Claude Laprise

We’ve seen a strong rally off lows for several names in the Gold Miners Index (GDX), and few names are more deserving of this share-price appreciation than Osisko Gold Royalties (NYSE:OR). This is because the company was significantly undervalued earlier this year despite seeing multiple positive developments across its partner’s assets and sporting one of the most attractive growth profiles sector-wide. The latter point is evidenced by a 4-year plan to grow attributable production towards 140,000 GEOs and what looks like a long-term potential to reach the 200,000 GEO mark.

While the most recent development may not impact its business model, it is significant, with the de-consolidation of Osisko Development (ODV) helping to clean up Osisko Gold Royalties (“Osisko”) financials and finally allowing it to secure the title of truly being a pure-play royalty/streaming model with no noise from ODEV leaking into its high-margin business. This is a massive upgrade from when it had Barkerville under its umbrella following its 2019 acquisition which made it a much messier story that wasn’t deserving of a premium multiple despite having royalty assets in Tier-1 jurisdictions. Let’s take a closer look at recent developments below:

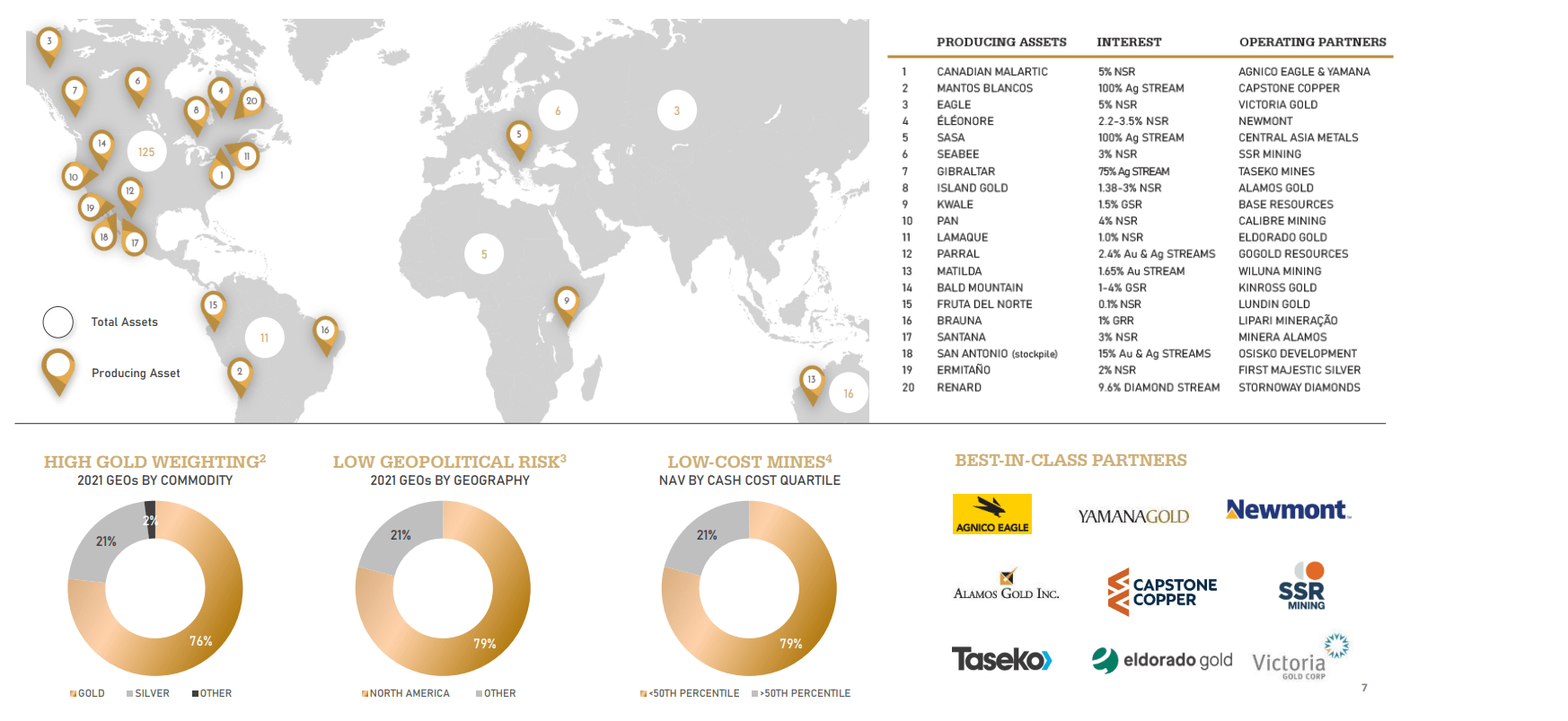

Osisko Gold Royalties – Portfolio, Revenue Weighting, Jurisdictional Profile (Company Filings, Author’s Chart)

All references to “Osisko” refer to Osisko Gold Royalties.

Q3 Results

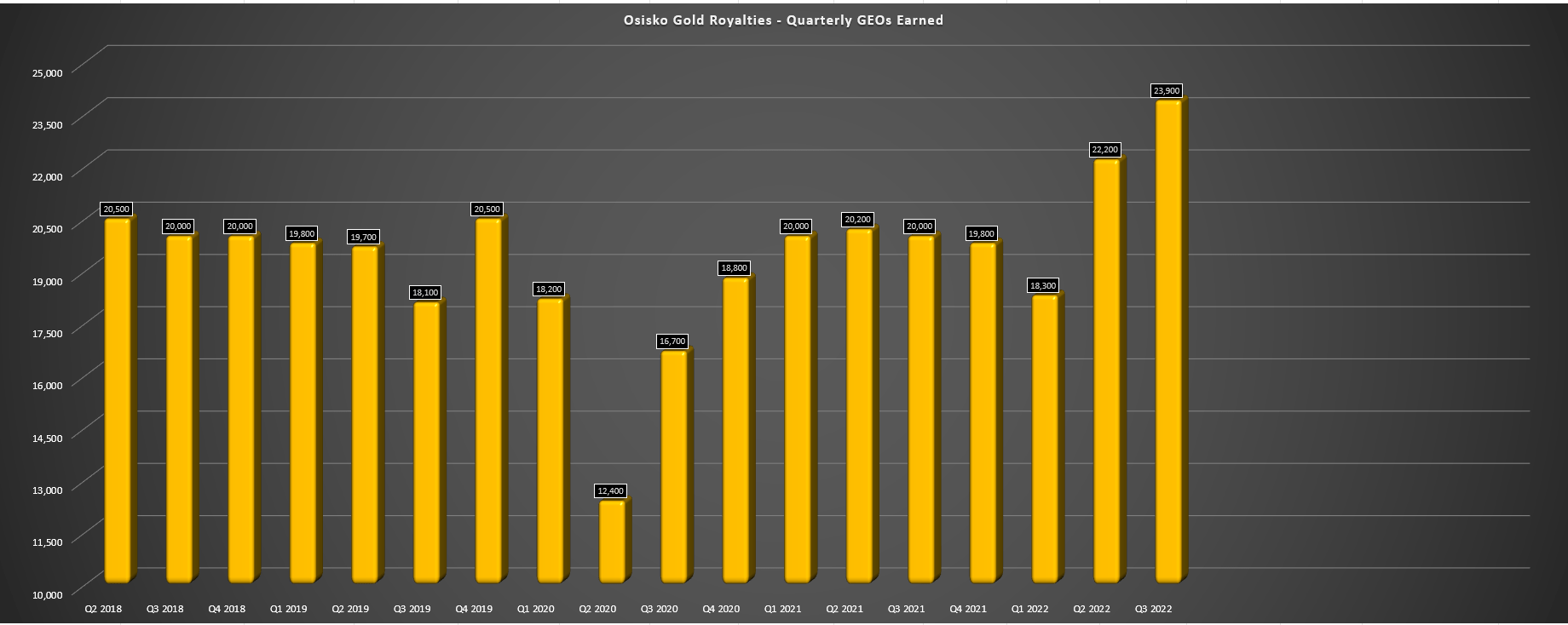

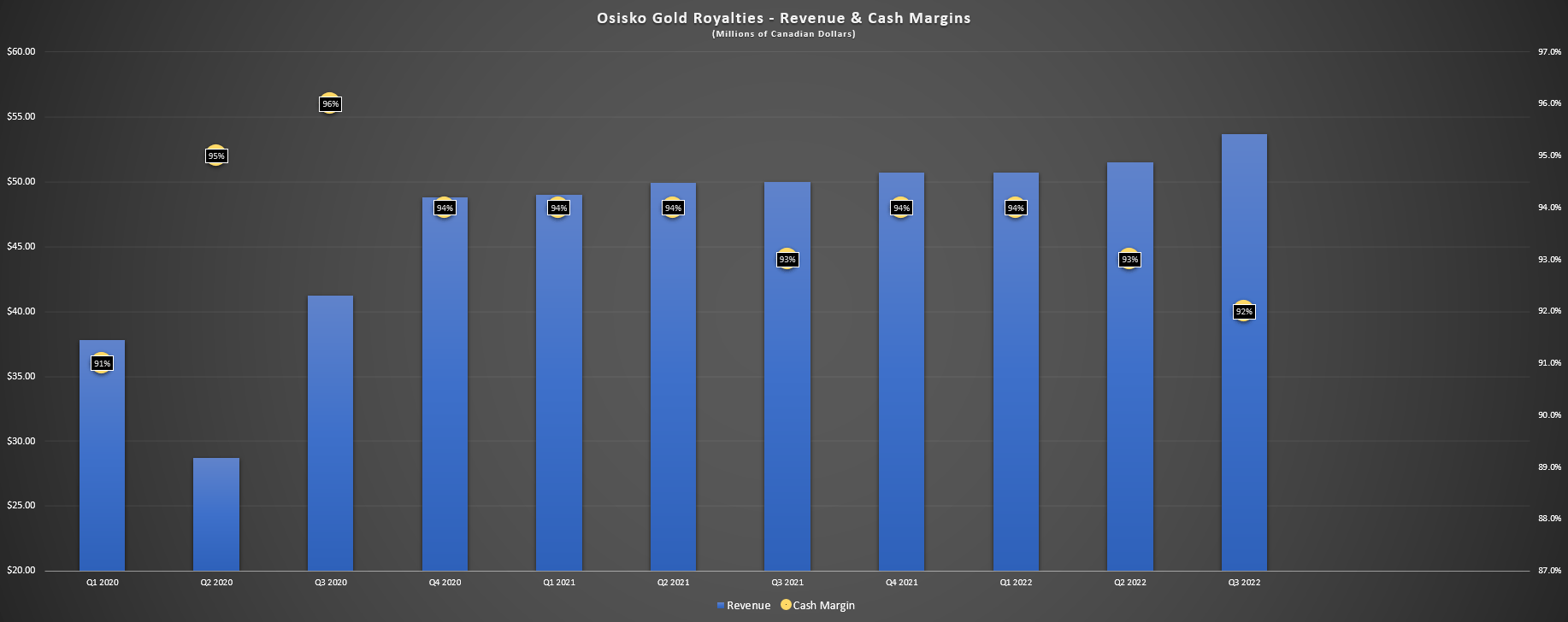

Osisko Gold Royalties reported its Q3 results last month with record attributable gold-equivalent ounce [GEO] production of 23,900 GEOs, strong cash margins (92%), and it enjoyed a 16% increase in cash flow year-over-year. This was despite a weaker-than-planned quarter from Eagle and a less favorable gold-silver ratio when it came to converting silver deliveries into GEOs. Based on what should be a much stronger quarter ahead for Eagle, the continued ramp-up at Mantos, and a solid finish to the year at Seabee. Still, even with lower metals prices and a softer quarter from a couple of key assets, Osisko reported revenue of C$53.7 million, a more than 7% increase year-over-year.

Osisko Gold Royalties – GEOs Earned (Company Filings, Author’s Chart)

Osisko Gold Royalties – Revenue & Cash Margins (Company Filings, Author’s Chart)

The major news in the quarter was that Osisko has de-consolidated Osisko Development finally from its financial statements, which has weighed on the stock given that it was the last milestone required for Osisko Gold Royalties to truly transition to being a pure-play royalty/streaming company. The de-consolidation occurred ahead of my expectations and is a huge positive, given that for new prospective investors not familiar with the story, this no longer looks like a low-margin and or money-losing royalty/streaming company due to the inclusion of Osisko Development’s mining exploration and development expenditures in its financial statements.

Based on ~67,400 GEOs earned year-to-date, Osisko is positioned to meet its FY2022 guidance of 90,000 to 95,000 GEOs, which would translate to double-digit growth year-over-year, with a partial benefit from the Renard Diamond Stream not being included last year. As we look out towards 2023 with the benefit of higher throughput from Mantos Blancos, what will hopefully be a less challenging year for the Eagle Mine and another strong year from Ermitano, we should see a further increase in attributable production, which will push Osisko Gold Royalties past the elusive 100,000 GEO mark which is a major accomplishment, especially with competition increasing in the sector over the past few years.

Recent Developments

While Osisko had a solid quarter from an attributable production standpoint with record quarterly GEOs earned, and it continued its opportunistic share buybacks (1.65 million shares repurchased year-to-date at an average price below US$10.30), we’ve also seen several positive developments across its existing royalty/streaming portfolio on its partner’s assets. There were far too many to go into detail on all of them, but a few highlights are as follows:

- Canadian Malartic: successful step-out drilling and infill drilling in the Odyssey internal zones, the western extension of East Gouldie, and the East Gouldie Extension, suggesting considerable resource growth at this key asset for Osisko (3-5% NSR).

- Mantos Blancos: Concentrator Debottlenecking Project is expected to be completed this quarter, and a further expansion is being looked at to potentially expand throughput by another 37% to 10.0 million tonnes per annum (100% Silver Stream).

- Eagle Mine: A maiden resource was announced on the Raven deposit (~1.07 million ounces of gold at 1.67 grams per tonne of gold), and the main producing Eagle Mine continues to increase along strike and at depth, suggesting a longer mine life at Eagle and the possibility of a larger production profile long-term with the addition of a second mine (5% NSR).

- Trixie Mine: Osisko Development continues to work on its surface decline to be completed in Q2 2023, and the ultimate goal is to increase mine production to 500 tonnes per day by Q1 2025, potentially increasing production to 90,000+ ounces per annum, assuming a 22 gram per tonne average mined grade (2.5% Gold Stream).

- Windfall: A positive Feasibility Study was completed that highlighted the average production of 306,000 ounces of gold per annum, but this assumes no positive grade reconciliation, which looks likely due to 60% grade outperformance vs. expected grades. Additionally, Osisko Mining announced a new discovery hitting 81 grams per tonne of gold over 3.5 meters in what could be a down-plunge extension of the Lynx 4 Zone (~2.15% NSR).

- Hermosa: South32 (OTCPK:SOUHY) released a positive Pre-Feasibility Study for the Taylor Deposit in Arizona. A Feasibility Study and final investment decision are expected by H2-2023. This is a massive operation with ~340,000 tonnes of zinc equivalent production in steady-state years, translating to a mine with $1.0+ billion in annual revenue (1% NSR).

Overall, these are very encouraging developments, and nearly all of this positive news has come from key assets in top-20 ranked jurisdictions, including Arizona, Quebec, Yukon, and Utah. There are several other notable developments that I have missed, such as new high-grade extensions to the Island Gold orebody (Ontario), world-class lithium intercepts at the Corvette Property in James Bay (Quebec), and continued exploration success at Upper Beaver (copper-gold project in Ontario) and Amalgamated Kirkland [AK] just to the west, which both benefit from existing infrastructure in the Kirkland Lake Camp where Macassa is currently in operation.

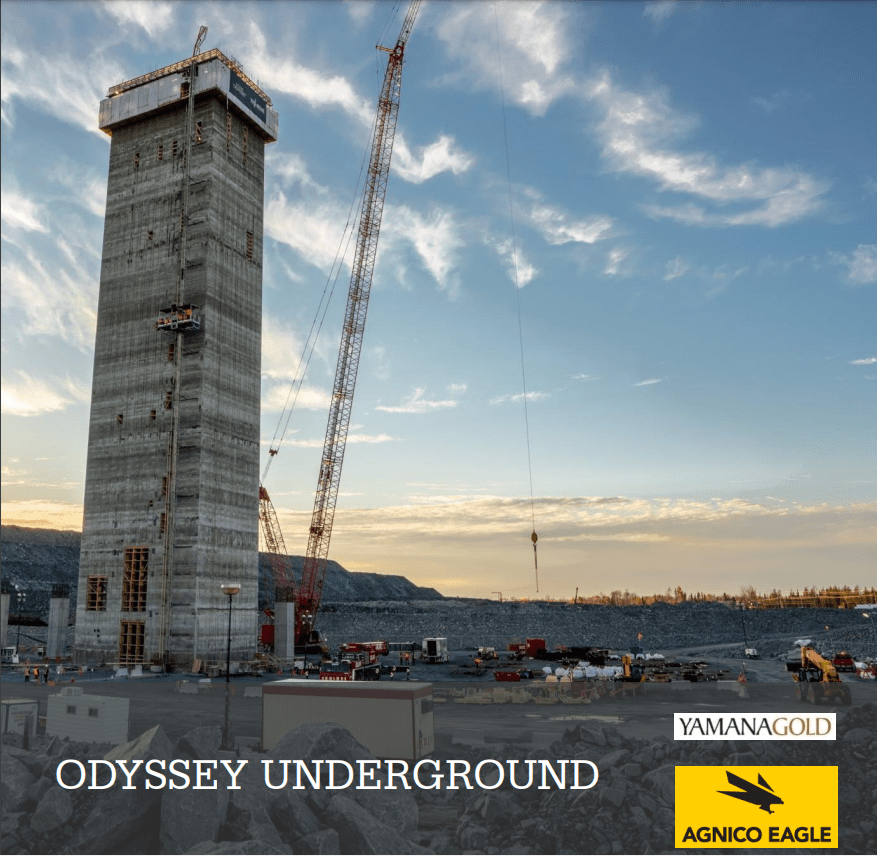

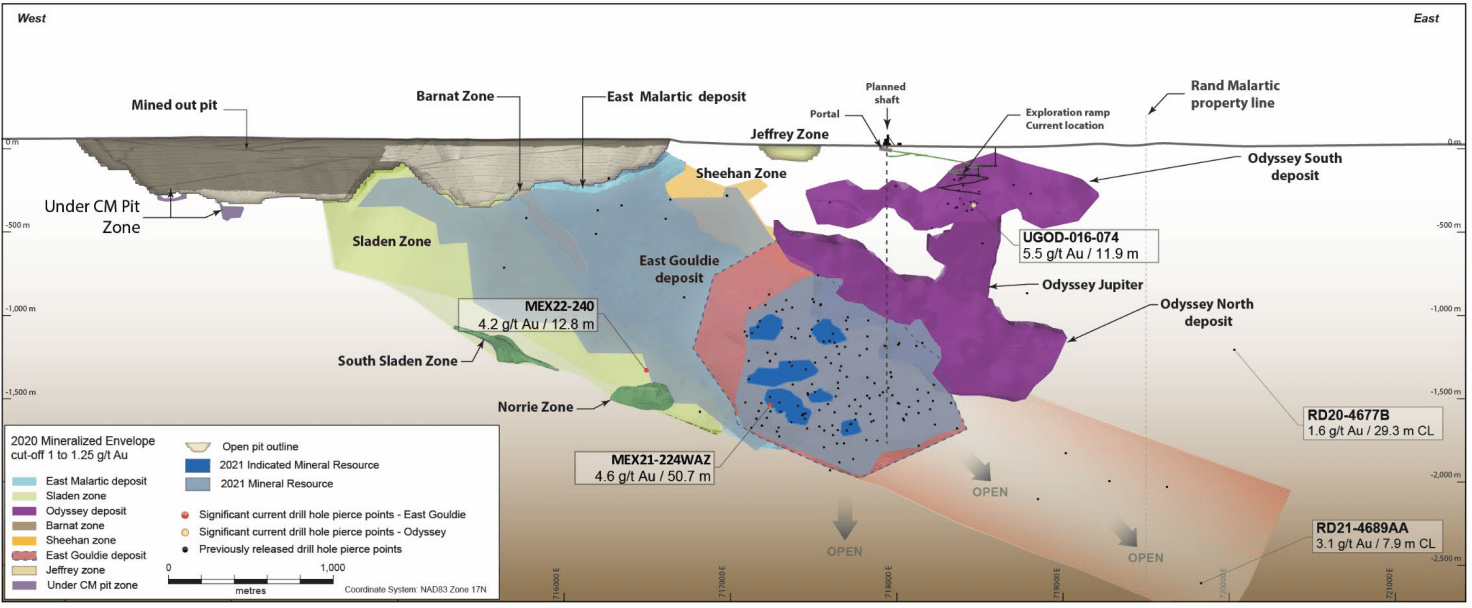

Perhaps the biggest news was the potential consolidation of the massive Canadian Malartic Mine by Agnico Eagle (AEM) with an offer to acquire Yamana’s Canadian assets. This not only would put this Tier-1 mine under the umbrella of one operator and the sector’s most aggressive driller on a dollar spent per ounce of production ratio, but there is no company with a better understanding of the geology and the balance sheet to support a future expansion than Agnico Eagle. The news is a huge plus for Osisko, which has a $0.40/tonne royalty on any material processed at the Canadian Malartic Mill and a 3-5% NSR on the Odyssey Project currently being developed by the Canadian Malartic Partnership.

Shaft Sinking Odyssey (Company Presentation)

For those unfamiliar, the Canadian Malartic Partnership is busy transitioning to underground (Odyssey Project) at Canadian Malartic after more than a decade of continuous open-pit mining. While this will lead to a ~30% lower production profile, this production profile will utilize less than one-third of the operation’s processing capacity (~61,000 tonnes per day). So, while production will dip to ~545,000 ounces from 2029-2039, there is considerable upside to this production profile by utilizing existing infrastructure. Hence, although Osisko’s attributable production from this asset will initially dip (~26,000 GEOs per annum vs. 30,000+ GEOs per annum previously), which will slightly offset some of its organic growth from other assets, I don’t expect this to be the case for long.

Canadian Malartic – Exploration Success (Agnico Company Presentation)

Assuming that Agnico Eagle processes an additional 15,000 tonnes per day (~5.5 million tonnes per annum) of material from mines outside of its royalty ground, this would result in an incremental $2.2 million in revenue per annum or ~1,200 GEOs. Meanwhile, if Agnico were to sink a second shaft to take advantage of the significant resource growth in the East Gouldie Extension and ~10,000 tonnes per day was coming from Osisko’s royalty ground, this would translate to an additional ~12,500 GEOs per annum attributable to Osisko. Plus, even under these assumptions (post-2029 opportunities), there would still be an additional 15,000 tonnes per day of excess capacity at the plant. Hence, we can see why Yamana has discussed this potentially being a 1.0 million ounce per annum producer.

If we combine the potential for ~1,200 GEOs (dependent on tonnes mined by Agnico at other deposits) from its processing agreement and an additional ~12,500 GEOs if Agnico sinks a second shaft to pull ounces forward in its mine plan, this could push Osisko’s annual attributable production at Malartic towards the 40,000 GEO mark post-2029. So, while the scaling down of the processing plant will be a minor drag short-term, this asset is truly a company-maker long-term. In fact, I’m amazed Osisko Gold Royalties hasn’t been approached with a takeover offer by a large royalty/streaming company, given the ability to tuck this world-class royalty asset into their portfolio while simultaneously adding considerable depth to their pipeline.

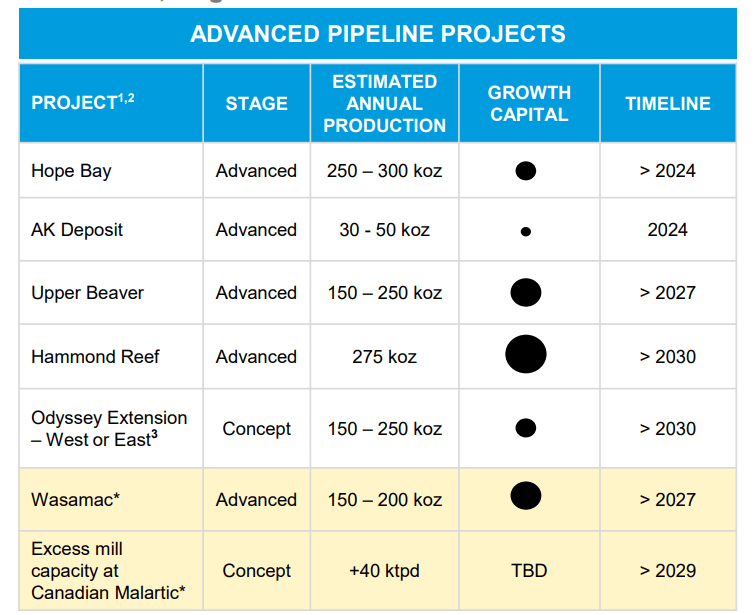

It’s important to note that these opportunities are not 2023, 2024, or 2025 opportunities; it’s a post-2029 opportunity, I would think, given that a second shaft would be a significant investment decision and a multi-year project that would take time to complete. Still, with Odyssey looking like it could ultimately grow into a 12.0+ million-ounce reserve base, it isn’t a stretch to think that Agnico might want to pull some of these ounces forward vs. mine it at a rate of ~550,000 ounces per annum. As the image above shows, Agnico Eagle has finally added this to its presentation, so it appears to be something that is at least being considered internally.

Agnico Eagle – Advanced Pipeline Projects (Company Presentation)

My assumptions of a 12,500 GEO per annum contribution to Osisko are based on a second shaft with a hoisting capacity of 15,000 tonnes per day, with at least 10,000 tonnes per day being mined from Osisko’s ground at an average grade of 2.5 grams per tonne gold, a 94.5% recovery rate, and an average royalty rate of 4.50%. This would translate to a ~275,000-ounce incremental increase in production for Agnico Eagle, or ~12,500 GEOs attributable to Osisko Gold Royalties.

In addition to positive developments on existing assets, Osisko has been busier in H1-2022, acquiring new royalties and streams, and it’s done an excellent job of waiting for a favorable market environment to put this money to work and exercising extreme discipline not to overpay just to ensure it secures future growth. Some of the recent deals include the following:

- A 0.60% NSR on the Cascabel Property in Ecuador with the world-class Alpala deposit (potential future contribution of 7,000+ GEOs per annum)

- A 2.0% NSR on the Pipeline West/Clipper Gold Project and a 0.5% royalty on the Tokop Gold Project in Nevada

- A 1.0% NSR on the Kandiole Project in Mali that currently has a million-ounce resource (potential future contribution of ~2,000 GEOs per annum in its early years, depending on throughput rate)

- A 0.125% to 1.50% NSR on the AntaKori Project in Peru and a right to buy back a 1% NSR from a third party on AntaKori claims.

- A 1.5% NSR on the Acocarire Project and a 1.25% NSR on the Horizonte Project (near the Salares Norte Mine), with both located in Chile.

- A 1.0% NSR on the Marimaca Project in Chile, a very attractive copper project with modest upfront capex (potential future contribution of ~2,500 GEOs per annum, assuming a higher throughput rate is approved)

Among this list, there are no deals that I dislike, and I am glad to see that Osisko did not chase any of these deals, paying a very attractive price to increase its royalty portfolio’s depth and adding some new jurisdictions and metals to diversify further. In fact, the company paid just over $80 million to secure all of these new royalties, and several look like they could head into production before the end of the decade.

It’s worth noting that its acquisition of the 1.0% NSR royalty on Marimaca was quite prescient, with the M&I resource growing by 98%, the company entering into a water option agreement to secure future water supply for Marimaca, and strong infill drilling results plus high-grade sulphide mineralization down-dip from the oxides at Marimaca. Given what could ultimately be a 25+ year mine life at this asset at a higher throughput rate than initially envisioned, this looks like a deal that will pay off very nicely for Osisko relative to its $15.5 million investment. Let’s take a closer look at Osisko’s pipeline:

A Royalty/Streaming Pipeline With Considerable Depth

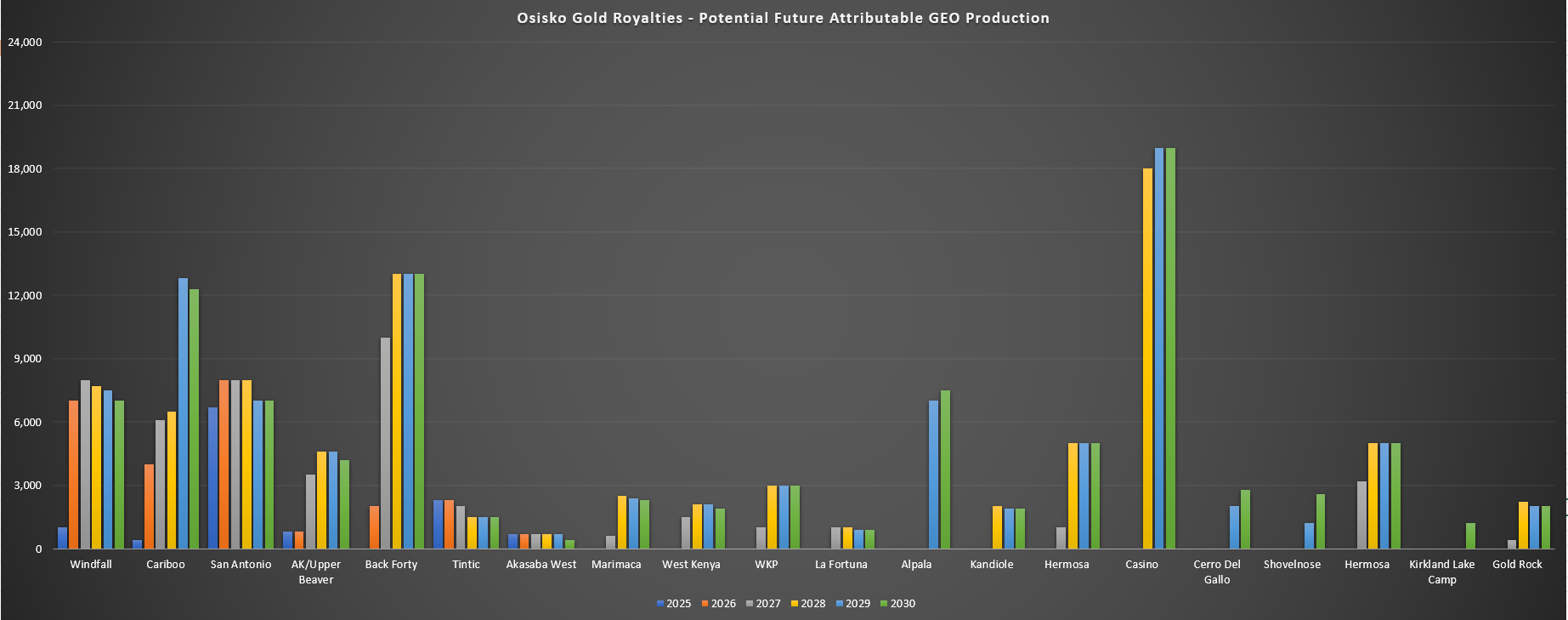

While Osisko Gold Royalties has royalties/streams on some of the best assets globally in Tier-1 jurisdictions (Island Gold, Malartic, and the CSA Mine, subject to the deal closing), its development portfolio also has considerable depth. This is evidenced by the fact that it has over 20 royalties/streams in the development stage or already producing, but that will ramp up considerably (outside of core producing assets). I have highlighted some of these assets in the below chart based on their first five years of production, and I have modeled conservatively where operators are juniors vs. mid-tiers, intermediates, or majors.

The most significant opportunities are Casino (~20,000 GEOs per annum), Back Forty (~10,000+ GEOs per annum), Windfall (~7,000 GEOs per annum), San Antonio (~7,000+ GEOs per annum), Alpala (~7,000 GEOs per annum), Hermosa (~5,000 GEOs per annum), Cariboo (~4,000+ GEOs per annum), and Upper Beaver/AK (~4,000 GEOs combined per annum). I have purposely excluded some assets that have a less clear sight to production, but if these assets are constructed, like Horne 5 (22,000+ GEOs per annum), White Pine (24,000+ GEOs per annum), Altar (12,000+ GEOs per annum), we would see an even more significant lift in attributable production.

Osisko Gold Royalties – Potential Future Attributable GEO Production (Company Filings, Author’s Chart & Estimates)

The above chart highlights just 20 of these potential contributors. In a perfect world where all of them came online, they could contribute upwards of 98,000 GEOs per annum based on their estimated production profiles. So, if we add this figure to a base production profile of 105,000+ ounces per annum from its main assets (already producing, organic growth, and near-term), Osisko could potentially become a 200,000+ GEO royalty/streamer by 2030. However, that makes four conservative assumptions:

- Osisko doesn’t acquire any more royalties on producing assets by 2030

- Malartic’s contribution doesn’t exceed 30,000 GEOs per annum

- No assets outside of those listed in the above chart begin production

- Osisko doesn’t acquire any more royalties/streams on development assets that begin production by 2030

I would argue that these are very conservative assumptions, given that Osisko has completed multiple deals this year and has over $600 million in liquidity with a growing cash flow profile. More importantly, the market for purchasing royalties/streams is the most favorable it’s been in years, given that explorers/developers are working with weak share prices, which makes capital raises less favorable, and debt is very expensive when it comes to financing new projects. Hence, I would not be surprised if Osisko remained quite active in building out its portfolio over the next 12-18 months, further augmenting what’s already a very robust pipeline.

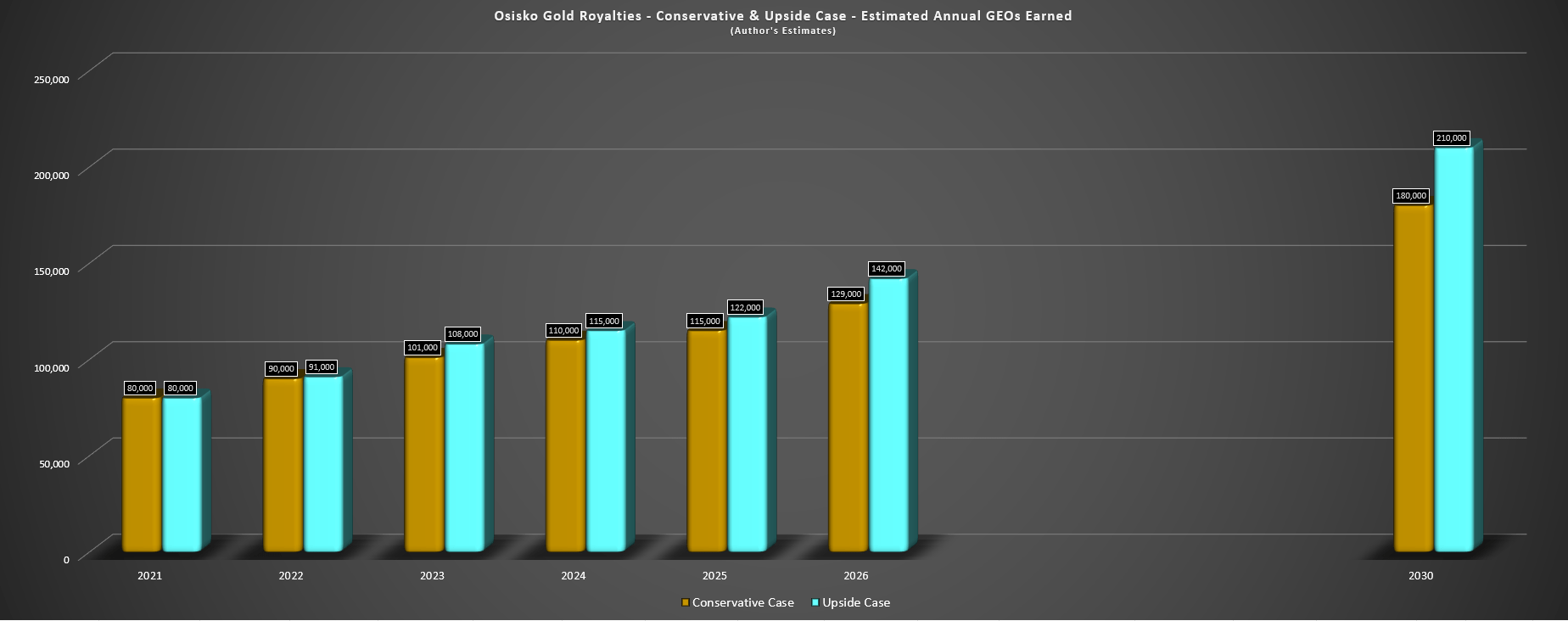

Even if we use a conservative $1,950/oz average gold price in 2030 and assume Osisko has an attributable production profile of 200,000 GEOs, this would translate to roughly $390 million in annual revenue and over $300 million in annual cash flow. Using a cash flow multiple of 24.0 to reflect its mostly Tier-1 jurisdictional profile could translate to a long-term fair value for the stock of ~$6.9 billion or a fair value of ~$36.00 per share (assuming 192 million shares outstanding). Obviously, this is a very conceptual long-term target, and much can happen in eight years. Still, the point is to show just how impressive Osisko’s pipeline is in a base case scenario, assuming that two-thirds of its more likely to be advanced development assets move into production, and it only does a few new deals to bolster its production profile.

Osisko Gold Royalties – Conservative & Upside Case of Estimated Annual GEOs Earned (Company Filings, Author’s Chart & Estimates)

The ~200,000 GEO potential for 2030 makes the assumption that several assets in its development pipeline come online and that Osisko adds just 20,000 GEOs per annum in additional production through new acquisitions.

Valuation

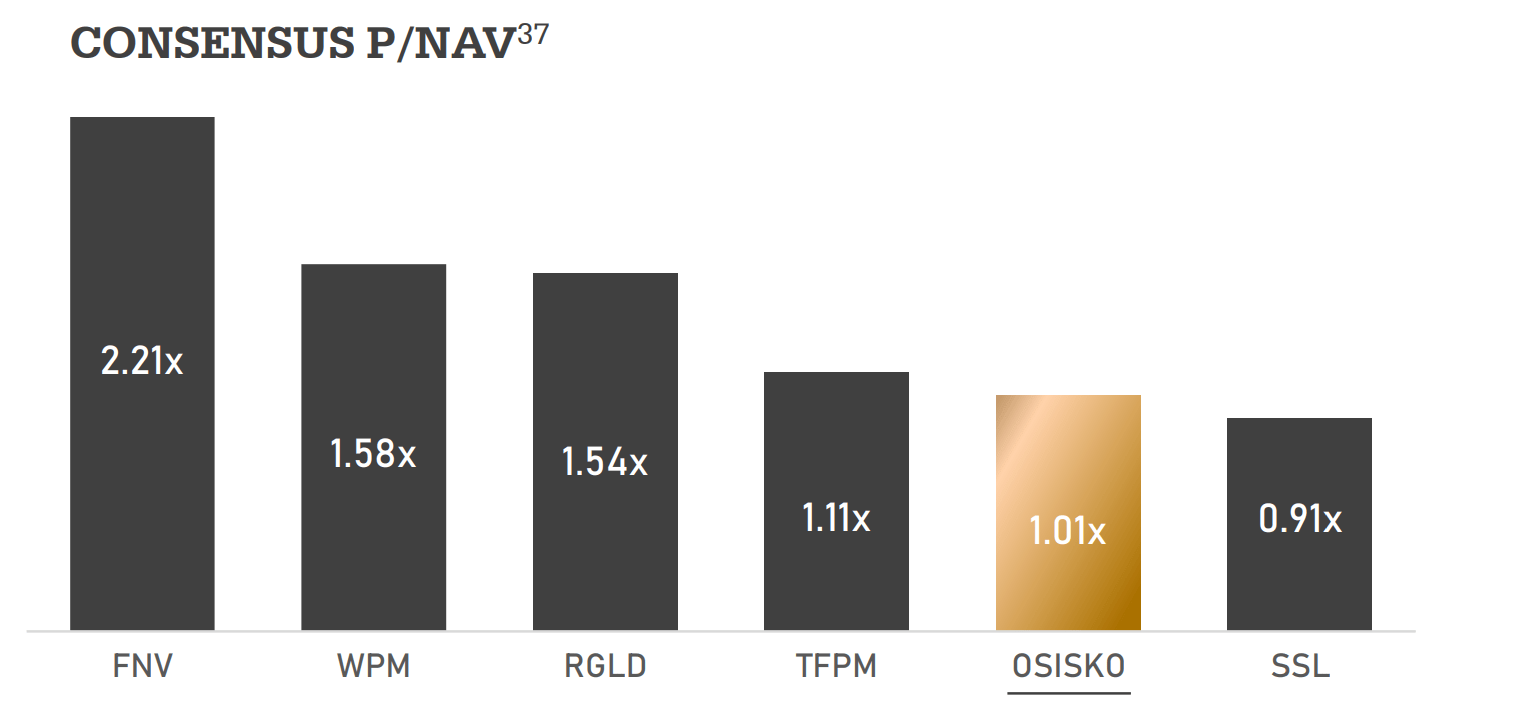

Based on ~185 million fully-diluted shares and a share price of US$12.15, Osisko trades at a market cap of ~$2.23 billion, which leaves the stock trading at 1.0x P/NAV vs. an estimated net asset value of ~$2.24 billion. This is a significant discount to larger royalty/streamers in the sector (which is partially justified due to Osisko’s smaller scale) but Osisko should benefit from a considerable re-rating as it begins to move up the ranks. Based on what I believe to be a reasonable multiple of 1.50x P/NAV to reflect its superior jurisdictional profile and the recent shift to a pure-play royalty/streaming model offset by the weaker market sentiment that has put pressure on valuations, I see a fair value for the stock of US$18.15 per share.

Consensus P/NAV vs. Peers (Company Presentation)

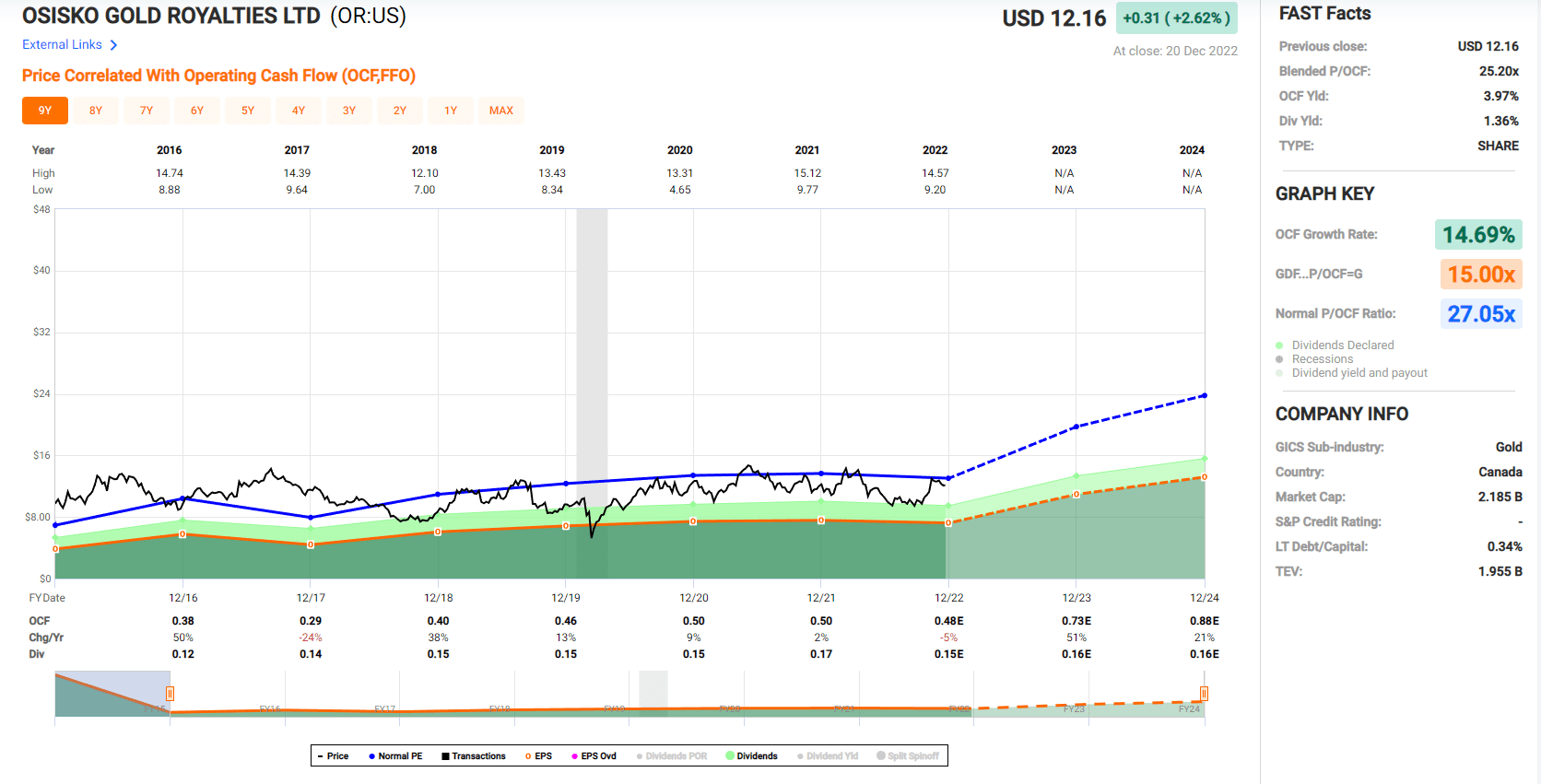

Meanwhile, from a cash flow standpoint, OR also looks heavily undervalued based on FY2023 cash flow per share estimates of $0.73. This leaves Osisko trading at just ~16.6 forward cash flow estimates vs. a historical multiple of 26.1x cash flow during a period where it was out of favor due to its non-pure-play model. However, new CEO Sandeep Singh has made great progress in simplifying the story since then. In addition, I would argue that the company’s portfolio has never looked better, and its recent acquisitions continue to stack up great vs. peers from a price-paid standpoint. Hence, I don’t see any reason Osisko can’t command a similar or even higher cash flow multiple. Still, even using a more relaxed multiple of 25.0 (4% discount to long-term average) would translate to a fair value of US$18.25 per share.

Osisko Gold Royalties – Historical Cash Flow Multiple (FASTGraphs.com)

In summary, Osisko looks to have a nearly 50% upside to fair value no matter how you slice it, but this assumes that metals prices see no upside over the next year, and it assumes that there are no major discoveries on its projects that boost its net asset value. Given that we should see another year of more than 1.4 million meters drilled across its royalty/streaming properties in 2023, I would certainly not rule out another significant discovery, and we already saw several major developments this year, including the East Gouldie Extension, the Island West high-grade extension, the discovery of Golden Bear and a high-grade extension to Lynx 4, and the announcement of a maiden resource at Raven, with the latter development having the potential to add long-term upside to the production profile at the Dublin Gulch Property (Yukon).

Summary

The Osisko Gold Royalties investment thesis has never been stronger than it has today. And with a little luck and a lot of exploration dollars committed to its partner’s properties, the future for its royalty/streaming assets continues to be very bright. However, the major development is that the potential impediments to a significant re-rating are finally off the stock after the de-consolidation of Osisko Development and a massive pipeline of assets that will reduce the company’s concentration to its top three assets (Canadian Malartic, Mantos, Eagle).

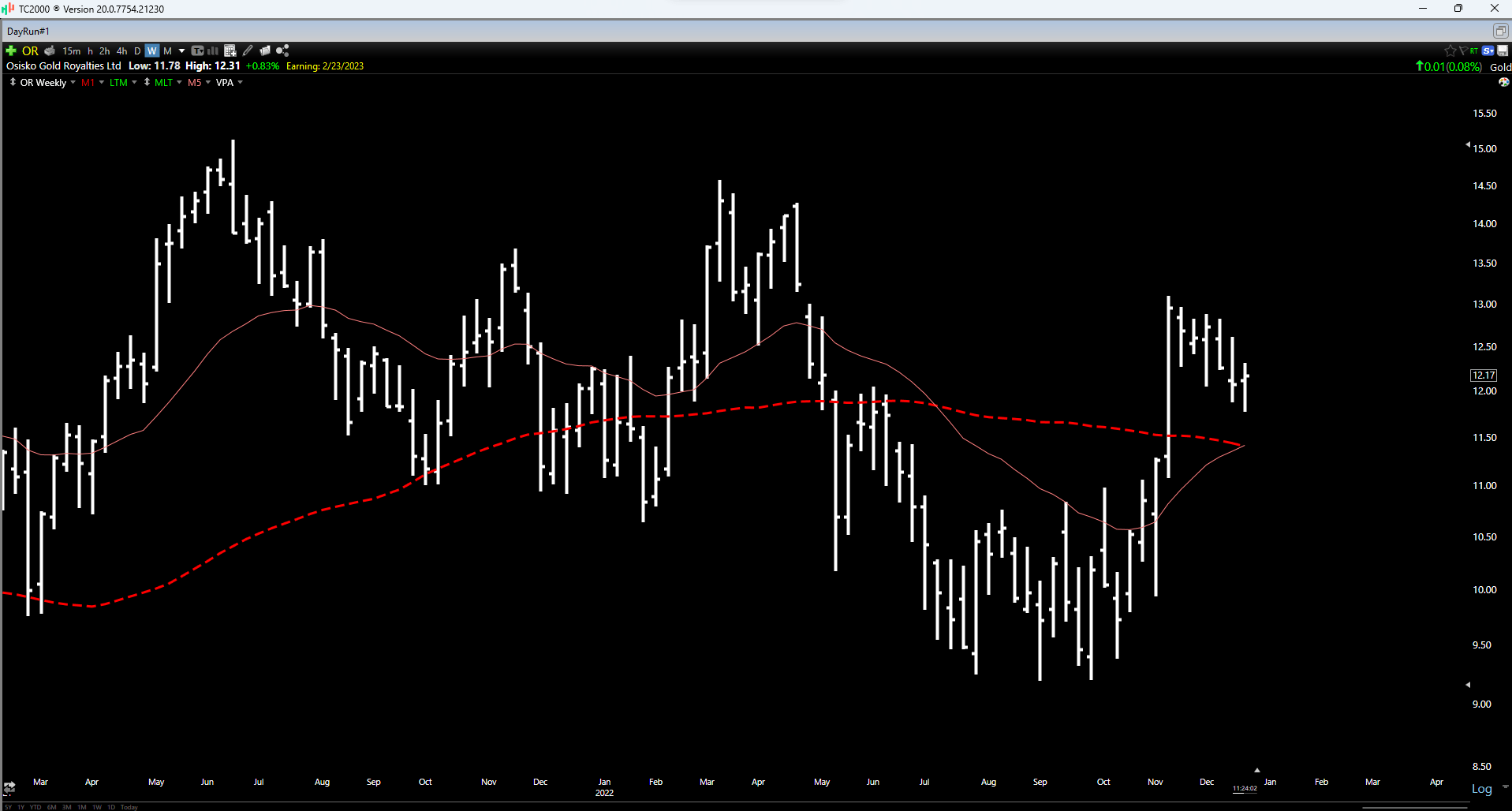

OR Weekly Chart (TC2000.com)

The latter diversification point cannot be overstated, as we saw recently, with Franco-Nevada (FNV) set for a softer Q4 with its largest Cobre Panama asset temporarily offline due to a disagreement between First Quantum (OTCPK:FQVLF) and the Panamanian government. Meanwhile, from a technical standpoint, Osisko has momentum at its back after its recent rally, reclaiming its key weekly moving averages, which increases the probability of dips being bought. Given that momentum and value can be a powerful combination, I would not be surprised to see higher prices over the next 12 months. So, with a ~50% upside to fair value and considerable growth on deck, any sharp pullbacks should provide buying opportunities.

Be the first to comment