Different_Brian/iStock Editorial via Getty Images

Dear readers,

In this article, I’m updating the case on Oshkosh (NYSE:OSK). The company is an infrastructure, truck, and machinery play that I wrote about months ago, then updated a few months back in February of 2022. Since that article, this has happened to the company’s overall share price.

Oshkosh Article (OSK IR)

Oshkosh has severely underperformed the market, in part due to its operational segments, and in another part due to its exposures and the overall market developments here. That is not even mentioning input inflation and other factors that impact OSK here.

Let’s look at what we got here as of mid-2022.

Oshkosh – Updating on the company

When thinking about Oshkosh, I’ve previously said that I often think about Caterpillar (CAT) – this is still very much the case.

Why?

Both companies are active in the segment of heavy-duty vehicles, and neither company is your “standard” manufacturer of these vehicles. They’re both extremely specialized, emphasizing customized solutions for very specific segments.

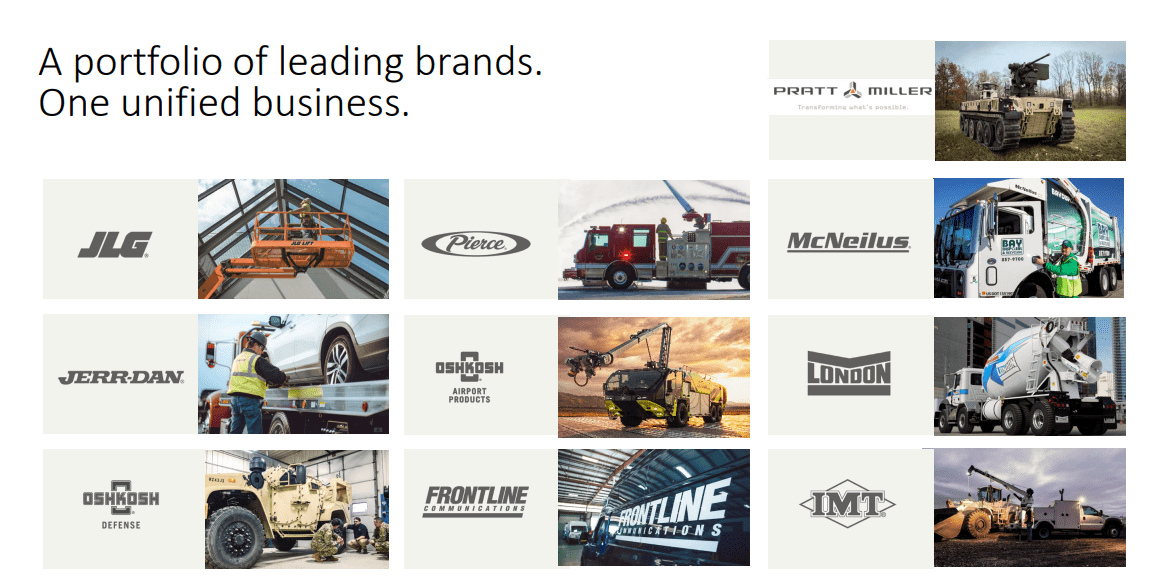

The company operates under several brands, most of them very well-known in their respective fields, but completely unknown to people outside of these fields. You might not have heard of any of them unless you work in the sector or have noted them, but let me assure you that they are very relevant.

Oshkosh Portfolio (OSK IR)

The company’s operations are split into the following segments.

- Access Equipment, focusing on telehandlers, cranes, boom lifts, lifting equipment and other similar products. The company operates, amongst others, under the brands of JLG and SkyTrak brands.

- Defense, focusing on the development and construction of defense vehicles. The company is a global leader in the design of best-in-class military vehicles, but also delivery vehicles.

- Fire & Emergency, focusing on the construction of custom fire engines.

- Commercial, which holds machines focused on concrete, refuse, and similar segments.

As I mentioned in my initial piece, Oshkosh from a high level depends on continued orders and flows from things like military budgets, the housing and infrastructure market, state and municipal buying trends for replacement orders of older fleets, and the like.

The company has appealing overall fundamentals, carries an investment-grade credit rating, and a market cap of nearly $8B at 2021 valuations and results. Company debt is extremely limited at 20% long-term debt/cap, and the company’s dividend coverage is stellar, at less than 30% payout ratio, bringing it to one of the lowest in the industry.

As of the latest valuation, that market cap is down to $5.2B – but the debt is still at 16.7% to capital, and the dividend is as well-covered as it once was, bumped back in October to $0.37 quarterly, which comes to $1.48 annual, or a yield just south of 2% at this particular time.

As I probably don’t need to tell you, things haven’t exactly gone swimmingly in the company’s main segments, including housing and infrastructure. The market is in upheaval, and this has cut OSK’s normal premium in terms of P/E for the past few years, to less than 15X P/E. Remember, the company had contributors arguing for why a 25X P/E was justified for OSK.

Newsflash – the market now disagrees with this.

OSK Valuation (F.A.S.T Graphs)

Recent results, despite this, are still good. The company’s outlook is supported by fundamental upsides, including an average fleet range well above the norm, which indicates a necessity of replacing older machines with newer ones. The company’s backlog supports this as well.

Oshkosh IR (Oshkosh IR)

There are also several, non-typical sector upsides, such as a growing presence in the growing NA agricultural market, new segments like EV, as well as growing into global markets where Oshkosh has previously had only marginal representation.

The increasing geopolitical uncertainty is of course also a massive upside to the company’s near-term future, with combat vehicles such as weapon systems, CATVs, and optionally-manned and robotic combat vehicles. Remember also that OSK has the USPS contract for 165,000 purpose-built EVs with a large aftermarket opportunity. OSK also remains the world’s largest producer of fire apparatus and is the largest dealer with the largest service network in all of North America. The company’s dealer network is by far best-in-class, with a 42% dealer service location growth in the last 5 years.

The company is also a leader in recycling & refuse.

OSK IR (OSK IR)

The company has seen earnings stability and expects the market to grow by 5% CAGR for the next 5 years. And this is despite that forecast excluding all residential construction segments. Infrastructure will be another driver with $110B allocated over the next 5 years, and the company’s increased focus on lifecycle parts and services will increase earnings as well.

The company is streamlining manufacturing and its internal processes in order to simplify things, using automation to a higher degree to get operational efficiency to higher degrees than before. The company has delivered fiscal targets for 2025E, with over $10B in annual sales, a 10%+ OM, an EPS of $13 on the high end, and an ROIC of up to 23%. The company also has a very clear capital allocation strategy, where dividends are at the bottom of the totem pole, with 10% of cash returned. The remaining cash is being focused on organic, accreditive investments, M&As, and repurchases of shares.

Oshkosh remains a powerful company in non-optional/mission-critical applications. While customers can wait for some time before replacing their assets, there comes a time when replacements have to be made. It’s my view that this is occurring for the company, with the current customer fleet age reaching critical levels, and the company’s order books for the next few years filling up.

This gives potential justification for a bump in the company’s stance.

Oshkosh – The valuation

Oshkosh has previously traded at a far too high valuation, which I’ve highlighted in my previous articles on the company. However, since the middle of 2021, the company has declined from a P/E of over 25X to now less than 15X. That’s a mighty decline, which completely changes the company’s overall upside because in part of the reverse potential based on post-2022E earnings growth.

For 2022, the company is still expected to see only very moderate EPS development. Expectations are for it to be negative due to input costs and unfavorable timing – but beyond this, we’re forecasting growth of 54% and 15% respectively until 2024E. This comes at a historical analyst accuracy of over 67%, with a 50% beat potential (by more than 10% on a 1-year basis).

In layman’s terms, this company is good at doing better than people expect it to do. This brings a fair bit of certainty to these assumptions right here.

OSK Upside (F.A.S.T Graphs)

Based on such EPS growth assumptions, this company could potentially deliver some absolutely stellar levels of outperformance. Before, investing in Oshkosh could have delivered maybe 5-11% annually – at optimistic expectations or so.

Today, that upside is far higher. Following a 30% drop, a realistic sort of upside for OSK is no less than 28% annually, to a 2024E 15X P/E of $145/share, or an annual RoR of almost 86%.

Those are respectable returns, and returns I’m very happy looking closer at. I wrote the following in my initial OSK article.

To me, the current valuation thesis for Oshkosh is quite simple. Any, and I do mean any, deviation from this positive thesis and downturn to more historically accurate multiples will result in sub-par or close to negative returns at these multiples. If you invest here, you might get an annual RoR of 10% in a very positive scenario. You might.

Obviously, this is now massively changed. I said you should buy OSK cheaply. It is now a cheap business trading at, for the moment, under 15X P/E. The upside here is significant.

S&P Global gives the company a price target range of $84 on the low end and $126 on the high end. Note that even on the low end, the company’s current share price is well below this. Based on a 1-year 35% drop, the company is now more attractive than in a long time, and the average PT from S&P Global here is currently $109/share. I would concur with this being an accurate and appealing sort of share price target.

18 analysts following the company have 10 at either a “BUY” or an “outperform”, with 7 still wanting to see where things are going and at a “Hold”. 1 is at a Sell/Underperform.

I personally believe that the company has dropped enough, but at the same time, it’s near-impossible to say at which point the market stops dropping, given everything that is currently going on.

Still, at this point, I think it’s fair to shift my target.

OSK is now a “BUY”. The upside is well above 20% here annually, for the next few years.

Thesis

The current Oshkosh thesis is as follows:

- This is a very high-quality business with great fundamentals and excellent management in an appealing, if cyclical, set of segments.

- In my first article, I said that this company’s cyclical characteristics will bring this company back down to fair value. That has now happened, and in my view, fair value has turned to “undervalued.”

- Due to this, I call this company a “BUY” at this valuation.

Remember, I’m all about:

1. Buying undervalued – even if that undervaluation is slight, and not mind-numbingly massive – companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn’t go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

This process has allowed me to triple my net worth in less than 7 years – and that is all I intend to continue doing (even if I don’t expect the same rates of return for the next few years).

If you’re interested in significantly higher returns, then I’m probably not for you. If you’re interested in 10% yields, I’m not for you either.

If you however want to grow your money conservatively, safely, and harvest well-covered dividends while doing so, and your time frame is 5-30 years, then I might be for you.

These are my overall criteria, and how the company fulfills them.

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company has realistic upside based on earnings growth or multiple expansion/reversion.

Be the first to comment