There have been numerous articles on Palantir (NYSE:PLTR) and YouTube reviews of this stock and how Q3 earnings was a disappointment. My goal for this article is to provide a different perspective on their earnings but more importantly educate investors and critics on how they should be evaluating the company. Palantir is approaching software-as-a-service (SAAS) sales differently than most in the industry today. They understand the importance of proving themselves and delivering immediate value upon the initial customer acquisition. They understand to be the core operating system for both their government and commercial customers, then large positive value and disruption must be realized at the highest levels.

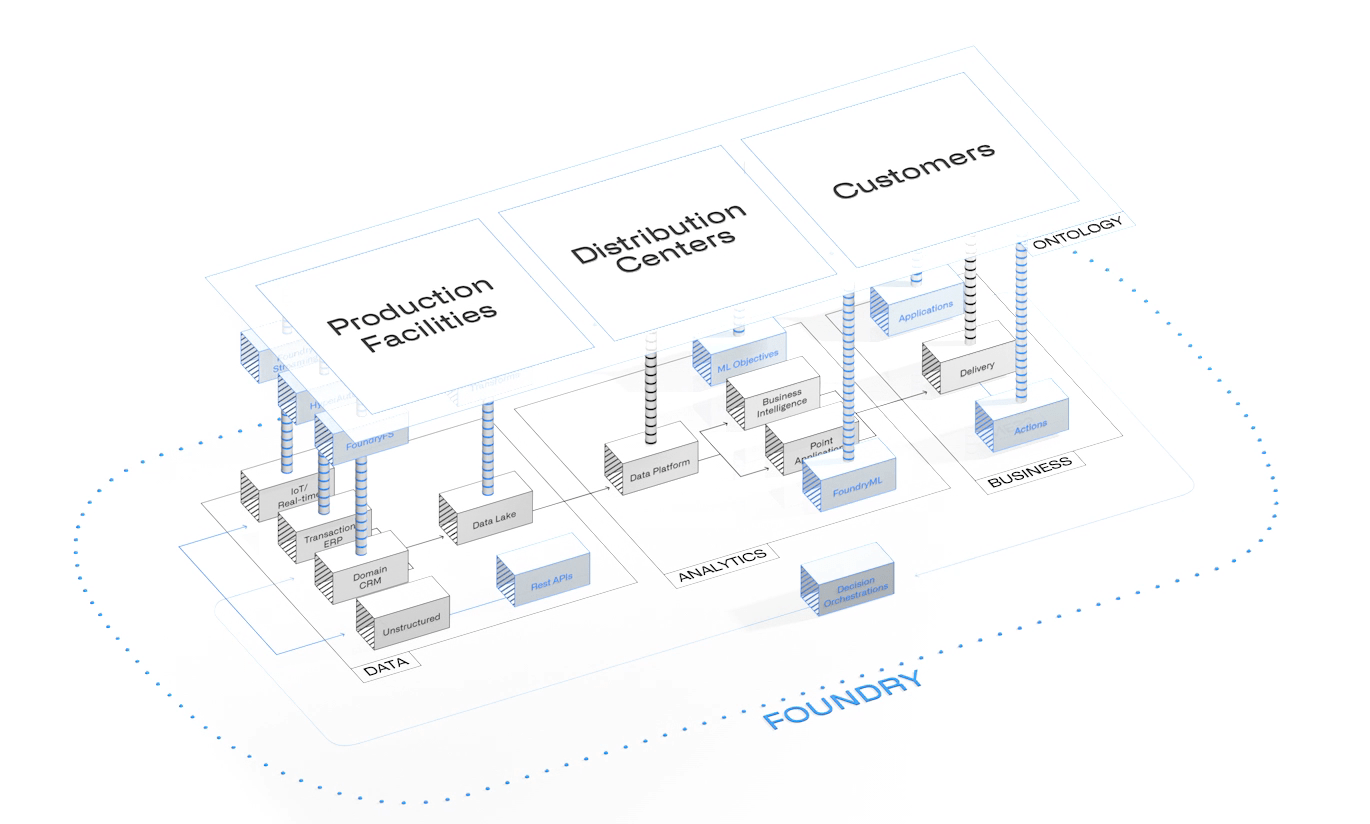

Foundry the Core Operating System for Business (Palantir Foundry Website)

Palantir must get to the decision makers and C-Level executives to win deals not just because the cost of the platform can be expansive, but because using a software platform like this is a paradigm shift in how the business will operate. Now this paradigm shift is a positive one, but it can be a culture shock because enterprise software is typically only used by IT and developers, and is not very functional or easy to use to create new value for the rest of the business. Because of this, the sales motion is not an extremely fast one or even the initial first project completion of using the Palantir Foundry solution.

However, once real dollars are saved, adoption spreads within the company, kind of like a virus, but in a good way. Other departments and business units want to be able to have visibility to all the company data that they are supposed to securely see and be able to understand the data relationships that will help them make better decisions.

What Did Institutions, Shareholders, and Critics Not Like About Q3 Earnings and Previous GTM Strategy?

Many institutions, shareholders, and critics were underwhelmed with the 22% revenue growth YoY results by Palantir. They were also disappointed by the EPS miss by -$.01. The company did beat revenue expectations by $2.77M to deliver $478M in Q3. Investors were also not pleased with the decrease from 30% operating margins a year ago to 17% this past quarter. The overall commercial growth decreased substantially to 17% YoY globally, due to additional headcount in sales being added and macro headwinds in Europe for their customer base. However, the U.S. commercial growth was a strong 53% YoY, but some would argue that is still not good since they had 120% just a quarter ago. Stock based compensation did decrease 24% YoY, making shareholders thankful, but it was still $140.2M and Palantir was still not profitable in Q3.

Many institutions would not invest due to the stock dilution, not being profitable, and growing above the 30% YoY commitments previously made. Feedback on the GTM strategy that Palantir was using was rejected by critics because originally Palantir didn’t have a lot of sales employees and the company did not advertise what they were capable of in the commercial space effectively. They were doubted originally that they could make meaningful revenues in the commercial arena but they have already disproved that.

So, there it is folks, that is what the market was frustrated with regards to Q3 earnings and Palantir’s flaws in GTM. Is this stock just another high-flyer from 2020 that will continue to stay below its DPO price of $9.50 a share? Or were there indicators and business results in Q3 and 2022 overall that lead us to believe the contrary?

What Should Institutions, Shareholders, and Critics Love About Q3 Earnings and Palantir’s Change in GTM Strategy?

Before looking at Palantir’s Q3 earnings results, you have to make sure you understand Palantir’s business model and goals, in order to appreciate the results and changes the business has made. Palantir as most of you know started out in the government sector 18 years ago and you can read more about its early days in my previous articles, but it now has two commercial products in Palantir Foundry and Apollo.

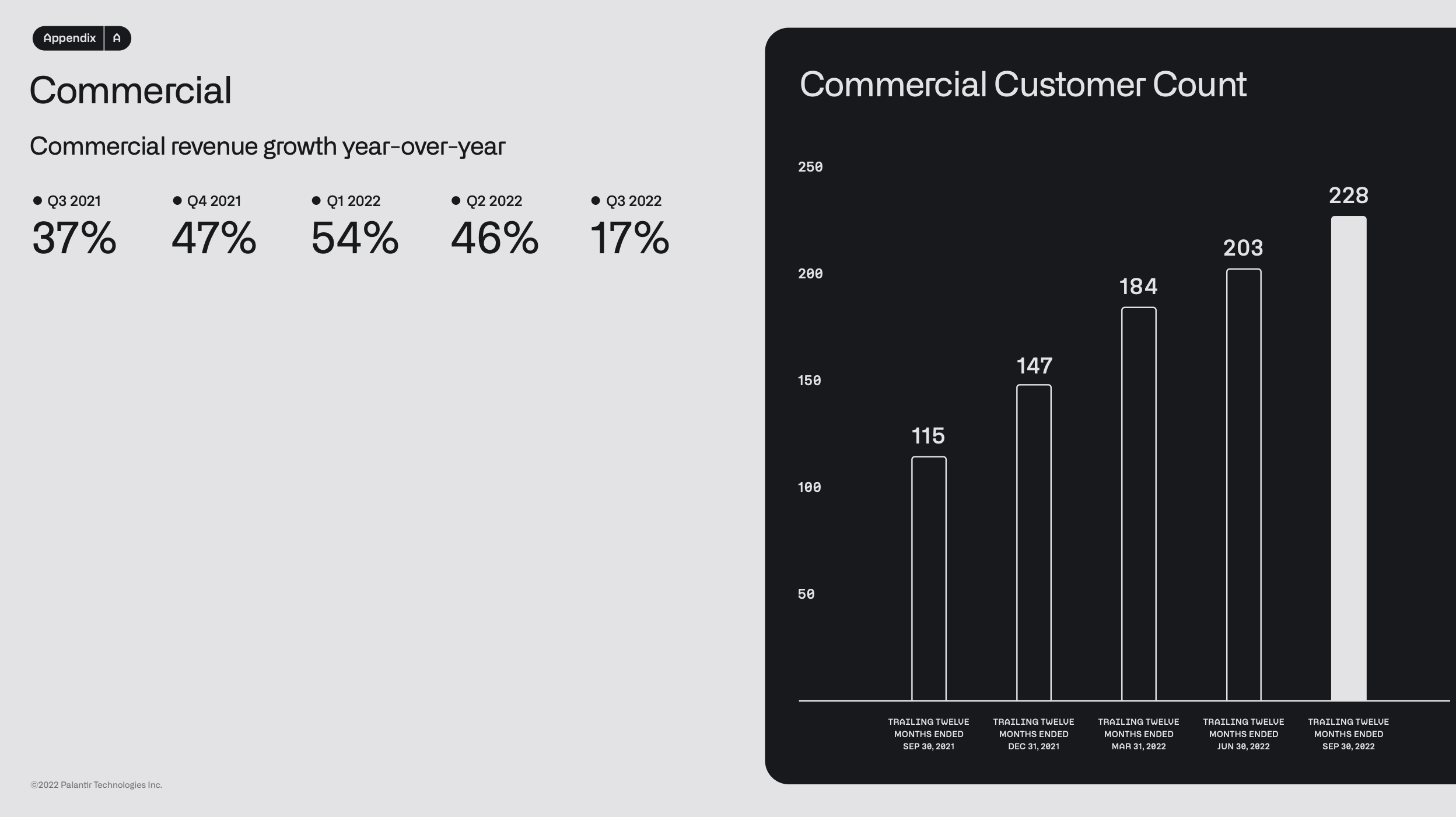

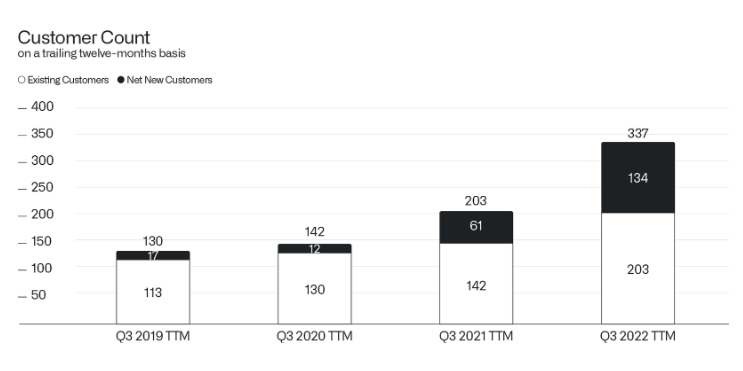

These software products have only been around for about 6 years and have gained much traction with the Fortune 500 and other large commercial organizations. Palantir is growing their customer base significantly, the number of new customers that are purchasing Palantir software has more than doubled in the past year.

Customer Count Growth (CEO Alex Karp Shareholder Letter)

In another section of CEO Alex Karp’s letter to shareholders he explains the landscape of how software is viewed, procured, and adopted is transforming. He also reminds shareholders what Palantir has accomplished with their software and recreating it will be extremely difficult for others, see the specific commentary below.

Where there was once a firm belief that the adoption of tools in isolation was sufficient for success in the long run, there is now a broader understanding that enterprises will only begin to be able to exploit the value of their data when their own offerings and applications are running on top of a broader and integrated platform.

There is a reason why the market is not overrun by competing enterprise software systems for integrating and then transforming data into something of operational value. They are extraordinarily difficult to build.

The lack of widespread development of competing offerings is principally a reflection of the distinct hurdles that must be overcome for a mere data integration platform to mature into a foundational system that can model the world.

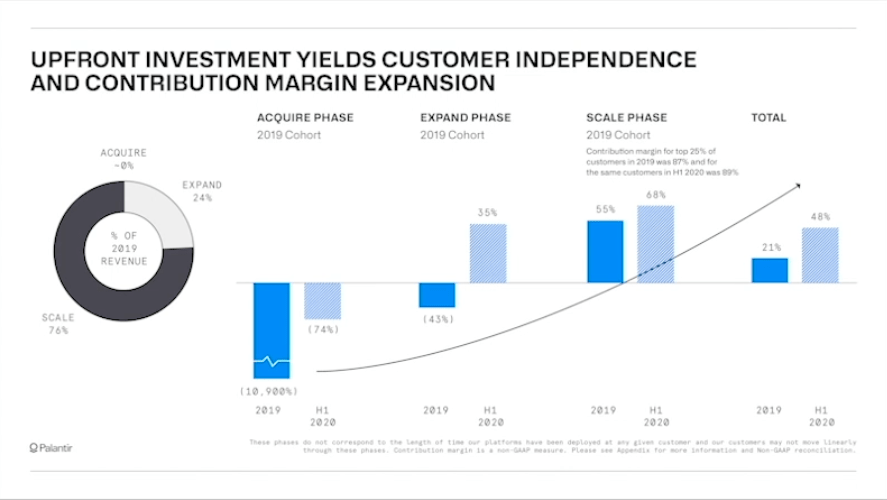

The sales-motion and business model of Palantir Software is primarily focused on identifying critical and complex problems the customer may or may not be aware of. The next step is to show them they can solve these problems by enabling the customer’s data relationships to make better real-time decisions that impact the business for quantifiable savings and production. Palantir achieves this with a three phased approach in their adoption model of the software: acquire, expand, and then the scale phase. Palantir is willing to lose money in the first two parts of the journey with the customer, to ensure true quantifiable returns have been realized by the customer which leads the customer to scale the software platform further throughout the business and sign large expansion contracts.

Explaining the Acquire, Expand, Scale Business Model (2019 Palantir Investor Presentation )

The more projects the customer implements with Foundry the more use cases they identify which leads to more network effects, higher switching costs, and the usage of the platform throughout the company. So, the acquire and expand phase may take some time to complete for the customer, but Palantir helps them identify these challenges and prepare how to utilize the software to build applications to drive to the desired outcomes. It is through phases two and three where CEOs, CFOs, and others are engaged that this platform could be utilized as the backbone foundation operating system for all of the business.

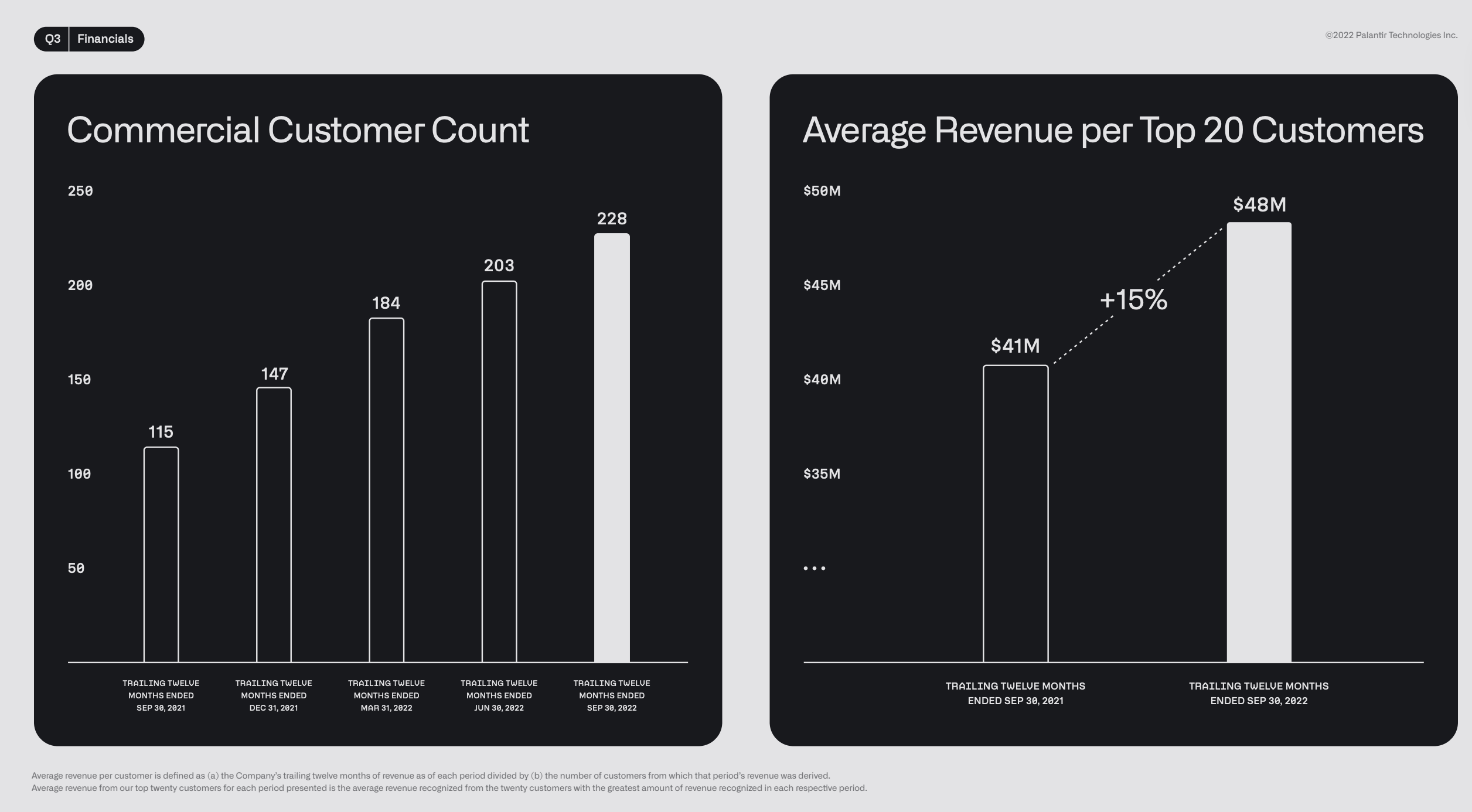

In order to operate in a sales motion like this and be successful, a company has to have an exceptional product that stands on its own along with exceptional talent to help customers think about solving problems differently and integrating this platform into their current set of tools. Palantir’s software products are all that and more, and you may ask how would I know this? Palantir’s Top 20 customers continue to expand each year and spend more and more on the platform, with an average annual spend of $48M a year. Swiss Re has been using Palantir for four years and now has 33% of the entire company actively using Palantir Foundry! Other than email and spreadsheets I cannot think of any other type of application that an entire third of a company is using a software product regardless of role at the company. Not to mention Palantir has had the U.S. Government as a customer for over 18 years, which is not an easy customer to acquire and retain, especially for this long.

Top 20 Customer Growth in Spend (Q3 2022 Palantir Earnings Presentation)

Investing critics first said Palantir was just a government consulting or software company, and their struggle would be getting commercial customers in the enterprise. In a very short two years Palantir has grown their commercial customer count to 228 and closed 273 deals in total in Q3! U.S. commercial revenue in two short years has become 18% of their overall annual revenue.

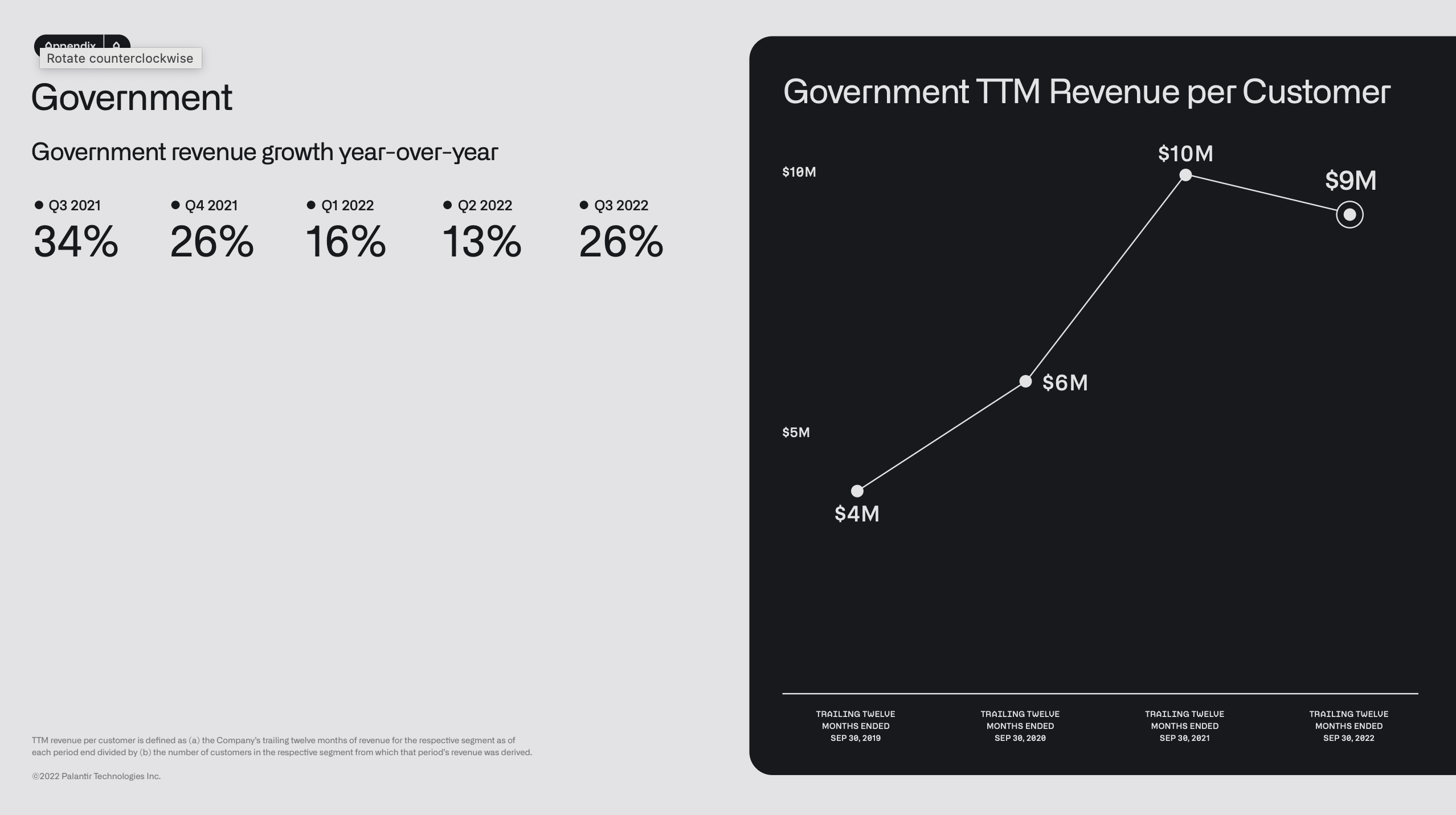

Then the critics said their government business was slowing down and wasn’t even over 20% anymore for the first two quarters in 2022. This was true, however, government business flows in cycles and government budget approvals are key as to when funds can be released for procurement. The numbers for government revenue will always be lumpy but when you average it together it has always been a 30% CAGR for the past several years. This past Q3 the revenue had 26% YoY growth and the average twelve-month trailing revenue per customer was $9M.

Government Average Revenue Spend (Q3 2022 Earnings Presentation)

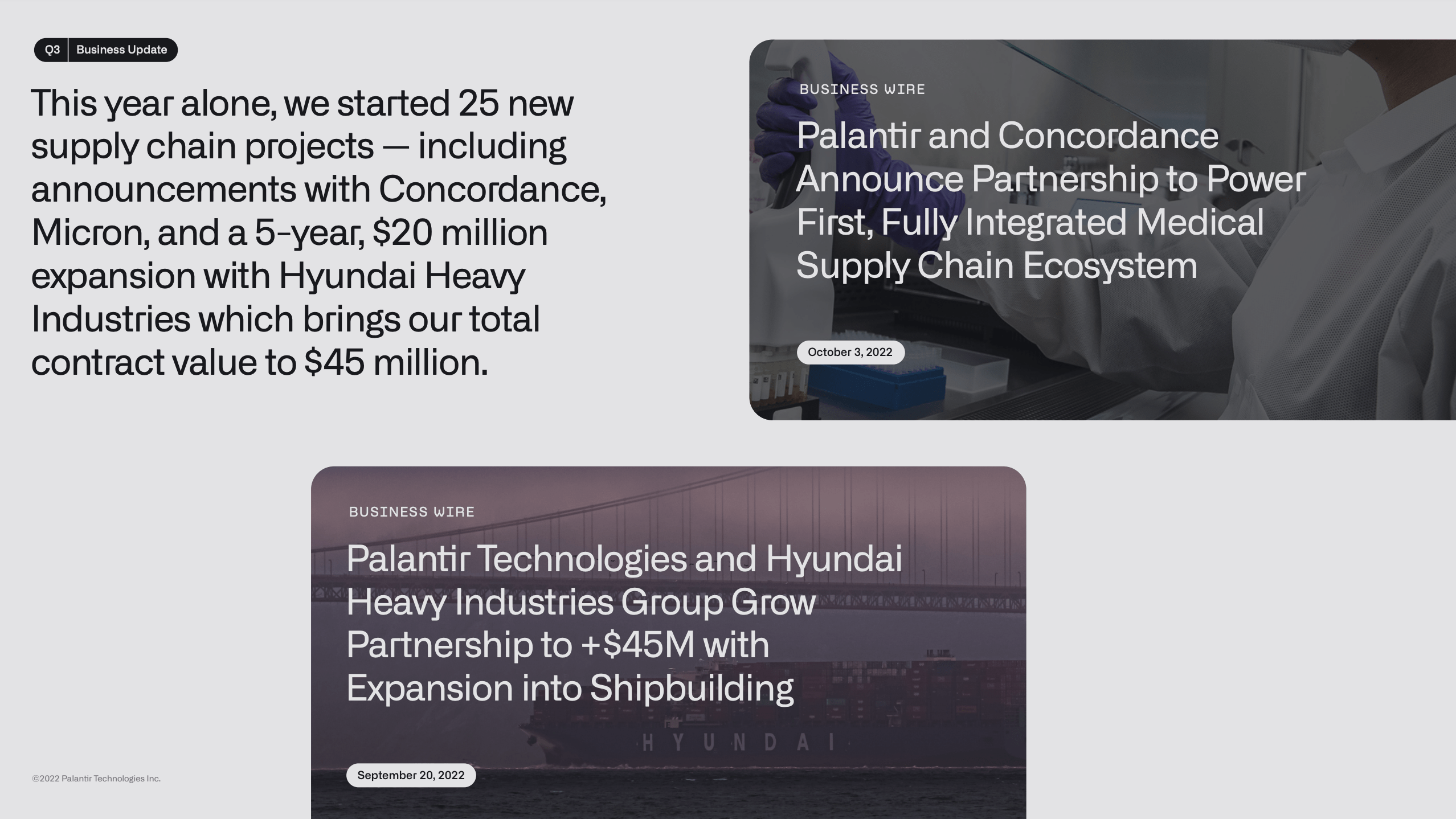

Lastly, critics are now talking about how Palantir did not hit their revenue guidance of 30% growth YoY for 2022 and is now projected to be 23% for a total of $1.9B of revenue. However, the leadership team forecasted originally having a CAGR of 30% through 2025, so if the next two or three years were much higher numbers, they could still maintain this commitment, as government revenues are lumpy as stated before. The other key takeaway that critics are not factoring in enough is how their business model operates with a slow but steady ramp until their customers hit the expansion phase where they sign larger expansion contracts. We saw a great example of this with Hyundai Heavy Industries Group signing an initial $25M contract in January 2022, and then in the same year in October they signed a 5-year, $20M expansion, for a total contract value of $45M. Companies of this size do not make large expansion investments in a software platform in the same year of their initial purchase unless significant return on investment is being reached by the customer.

Palantir added 33 net new customers, but most of those customers won’t hit the expand phase until 12 to 18 months out from initial purchase. The remaining 240 deals that Palantir closed were all renewals or expansion deals in Q3. I believe critics and even shareholders are not fully appreciating the high switching costs and network effects of Palantir’s software within customer organizations. Palantir customers continue to expand on other business segments to adopt the technology so they too can realize better business decisions based on real-time data correlations. Even some of the customers Palantir previously had whom left, came back to Palantir because they couldn’t achieve the same results with other software companies.

I have never seen a software company consistently do such a large amount more of expansion deals than net new customers. This can only happen in a unique business model like Palantir’s which can only work if the software platforms are delivering clear quantifiable value and alpha to its customers. This demonstrates the power of the effectiveness of Palantir ‘s Gotham, Apollo, and Foundry software platforms. The net revenue retention rate stayed strong at 119% which is extremely impressive because the average spend with each customer is in the millions. It is the quality and quantities of these large revenue customer spends, which should breed confidence to shareholders on the sustainability of the business. While other software point solutions will come and go throughout the years, I am confident Palantir will still be here solving some of the most complex challenges for our government and commercial businesses.

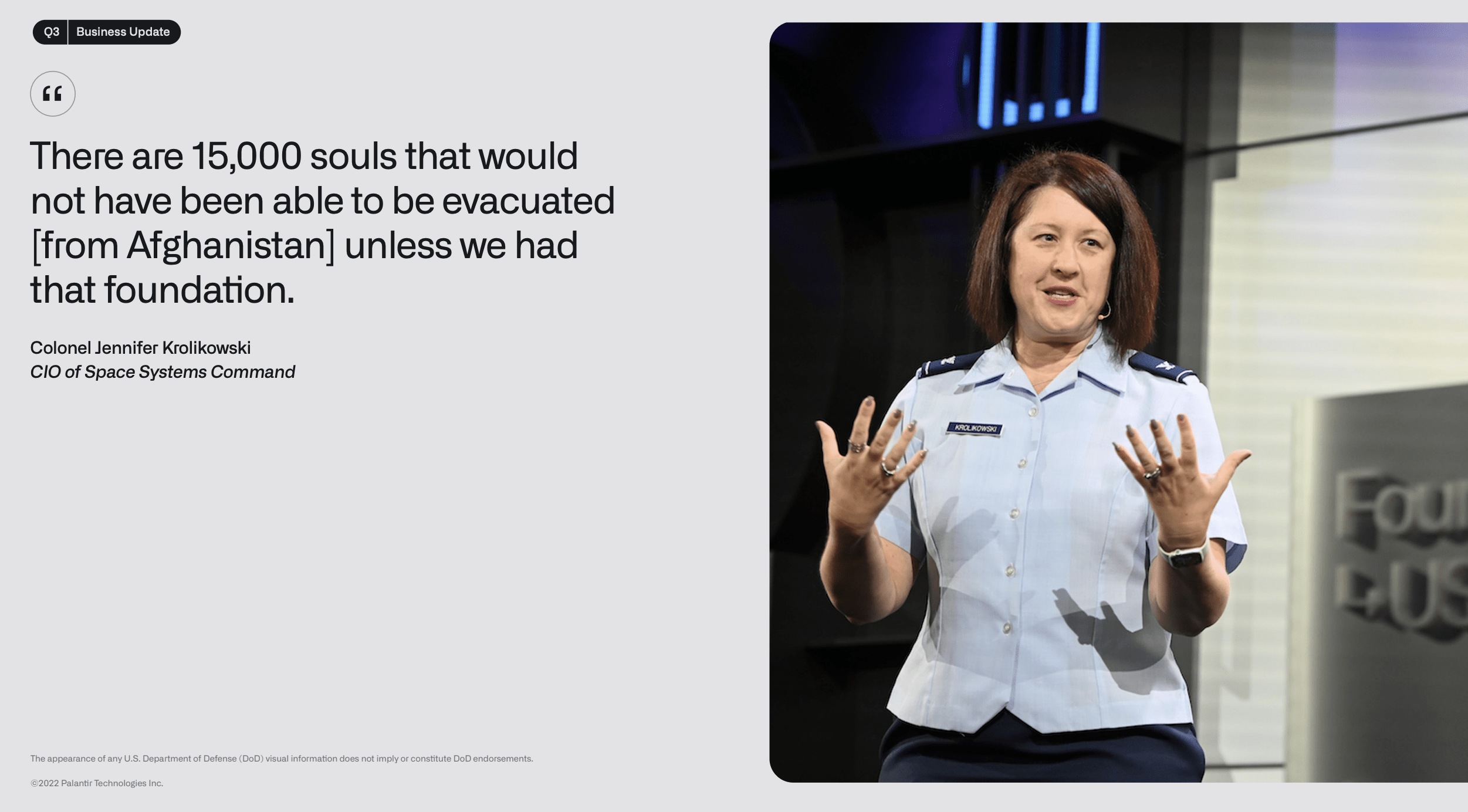

Palantir Helping Save Over 15,000 Americans (Q3 Earnings Presentation)

Palantir not only has a sustainable sales business model and customer base, but financial sustainability in how they run the business. CEO Alex Karp catches judgement by some that he is not a financially minded CEO and just engineering minded, but this is false. Karp and his leadership team understood ahead of time where political tensions were rising, planned for challenging financial times ahead, and ensured they were operating with $0 in debt. Palantir also has $2.4B in cash and another $950M in undrawn credit commitments. CEO Alex Karp’s comments in his letter to shareholders says it all regarding this matter.

We have the privilege of planning and building a company for the long term. The current shift in macroeconomic conditions has served to winnow the field of participants in the technology sector and will continue to do so. Our ability to plan for the future is made possible because we have $2.4 billion in the bank and no debt. We have also now generated $461 million in cash flow from operations over the past two years. Our preparation for the current moment is anything but accidental.

We anticipated the present volatility and will continue to grow not in spite but because of it.

Palantir has entered its next phase of transformation selling downstream, modularizing its Foundry platform, and providing easier access to customers to adopt the technology. The company provides usage billing now allowing customers to realize ROI faster and as the customers’ success grows so does Palantir’s revenue. Palantir is one of the few SaaS companies in the market who utilize contribution margin as a key indicator of performance, health of the business, and its’ efficiencies.

In their 10-Q Palantir comments the following on measuring contribution margin. “We believe that the revenue we generate relative to the costs we incur in order to generate such revenue is an important measure of the efficiency of our business. We define contribution margin as revenue less our cost of revenue and sales and marketing expenses, excluding stock-based compensation, divided by revenue.”

I also agree that contribution margin provides a company the best measurement of its efficiencies on customer acquisition and lifecycle value and the health of their business model being sustainable.

Palantir’s Evolving GTM Strategy

Palantir is expanding its marketing efforts and evolving its Go-To-Market (GTM) strategy with accomplishing the following:

Holding its first user customer conference FoundryCon in Palo Alto and London, where customers got to network and share their success stories with the public.

The company also has its first nationally aired commercial coming to market while be a sponsor of the Army vs. Navy football game on December 10, 2022.

Customer use cases are becoming more public and they are highlighting the quantifiable savings and value of Palantir is delivering.

Palantir is gradually entering into standard forms of marketing like commercials, attending conferences, and submitting their technology for analyst reports.

This year IDC’s Worldwide Artificial Intelligence Software Study for Market Share and Revenue ranked Palantir number one against all other competitors.

Palantir was Named a Leader in AI/ML Platforms by Independent Research Firm Forrester this year.

They have also earned awards from Gartner and even had a presence at Gartner’s Supply Chain event.

The “black box” company is nothing of the sort anymore, and in my opinion never was if investors took the time to read the resources provided on Palantir’s website, blog site, and watched the videos on their YouTube channel. All the resources are there for investors and potential customers to learn what Palantir software delivers and their advantages in the market.

Becoming the Software Foundation for Industries

Palantir is gradually becoming the foundational software or operating system for entire industries. They have over 25 supply chain deals currently in the works including projects with customers like Micron (MU), Merck (MRK), Hyundai (OTCPK:HYMTF), the U.S. department of Health and Human Services, The World Food Programme, and Airbus (OTCPK:EADSY). This company is solving real world problems at scale that are delivering growing value for its customers.

CEO Alex Karp describes this transformational movement in his most recent shareholder letter very effectively. I believe it is important for shareholders to pay attention to some of the details in the following commentary:

This shift has been made possible by a more sophisticated and coherent commercial offering, which can now be deployed to new customers within minutes.

In the past, the time and effort required to build relationships with and deliver our software to customers weighed on our ability to expand at a pace commensurate with demand in the market. We were iterating and experimenting with building a software platform, and our customers were iterating and experimenting with us.

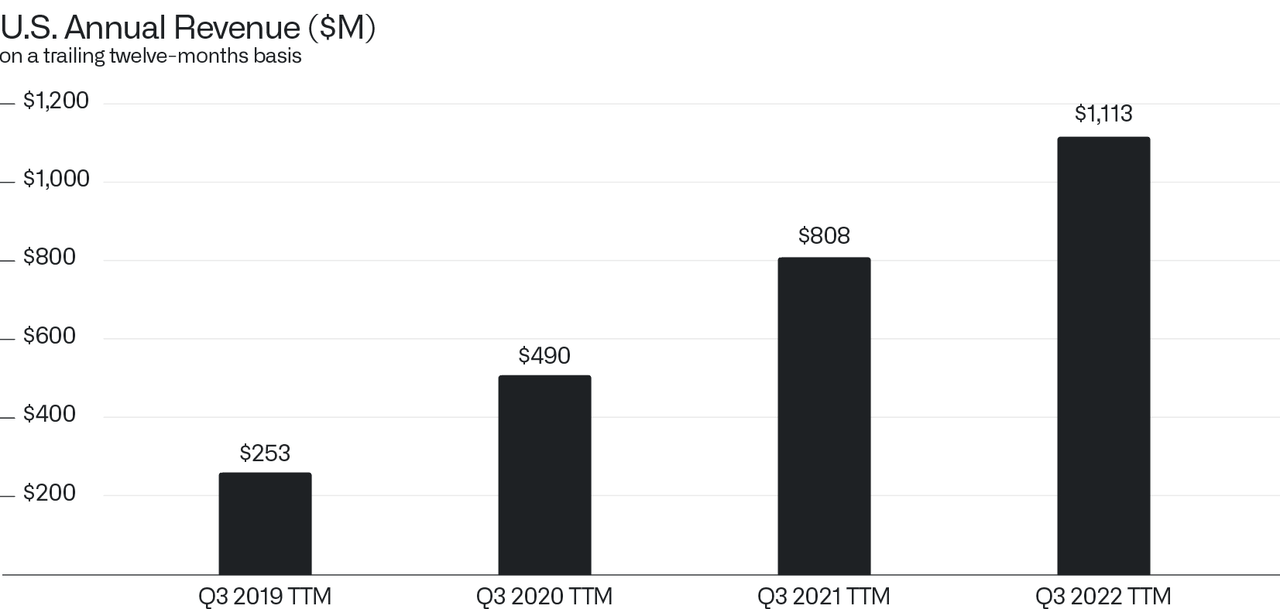

In the twelve months that ended September 30, 2019, we generated $253 million of revenue in the United States. Three years later, we generated $1.1 billion of revenue, representing a 64% compound annual growth rate.

U.S. Annual Revenue Growth (Q3 CEO Letter to Shareholders)

We now anticipate that individual regional markets within the United States, including, for example, the Midwest, the Southeast, New England, and Texas, all have the potential to develop into billion-dollar businesses on their own over the near term.

We are also seeing individual markets abroad, which were once an ancillary part of our operations, develop into significant businesses in their own right.

In the United Kingdom, for example, we generated $160 million in revenue in the twelve-month period that ended September 30, 2021. The following year, we generated $213 million, representing a year-over-year growth rate of 33%.

We believe that our revenue in the United Kingdom has the potential to grow significantly in the coming years.

Other countries will follow.”

Summary:

Karp’s comments around Palantir’s business evolving in how it acquires and onboards customers says it all. I am including a lot of communication from the CEO’s message to shareholders because it lets you understand where his vision is for the future.

It was perhaps a necessary interregnum. Our approach, however, to the acquisition and onboarding of new customers has changed significantly, a shift made possible by a far more systematic and mechanized sales operation.

A pure software business has now emerged.

I leave you with this final thought, Palantir has demonstrated consistent execution on their approach to delivering business outcomes for customers and they are disciplined in their management of the business. They are not frivolously spending on stock-based compensation for no reason, but to keep the most talented employees worldwide away from those who could pay more like Microsoft (MSFT), Google (GOOG) (GOOGL), and Amazon (AMZN). Palantir’s technology is so exceptional that all of those mega cap companies partner with Palantir.

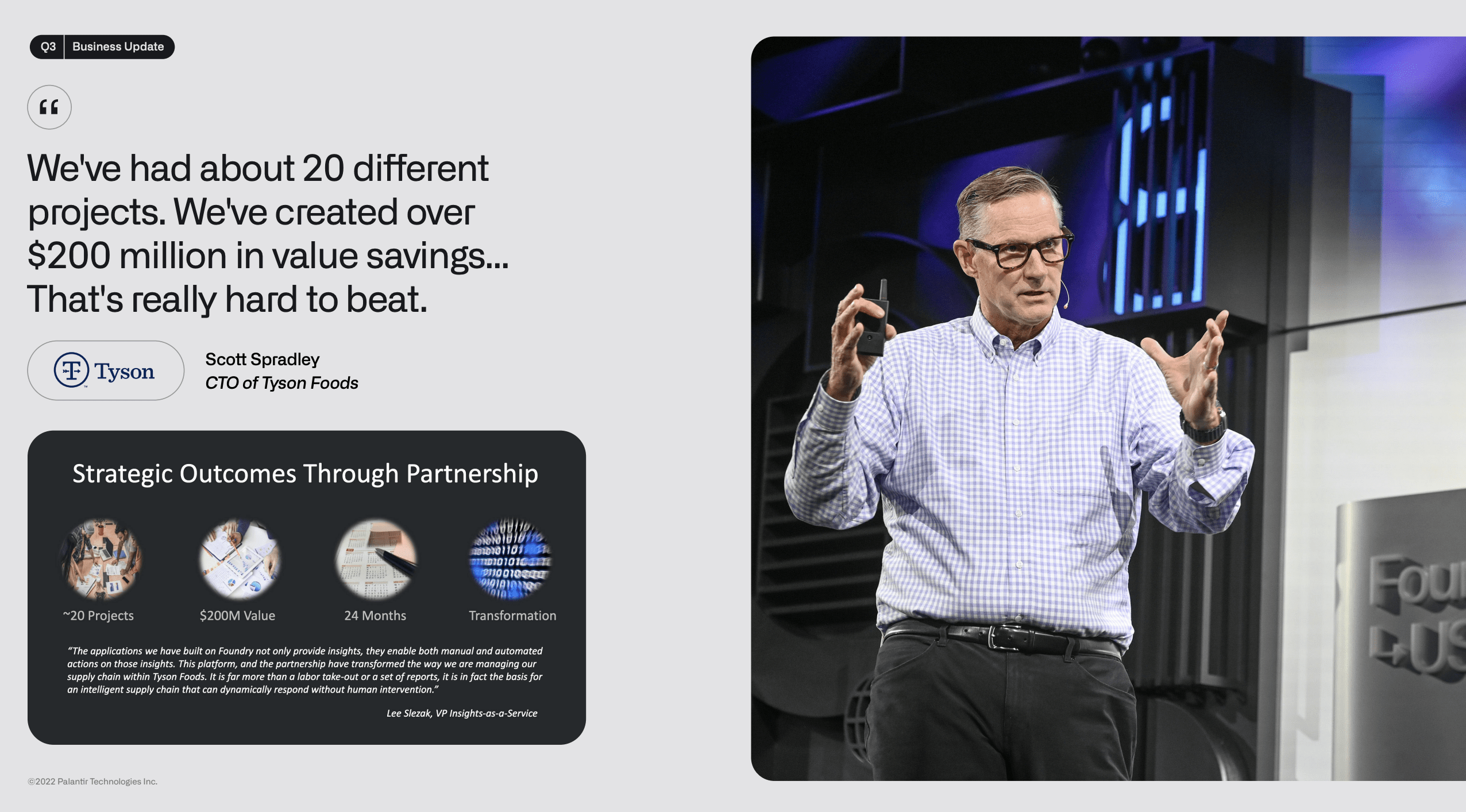

Tyson Foods CTO Saves $200M with Palantir (Q3 Earnings Presentation)

Palantir has an extremely meaningful technological advantage in its software and this has been demonstrated by the types of problems that only they have been able to solve. Shareholders can rest assured Palantir is focused on creating meaningful contribution margins with each customer it acquires, they are not making decisions recklessly.

For all who read this article and dig deeper into these areas of Palantir stated above, they will then truly understand why I am saying this company is playing 4D Chess for the long game and everyone else is playing checkers.

I continue to dollar cost average my position to continue lowering my cost basis, and continue to learn more about the technology advantages Palantir is creating. This is not financial advice but in my opinion this is what shareholders should want to do as well, and stay patient as the results have time to grow.

Whether you like the stock, hate the stock, or love the stock I encourage you to provide comments below on your takeaways from the article. Please share your thesis on the company so others can hear your point of view, and let’s continue to learn together. Thank you for reading this article and you can find my other articles on Palantir and other stocks here.

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Be the first to comment