Drs Producoes/E+ via Getty Images

Investment Thesis

Owens & Minor (NYSE:OMI) is a leading healthcare logistics company with a strong presence in the US and Europe. The company’s recent strategic initiatives, including the acquisition of Apria Healthcare and the Operating Model Realignment Program, are expected to improve profitability and cash flow in the coming years. The Patient Direct segment has been a strong performer for the company and is expected to continue to grow, driven by favorable industry tailwinds such as an aging population and increased demand for home healthcare. However, the global products division faces headwinds such as pricing pressure and declining volumes. The company’s valuation is currently reasonable compared to peers in the industry, based on traditional valuation metrics.

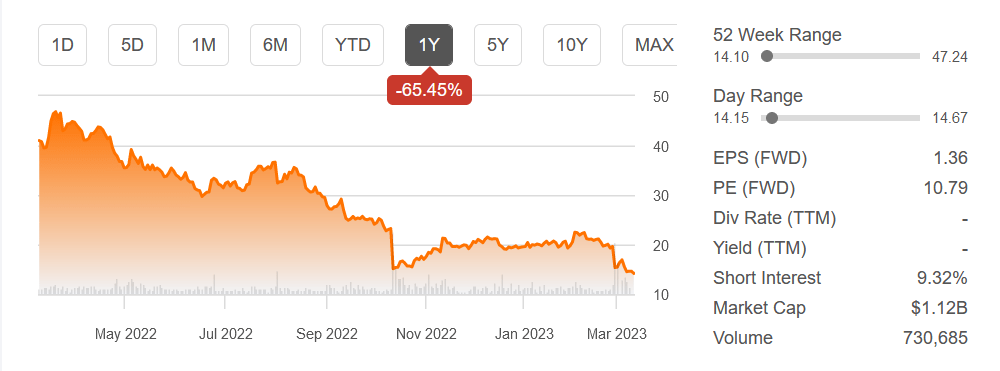

Company Share Price (Seeking Alpha)

Overall, Owens & Minor is a company with the potential for growth and improvement, but investors should be aware of the risks and uncertainties the company faces, including the ongoing COVID-19 pandemic and the competitive nature of the healthcare logistics industry. Taking into account the company’s current performance, growth prospects, and valuation, I will rate them a hold as the growth isn’t really there to justify it as a buy. It’s by no means a bad company, but a possible higher ROI could be found elsewhere.

Market Tailwinds

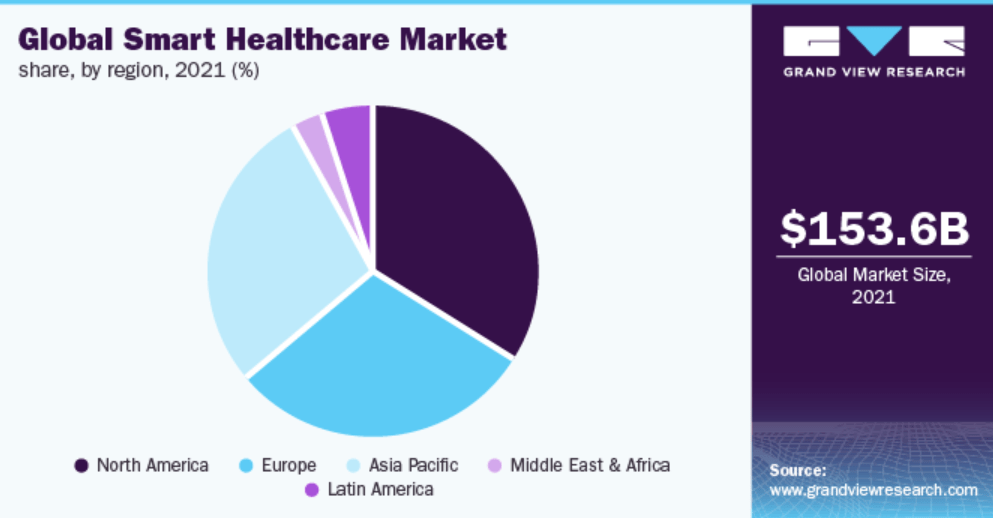

Owens & Minor operates in the healthcare industry, which is an essential sector that is expected to grow due to demographic trends, advances in medical technology, and increasing demand for healthcare services. The global healthcare market is projected to grow at a compound annual growth rate or CAGR of 6.7% from 2020 to 2025, driven by factors such as rising healthcare expenditure, increasing prevalence of chronic diseases, and growing awareness of preventive healthcare measures.

Market Outlook (Grand View Research)

There are several tailwinds that could benefit Owens & Minor in the future. Firstly, the aging population is expected to drive demand for medical products and services, especially for chronic disease management. Secondly, the COVID-19 pandemic has highlighted the importance of healthcare supply chain resilience, which could lead to increased investment in supply chain infrastructure and technology. Finally, advances in medical technology are likely to drive innovation and create new opportunities for healthcare companies.

However, there are also headwinds that investors should be aware of. One key risk is the ongoing trend of healthcare cost containment, which could lead to pricing pressures and lower profitability for healthcare companies. Additionally, regulatory changes and political uncertainty could impact the healthcare industry, especially in terms of pricing and reimbursement policies. Finally, technological disruption and the rise of new competitors could disrupt the healthcare market and pose a threat to established companies.

Analysts generally have a positive outlook on the healthcare industry, with many predicting strong growth over the coming years. According to a report by Grand View Research, the global healthcare market is expected to reach $11.9 trillion by 2028, with a CAGR of 6.9% from 2021 to 2028. The report also notes that increasing government initiatives to improve healthcare infrastructure and rising demand for remote patient monitoring services are expected to drive growth in the sector.

Revenue Breakdown

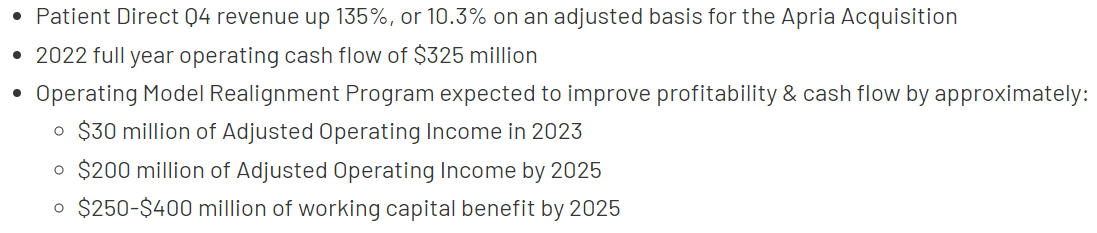

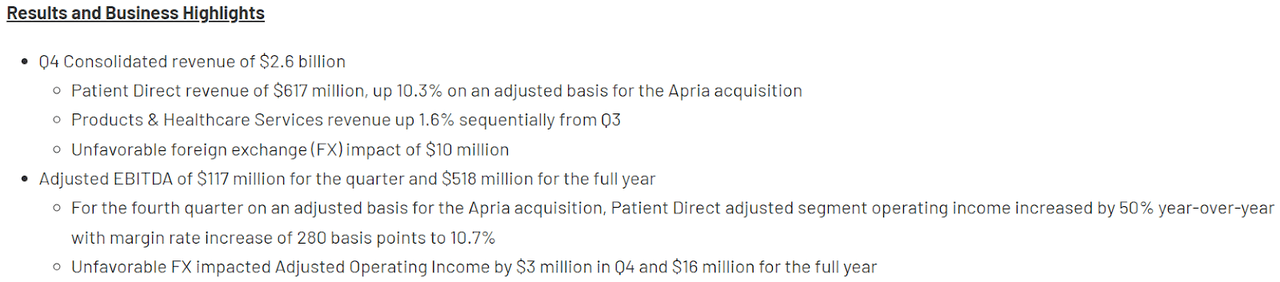

Owens & Minor, a leading healthcare logistics company, reported its Q4 2022 and full-year 2022 financial results. Consolidated revenue for Q4 was $2.6 billion, while Patient Direct revenue was $617 million, up 10.3% on an adjusted basis for the Apria acquisition. Products & Healthcare Services revenue also increased 1.6% sequentially from Q3. The company reduced its total debt by $61 million in Q4 and generated $87 million of operating cash flow, up 73% year-over-year. Additionally, Owens & Minor’s Supplier Diversity Award celebrated its 10th consecutive year, and Byram Healthcare was awarded Verywell Health’s “Best Overall Diabetic Supply Company” for the fourth year in a row.

Segment Highlight (Earnings Report)

Despite the strong results, Owens & Minor’s global products division faced volume decline, cost, and pricing headwinds in the fourth quarter. As a result, the company initiated an Operating Model Realignment Program to improve profitability and cash flow, with a dedicated team aiming to deliver approximately $30 million of Adjusted Operating Income in 2023 and approximately $200 million by 2025. Management believes this program will enhance the company’s quality of service, increase margins, and reduce debt while reinvesting in higher-growth and more profitable opportunities.

Company Highlights (Earnings Report)

Looking ahead, Owens & Minor has provided an outlook for 2023, with revenue expected to be in a range of $10.1 billion to $10.5 billion, Adjusted EBITDA in a range of $490 million to $550 million, and Adjusted EPS in a range of $1.15 to $1.65. Despite some headwinds facing the company, management remains optimistic about Owens & Minor’s future growth prospects.

Risks

Owens & Minor competes with a number of large, well-established companies, as well as smaller players. These competitors may have greater financial resources, better brand recognition, and broader product offerings, which could put Owens & Minor at a disadvantage.

Another risk facing the company is the potential for changes in government regulations or policies, particularly those related to healthcare. Any changes that result in decreased reimbursement rates for medical products and services, increased regulatory compliance requirements, or reduced funding for healthcare programs could negatively impact Owens & Minor’s financial performance.

Additionally, Owens & Minor is subject to fluctuations in demand for its products and services, which can be influenced by a number of factors, including changes in demographics, economic conditions, and advances in medical technology. The company’s financial performance may be adversely affected if demand for its products and services were to decline.

Finally, Owens & Minor is exposed to risks related to its supply chain and distribution network. The company relies on a number of suppliers and distributors to provide the products and services it offers, and any disruptions or delays in these networks could result in lost revenue, increased costs, and reduced profitability.

Valuation and Conclusion

Using the price-to-earnings (P/E) ratio, which compares a company’s stock price to its earnings per share, Owens & Minor Inc. has a forward P/E of 10.6x as of February 18, 2023. In comparison, the average forward P/E ratio for the healthcare distribution industry is around 18.1x. This suggests that Owens & Minor Inc. is undervalued relative to its peers.

Similarly, the company has a price-to-sales (P/S) ratio of 0.14x, while the industry average is around 0.34x. This suggests that Owens & Minor Inc. is trading at a discount compared to its peers based on sales.

However, it is important to note that valuation metrics should not be the only factor to consider when making investment decisions. Investors should also consider the company’s growth prospects, financial health, and industry trends, among other factors.

In conclusion, based on the undervaluation of Owens & Minor Inc. compared to its peers using traditional valuation metrics, the investment stance for the company could be considered a hold. The growth isn’t necessarily there to rate it a buy. A bigger ROI could possibly be found elsewhere.

Be the first to comment