion of free cash flow next year, with a substantial portion of its production already hedged out.

Paying around 4x this year’s free cash flow for a business like Peabody Energy Corporation that is committed itself to return meaningful cash flows back to its shareholders, I believe, is a compelling investment.

Be the first to comment