Drew Angerer

Palantir Technologies Inc. (NYSE:PLTR) is a leading software company which helps organizations and governments break down data silos and unlock the power of their data. The company recently reported a strong fourth quarter of 2022, as it beat both top and bottom line growth estimates.

Palantir has its roots as a military-first organization, and it was originally backed by the CIA and used for “terrorist hunting.” Palantir’s platform was even rumored to be used high profile cases such as the assassination of Bin Laden. Given the increased global uncertainty, especially surrounding the Russia-Ukraine war, it is no surprise that world defense budgets surpassed $2 trillion for the first time ever in early 2022. More recently U.S. lawmakers authorized a staggering $858 million in national defense spending, which was $45 billion higher than the Biden administration had initially requested. Data from Statista indicates the U.S. defense budget will reach close to $1 trillion by 2032.

Given that the data source doesn’t seem to have been updated with the most recent details, I forecast a $1 trillion defense budget will come sooner than we may think. Palantir is poised to benefit from these increased spending trends, as it provides the technology platform for key military decisions. In this post, I’m going to break down Palantir’s fourth quarter financials and dive into recent contract discussions before revealing my valuation model of the stock.

Strong Fourth Quarter Financials

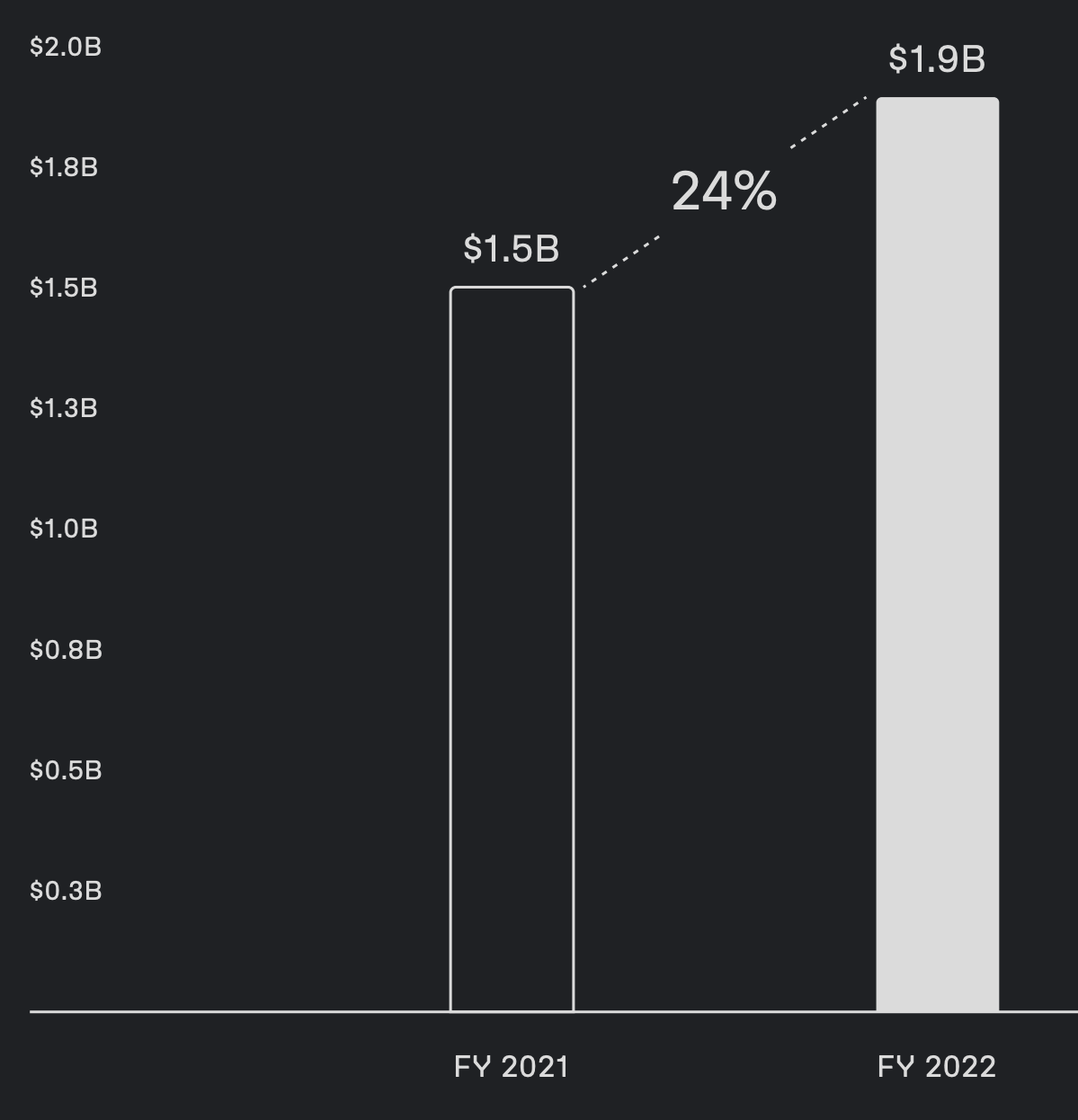

Palantir Technologies Inc. reported strong financial results for the fourth quarter of 2022. Its revenue was $508.62 million, which increased by a solid 18% year-over-year and beat analyst expectations by 0.72%. For the full year of 2022, revenue was $1.9 billion, which increased by a rapid 24% year-over-year.

Revenue Palantir (Q4,22 report)

The results for the company in Q4 2022 were driven by mostly U.S. revenue, which contributed to 59.3% of its total or $302 million and rose by a solid 19% year-over-year. This was a positive sign given the strong U.S. dollar, which has resulted in a foreign exchange headwinds for many companies, with large international revenue contributions. Over 40% of internationally derived revenue is still fairly high, but the trend of strong U.S. revenue growth should help to offset this, as international revenue grew by a lesser 11% year-over-year. In addition, the currency markets tend to be cyclical by nature, and the U.S. dollar has corrected down versus the euro from its high in February 2023. Therefore, I don’t deem this to be a long-term issue.

Overall, Palantir Technologies Inc. added 30 net new customers in Q4 ’22, which represented an increase of 55% year-over-year. You may initially wonder why this didn’t translate directly into a major revenue boost, and this is for a couple of reasons. The first major reason is that when a deal is “signed,” Palantir doesn’t capture that revenue in the same quarter (usually), as it is normally recognized over time. In addition, Palantir operates a “land and expand” business strategy in which it aims to win a “small” contract, build trust, prove its ability, and then “expand” to help other parts of large organizations solve problems. During the fourth quarter of 2022, Palantir closed 55 deals with a value of at least $1 million, with 11 of these deals worth at least $5 million and 5 deals worth at least $10 million. Thus, you can see the scale and range of deals are substantial.

By segment, commercial revenue rose by 11% year-over-year, to $215 million. This was mainly driven by a rapid 79% increase in U.S. commercial customers, which rose to 143.

This highlights the beautiful element of Palantir’s business model. The company is targeting large organizations/enterprises, or the “whales” of the industry. This does result in longer sales cycles, but it means fewer deals need to be signed in order to generate significant revenue growth. As the old sales quote says, where there is “pain,” there is “profit” to be made. In this case, Palantir is targeting industries with the largest pain points. A prime example is healthcare, which is an essential but expensive and badly run service globally. Palantir previously scored a partnership with the National Health Service (NHS) in the U.K., which is the largest single-payer healthcare system in the world. Palantir previously helped the vaccine rollout and various Personal Protective equipment (PPE) schemes. Upon further research, I discovered that Palantir was recently awarded a contract award extension until June 2023, with a value of £11.5 million ($14.23 million).

Palantir Contract Extension £11.5 million (UK Government data)

This contract mentions “data platform services” and the “Federated Data Platform,” which is expected to be the new NHS data platform. Palantir Technologies Inc. was a front-runner for a ginormous $437 million (£360 million) contract related to the entire data platform. To put the size of this contract into perspective, this is ~86% of its entire Q4,22 revenue of $509 million, which would seriously accelerate the company. Of course, given the size of this contract, it is no surprise that the deal has come under scrutiny and sparked concerns about a U.S. company holding U.K. healthcare information.

The good news is Palantir has continued to get its claws into the NHS and has poached its former deputy director of data services (Harjeet Dhaliwal) and the former NHS director of AI. A Palantir spokesperson indicated the talent will “not be working on NHS-related projects.” This may be true but it is a strange coincidence, and the relationships and insights carried over will be valuable either way. On a purely competitive basis, the contract bidders include U.K. based Quantexa and Privitar, a small British software company. Personally, I believe these companies don’t have the same brand clout as Palantir, or the vast experience directly with the NHS. Therefore, I believe Palantir is still a frontrunner for this if it can get through regulatory hurdles.

Over in the U.S., Palantir has signed a number of large hospitals throughout 2022. This includes the Cleveland Clinic, Tampa General and a another operator with over 2,400 healthcare sites. Combined Palantir currently works with at least 10% of the entire hospital system in the U.S. In late January 2023, it was also reported that Palantir scored a major contract with Cardinal Health, a huge pharmaceutical distribution company.

Palantir is also helping many companies with supply chain management. This has been a major “pain point” for companies since the lockdown of 2020 and increased global uncertainty. Examples of recent client wins include Coca-Cola distributors in the U.S. and Europe, and Toyota Material handling.

Palantir’s government revenue increased by a solid 23% year-over-year, to $293 million. This was driven by a huge $75 million contract with the U.K. ministry of defense for its Defense Digital data platform.

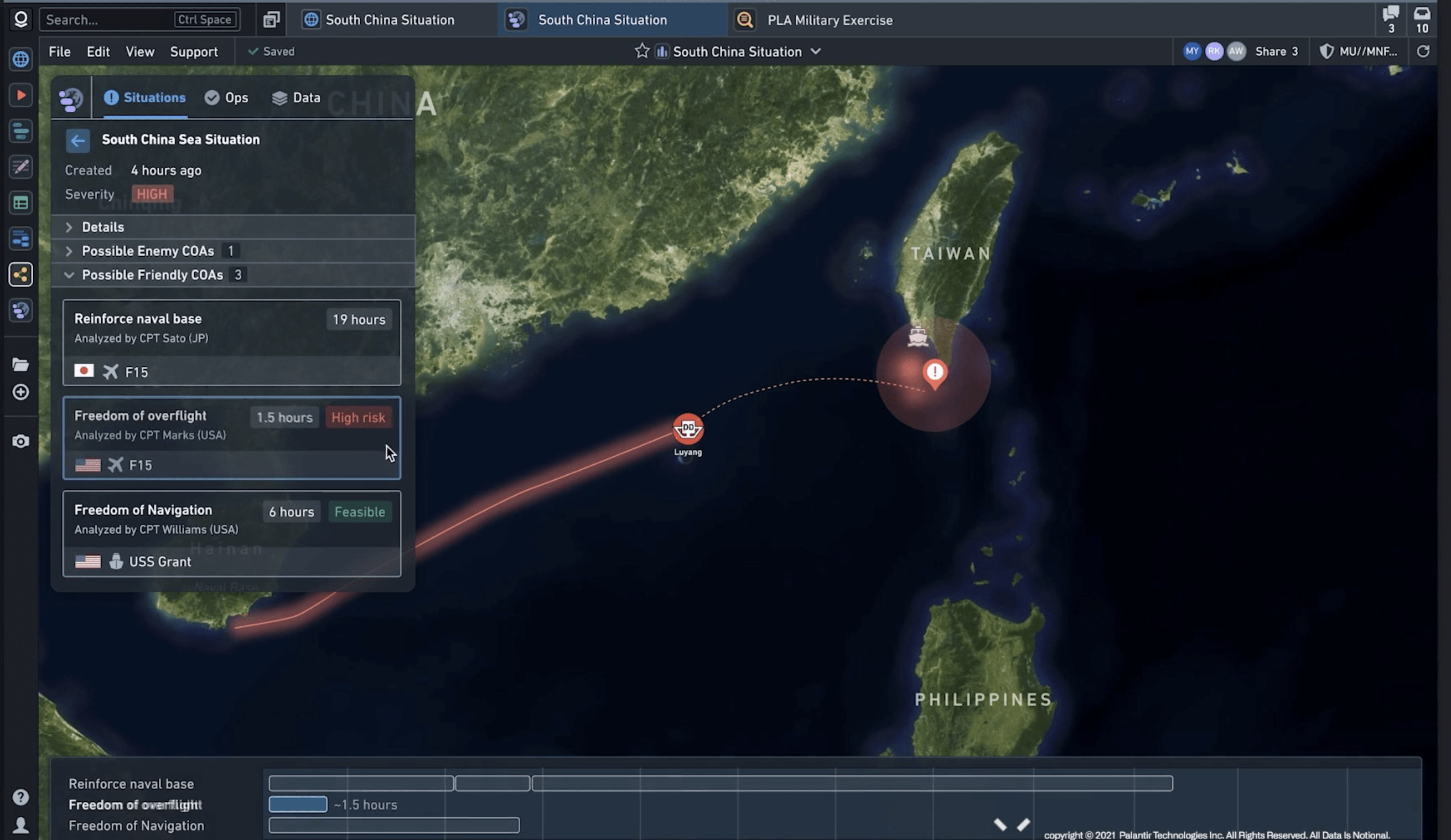

CEO Alex Karp has had a military-focused rhetoric for a long time and Palantir’s website has lots of content on this topic. For example, Palantir’s website shows a video of its software being used to detect Chinese battleships around the coast of Taiwan. This was meant to be an example, but given the military rhetoric by Chinese leader Xi Jinping and the Russia-Ukraine war, this could be a reality in the future. Either way, the fear of such a scenario should be a strong motivator for more military contracts.

Palantir Military Application Taiwan-China (Author Demo Screenshot)

On a technology front, Palantir is continually innovating and recently launched its Foundry Marketplace Developer Suite. This enables users to build and launch data Software as a Service (“SaaS”) apps on its platform, which offers huge potential for an “App Store” style business model.

In addition, Palantir Technologies Inc. has a developed specific use case based offerings such as its “Fed Start” product on Apollo. This enables organizations to gain FedRAMP authorization in record time and at a much lower cost. I forecast this solution will be popular, as achieving FedRAMP authorization effectively enables companies to sell directly to government agencies which is a huge underserved and lucrative market.

Profitability and Balance Sheet

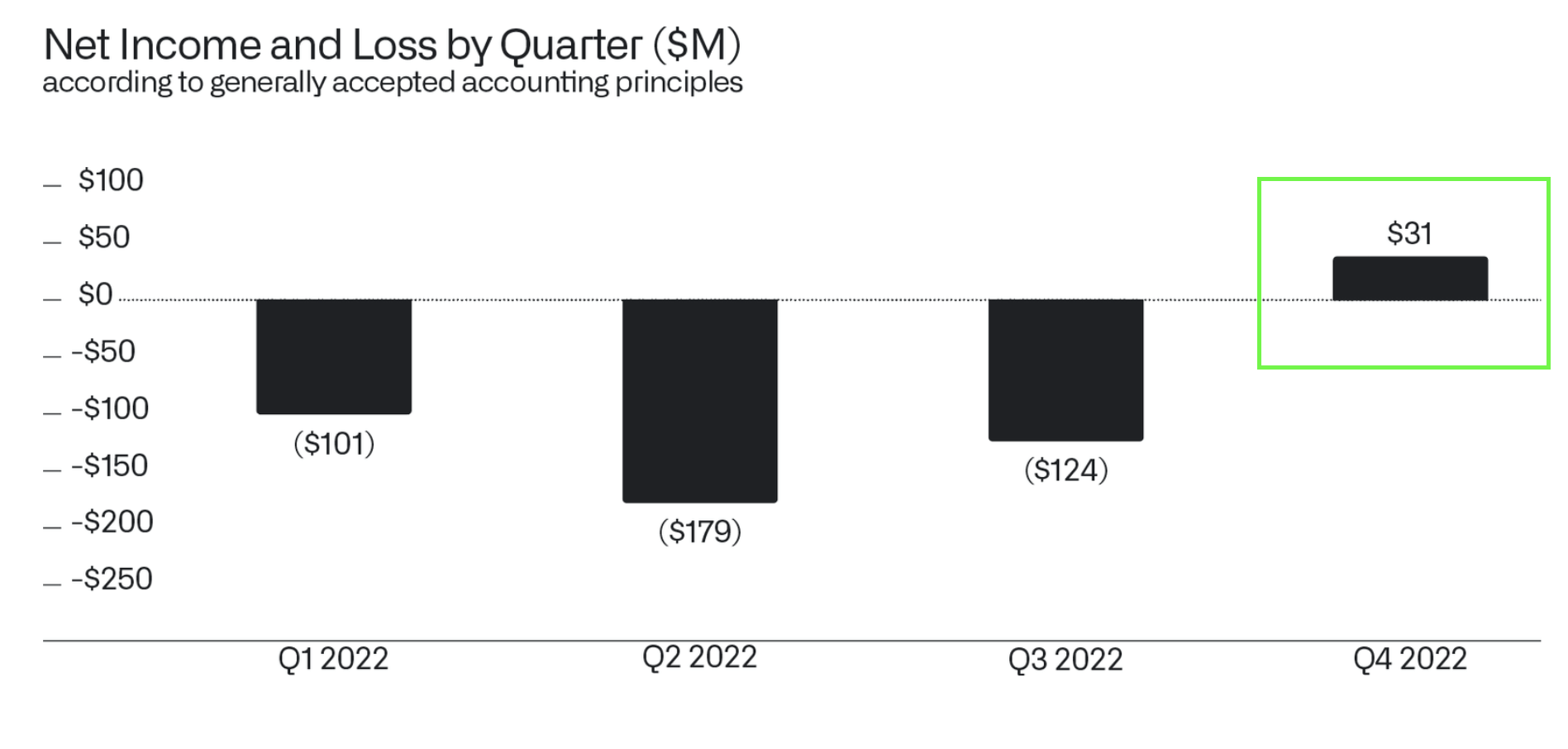

Palantir’s profitability was especially exciting during the quarter, as the company reported net income profitability (on a GAAP basis) for the first time ever. Its net income was $31 million, which was substantially better than the negative $124 million reported in the prior quarter. Earnings per share (EPS) was $0.04, which beat analyst expectations by 49.48%, according to Google Finance data.

Profitability (Q4,22 report author annotations)

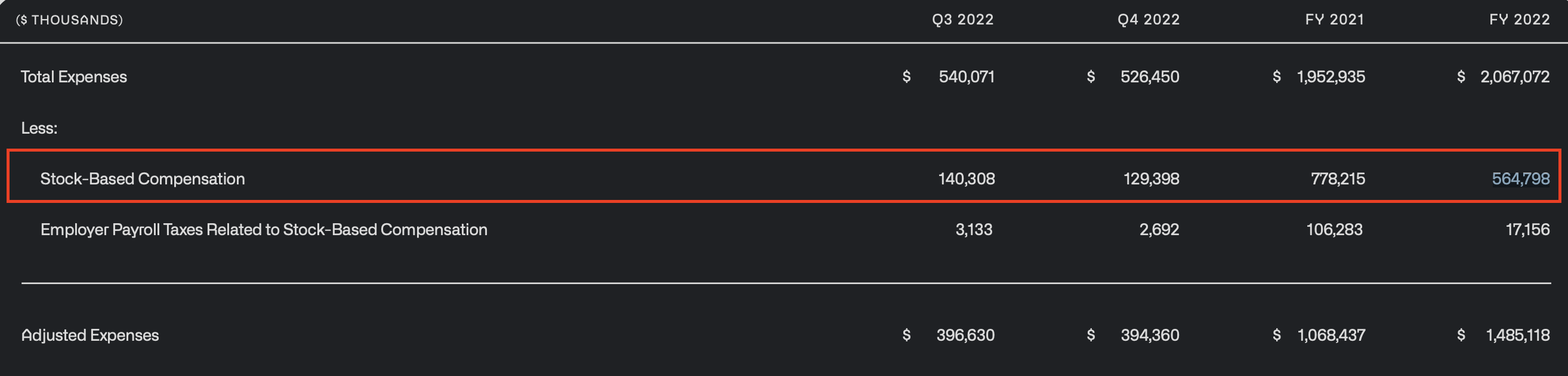

Stock-based compensation (“SBC”) is still an issue for the company, although this has declined from $778.2 million of total expenses in the full year of 2021 to $564.8 million for the full year of 2022. In terms of dilution, Palantir’s share count has increased by ~4%, from 2.01 billion shares in Q4 ’21 to 2.09 billion shares by Q4,22. This increase is not a major issue, given revenue has increased by 18% year over year.

Stock Based Compensation (Q4,22 report author annotations)

Palantir has a fortress balance sheet, with $2.6 billion in cash and cash equivalents and virtually no debt. In addition, the company has $950 million related to an undrawn credit facility, should it need extra dry powder.

Valuation and Forecasts

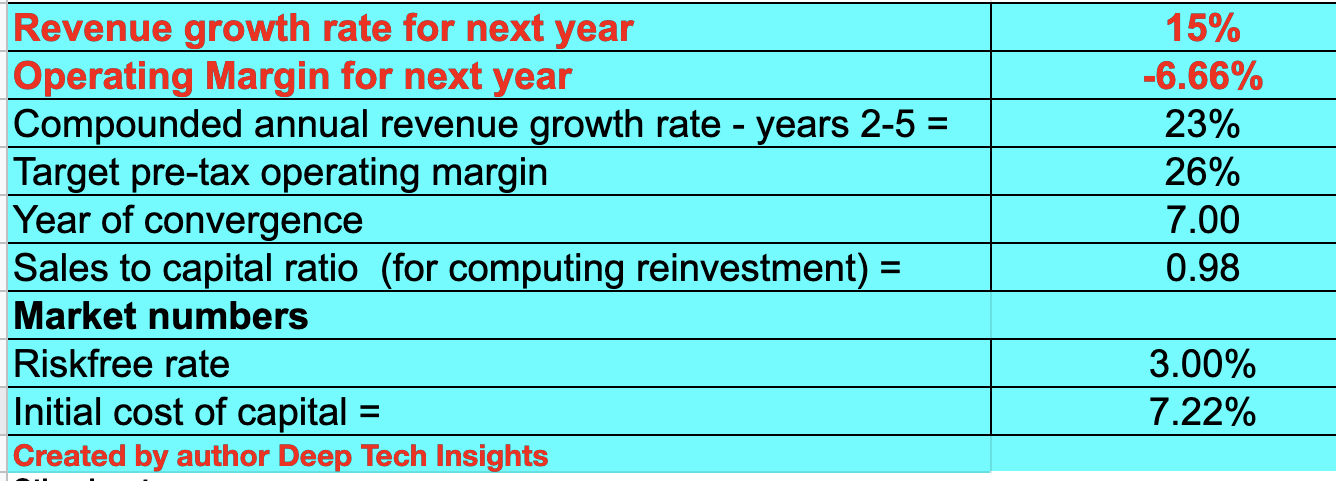

In order to value Palantir, I have plugged its latest financials into my discounted cash flow valuation model. I have forecast just 15% revenue growth for “next year” which is referring to the full year of 2023 in my model. This growth rate is based upon the mid-range of management’s guidance of between $2.18 billion and $2.23 billion for the full year of 2023. In years 2 to 5, I have forecast a faster growth of ~23% per year.

This may seem optimistic, but it is really just a return to the prior growth rate generated in Q3,22 and is still much lower than the greater than 30% growth rate experienced in the early half of 2022. I forecast this growth to be driven by improved economic conditions, as well as increasing wins across military and healthcare applications, as per the current trend.

Palantir stock valuation 1 (created by author Deep Tech Insights)

To increase the accuracy of the model, I have capitalized Palantir’s R&D expenses, which has lifted operating income slightly. Over the next 7 years, I have forecast a 26% operating margin. This is fairly optimistic but given Palantir’s “land and expand” growth, I forecast its contract wins to expand inside organizations. For the full year of 2022, the company reported a solid net dollar retention rate of 115% which means its customers are staying with the company and spending more.

Palantir stock valuation 2 (created by author Deep Tech Insights)

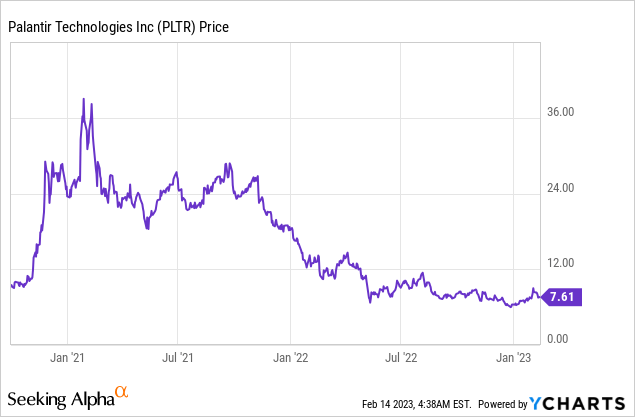

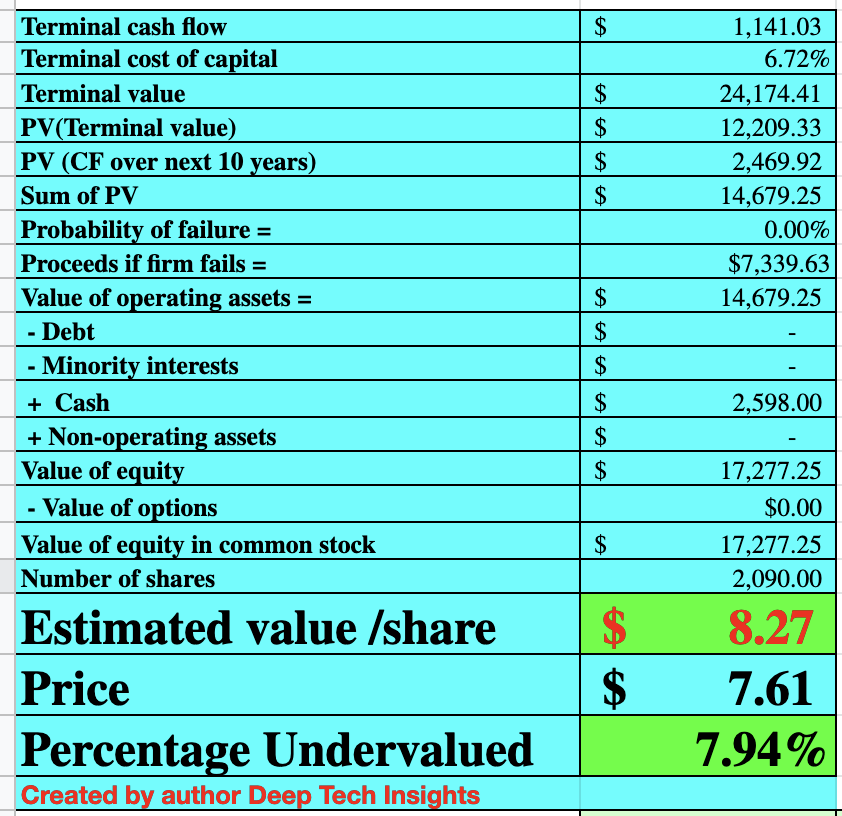

Given these factors, I get a fair value of $8.27 per share. Palantir stock is trading at $7.61 per share at the time of writing and thus it is ~8% undervalued, according to my model and forecasts. The stock price looks to be on the move upwards in pre-market trading, thus it will likely be higher, when you read this post. Therefore, I will label the stock as a “hold.”

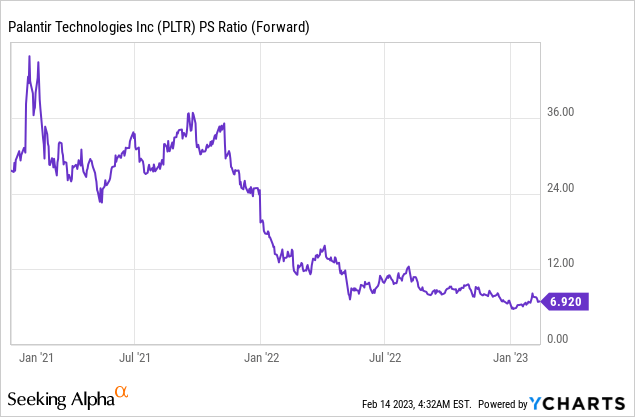

Palantir also trades at a price to sales ratio of approximately 6.92, which is significantly cheaper than its 2021 P/S ratio of between 24 and 45.

Risks

Recession/Longer Sales cycles

Many analysts have forecast a recession in 2023. Therefore, I would expect longer sales cycles for Palantir, especially as the company tries to close larger commercial contracts.

Final Thoughts

Palantir Technologies Inc. is a tremendous software company which is truly innovating across the worlds of big data and AI. Given the AI industry is forecast to grow at a 37.3% compounded annual growth rate (CAGR), Palantir is poised to benefit from this trend. Its strong military roots should also give it a competitive advantage when securing military-related contracts, driven by rising defense budgets. 2023 will likely be a year of slower growth, but the secular trends are solid for Palantir Technologies Inc.

Be the first to comment