Michael Vi

With the sharp rally in the markets since the start of the year, especially in tech stocks, one question that many investors are asking is: is it too late to benefit from the rebound? Many of last year’s deepest-hit growth stocks are up double digits already this year almost entirely on sentiment; while earnings season has yet to play out for most of these names.

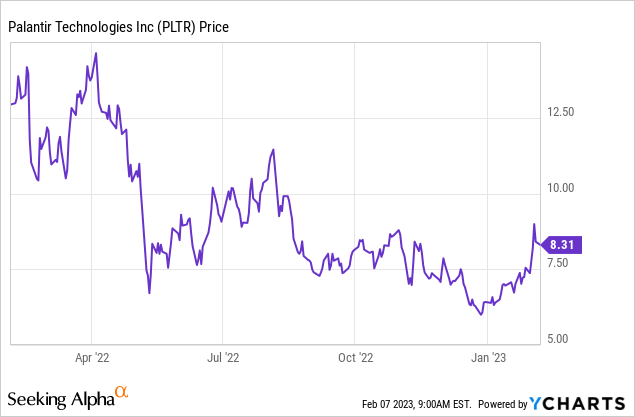

My short answer here: no, it’s not too late – and stock selection remains of the utmost importance. That’s why I’m doubling down here on Palantir (NYSE:PLTR), the big data giant known for its close association with the U.S. government. Having rebounded ~30% so far this year, I think Palantir still has plenty of steam to rally further.

The bull case for Palantir remains vibrant, even amid darkening macro clouds

I am very bullish on Palantir. It is still one of the largest individual holdings in my stock portfolio, and I routinely use dips as an opportunity to either add to my position or sell short-dated puts to earn quick premiums. In my view, short-sighted thinking has dragged Palantir down: yes, even though macro headwinds are pressuring Palantir’s deal flow, this is not at all a problem unique to Palantir as all enterprise SaaS companies have experienced higher scrutiny in the deal approval process. Few, however, have software products with as broad of a use case as Palantir, and with as large of an addressable market.

Here is my full bullish thesis on Palantir:

- Big data is a massive discipline that can be applied in nearly limitless ways. Palantir isn’t a software company that serves only one or a limited set of use cases. Data and inferences that can be made from data are prevalent in just about everything: which explains why Palantir is such a powerful tool for both public and private sector clients.

- Growth at scale. Despite being at a ~$2 billion annual revenue scale, Palantir continues to deliver mid-20s y/y revenue growth. Few companies are able to achieve this kind of growth at scale, and it’s a testament to the wide applicability of Palantir’s products and the humongous clientele it has drawn (in particular, the U.S. Army). Prior to the recent government spending slowdown, Palantir had forecasted >30% y/y growth through 2025 (which may still be feasible when macro conditions turn around).

- Stepping up go-to-market momentum. Palantir is chasing growth across a wide variety of channels. The company has stepped up its sales hiring, a nod at the broad market opportunity it has and the need for more territory coverage. Palantir also has deepened relationships with ISVs (integrated service vendors) that can resell Palantir’s products without its involvement and offer additional coverage that Palantir’s direct sales force can’t handle.

- One foot in the public sector, one foot in private. Palantir made its name on being a large federal government contractor, but its products are just as compelling to an enterprise segment that is growing ever more obsessed with the value of big data. Most software companies start off as primarily dealing with enterprise buyers, and then hopefully getting FedRAMP certification to sell into public sector clients later. Palantir did the reverse: but now, its momentum with Fortune 100 companies is continuing to grow, and customer adds are continuing to trend at an impressive pace.

- Free cash flow. Though not yet profitable from a GAAP standpoint, Palantir continues to exceed internal expectations for free cash flow, which means the business is self-financing (a departure from many other rapid-growth software companies that continue to need to raise capital to finance their losses).

Valuation is now accessible

Recall that during the peak of tech-stock mania during the pandemic, Palantir was one of the hottest trades in the stock market, commanding valuation multiples north of >20x forward revenue.

That valuation is a relic of the past, and though I’m almost certain Palantir will never return to such an aggressive valuation, I think there is room for the stock to climb north.

At current share prices of just over $8, Palantir trades at a market cap of $17.29 billion. After we net off the $2.47 billion in cash on Palantir’s most recent balance sheet, the company’s resulting enterprise value is $14.82 billion. For the current fiscal year FY23, meanwhile, Wall Street analysts have a consensus revenue target of $2.29 billion for the company, representing 21% y/y growth (data from Yahoo Finance).

This puts Palantir’s valuation at just 6.5x EV/FY23 revenue. In my view, I’m a confident buyer here until the stock reaches 9x forward revenue, implying a $11 price target and ~34% upside from current levels.

Strong business momentum continues, even despite growth deceleration

Much fuss has been made over Palantir’s declining revenue growth rates. In Q3, Palantir’s most recently released quarter, the company reported 22% y/y revenue growth – slightly beating Wall Street’s expectations, but guiding to $501-$503 million in revenue for the fourth quarter as well, implying a deceleration to 16% y/y growth.

The usual suspects are at play here: FX headwinds have hurt the company’s international revenue, and macro headwinds are impacting the company’s pipeline.

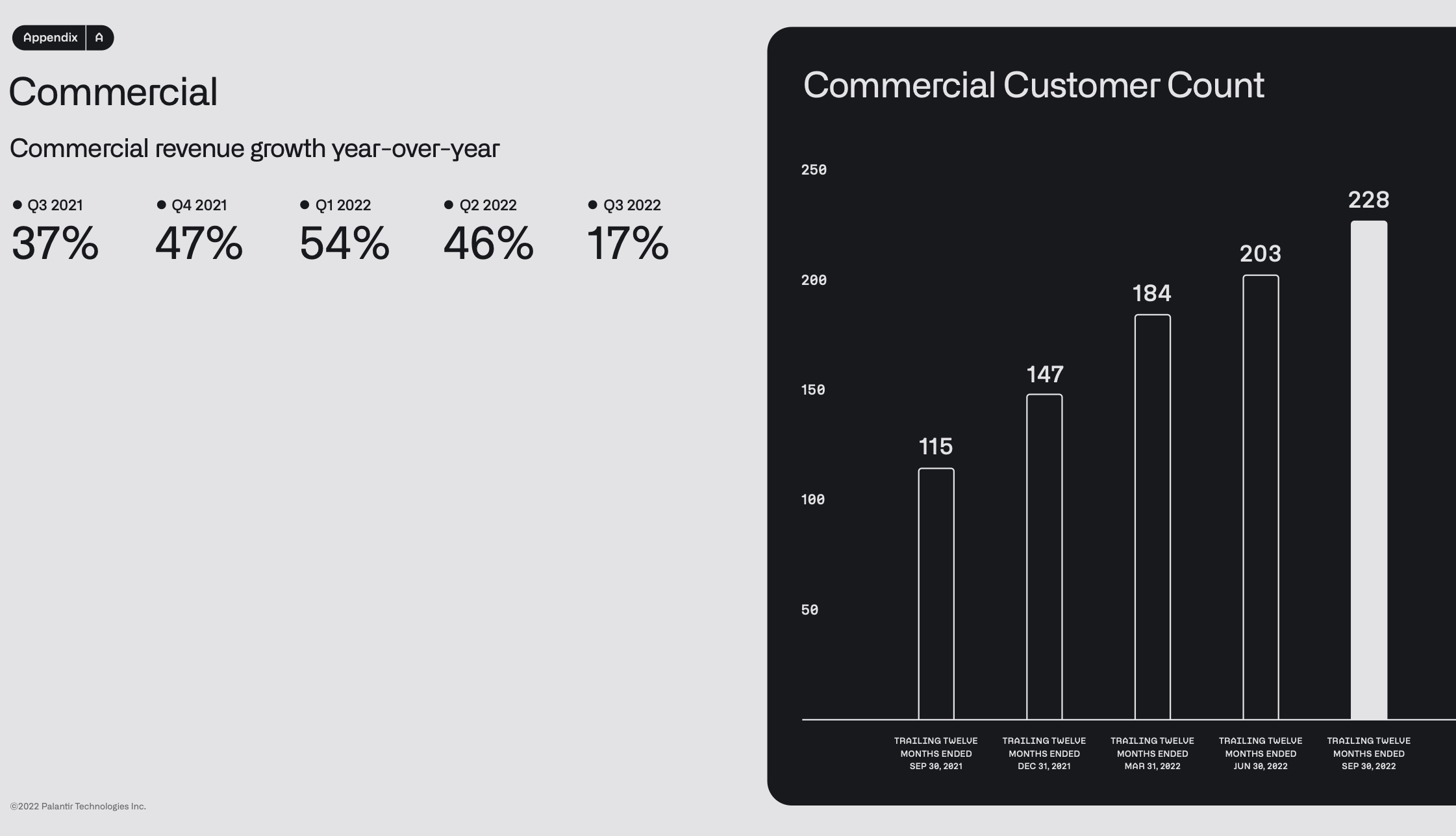

And as shown in the chart below, the impact to the company’s commercial segment – its biggest growth engine – has been severe, with revenue growth decelerating to 17% y/y from 46% y/y in the prior year quarter.

Palantir commercial trends (Palantir Q3 earnings deck)

Alex Karp, the company’s CEO, certainly acknowledged the impacts of a toughening macro environment, but expressed confidence in Palantir’s ability to navigate through it during the Q&A portion of the Q3 earnings call:

I mean other people should — we’ve been predicting an even more challenging macro environment than this for the last 20 years. I mean how long have we been in the trenches together? 17 years in the trenches. The products are built for a disjointed world, a world where you need horizontal and vertical integration in the military context or actually we have low latency where your systems — underlying systems actually don’t work even though on the PowerPoint, they say they do, where you have to deliver results overnight, where your business totally f-ed and you got to make it work in a quarter. That’s what our business is built for.

By the way, that’s why we prepared and then that’s the technical thing. Why do we have 8 quarters of free cash flow? Do you think it’s a coincidence, we were preparing for this. We have — why do we have $2.4 billion in the bank and no debt? We weren’t living in the metasphere. We were living in this world in the way we thought it would be — and we’ve been essentially — you could even look at this as a prep. We’re a prepper company. We’ve been preparing it’s like — preppers have their rucksack and a rifle. We have PG, GAIA, Foundry and $2.4 billion in the bank and no debt.”

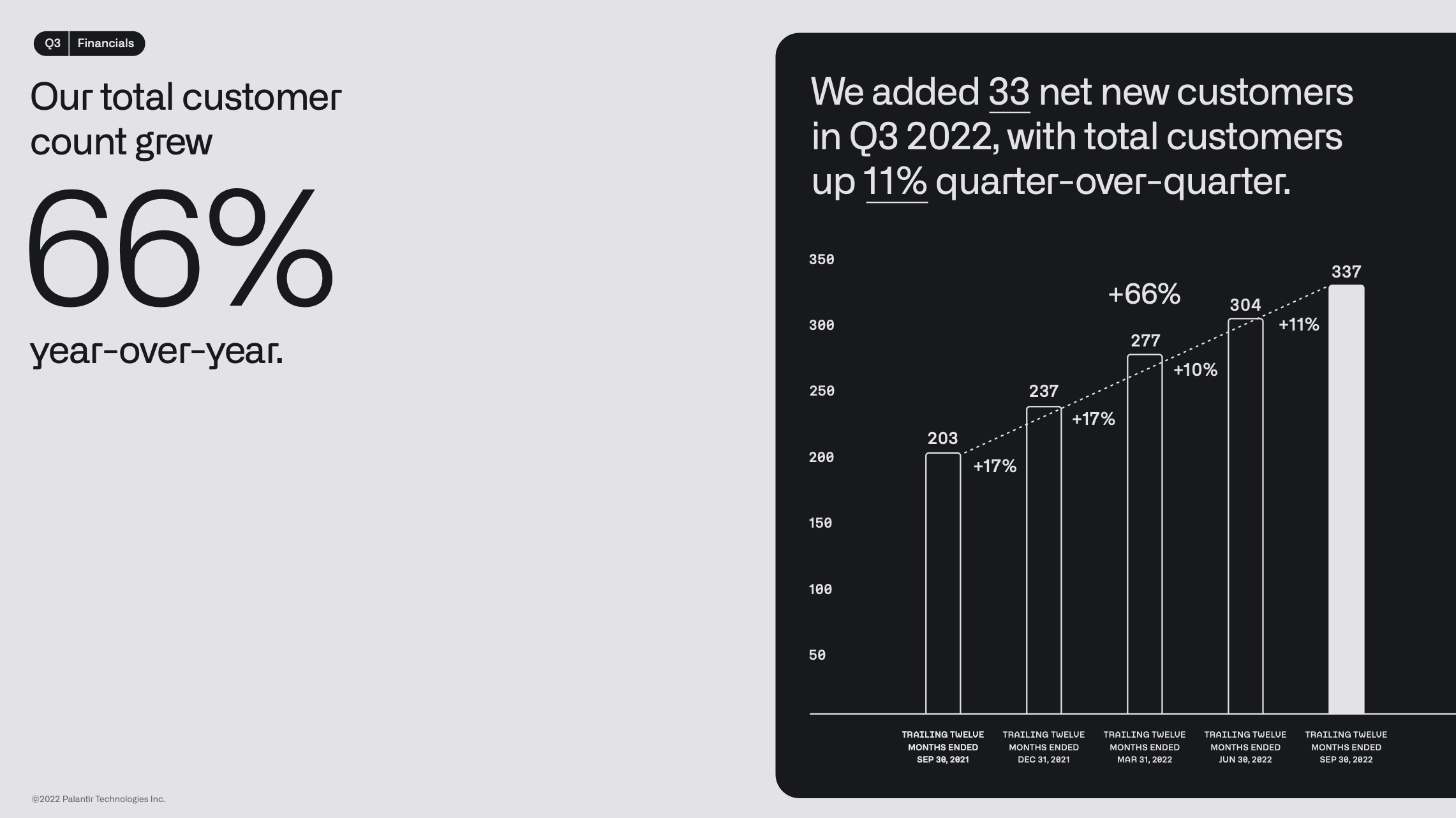

It’s worth noting that Palantir, which has historically had a very small number of overall customers (with its reliance on government contracts), still managed to add 33 net-new customers in Q3 as major headwinds intensified, growing the total customer base by 66% y/y.

Palantir customer count (Palantir Q3 earnings deck)

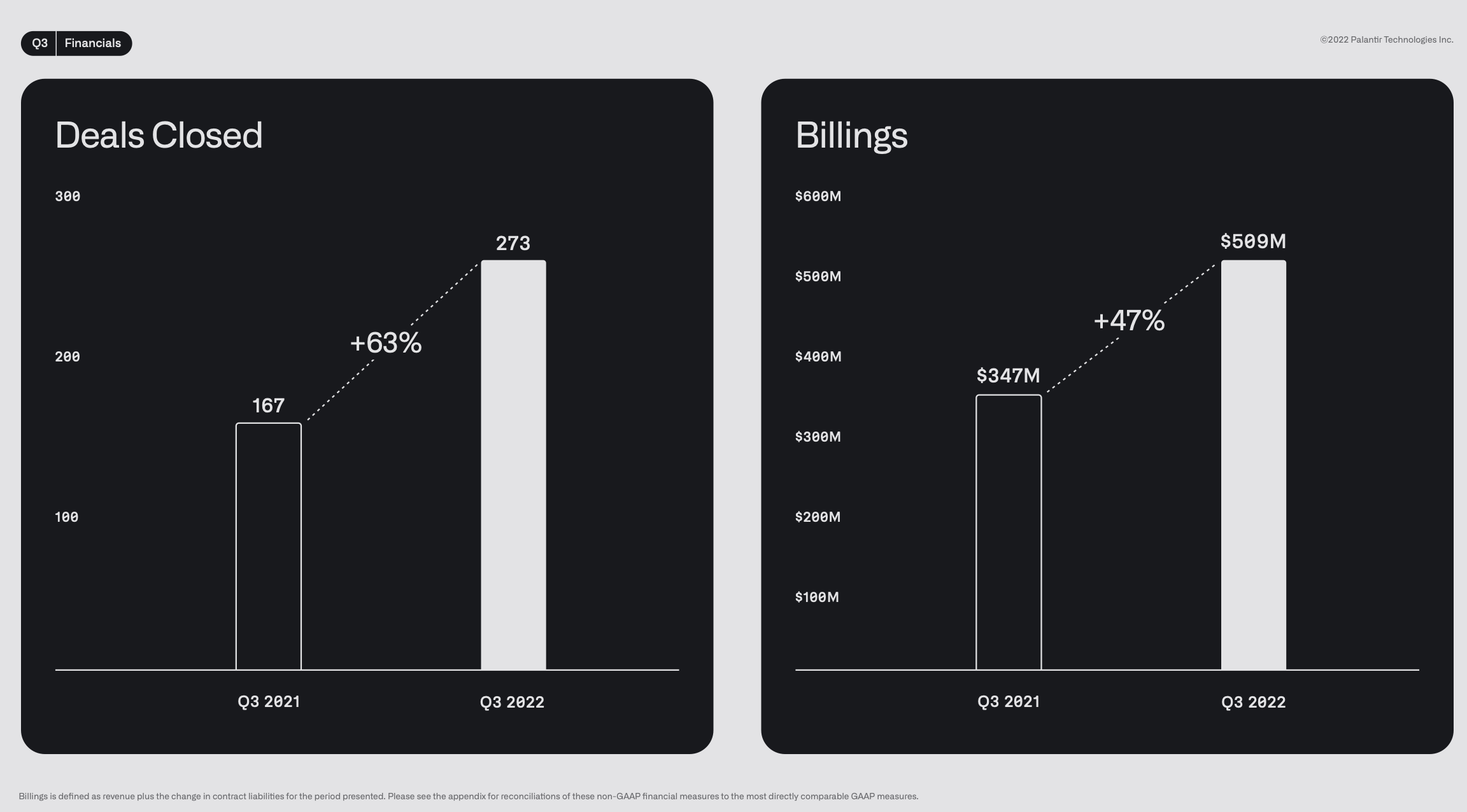

Year-over-year metrics also look quite rosy from a billings perspective. The company closed 273 deals in Q3, up 63% y/y, while billings grew 47% y/y to $509 million, well in excess of revenue and adding to the company’s deferred revenue backlog. As seasoned software investors are aware, billings represent a better longer-term trajectory of a company’s growth trend, as it captures deals signs in the quarter that will get recognized as revenue in future quarters.

Palantir billings (Palantir Q3 earnings deck)

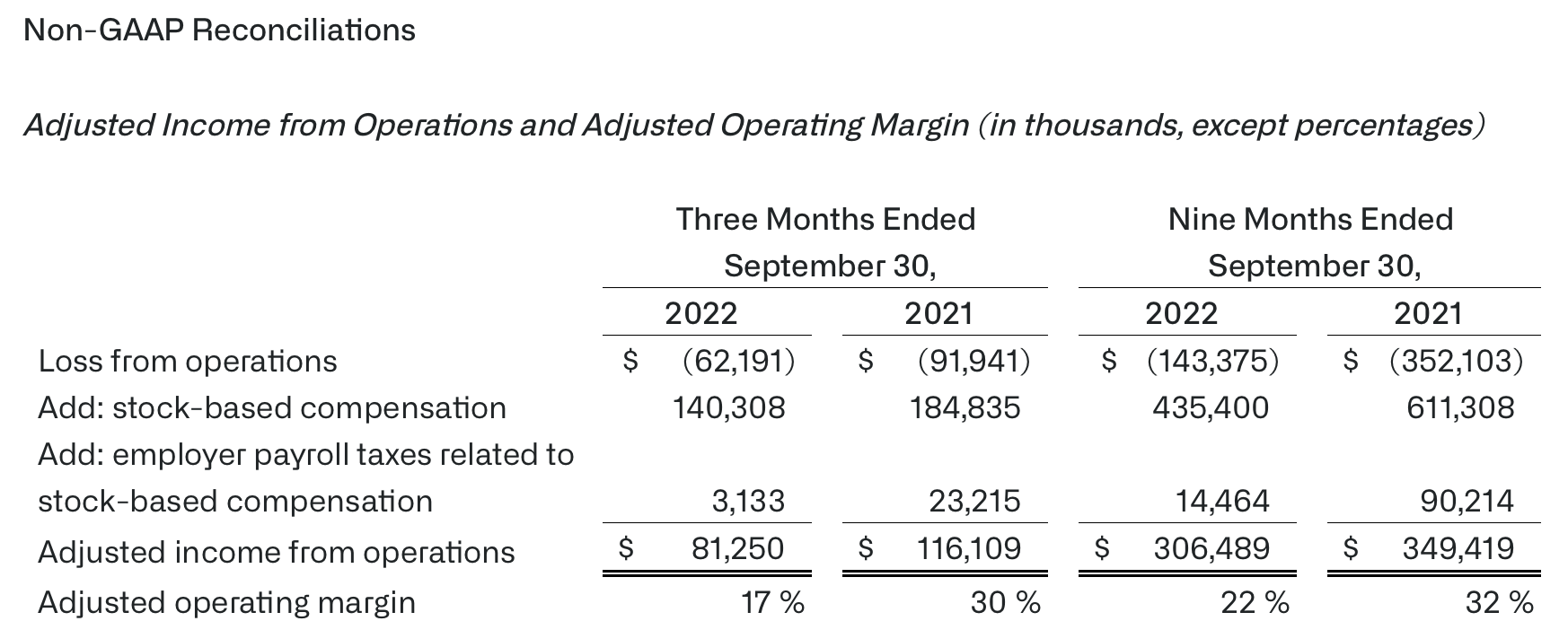

One final positive callout worth making: the compression in Palantir’s share price, at the very least, is lowering the company’s stock-based comp expense on an as-reported basis. This means that the company’s GAAP operating losses were cut down in Q3 to -$62.1 million, representing a -13% operating margin: significantly better than -23% in the year-ago quarter.

Palantir GAAP vs. non-GAAP results (Palantir Q3 earnings deck)

In today’s market, which is more sensitive to tech companies’ bottom lines, I think the positive GAAP developments here will be an additional tailwind to Palantir stock.

Key takeaways

In my view, investors have a very rare window to buy into this iconic tech company at a heavy discount to its true worth. Palantir still has plenty of growth levers to pull, especially in the enterprise space, where its products have been deployed only across a small number of companies and industries despite having broad-based applicability. Stay long here.

Be the first to comment