sankai

EV is an obvious area for future growth, and I estimate that EV production can penetrate only 50% of the total auto market by 2030. How can investors participate in EV growth? Of course, some investors choose to invest in individual automakers like Tesla (TSLA). Another better way, in my opinion, is to invest in auto semiconductors.

ON Semiconductor (NASDAQ:ON) in the US, and STMicroelectronics (STM) and Infineon Technologies (OTCQX:IFNNY) in Europe are the main players in automotive silicon carbide. While NXP Semiconductors (NXPI) is a key player in the auto semiconductor market, they primarily provide commoditized products. Additionally, Wolfspeed (WOLF) is the main wafer provider for silicon carbide; however, they are a capital-intensive business with a weak balance sheet. Overall, I believe ON Semiconductor is the best choice in the US equity market for the automotive semiconductor space.

I estimate that the auto and industrial end-markets will soon represent more than 85% of ON’s group sales. Auto and industrial markets are the two main industries for carbide and electrification, with high-growth potential over the next decade, in my view.

Growth Drivers

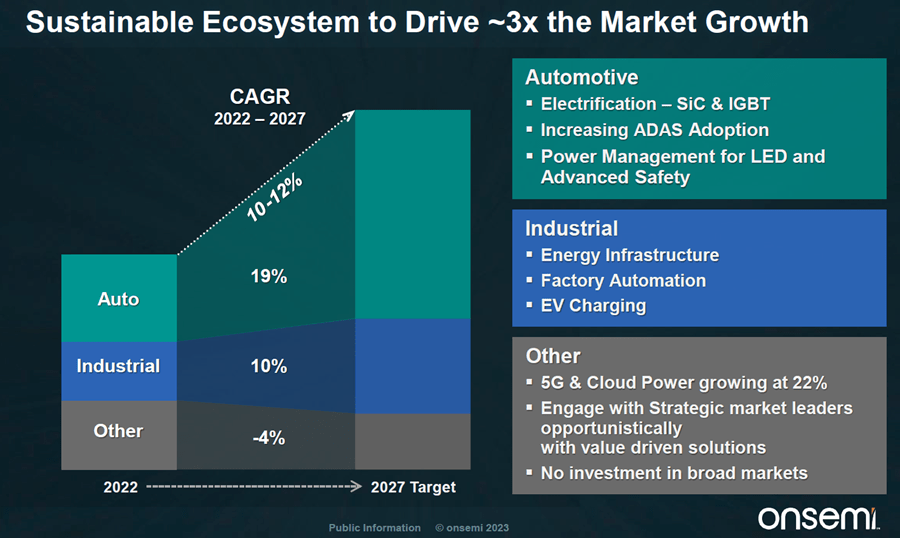

ON is targeting 3 times the market growth from 2022 to 2027, implying a sales CAGR of 10-12%. I believe the main growth drivers will come from the auto and industrial sectors. Electrification and silicon carbide ((SiC)) are the critical growth catalysts.

ON 2023 Capital Market Day

Broadest Portfolio to Capture the EV Market: From EV manufacturers’ perspective, most OEMs have multiple platforms, including entry-level, mid-range, high-performance, and ultra-high-performance vehicles. ON Semiconductor has a broad portfolio that addresses these multiple solutions, including converters, electronic power steering, e-compressors, inverters, and more. The continued penetration of the EV market is a significant growth driver for ON. Additionally, according to ON, electric vehicles require up to $700 of incremental ON Semiconductor content for drivetrain and onboard charging, compared to an internal combustion engine car. Therefore, in addition to penetration growth, I believe ON will also experience growth in content per car.

Leading Silicon Carbide ((SiC)): Compared to traditional silicon technology and IGBT, silicon carbide offers an extended range for EVs, but currently comes with a higher cost. For entry-level vehicles, IGBT is a cost-effective option, and ON offers a broad and leading IGBT-based solution. However, OEMs looking to design premium or long-range vehicles need to utilize SiC technology. ON provides best-in-class single SiC inverters. They are targeting a 70% CAGR for SiC-related solutions from 2022 to 2027. To support this, they are phasing in 200 mm SiC substrates for the next wave of EV ramps.

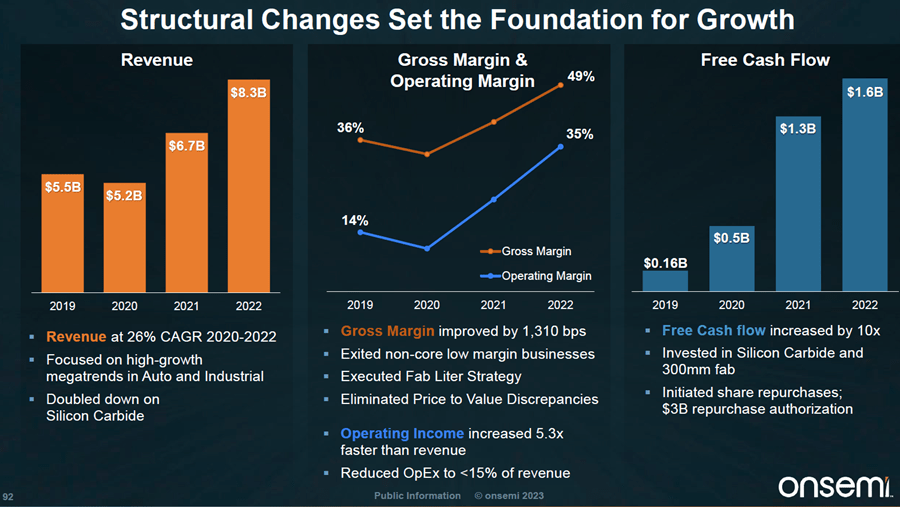

Portfolio Rationalization: ON caught my attention when they started divesting their non-core businesses and focusing on high-growth end-markets in the auto and industrial sectors back to several years ago. They have exited some low-margin and low-growth portfolios, including computing-related businesses. In 2021, they walked away from $170 million of non-core business with an average gross margin of 20%. It’s worth noting that ON’s gross margin was 49.2% in 2022. Additionally, they still have around $350 million of non-core business to exit this year. On the other hand, they are making heavy investments in SiC, auto, and industrial chips. I believe they are effectively managing their portfolios, focusing on higher-growth and higher-margin opportunities.

ON 2023 Capital Market Day

Key Risks

Cyclicality: Although cyclicality is a typical risk for any semiconductor company, we need to consider ON’s business in this regard. Automotive and industrial end-markets accounted for approximately 40% and 28% of group sales, respectively. I believe ON has less cyclicality compared to a typical semiconductor company. On one hand, while automotive markets are highly cyclical, the growth of EVs is expected to be less cyclical over the next decade. For example, while internal combustion engine vehicle sales were nearly flat in 2021, EVs grew by 94%. The growth of EVs is driven by increasing penetration, and I estimate that EV production can only reach 50% of the total auto market by 2030. Therefore, there is a significant runway for auto semiconductor chips.

On the other hand, in the industrial end-market, ON’s solutions cover energy infrastructure, factory automation, and EV charging systems. ON expects these businesses to grow at a CAGR of 10% from 2022 to 2027. Their industrial business is capturing the new energy generation and storage needs to enable the automotive transformation. Additionally, factory automation and machine vision are expected to continue growing due to macro environmental factors, in my opinion.

Other Non-Growth Business: This includes 5G & cloud power and some computer-related businesses. ON expects these businesses to decline by 4% from 2022 to 2027, and they do not have any plans to invest in these areas. On the contrary, they continue to divest some low-margin businesses, as mentioned above. These other businesses accounted for 32% of group sales in 2022. I believe ON should gradually divest from non-growth areas such as notebooks/laptops/PCs, USB, white goods, set-top boxes, etc. However, before ON divests these businesses, they could continue to create noise in ON’s earnings, in my view.

Outlook and Valuation

ON expects a sales growth CAGR of 10-12% from 2022 to 2027 and aims to achieve a gross margin of 52%, operating margin of 40%, CAPEX ratio of 11%, and a free cash flow conversion rate of 25-30%. I believe these financial targets are achievable based on the analysis above. ON is continuing to ramp up its SiC business and expects to accelerate sales to reach $1 billion by the end of the year. In the last quarter, they have already secured $17.6 billion worth of long-term supply agreements (LTSA). These long-term contracts pave the way for ON’s future growth.

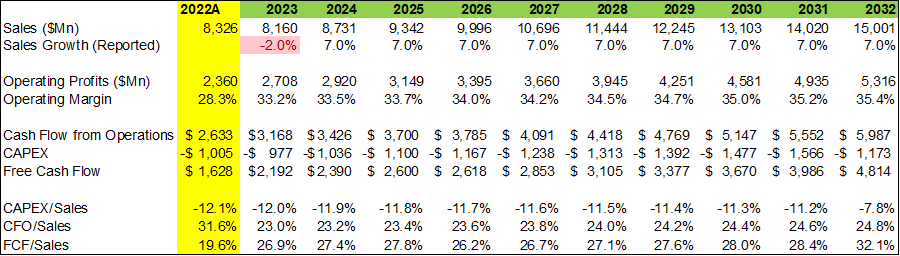

I put conservative growth projection in the DCF model, only assuming 7% of sales growth. I expect the operating margin to reach 35.4% in 2032, which is in line with ON’s guidance. The CAPEX/sales ratio is projected to be around 11% in the model. As a result, the free cash flow conversion is around 26-30% range over the next ten years as per my estimates.

DCF Model-Author’s Calculation

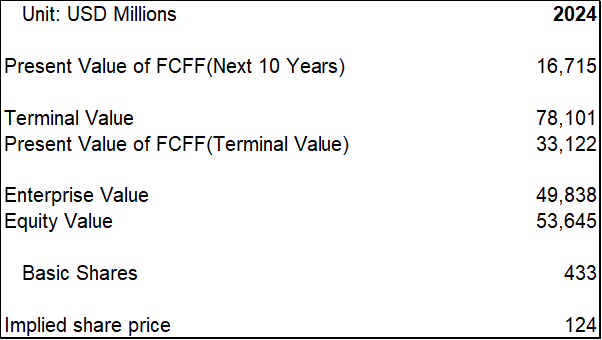

I am using 10% of WACC and 4% of terminal growth rate. With these assumptions, the present values of FCFF over the next 10 years and terminal value are $16 billion and $33 billion, respectively. Adjusting the debt and cash, the fair value of their stock price is estimated to be $124.

DCF Model-Author’s Calculation

In addition to the DCF model, I also want to demonstrate to our readers how to estimate the value using the future free cash flow multiple. According to ON’s target, they are expected to generate $3.5 to $4 billion of free cash flow in 2027. I will use the midpoint of $3.75 billion as the estimate for 2027. As a rule of thumb, for a stable company with 5-6% organic growth, the equity fair valuation is typically around 20 times their free cash flow, based on my experience. While I can’t argue that ON is a stable growth company, they are growing at a higher rate compared to the average growth company. If I use a 20x multiple, it implies an equity value of $75 billion in 2027. Considering that ON’s current market cap is $38 billion, investors should expect a compound annual growth rate of 18% in stock returns over the next four years.

Takeaways

ON Semiconductor strategically focuses on high-growth megatrends in the automotive and industrial sectors by offering a wide array of solutions for intelligent power and sensing. Simultaneously, they are actively optimizing their portfolios to reduce complexities and expand margins. They are positioned in the sweet spot of electrification and silicon carbide, two key areas driving innovation and growth in the industry. By capitalizing on these trends, ON Semiconductor is well-positioned to capture opportunities and deliver value to its customers.

I give ON Semiconductor a “Strong Buy” rating.

Be the first to comment