Drew Angerer

Investment Thesis

Paramount Global (NASDAQ:PARA) looks cheap on the surface but there are problems under the hood. They have declining profitability and a monstrous debt pile. The streaming business model is highly competitive and has a low amount of potential upside. We believe Paramount is a value trap that investors should avoid for now.

Declining Profitability

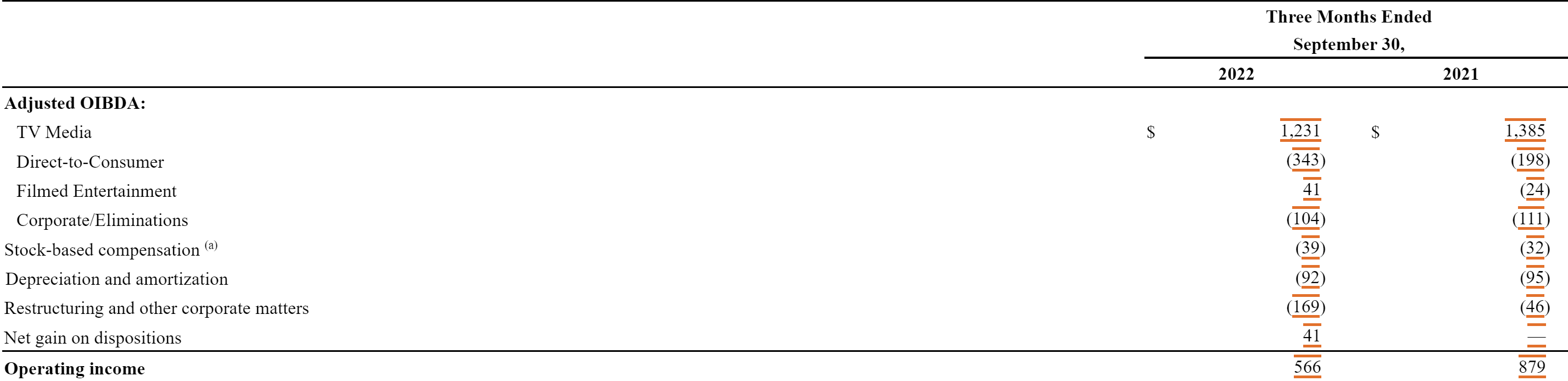

In their most recent quarter Paramount reported a decline in operating income of 36%. Their most lucrative operating segment of “TV Media” saw a modest decline in adjusted OIBDA of 11.12%, but even a small decline in this segment is a problem considering their DTC segment losses ballooned by 73.23% in the quarter.

Profitability of Operating Segments (Paramount Q3 Earnings Report)

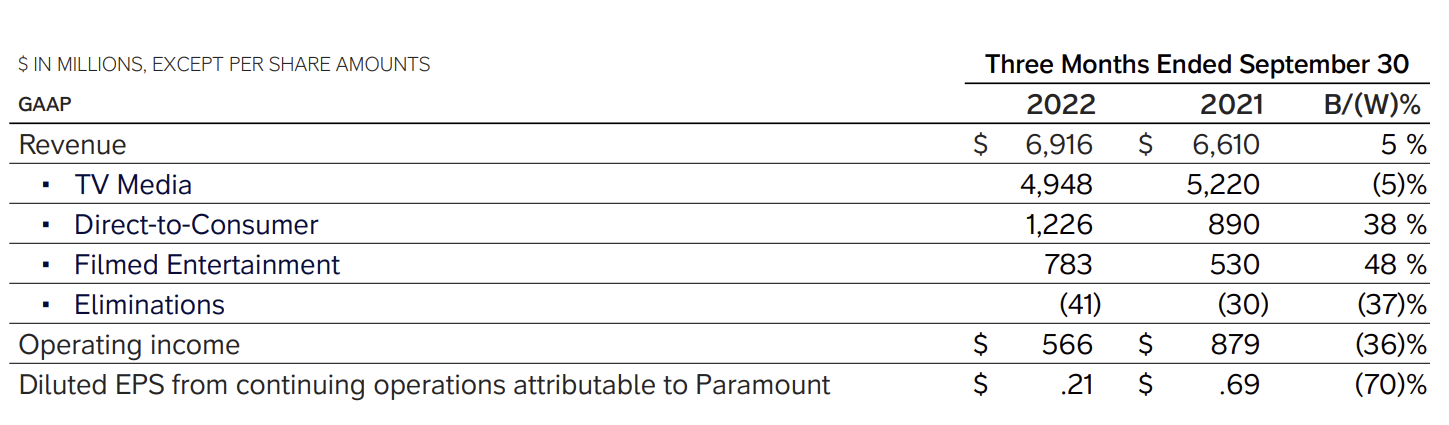

Paramount was able to grow their overall revenue by 5% year over year and their DTC and filmed entertainment segments grew revenue at a rapid rate. The 5% decline in TV media revenue is concerning, especially because it’s currently the profit center of the business.

Revenue Growth Rates by Segment (Paramount Q3 Earnings Release)

Paramount states in their earnings release that:

Paramount+ Added 4.6M Subscribers and Grew Revenue 95% and that Total Global Direct-to-Consumer Subscribers Rose to Nearly 67M

This subscriber growth is a good sign, but the company is paying dearly for that growth.

Paramount is focused on growing their DTC business and they are not afraid of losing money to do so. Their TV Media segment is likely saturated and diversifying their business seems to make sense on paper. The issue is that their business as a whole is challenged, and the reward for growing their DTC segment isn’t even that high. It may be better to accept being a company that is in the late stage of their corporate lifecycle and focus on paying down debt and maximizing shareholder payouts rather than burning money to chase growth.

Challenged Business Model

Let’s take a look at Paramount’s three main business segments:

TV Media

According to Paramount’s 10-Q their media business segment “consists of our domestic and international broadcast networks, including the CBS Television Network, Network 10, Channel 5, Telefe, and Chilevisión; our premium and basic cable networks, including Showtime, BET, Nickelodeon, MTV, Comedy Central, Paramount Network, Smithsonian Channel, international extensions of these brands, and CBS Sports Network; our television production operations, including CBS Studios, Paramount Television Studios and CBS Media Ventures, which primarily produces or distributes first-run syndicated programming; and our owned broadcast television stations, CBS Stations.”

This business segment is comprised of news and entertainment TV networks, as well as TV production studios. They make money from advertising deals, affiliate and subscription revenue, and licensing deals. This is a mature market that doesn’t have much room for growth. At the moment, Paramount is actually seeing a revenue and operating income decline in this segment. Without much of a pathway for growth Paramount has two options. Continue to operate a stagnant business and focus on paying down debt and increasing payouts to shareholders, or chase growth. It appears that for now Paramount has chosen the latter.

Direct-to-Consumer

Paramount states in their 10-Q that their DTC business segment “consists of our portfolio of pay, free and premium global direct-to-consumer streaming services (“DTC services”), including Paramount+, Pluto TV, Showtime Networks’ premium subscription streaming service (Showtime OTT), BET+ and Noggin.”

The company makes money from this segment when people spend money to become subscribers, usually for a monthly rate. They also have ad-supported tiers and make money when advertisers spend money to place ads on their content.

This is a great way to utilize assets that they have already paid for, and many other companies in the industry are doing the same thing. The issue is that they are investing heavily into growing their DTC business, and many other companies in the industry are also investing heavily into their DTC businesses.

Streaming has turned out to be an incredibly competitive business, as well as a capital intensive one. Companies are spending large amounts on content and marketing to attract and retain subscribers, but the payoff has so far been mediocre at best. The most successful companies in DTC streaming are probably Netflix (NFLX) and Disney (DIS).

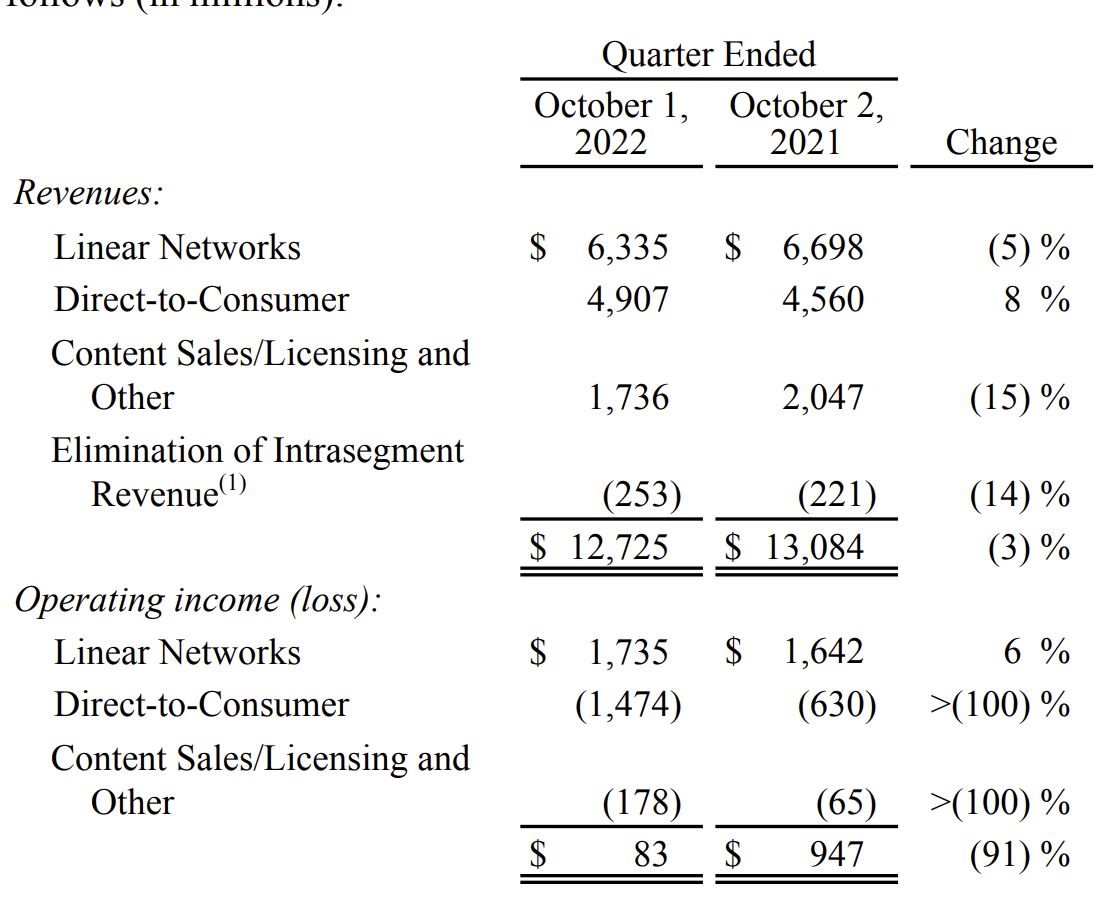

Disney has what some would consider the leading content library of any traditional media company. If any company would be able to make streaming profitable it would be them. Despite their unassailable content advantage, in their most recent quarter Disney’s DTC segment reported an operating loss of $1.474 billion. This is compared to a loss of $630 million during the same quarter of the prior year. The operating losses in their DTC division almost wipe out their operating profits in their linear networks division. A similar scenario could play out at Paramount, though unlikely to be as extreme.

Disney Media and Entertainment Segment Results (Disney’s Fourth Quarter and Full Year Earnings For Fiscal 2022)

Netflix is the dominant player in streaming but until recently has struggled to produce positive operating cash flow. They have $13.88 billion in debt and not much to show for it except for market share that they could lose to their new competitors in streaming. To their credit, Netflix is the clear leader in the streaming space. Even though they are financially successful now, Netflix had significant struggles activating the operating leverage in their business model. That doesn’t bode well for Paramount’s streaming endeavors or the endeavors of any legacy media company trying to enter the streaming market against heavily entrenched competitors.

The core issue is that many streamers pay too much for content. The amount they pay for a piece of content often doesn’t result in creating value for the customer that is greater than what the company paid for the content. The theory is that while one piece of content may not generate the value paid for it, the library as a whole will benefit from economies of scale. In practice it doesn’t seem to work this way for the smaller streamers and even most of the big ones, and they continue to incinerate increasing amounts of money for an ever diminishing reward as market share and customer dollars become more difficult to come by.

In summary: Streaming has turned into a highly capital intensive business with a large number of companies competing for a small amount of potential reward. The content often ends up being not as valuable as the price paid for it. The streaming segments of most legacy media companies struggle to make a profit and are quickly becoming money furnaces.

Filmed Entertainment

Their filmed entertainment segment consists of their film production studios. These film studios are Paramount Pictures, Paramount Players, Paramount Animation, Nickelodeon Studio and Miramax.

This segment did well in the most recent quarter compared to the year ago period. One potential downside is that this segment relies on theatrical release cycles and the willingness of the consumer to watch movies. As a result, there can be significant fluctuations in this segment. This is especially true if Paramount has no blockbuster releases.

Massive Debt Pile

Paramount has a massive debt pile of $15.638 billion. This resulted in an interest expense of $231 million in the most recent quarter alone. This interest expense is very high relative to their $566 million in operating income, and the trend is worsening. This quarter’s interest expense was 40.81% of operating income while in the year ago period it was 27.64%.

To put their debt problem further into context let’s consider the Q3 net income attributable to Paramount of $231 million. On an annualized basis that’s $924 million. It would take Paramount 16.92 years’ worth of net income to pay off their debt as things currently stand. And that’s before taking into account that their net margins are likely to contract even further as the DTC business continues to hemorrhage money.

This debt pile adds tremendous pressure to their financial situation and reduces the flexibility of the business. We could be entering a new era for interest rates and they could remain higher for longer than people expect. If Paramount needs to refinance their debt at a higher interest rate it would be a disaster for the company.

Over the long-term the cash flow available to equity holders will be severely cut into by interest and principal payments on the debt. The valuation looks cheap on the surface, but the market is taking into consideration the future cash flow commitments this company is going to be locked into and that the free cash flow available to equity holders is actually quite low going forward.

Valuation

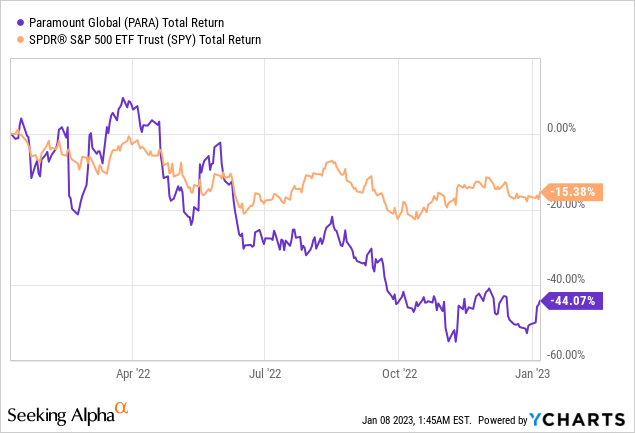

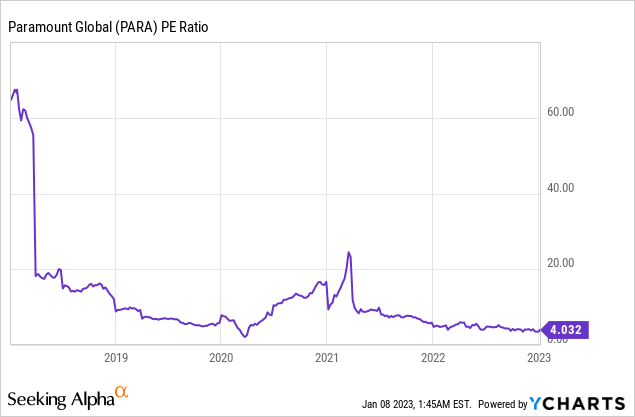

Over the past year Paramount’s stock has gotten crushed, although not unjustly. Investors are not liking the margin compression that is going on and the looming debt burden.

On a PE basis Paramount looks tantalizingly cheap but there is more to the valuation story than meets the eye. Paramount appears to be a classic case of a value trap.

The issue is their future earnings aren’t entirely available to the equity holders. Much of the earnings going forward will need to be used to pay off the debt. As mentioned earlier, it would take 16.92 years of current net income run rate to pay off their debt. That’s 16.92 years of earnings that don’t go to shareholders. Investors may shrug this off and say that the debt isn’t due for many years or that they will just refinance it, but eventually they will need to pay off the principal.

If an investment is the present value of future cash flows then the value of that investment is reduced by any large future payments that are owed to bondholders. A company can put this off for some time, but not forever.

I wouldn’t touch Paramount anywhere close to these levels because of their high debt load and challenged business model/DTC money furnace. If Paramount’s streaming business becomes profitable and they begin to expand their margins and aggressively pay down debt I’d consider taking another look. For now this appears to be a value trap.

Risks

In this case a risk to our thesis would be Paramount performing better than expected. Here are some ways they could do that.

Paramount could end up being highly successful in their DTC endeavors and start earning operating profit from that segment.

Their margins could improve as they achieve greater operating leverage.

Their TV Media business segment could return to growth.

They could be able to refinance their debt at an even lower rate than they are paying now.

We don’t have anything against Paramount and would like to be proven wrong for the sake of investors and consumers alike. We just don’t think the risk/reward looks favorable as it currently stands.

Key Takeaway

Paramount had a rough year in 2022, and the stock appears to be cheap. We think the stock is a value trap and that investors should say away until the company can clean up some of their operating metrics and the quality of their balance sheet improves. We would be willing to take another look once the risk/reward becomes more attractive.

Be the first to comment