courtneyk

Dear readers/followers,

Omnicom Group (NYSE:OMC) was one of my Coronavirus discounts almost 2 years back – and the company has been on a great performance since that particular time.

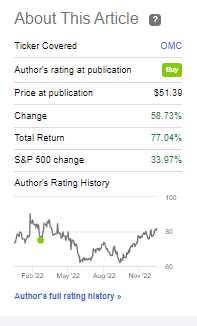

OMC article (Seeking Alpha)

This all goes with my strategy – of buying quality at cheap prices, and hold onto that quality until it’s either overvalued or while it produces excellent returns and superb dividends for you. Omnicom has certainly done that.

I have rotated/trimmed the position twice at this point at superb profits, but I’ve also bought back most of that which I sold – though at much cheaper prices. When I initially wrote about the company, I compared them to things like ViacomCBS and Meredith. Ironically enough, these companies no longer exist at their current names. My positions in them were limited – but Omnicom, together with the mid-cap company Interpublic Group (IPG) are the clear winners of my advertising investments.

Let’s review Omnicom Group again and let me show you why I believe the time has come to once again buy the business.

Omnicom Group – Timeless Advertising

Omnicom provides advertising, corporate communications services, and marketing services. It has branded networks and agencies not just in the USA, but in the entire world. The total number of services that the company offers is over 20, and here are some of the services that the company offers.

- CRM – Customer Relationship Management, Customer, experience, and executions & support/PR

- Advertising, including creative services as well as strategic media planning and data analytics.

- Corporate Communications & Crisis management, public affairs, and media relations services.

- IR services

- Mobile marketing, package design, product placement, retail marketing.

- Field marketing, experiential marketing, entertainment marketing

- Healthcare, including advertising and media services to healthcare clients.

…and others.

The company still retains BBB+ – the same it had when I first wrote about it. It never cut its dividend, not even during COVID-19, despite a 17% earnings decline for that particular year. Another dip is expected in the year 2023E. The company now has a market cap of around $16.6B and still, without spoiling too much of the valuation, trades at what I consider to be a relatively attractive share price range.

The clients are still found across the spectrum. It’s not uncommon that several of Omnicom’s agencies service different brands and product lines of the same client. The company has an incredible diversification and lack of individual exposure on a client basis, where the largest client represents less than 5% of the company’s entire revenue base and was served by more than 210 of the company’s individual agencies.

The company’s 100 largest clients, many of which represent the world’s major marketers, were no more than 51% of revenues and were served on average by over 60 agencies each.

The company was founded in 1986, by merging the then-three larger advertising conglomerates. In terms of size, it’s the world’s second-largest provider of advertising and marketing communications services across the entire world. To give you a rough estimate how many clients the company does have, it’s more than 5,000, found in over 100 countries across the globe, and Omnicom is represented across the entire world with offices in most major metropolitan areas.

Omnicom provides full-spectrum marketing services to its clients with the major focus being NA and Europe. Its 35-year-old history gives it incredible expertise here, and it has solid diversification across industries, geographies, and end segments (in terms of what its customers do).

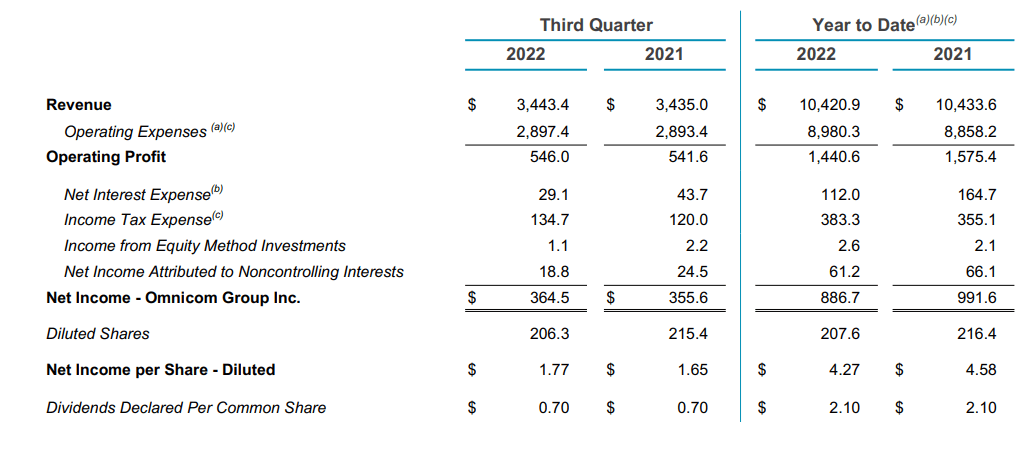

3Q22 is the latest set of results we have – at this point, these results are over 2 months old. The company’s 2020-2022 results have been a history of revenue growth, with top-line growing impressive amounts.

It did this in 3Q22 as well, with organic revenue growth at 7.5%, with growth in all disciplines and all geographies. The company expects top-line growth of close to 8.5% as a result of this.

Bottom-line results are excellent as well. Net profit is up 7.3%, and the company’s operating-level margin is intact, just south of 16%. The company’s P&L’s look excellent with nothing really “out of whack”.

Omnicom IR (Omnicom IR)

on a high level and for 9M22, we can see some increases in operating expenses, but this was to be expected – the company isn’t immune to inflation and wage increase trends.

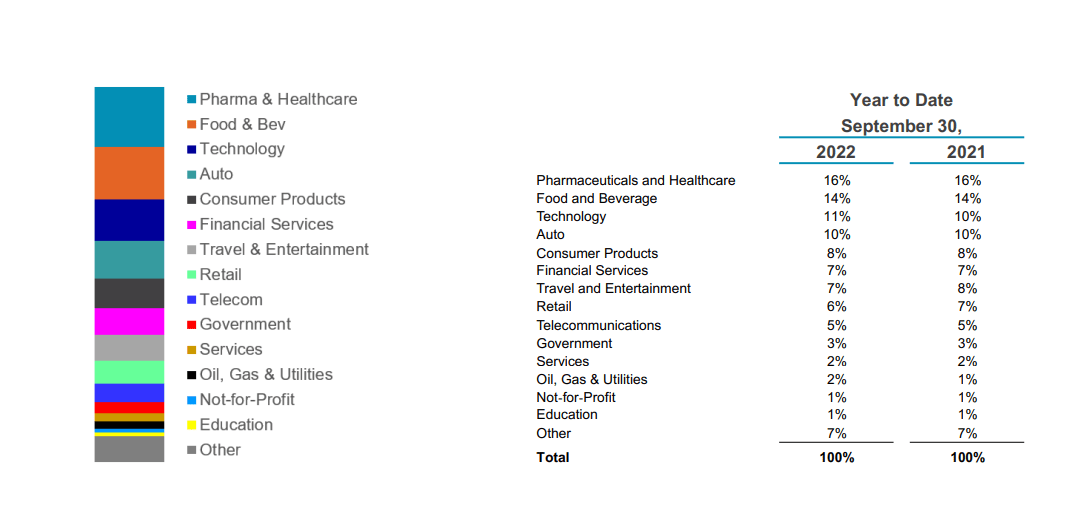

In terms of segment, the company’s revenue trends are positive in nearly every segment even when looking beyond organic growth into straight growth. Advertising & Media end segments are down 3.2%, and Experiential as well as Execution/Support are down around 7% each. Beyond that, everything is up. In terms of geography and beyond organic numbers, Europe is down the most.

Again, expected due to macro and Ukraine, with a 15.8% YoY drop, the UK down 3.9%, and APAC down nearly 7% – everything else is up. This is how the split currently looks in terms of end markets.

OMC IR (OMC IR)

OMC has been using its impressive FCF ($1.2B of it during 9M22), to repurchase shares, pay down M&As and distribute shareholder dividends. The company is one of the best-rated advertising agencies out there and has one of the lowest debts in the industry. In 2021 it was less than 0.5x net debt/EBITDA, now it’s around 0.9x – but still below 1x, with no maturities in all of 2023, and only a $750 Senior note in late November of 2024. After that, nothing comes due until 2026. Over 70% of the company’s debt is USD.

No, when it comes to OMC, I don’t see a whole lot of fundamental risks to the company. The advertising business will continue to go up and down as it always has. Certain end markets will fall, but other end markets will rise in appeal. During the COVID-19 and tech-froth pandemic, there were analysts and even contributors that seriously argued that companies like OMC would fail – and that the future of advertising lay strictly in the digital realm which would put their revenues and cash flows mostly in the hands of tech giants.

Obviously, this has not come to pass – nor do I believe it will come to pass at any near sort of future. It’s a common flaw and misconception that we can’t rise out our current circumstances and see what’s happening from a “higher” level. If more analysts had done so, I don’t believe it would have been hard to see that things, as they were a year or two ago, couldn’t continue that way for long.

For the time being, Blue-chip is blue-chip. And OMC is that – quality above quality.

It doesn’t have the greatest yield – just below 4% here – but it’s one of the safer yields in the entire industry, and that’s what I look for.

Sure, there are risks. This includes cost of digital media and advertising, which is more out of the company’s hands. There are also FX risks, and the contract structure in this particular industry isn’t exactly company-friendly – contracts are short, to the point, and open for quick cancellations.

But in the end, this is a great business.

Let’s review the valuation.

Omnicom Valuation

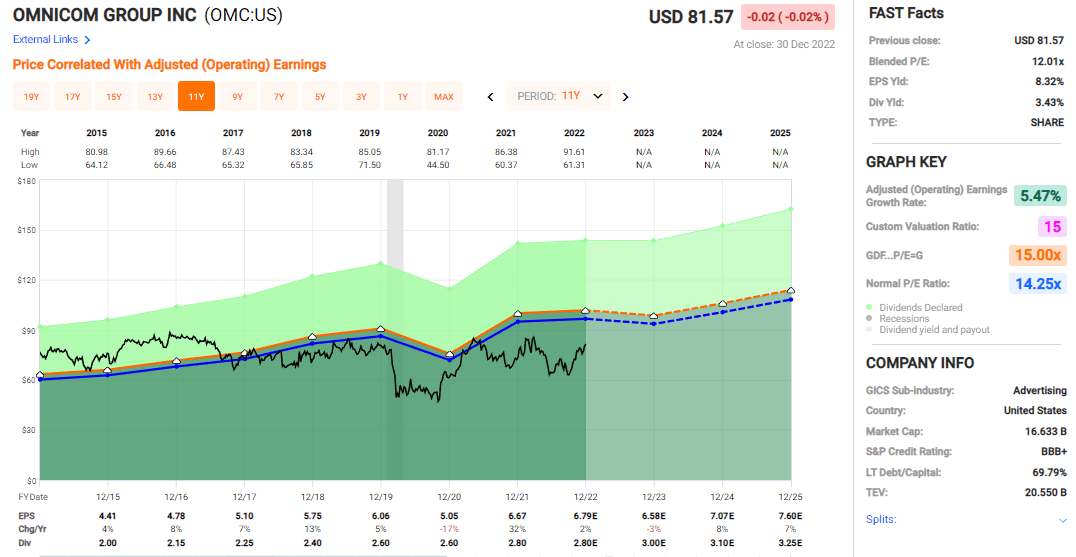

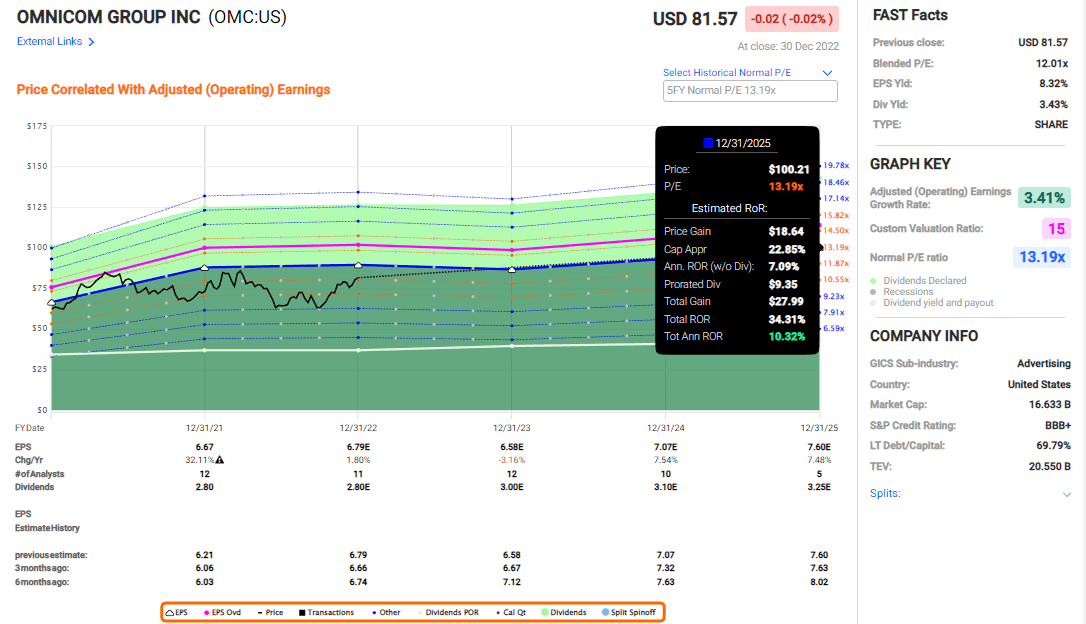

When looking at Omnicom, we can now see a valuation that trends towards up again, but that’s positive over a longer time period. Omnicom hasn’t really fully recovered from the COVID-19 drop. If it did, I wouldn’t consider it attractive any longer.

Omnicom Valuation (FAST Graphs)

But when it trades at valuations of 9-12x P/E, that’s an undervaluation not only to history, but to fundamentals and to logic itself. This company hasn’t seen a massive drop in earnings for decades (no, 17% isn’t massive). The company is volatile – it goes up and down with sudden lurches, and those trends can last for years. There was a period between 2013-2016 where the company at no point, as I see it, was investable. The troughs can last as long though – technically the company has now been undervalued for over 4 years.

Forecasting Omnicom is rather easy, as I see it. This is a BBB+ rated advertising giant with solid earnings, a good yield that’s well-covered and class-leading fundamentals. 13-15x P/E is the very least I would give this business as a mid-term valuation target. I did my last trim around the upper $80-range, which came to around 14x P/E at the time.

The company is forecasted to see a slight drop in earnings in 2023 – but only 6-7% before picking back up again, making this a low grower for the next couple of years. However, investing here still has the potential of yielding an RoR of 10.32% per year, and that’s to a 13.2x forward P/E.

Omnicom Upside (FAST Graphs)

Omnicom is now trading at the upper range of my acceptable valuation potential/targets – if it goes up another $6-9 per share, that’s when I’ll draw the line and start calling it a “HOLD”.

The street is already saying it’s gone too far. 11 analysts from S&P Global follow OMC, and they give it a range from $57 to $95, currently averaging $79.

If you recall, my PT for OMC in my last piece was $86. I see no reason at this point to diverge from this. A slight gap in EPS for the next year certainly isn’t reason enough – the potential for this was already “baked in” to my model at that point.

And despite the PT divergence, a majority of the S&P Global analysts still have the company listed as a “BUY” or “outperform” – so there’s some lack of clarity here.

Me, I say that 10% RoR per year is the least you can expect from OMC. In the case of reversal, which might happen, that annual RoR goes up to 15%, or 51% until 2025E.

Based on those assumptions, my continued conservative target for Omnicom is a “BUY” here with the following thesis.

Omnicom’s Common Share Thesis

- My thesis for Omnicom remains a positive one this time. Omnicom is a class-leading advertising giant with significant fundamental upsides across the board. I view the company as highly investable at the right valuation.

- The “right” valuation, as I see it, is no higher than $86/share to get that upside we’re looking for. Everything above that is a level where the upside is no longer intact, conservatively.

- Because that’s where we are today and the company still trades below $86/share, I give the company a “BUY” rating at this particular time.

Remember, I’m all about :1. Buying undervalued – even if that undervaluation is slight, and not mind-numbingly massive – companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn’t go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

While the company cannot rightly be called “cheap”, it fulfills every single other of my criteria, and is, therefore, a “BUY”.

Omnicom’s Options Thesis

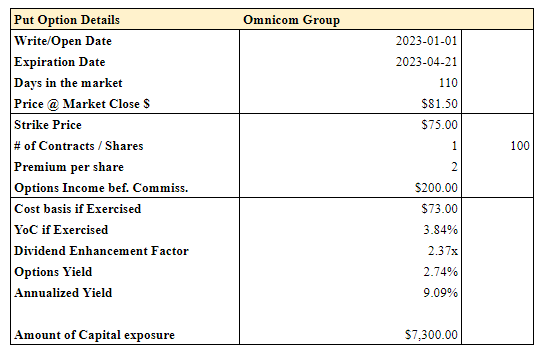

When a company like this trades so close to the brink of its PT, it becomes interesting (potentially at least) to look at the options chain for the business. While at the time of publishing markets are closed, I can still use 24-hour old data to give you an idea of where the returns for this company currently are in terms of a cash-secured PUT.

Omnicom PUT (Author’s Data)

This is essentially the best I could find at this time. I believe it to be better than buying the company outright here, but I also believe you could probably wait for a day when the company goes into the red and get higher premiums for some of these contracts, particularly the FEB -23 ones.

Still, 9% annualized is decent, and $7,300 in capital isn’t that bad compared to what’s out there. I would classify this put as “Okay”.

Those are the potentials I currently see.

Be the first to comment