Scott Heins

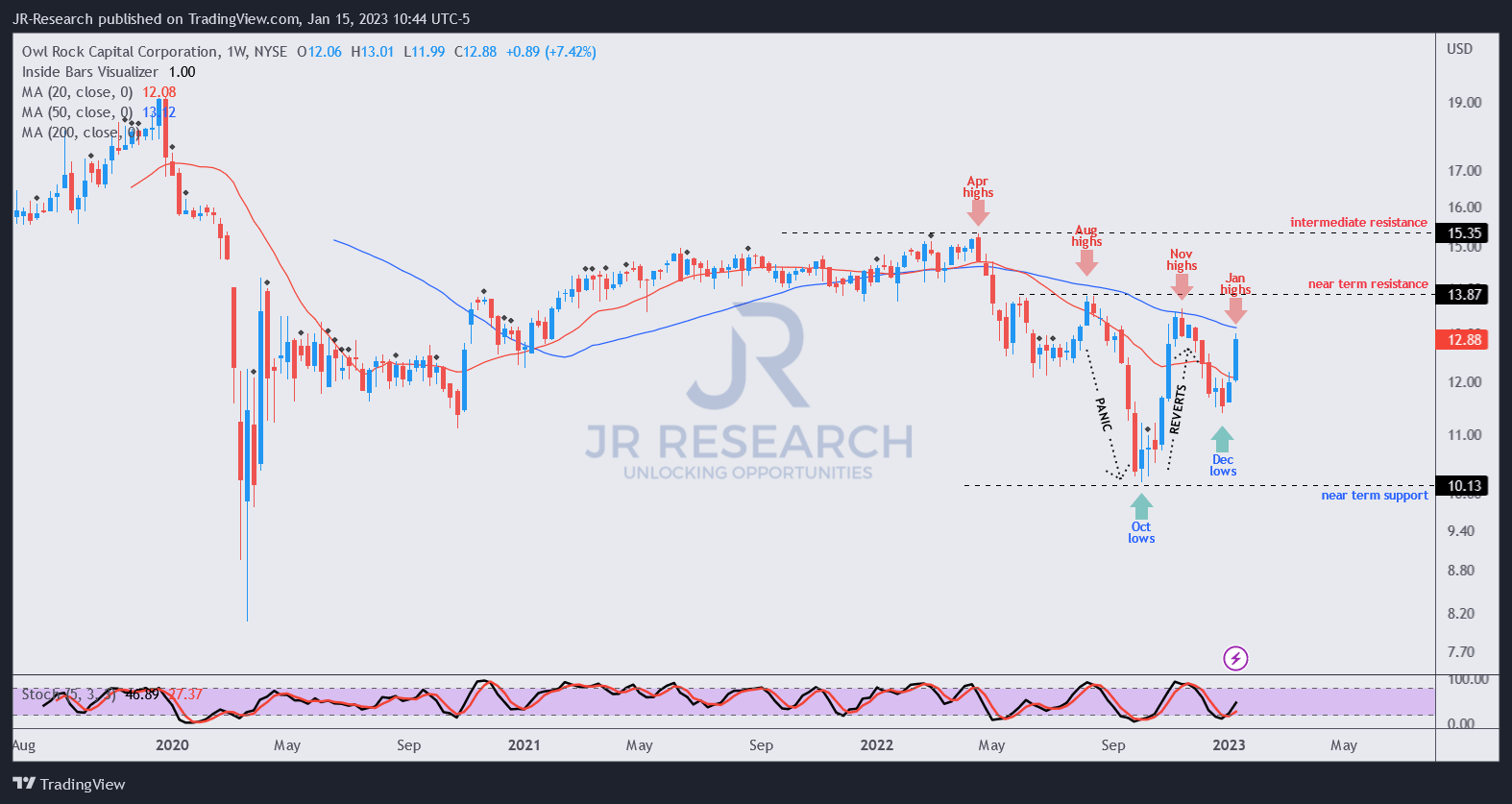

Investors of leading middle-market business development company (BDC) Owl Rock Capital Corporation (NYSE:ORCC) had an opportunity to pick its recent December lows, as ORCC pulled back sharply.

In an early November article, we also cautioned investors that ORCC seems due for a steep pullback after a massive recovery from its capitulation lows in October.

Accordingly, ORCC fell nearly 16% from its November highs to its December bottom, allowing astute investors a fantastic opportunity to add exposure.

ORCC surged last week as it outperformed the S&P 500 (SPX) (SPY) and closed nearly 8% above its week’s lows. As such, we assessed that ORCC’s valuation has normalized from its December bottom, even though it remains priced at a discount against its peers’ median.

Despite that, we don’t expect ORCC to revisit its October lows, with the Fed is likely closer to the end of its historic rate hikes that have inflicted massive damage.

Keen investors should recall that 98% of Owl Rock Capital’s investment portfolio is predicated on floating rates, allowing the company to capitalize on the Fed’s hikes. However, with the Fed likely moving to temper the cadence of its hikes from the next FOMC meeting, it should moderate the NII per share tailwind that has benefited ORCC moving ahead.

As such, we believe investors’ focus could turn to its portfolio companies’ net asset value (NAV) performance as investors parse which sectors/industries could emerge with more resilience against a potential downturn/recession.

Accordingly, ORCC has a well-diversified portfolio, with 23% of its Q3 portfolio fair value (FV) attributed to its top ten holdings. The company also has a diversified industry exposure, even though Internet software and services companies accounted for 12.7% of its portfolio FV.

Hence, the company’s positioning and selection could help shield it against a steeper-than-expected economic downturn by avoiding more exposure to cyclical companies.

Bloomberg reported recently that “software firms are by far receiving a disproportionate amount of attention from private credit lenders.” Hence, we believe the market for private credit is functioning well, more so in the current environment where banks have pulled back their financing.

Accordingly, leading Wall Street banks have been laden “with more than $40 billion of debt they were unable to offload,” reducing their appetite to take on more leveraged lending activities.

Hence, the BDC market remains well-placed to serve its portfolio companies, which should benefit a major lender like Owl Rock, given its relatively low leverage and prudent underwriting. Golub Capital accentuated:

Lenders can be choosy now as there is a lot of demand for our capital. We are focused on providing good loans to companies that are likely to do well even if market conditions, [and] macroeconomic conditions, get more challenging. – Bloomberg

With Owl Rock due to report its FQ4 and FY22 earnings release on February 23, investors are urged to assess whether there is a deterioration in its key lending and underwriting metrics.

Also, investors should assess management’s commentary on the expected moderation in its NII per share uplift, given the Fed’s likely pause or even earlier than expected pivot in its rate hikes.

While investing in ORCC benefits from an attractive NTM dividend yield of 11.5%, newer BDC investors should acquaint themselves with the regulatory gap and valuation metrics of their portfolio companies.

Bloomberg ran a primer on private credit recently, given the surge in interest, highlighting some of the critical pitfalls:

Yet the inherently risky industry receives little oversight. Most private credit funds and business development corporations, which are companies that hold the assets in a loan portfolio, are only required to make basic quarterly disclosures to the US Securities and Exchange Commission. They aren’t overseen by banking regulators. And most private credit funds haven’t lived through a prolonged recession, which typically brings a spike in defaults. At times, the parties, which often use outside services to measure loan values, can arrive at a different number, says Eugene Grinberg, co-founder of financial research firm Solve. “Lenders can shop valuation companies like issuers shop ratings agencies,” he says. – Bloomberg

In Owl Rock Capital’s filings, the company also highlighted such valuation risks entailed with an investment in ORCC as it added:

Because such valuations, and particularly valuations of private securities and private companies, are inherently uncertain, the valuations may fluctuate significantly over short periods of time due to changes in current market conditions. The determinations of fair value in accordance with procedures established by our Board may differ materially from the values that would have been used if an active market and market quotations existed for such investments. Our net asset value could be adversely affected if the determinations regarding the fair value of the investments were materially higher than the values that we ultimately realize upon the disposal of such investments. – ORCC 10-K

Takeaway

ORCC price chart (weekly) (TradingView)

ORCC buyers have vigorously defended its October lows even as it pulled back sharply from its recent November highs.

Hence, we believe market operators don’t expect a significant recession that could batter ORCC’s portfolio companies. Still, we urge investors to be cautious as its NII growth tailwinds could moderate as the Fed slows down its rate hikes or pauses.

Also, sellers continue to resist attempts by buyers to force a decisive reversal of its downtrend bias since April 2022. ORCC’s near-term resistance and 50-week moving average (blue line) has continued to offer stiff resistance.

Despite that, ORCC’s NTM NII per share multiple of 7.8x remains priced at a discount against its peers’ median of 8.3x (according to S&P Cap IQ data). Hence, a deeper pullback should attract dip buyers to add more positions.

Rating: Hold (Reiterated).

Be the first to comment