hapabapa

Palantir Technologies (NYSE:PLTR) is a software company that has a focus on data integration, application development, simulation and modeling. The company has developed technology that allows for the marginal cost of data integration to be effectively zero, enabling its customers to perform data integration and use it to their advantage. Another pillar of its technology is simulation and modeling, which allows for the creation of digital twins of entire enterprises. These capabilities were valuable during the COVID-19 pandemic, as they allowed for the ability to make decisions and optimize during times of uncertainty and change.

Palantir Technologies has developed Apollo, a continuous delivery infrastructure and platform engineering tool that allows the company to deploy its products as SaaS environments in on-premise locations, such as Swiss banks, and in exotic edge environments, like on the factory floor or in the automotive industry. Apollo allows for automation of the deployment process, including the adjudication of service level obligations, built-in security measures, and integration with the software supply chain. The tool has been transformative for Palantir and the company believes it will be useful for other companies as well, especially given the increasing geopolitical fracturing and the need for specific environments in different markets. Palantir also expects the US government will soon require all vendors selling software to the government to have an automated software supply chain.

Palantir’s Commercial strategy

Palantir Technologies is evolving its go-to-market strategy to focus more on working with IT departments and selling modular products. Previously, the company’s sales strategy involved selling monolithic solutions to business users and avoiding IT. The new strategy involves selling to IT first and understanding their needs and architecture, then using that knowledge to create business value and build a relationship with both IT and business users. This shift has resulted in shorter sales cycles and a more modular approach to product development, including the creation of HyperAuto, a software-defined data integration product for ERP systems with a three-month sales cycle and one-day pilot.

The company has also been working on developing modular products and identifying buyer personas to help the sales force better understand their customers and match the right products to their needs. This focus has allowed the company to shorten the cycle time on customer relationships and establish a strong presence in the market. Palantir is now planning to apply this same approach in Europe and continue hiring at the same pace in the US.

Palantir has also been making strategic investments, primarily through SPACs, in order to expand the capabilities of its Foundry platform and make it the go-to destination for building applications that require integration of disparate data and the creation of decision-making interfaces. These investments have also allowed the company to bring its cutting-edge technology in Edge AI to the commercial world.

Palantir Technologies has evolved its pricing model to be based on consumption, allowing customers to start with a minimal commitment and gradually increase their product consumption over time. This allows them to start with specific problems and then expand as they find more value in the product. The consumption-based pricing model also motivates Palantir to invest in capabilities and allows them to activate their partner ecosystem in a way that was previously not possible with the use of case-based pricing.

Palantir’s dilemma

As we consider the company’s valuation, it is worth noting that some have argued that it is being treated with technology industry multiples, when it could be seen more as an IT consulting firm. Some bear analysts maintain that much of the company’s work involves manual labor that cannot be easily automated, and that therefore the key area of focus for the company should be demonstrating its capabilities in artificial intelligence and machine learning.

These technologies have the potential to significantly improve the company’s margins. However, it is important to carefully evaluate the various programs and initiatives that the company has in place to support its case. I have gathered indications from the Q&A sessions in the earnings call (you can check them here and here). There is also a very interesting white paper on Edge AI, you can request it here.

One noteworthy development mentioned by executives in the earnings call is the company’s Edge AI capability, which is set to be launched on a satellite this month. This technology is designed to facilitate autonomous decision-making across a range of devices and environments, even in conditions of low bandwidth and low power.

Another example of the company’s use of AI and automation can be found in its work with MetaConstellation, which is being used by various Western allied services to make real-time decisions by combining inventory data with AI models. The company has also applied AI and automation in the context of the Army program CD-2, which was used to plan tank movements and navigate difficult terrain.

Additionally, the government customer Space Force is using the company’s software factory, Foundry, as a platform to build AI-powered applications and drive its dominance in space. Foundry is an operating system that integrates siloed data sources and deploys AI/ML models on top of that foundation.

Finally, the company’s Edge AI platform, Apollo, enables the deployment of AI/ML models on low-power devices and networks, allowing for real-time decision making.

In the pursuit of sound investment, it is crucial to assess the company’s performance not just based on its marketing claims, but also by examining the changes in its cost of goods sold and operating expenses relative to revenue. By analyzing the data presented in the table, we can observe that the company has experienced rapid growth, although at a slower rate of 20% compared to previous years at 40%. Additionally, it is notable that all cost items have decreased in proportion to revenue. These observations can be checked below:

Author’s computations based on company financials Author’s computations based on company financials

All this sounds great, but there’s a caveat.

Palantir’s Valuation Risks

It appears that the company has been caught unprepared, facing accusations of utilizing investments in Special Purpose Acquisition Companies (SPACs) for the purpose of acquiring new clients and increasing their own revenue streams. Now, I can’t deny that the company did indeed invest in SPACs that were also clients, but they insist that they plan to continue making strategic investments in the future, even if they don’t take the same form as the SPAC investments of the past. They claim to be dedicated to being the infrastructure that businesses rely on, and will do whatever it takes to achieve that goal. Apparently, the SPAC program is reaching its peak, and none of the 30 or so customers they acquired in the fourth quarter were SPACs. That being said, it’s hard to ignore the fact that their revenue growth rate slowed down significantly in 2022. Any potential investors should definitely keep an eye on this situation.

Palantir

Well, it seems the impact of all this has already hit us. In 2022, the company reported a significant new cost related to losses on marketable securities. It’s highly likely that these securities were mostly SPACs. We should note that the utilization of the SPACs strategy has allowed smaller companies to gain access to the technology offered by Palantir from the onset, as they exchanged shares instead of cash. However, the current situation does seem to bear resemblance to the actions taken by Enron, which is not great.

There are other investment risks to consider with this stock, but in my opinion, the entanglement with SPACs and the possibility of the company being downgraded to an IT consulting business are the biggest concerns. One could have serious implications for the company’s financials, potentially even raising questions of fraud and bankruptcy, while the other presents a risk to the company’s valuation.

Investment Case for Palantir

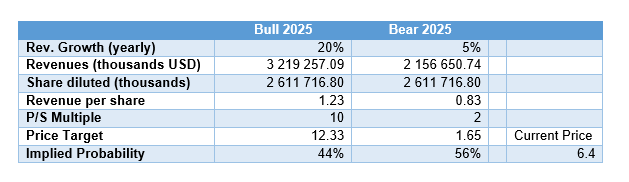

Given the previous assessment, we are led to two basically conflicting scenarios. On the one hand, things could go swimmingly for the company. They could shake off their SPAC-related woes and keep chugging along with an AI/ML business status. But on the other hand, it’s possible that they’ll be demoted to IT consulting status and take a hit in their valuation, not to mention the losses they might suffer from the SPACs. The bull scenario assumes a healthy 20% revenue growth rate and a generous 10 times revenue valuation multiple. But the bear scenario paints a gloomier picture, with a 5% growth rate and a measly 2 times revenue valuation multiple.

Author’s computations

If we consult the table, we can see that the bearish scenario could spell disaster, with a potential loss of 74% from $6.40 to $1.65. It’s not looking good, with an estimated probability of around 56%. I’m not one to be pessimistic, but I got to say, it doesn’t look like a great asymmetric bet.

We’ll have to see how things play out in 2023. Maybe if they can get a handle on the SPAC situation and continue to reduce their costs relative to revenue, we’ll see a dramatic change in those probability numbers. But for now, based on what we know, I don’t think we can be too optimistic.

Be the first to comment