Khosrork

It is hardly a secret that one of the biggest problems facing many American families today is inflation. The inflation that we are seeing today is at the highest level that it has been in more than forty years and it has unfortunately been concentrated in food and energy, which are necessities for life. Thus, it has been straining the budgets of many families and has even forced numerous people to take on second jobs simply to obtain the money that they need to survive.

Fortunately, as investors, we have other methods that we can employ to obtain the extra income that we need to maintain our lifestyles. One of the best of these options is to purchase shares of a closed-end fund that specializes in the generation of income. These funds provide investors with an easy way to obtain a professionally-managed portfolio of assets that can in many cases deliver a higher yield than pretty much anything else in the market.

In this article, we will discuss the RiverNorth/DoubleLine Strategic Opportunity Fund, Inc. (OPP), which is one fund that falls into this category. This fund is admittedly not as well-known as some other funds, but its 19.76% current yield is more than enough to turn anyone’s head. While this yield may be appealing, generally speaking, a yield this high is usually a sign that the market expects a cut so we will need to pay extra attention to the fund’s finances during our analysis. Let us begin discussing whether or not this fund could be a good addition to a portfolio today.

About The Fund

According to the fund’s webpage, the RiverNorth/DoubleLine Strategic Opportunity Fund, Inc. has the stated objective of providing its investors with a high level of current income and overall total return. This is hardly unusual for a closed-end fund as many of them have the provision of current income as one of their goals. This is something that these funds do as a way to set themselves apart from regular open-end mutual funds. The provision of current income is especially common as an objective for fixed-income funds such as this one. This is because fixed-income securities provide the overwhelming majority of their investment return in the form of current income because their potential for capital gains is limited. Admittedly, until this year bonds were in something of a bull market for many years, but that was due to interest rates declining since the early 1980s.

A very important tenet of bond investing is that bond prices are inversely correlated with interest rates. Thus, when interest rates rise, bond prices decline, and vice versa. This is because newly-issued bonds will have an interest rate that corresponds to the interest rate in the market. In a rising rate environment, these newly-issued bonds will thus have a higher yield than an existing bond so nobody will buy the existing bond. Thus, the price of existing bonds will decline until they have the same yield-to-maturity as a newly-issued bond with the same characteristics.

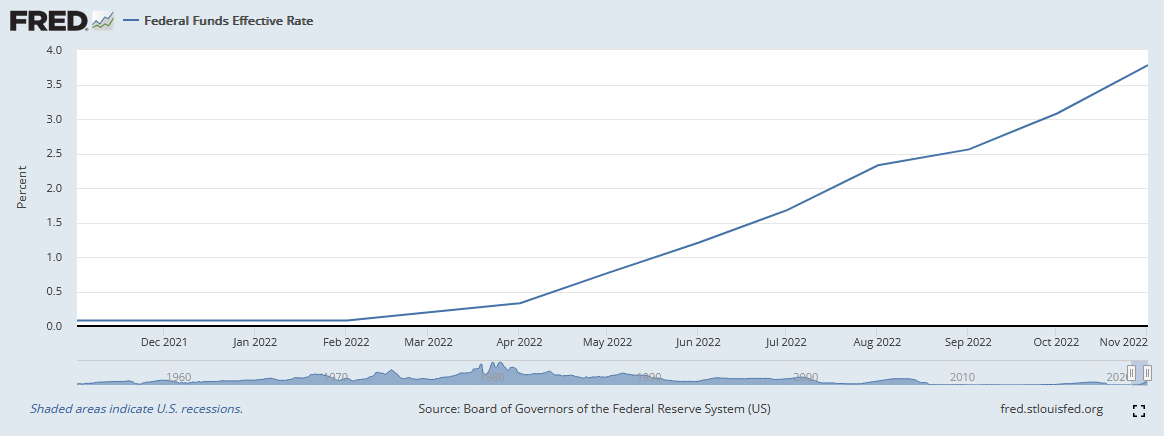

Over most of 2022, we have seen the Federal Reserve raise interest rates in an effort to combat the raging inflation that is devastating the economy. Back in February 2022, the federal funds rate sat at 0.08% but it has risen to 3.78% today:

Federal Reserve Bank of St. Louis

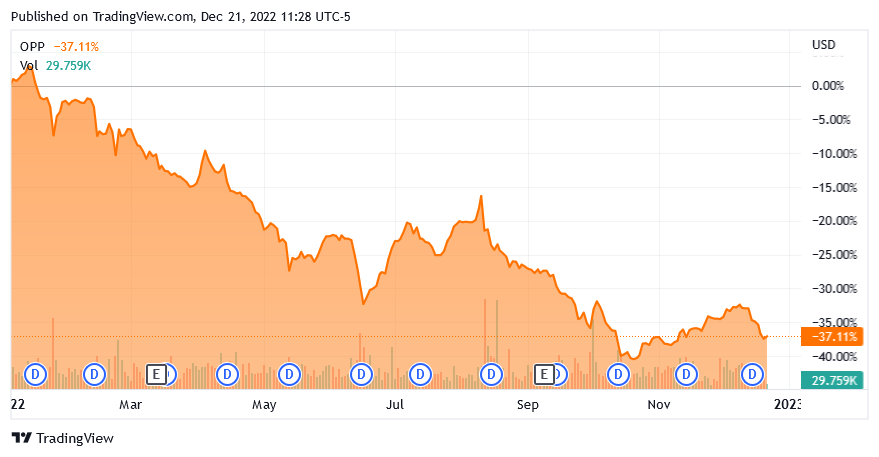

This is the big reason why we have seen bond prices decline over the past year. Indeed, the Bloomberg U.S. Aggregate Bond Index (AGG) is down 13.18% year-to-date. As the RiverNorth/DoubleLine Strategic Opportunity Fund, Inc. invests in fixed-income securities, it has been impacted by this as well. The fund is down 37.11% year-to-date:

Seeking Alpha

There are a few reasons why the fund has declined much more than the corresponding index, which we will discuss throughout the remainder of this article.

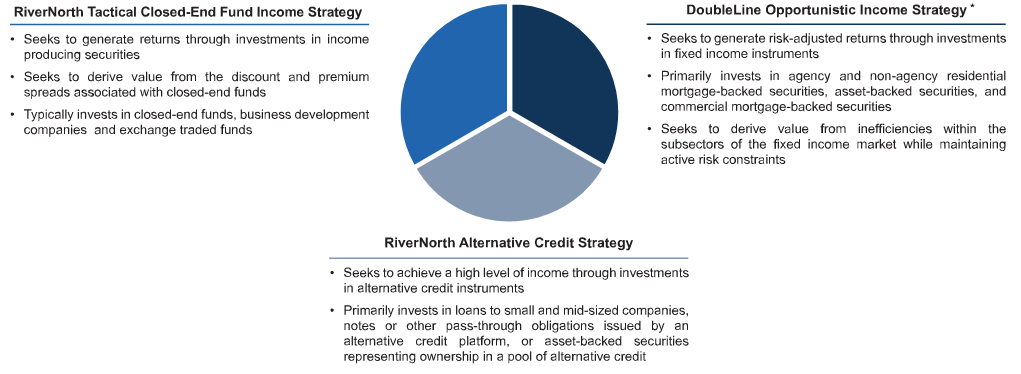

The fund uses something of a unique strategy for a closed-end fund as it does not invest solely in fixed-income securities. Instead, the fund essentially maintains three silos: Tactical Closed-End Fund Income Strategy, Alternative Credit Strategy, and Opportunistic Income Strategy:

RiverNorth

As we can see, the RiverNorth/DoubleLine Strategic Opportunity Fund, Inc. uses two fund managers for its portfolio, which explains the name. This is not necessarily a negative thing, though, as RiverNorth states that it does not have a good team to manage the Opportunistic Income Strategy portion of the portfolio. Thus, the better management provided by DoubleLine will likely provide an overall better return for investors than if it was managed entirely by RiverNorth.

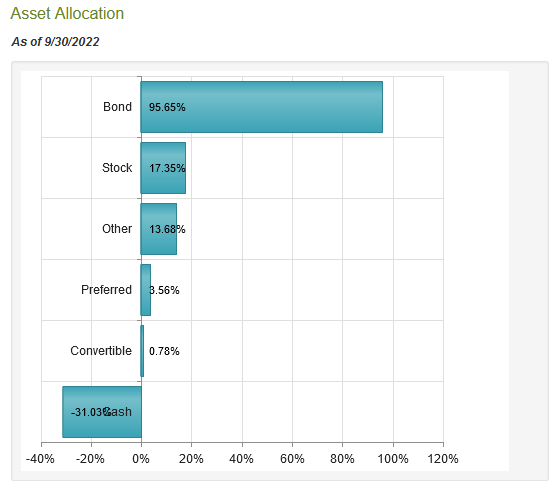

The most interesting thing here is that part of the fund is invested in other closed-end funds and business development companies. Business development companies are basically just a specialized kind of closed-end fund though so we can consider them all to be the same thing. This portion of the fund may step outside the fixed-income arena since some closed-end funds invest in common equities. In fact, this is the case as 17.35% of the portfolio is currently invested in common stock:

CEF Connect

This could provide some advantages to investors since the common stock has much more potential for capital gains than fixed-income securities. After all, interest rates can only go to 0%, limiting the potential for bond appreciation past that cap, whereas common stocks can go to pretty much any level since they are directly linked to the growth and prosperity of the underlying company. Thus, this could allow the fund to generate returns in excess of the income that the fund generates from its fixed-income portfolio. With that said, we can still see that the common stock allocation is fairly low so realistically the fund is generally making its profits from the money that it receives from the fixed-income assets held by it or from the closed-end funds in which it is invested.

The fund’s alternative credit strategies silo is also interesting, particularly considering that interest rates are expected to rise further as we enter 2023. This is because this part of the fund invests in bank loans as opposed to traditional bonds. These are what are sometimes considered “leveraged loans” as they are bank loans made to companies that already have a considerable amount of debt. Thus, they are riskier than traditional investment-grade bonds and so carry higher yields. This higher risk is frequently offset by the loan being backed by some form of collateral that can be seized to pay off the loan in the event of a default. By far the most important thing though is that these loans have floating interest rates. Thus, the yield increases with interest rates. This should help protect the value of these loans in a rising rate environment as well as cause the fund’s income to steadily increase. That is always nice since the fund’s ability to generate income is critical to its ability to pay out its distributions.

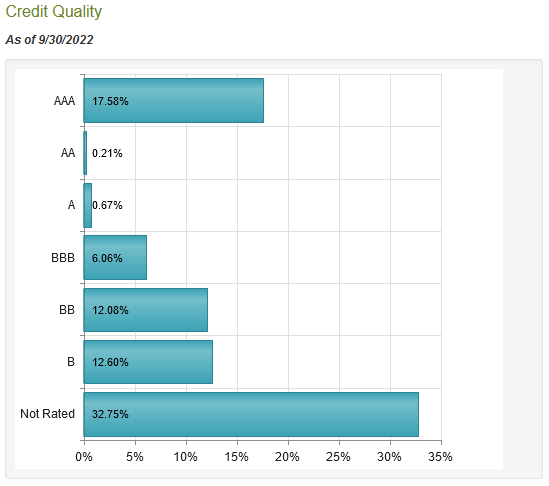

The fact that at least some of the fund’s assets are invested in speculative-grade securities may cause some risk-averse investors to pause. After all, we have all heard that junk bonds tend to have a fairly high risk of loss due to defaults. Fortunately, we have a few companies that evaluate the default risk of these securities and assign a letter-grade rating to them that ostensibly reflects that risk. Here is how the assets in the fund are rated across its portfolio:

CEF Connect

As we can see, 67.25% of the bonds in the portfolio carry ratings of B or better. As anything BBB-rated or above is considered investment-grade, that still provides a lot of exposure to junk bonds. However, according to the official bond rating scale, companies whose securities are rated BB or B do have the financial capacity to honor their debt obligations through normal economic conditions as well as short-term economic shocks. They may be at some risk of default if a long-term economic problem arises, but we have not had one of those since the Great Depression. Thus, it appears that at least two-thirds of the portfolio should be reasonably safe. Admittedly though, we do not know what the risk of those not rated assets actually is. It is certainly possible that some of those securities would have a fairly respectable rating if they were rated but it is also likely that any company with a reasonably strong balance sheet would have its bonds rated in order to save money on interest. Therefore, those securities likely represent the biggest risk of loss due to defaults that we have in this portfolio.

The fund can also reduce its default risk by investing in a large number of assets. This way, if any given company does default, its impact on the overall portfolio will be minimal. As of the time of writing, the RiverNorth/DoubleLine Strategic Opportunity Fund has 566 unique holdings. Also, it is important to bear in mind that many of these holdings are other funds or entities that will contain a significant number of positions. Thus, we can clearly see that the actual percentage of the portfolio represented by any individual debtor is quite minimal so a single default should have no noticeable impact on the portfolio as a whole. The only real risk here would be if widespread defaults occurred and if that happened, the economy has much bigger problems than a few fund holders losing some of their money.

Leverage

In the introduction, I stated that closed-end funds can frequently deliver higher yields than most other things in the market. They are also able to deliver higher yields than any of their underlying assets possess. One way that the RiverNorth/DoubleLine Strategic Opportunity Fund accomplishes this is the use of leverage. This is the reason why the fund is able to have a negative cash position. In short, the fund borrows money and then uses that borrowed money to purchase fixed-income securities or closed-end funds. As long as the yield on the purchased assets is higher than the interest rate that the fund has to pay on the borrowed funds, this strategy works pretty well to boost the overall return of the portfolio. As the fund is able to borrow at institutional rates, which are lower than retail rates, this will usually be the case.

However, the use of debt is a double-edged sword since debt boosts both gains and losses. As such, we want to ensure that the fund is not employing too much leverage since that will expose us to too much risk. I do not generally like to see a fund have a leverage ratio of more than a third as a percentage of its assets for this reason. Unfortunately, the RiverNorth/DoubleLine Strategic Opportunity Fund is above this level as the fund’s levered assets currently comprise 34.66% of its portfolio. This is admittedly not drastically above the level that I like and it probably wouldn’t be too bad except for the fact that the fund is investing in other closed-end funds, which also use leverage. Thus, the fund is piling leverage upon leverage here, which is probably the reason why it has declined as far as it did over the course of the past year.

Distribution Analysis

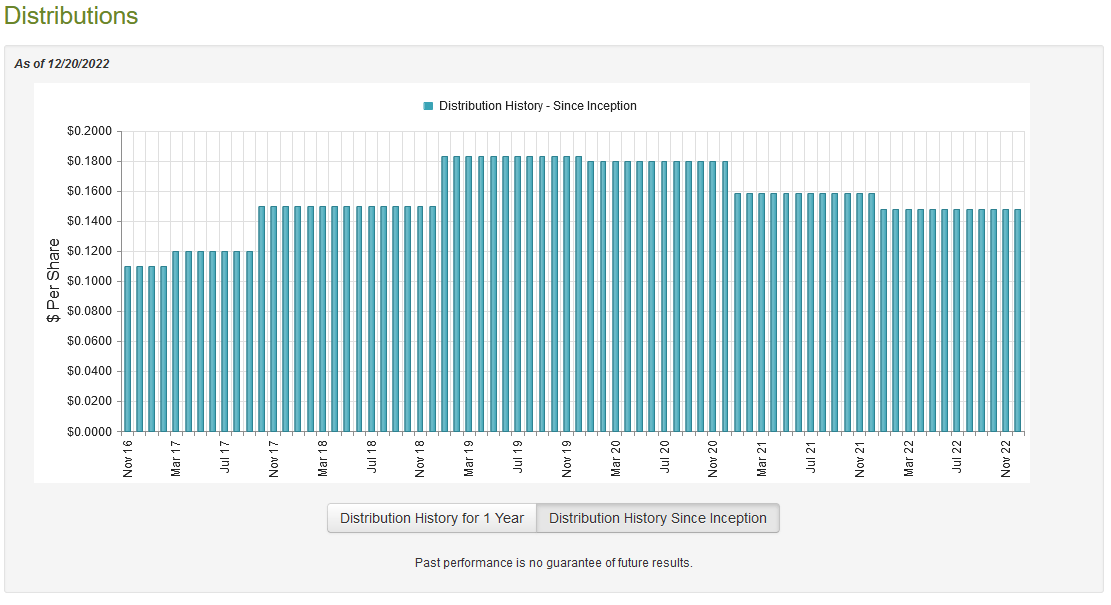

As mentioned earlier in the article, the primary objective of the RiverNorth/DoubleLine Strategic Opportunity Fund is to provide investors with a high level of current income. In order to achieve that objective, it invests in a levered portfolio of closed-end funds, business development companies, and high-yield fixed-income securities. As such, we might assume that the fund has a very high yield itself. This is certainly the case as it currently pays out a monthly distribution of $0.1478 per share ($1.7736 per share annually), which gives the fund a 19.76% yield at the current price. Unfortunately, the fund has not been particularly consistent about this payout and indeed it has varied quite a lot over the years:

CEF Connect

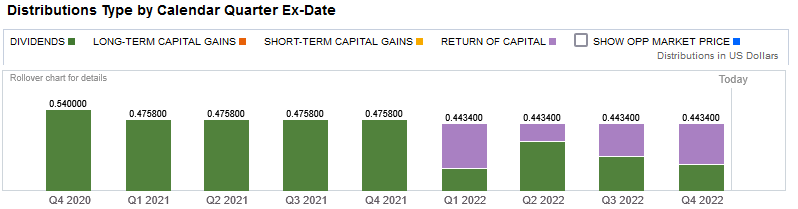

This is something that will almost certainly be a turn-off for anyone that is seeking a secure and reliable source of income with which to pay their bills or finance their lifestyles. However, anyone buying today will still receive the current distribution at the current yield. In addition, the lowest payout that the fund has ever had was $0.11 per share monthly, which is still a 14.70% yield at today’s price. Thus, even in the event of a distribution cut, it is quite likely that you would still be receiving a very attractive yield. This could be important because the fund has been making a lot of return of capital distributions this year:

Fidelity Investments

The reason that this could be concerning is that a return of capital distribution can be a sign that the fund is returning the investors’ own money back to them. This is obviously not sustainable over any sort of extended period. However, there are other things that can cause a distribution to be classified as a return of capital. One of these things is the distribution of unrealized capital gains. Another possibility is the distribution of money received from other closed-end funds that made a return of capital themselves. Thus, we should investigate exactly how the fund is financing these distributions in order to determine how sustainable they are likely to be.

Fortunately, we have a somewhat recent document to consult for that purpose. The fund’s most recent financial report corresponds to the full-year period ending June 30, 2022. As such, the report will not include any information from the past few months but it should still give us a good idea of how well the fund performed in the very volatile market that dominated during the first half of this year. During the full-year period, the RiverNorth/DoubleLine Strategic Opportunity Fund received a total of $17,995,877 in interest and another $2,798,153 in dividends from the investments in its portfolio. When we combine this with a small amount of income from other sources, the fund brought in a total of $20,801,875 during the period. The fund paid its expenses out of this amount, leaving it with $15,941,930 available for shareholders. This was, unfortunately, nowhere close to enough to cover the $33,819,415 that the fund actually paid out during the period. At first glance, this is highly concerning.

However, there are other ways that the fund can obtain the money that it needs to cover its distribution. One of these is from capital gains. As might be expected from the weakness that we saw in the fixed-income markets once the Federal Reserve started to raise rates, the fund failed miserably at this task. During the period, it did manage to achieve net realized gains of $2,894,301 but this was more than offset by net unrealized losses of $52,145,724. The fund did conduct a sale of new shares during the year, which brought in $68,214,886 but even this was not enough to cover all of the outflows. The fund’s assets declined by $5,703,420 over the year after accounting for all inflows and outflows. This is a clear sign that it cannot afford the distribution. It is not a surprise that the market expects to see a cut as the fund needs to do so in order to stem the bleeding. It would not be surprising if we saw a cut within the next few months.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to generate a suboptimal return on that asset. In the case of a closed-end fund like the RiverNorth/DoubleLine Strategic Opportunity Fund, the usual way to value it is by looking at the fund’s net asset value. The net asset value of a fund is the total current market value of all of the fund’s assets minus any outstanding debt. It is therefore the amount that the shareholders would receive if the fund were immediately shut down and liquidated.

Ideally, we want to purchase shares of a fund when we can acquire them at a price that is less than the net asset value. This is because such a scenario implies that we are buying the fund’s assets for less than they are actually worth. This is, fortunately, the case with this fund today. As of December 20, 2022 (the most recent date for which data is currently available), the RiverNorth/DoubleLine Strategic Opportunity Fund has a net asset value of $9.85 per share but the fund’s shares only trade for $9.00 a piece. This gives the shares an 8.63% discount to net asset value at the current value. This is a better price than the 6.38% discount that the shares have traded at on average over the past month so the price certainly appears to be okay today.

Conclusion

In conclusion, the RiverNorth/DoubleLine Strategic Opportunity Fund is an interesting fund that uses a somewhat unusual strategy. It invests in generally high-yielding assets in multiple categories and then leverages them up in order to boost the yield further. The strategy has backfired over the past year, though, as the fund’s leverage worked against it and resulted in a significant price drop. It appears somewhat unlikely that the RiverNorth/DoubleLine Strategic Opportunity Fund, Inc. will be able to sustain its current distribution, which could result in a cut in the near future. The price of RiverNorth/DoubleLine Strategic Opportunity Fund appears to be reasonable, though, so it might still be worth buying, especially since its yield would probably still be attractive even after a cut.

Be the first to comment