z1b

OneMain Holdings, Inc. (NYSE:OMF) is a consumer finance and insurance company that sells personal loans and insurance products through its subsidiary, OneMain Financial. These loans are sold primarily to people who do not have access to traditional financial services like banks and credit card companies.

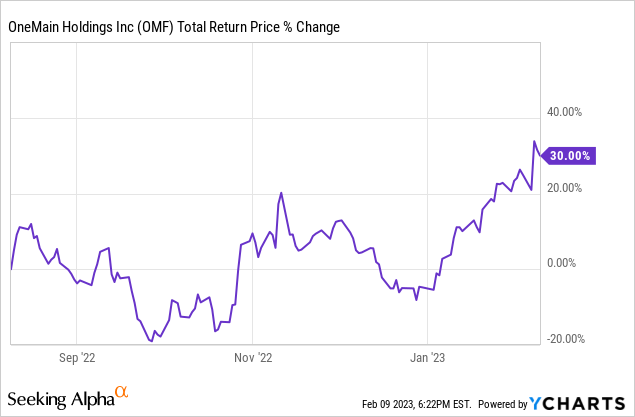

We bought OMF back on August 9th, 2022 at $35.52 because:

1. The company expects to remain highly profitable even if defaults reach levels seen during the Great Recession.

2. Their dividend yielded ~10.65% at the time and was covered ~2.5x by earnings.

3. OMF is pursuing several promising growth initiatives, including its credit card business and capturing some market share among higher credit quality counterparties as its weaker competitors have had to pull back from the market due to rising risks from the changing macro situation.

4. Despite an increasingly challenging macroeconomic environment, charge-offs remained well within management’s target range. This is largely due to the fact that – while the economy overall is struggling due to declining GDP and soaring inflation – the jobs market remains pretty strong, which is probably the single most important macro indicator for the health of OMF’s business.

5. The balance sheet remained in solid shape with a liquidity runway of over 24 months under various stress scenarios.

6. Management was putting its money where its mouth is. First of all, the company continued to return capital generously to shareholders, repurchasing 2.1 million shares in Q2, bringing the year-to-date total repurchases to ~4% of outstanding float on top of the annualized dividend yield of over 10%. Second, the CEO had been buying shares very aggressively over the past year at prices materially above the current share price.

Since then, the stock has soared higher, generating significant alpha for our portfolio in the process:

In this article, we delve more into the business and then offer our current take on the stock and how we are managing our position.

OMF Stock Overview

OneMain Holdings primarily serves consumers who do not have access to traditional lenders.

Generally, the people who the business serves have limited access to traditional financial products. They pose a greater credit risk because they have a lower credit score. These people could be considered “higher risk,” but with appropriate underwriting that accounts for their higher risk, it is clear from the business’s results that this segment can prove profitable.

This image below from a recent investor presentation breaks down what the average customer looks like for OMF. OneMain is serving middle-class, working people, and the loans are generally used to pay for one-off expenses.

Their average customer:

-

Has a checking account

-

Typically has been in the same job for 5+ years

-

Is generally employed in a stable industry

-

~$45,000 net income

-

~40% are homeowners

-

Has on average lived in the same residence for the past 10 years.

OneMain lends to working-class people. Generally, these personal loans are for one-off expenses. As a high-level overview, on average, the business:

-

Provides ~$10-15k loans

-

Lends at ~20-28% APR interest

-

Serves customers that have about a 600-650 credit score.

If you think about it, these loans are not very different from the types of loans credit cards provide. The difference is that about half of OneMain’s customers are subprime.

You can also see that the business sells a variety of optional financial products, like insurance products, home and auto memberships, term life insurance, and guaranteed asset protection.

OneMain Holdings specializes in offering personal loans to subprime borrowers. Currently, the business is pursuing a massive growth opportunity as they expand to also offer credit cards.

OMF Stock Growth Potential

Today, the company focuses on lending personal loans to subprime borrowers.

While personal loans are a strong business, OneMain expects that they can tap into a much larger market by offering credit cards.

This new growth opportunity is expected to complement their core business because:

-

1/3 of customers get a new credit card within 90 days of getting a OneMain loan. If OneMain offered a credit card, that could be an easy upsell.

-

The business already has a large pool of past customers they could offer the cards to. This past customer base would give the company lower customer acquisition costs and give OneMain visibility into their customers’ credit worthiness.

Management thinks it would be beneficial for the company to enter this space because credit card lending is a high-return industry, and there is a much larger total addressable market that the business can expand into. Cards are expected to bring in $100-$150 million in annual capital generation by 2025.

OMF Stock Dividend

Today, OneMain Holdings, Inc. offers a generous 8.7% dividend yield at current market prices after hiking the dividend by 5.3% in conjunction with their recent quarterly results.

Although this yield might seem unjustifiably high, the company has the means to safely continue paying this dividend. Management prioritizes the dividend as a part of the company’s capital allocation strategy alongside investing in portfolio growth, maintaining a leverage ratio between 4-6x, and repurchasing shares.

OneMain Holdings has paid dividends in each of the past three years and increased its regular quarterly dividend from $0.25/share in 2017 to $1.00/share in 2023. OMF generated $7.32 in normalized earnings-per-share in 2022, and analysts expect OMF to generate $6.54 in normalized earnings per share in 2023. With the dividend currently at $4.00 per share, the dividend looks safe and well-covered.

Moving forward, the combination of growth initiatives and share buybacks are expected to drive earnings per share growth, with normalized earnings per share forecast by analysts to reach $8.54 in 2025.

OMF Stock Risks

While the business has continued to grow, some near-term risks may impact the company’s performance.

Inflation can have a troubling effect on subprime customers since rising costs will make it even more challenging for customers to make loan payments to the company. Since we have not had a period of high inflation like this in decades, it is tough to draw comparisons to understand how this period of high inflation will impact loan delinquency for OMF, especially as we move into a period of weaker economic growth or even a recession.

Management has taken action to help offset some of these headwinds by increasing the strictness of their underwriting standards and the results are bearing this out. That said, earnings per share are still declining in the face of increased economic headwinds and the loss of the benefit from economic stimulus from the government that was evident during the COVID-19 era.

Overall, while this is certainly not a low-risk business as a severe recession will undoubtedly lead to significant defaults, we do not expect that macro risks will derail our long-term thesis for OMF. We expect that most businesses will face headwinds from the inflationary environment and will most certainly see a spike in defaults in the event we head into a recession, but with OMF we believe that a lot of this is already baked into the low share price and the dividend has massive coverage via free cash flow.

Even if management decides to cut the dividend in a recession (though it has explicitly stated that it has set up its dividend payout ratio in a way that they believe it can withstand a stress environment), the starting yield is so high that even a 50% reduction would still leave the yield at an attractive level on cost, especially since it would likely be increased again moving out of the recession.

Another important risk that will be important to monitor is the leverage ratio. At 5.5x net debt to EBITDA, it remains below their upper limit of 6x, but it is still pretty high, especially considering the riskiness of their underlying assets. Furthermore, they are taking out debt with interest rates in the high single digits, so clearly they are not perceived as a low-risk business.

Investor Takeaway

We like OneMain Holdings, Inc. because the company’s newly introduced credit cards are expected to be a strong growth lever (which we discussed more with them in a recent interview), and shareholders can get paid handsomely to wait on that growth with the business’s 8.7% dividend yield and significant share repurchases.

That said, we believe that the risk-reward is not particularly attractive at the moment given that we remain at an elevated risk of a recession at the moment. If a recession materializes, it is very possible that they will see a spike in write-offs on their loans. Given how leveraged their balance sheet is, this could lead to a significant plunge in earnings and – while we do not view the dividend at risk at this point – at the very least it would probably force them to abort their share buyback program in order to shore up their balance sheet.

OMF stock has seen significant downside volatility during previous periods where the market became concerned about a recession, and we expect to see this again in the future.

As a result, we are neutral on OneMain Holdings, Inc. at its current share price, sold our shares recently to lock in 53% annualized total returns and recycle the capital into a lower-risk, high-yielding stock, and would likely buy back in if the shares dip into the ~$35 range again.

Be the first to comment